As Finance Minister Grant Robertson continues to swat away calls to loosen the government purse strings, Amy Adams is reminding us those purse strings would be even tighter if she was in charge.

Adams, the National Party’s Finance Spokesperson, says if she was in Robertson’s position she’d be borrowing even less.

“If you don’t pay down debt in good times, when do you?” she told interest.co.nz.

While Treasury expects net core Crown debt to increase for the next three years – albeit at a slower rate than GDP growth – Adams says she wouldn’t be increasing debt in nominal terms at all.

Adams acknowledges her party’s position might change in the lead up to the next election, but is at this stage sticking to the line National campaigned on in the 2017 election to reduce net core Crown debt to 20% of GDP by 2020, and 10%-15% by 2025.

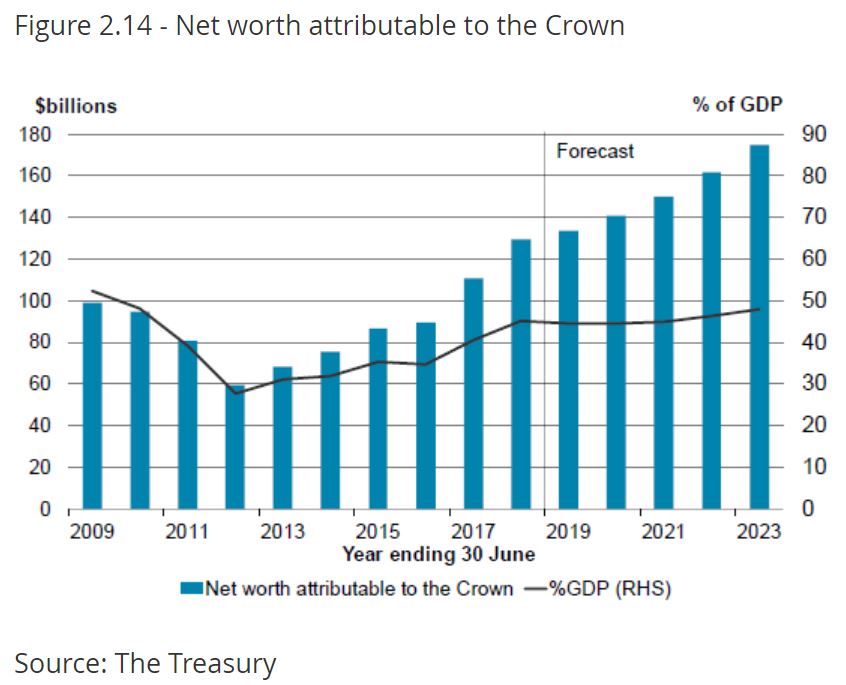

The 20% mark was hit this year and net core Crown debt is tracking to fall to 17.4% by 2023.

Adams reiterates her view on debt as credit rating agency Moody’s says the Government’s books provide “ample fiscal flexibility to respond to long-term spending needs related to social demands, or to absorb any sudden rise in expenditure to support the economy through a shock”.

NZ government debt 'significantly lower than many other Aaa-rated sovereigns'

Further to Treasury last week releasing its Half Year Fiscal and Economic Update, Moody’s says the Government’s debt levels are “significantly lower than many other Aaa-rated sovereigns”.

Asked whether his Budget Responsibility Rules, which include the goal of reducing net core Crown debt to 20% of GDP by 2022, are going too far – especially at a time borrowing is cheap and the country’s in need of infrastructure – Robertson again says no.

He recognises what Moody’s is saying about New Zealand’s sovereign debt being relatively low compared to other countries, but says it needs to be “because we’re a small economy, very exposed to the global economy and also very exposed to natural shocks”.

In a similar vein, Adams says because New Zealand is a small, trading nation exposed to global events out of our control, we must be more agile, resilient and able to fund our own needs.

“Debt head room is really important when there are crises, and crises don’t come necessarily in nice orderly amounts,” she says.

“We saw in 2009/10 not only the Global Financial Crisis, not only a private/manufacturing sector in recession, but then also had the Canterbury Earthquakes and then the Kaikoura Earthquake.

“If you go back then, debt to GDP was sitting at around 6% or 7% and actually went up quite quickly, as it should during a crisis.”

Things 'can change very quickly'

Noting GDP growth for the September quarter on Thursday coming in below expectations at 0.3% – the lowest quarterly growth in five years – Adams points out just how quickly conditions can change.

“While the percentage [of debt] to GDP might look alright at one level, when GDP starts to weaken, suddenly that can change very quickly,” she says.

Robertson has used “volatility” to frame the situation in a different way.

“While the volatile quarterly number was lower than expected due to temporary factors like the wind-down of major Kaikōura earthquake repair work and quarterly food manufacturing due to the international situation particularly in the dairy sector, there were positive signs of the underlying momentum,” he says in a media release, in which he focuses on the figures showing GDP growing to 3.0% in the year to September.

Adams concludes: “I absolutely support him [Robertson] having fiscal prudence measures.

“I think he could do a heck of a lot more though if he got rid of loose, wasteful expenditure…

“That debt is being spent because of loose poorly targeted programmes like a $3 billion provincial growth slush fund, $2.8 billion on tertiary, etc.”

Yet Robertson says: “I don’t believe I’ll be the only minister of finance in history who’s had a lot of people saying how I could spend the money that the Government has…

“It’s a balance. I recognise the importance of getting that balance right. I believe we have up to now and I believe we will in the future.”

22 Comments

Fiscal conservatism is a wonderful thing!

That luxury is afforded when the the private sector is up to its guts in debt. The big difference is that the constraints on the private sector are completely different to that of the govt. H'holds are carrying the can.

So basically J.C. in our current system, either a private or public entity needs to go into debt to create money as monetary expansion is what we deem as growth/desirable. Considering that private pays the public’s debt what the difference?

Do you think this is a good system we’re running out of curiosity if one way or another we are saddled by choice or not with debt?

So basically J.C. in our current system, either a private or public entity needs to go into debt to create money as monetary expansion is what we deem as growth/desirable. Considering that private pays the public’s debt what the difference?

Do you think this is a good system we’re running out of curiosity if one way or another we are saddled by choice or not with debt?

Not sure I really follow. Perhaps I read too much into the low public debt / high private debt trade off; but the reality is that govts are NOT constrained by debt to the same extent as h'holds or businesses. All I'm suggesting is that if private debt is destabilizing, shouldn't there be some attempt to reduce that debt? And obviously, greater public debt would go some way to resolving this.

Sorry it was poorly written and probably on a slight tangent. What I was trying to get at was the private sector pays for the public debt anyway through tax.

I think debt can be destabilising whether it's private or public as we have seen examples of both in recent history. If we alleviated some private debt by increasing public debt would we just be robbing Peter to pay Paul? The difference for me is the payment and responsibility horizons - private we pay ourselves, public is paid for by future generations.

Either way, I just think it's ridiculous that we need either public or private debt to keep increasing to prevent our system from crashing.

Agree.

Prudence and the pill? Spot the difference. Wasn’t much of a movie either.

Aggregate demand equals income plus the change in debt. So theorises Steve Keen. My first thought was that Amy Adams would run the economy into the ground if National wins the next election. Because let's face it, she is the next leader of the National party. On second thought being ultra neoliberal they'd just try selling the country again.

Dp

National takes office. Headlines then read:

"Auckland & Christchurch City Missions had to turn people away because of the demand. The missions have run out of food."

https://www.stuff.co.nz/national/109553240/city-mission-expecting-recor…

Note: Under the present government, City Missions are experiencing massively increased demand; this Christmas it is twice that of the last. Food parcels have been replaced by shopping trolleys full of stuff. My source is RNZ. This isn't in the script as it's been 15 months since the wicked National Government was removed from office. Please explain.

momentum

Sigh. All I can do is repeat my villa analogy cause property seems to be what most kiwis interested in economics focus on. Paying off the mortgage at all costs is though of as a good thing but not if you ignore the rusty roof, the borer, the crumbling foundations, the leaking rotting windows...yes you'll be debt free, but the house will be knackered and you'll have to borrow a whole lot more to fix it up. We are running excessively tight fiscal policy in NZ which is running down private sector wealth and forcing them into debt alongside tolerating general social decline.That can only go on so long before people pull back on spending.

Oh and in my analogy, government as villa owner is a bit lucky. It can always refinance itself at zero cost if it wants to and can never default. Why it doesn't use that privilege for public purpose and fix the damn roof ( the limit being capacity constraints and inflation) is beyond me. Some populist force will eventually when we are all sick of relying on food parcels...

I suggest modern monetary theory as summer reading for mr robertson.

"Because the government has the capacity to create money, it can always pay its bills and debts by printing money. But having the capacity is not the same thing as saying it should, which is the beginning of where MMT goes astray."

https://rwer.wordpress.com/2018/04/10/modern-money-theory-mmt-vs-struct…

I'd also suggest that there isn't much 'modern' in MMT, as variants of it have been about since the 13th century ( Copernicus)

https://en.wikipedia.org/wiki/Quantity_theory_of_money

Hi cs. Is there a country you would point to as a successful proponent of mmt?

Japan. Ongoing fiscal deficits- essentially financed via the bank of Japan buying government bonds - roundabout way of overt monetary finance. No inflation. Low interest rates. Close to full employment. Amazing public services. Japan has its demographic problems - but it is dealing with them well IMHO.

"Japan still to slip in the sea under its central bank debt burden"

http://bilbo.economicoutlook.net/blog/?p=40937

Do you see any ongoing issues with this? As per an article in Forbes japans interest payments will exceed tax income around 2041. What happens when the debt can’t be serviced? The bonds will be worthless and their current mode of operating will fail. It’s like the financial version of “emperor’s new clothes.”

I agree Japan’s infrastructure is good, I visited this year but like all things bought with gov debt it is enjoyed by the current citizenry and will be paid for by their children and grandchildren.

Am I missing something here? Can this system work in perpetuity?

I think that the public debt in Japan has been able to be maintained because of their sheer industrial capacity and productivity. Remember, Japan is still a net debtor to the world. They're only in the position because of their industrial output. Think about it. If NZ were to have public like that of Japan, we'd be toast.

But I do agree, it's unclear how long it can continue. MMT would argue that it could run into perpetuity as Japan effectively could never run out of money as a nation with its own sovereign currency.

If I were a betting person, I would bet that that debt will always be serviced regardless of tax income and that the future generations will do nothing but benefit from the infrastructure their predecessors have left them. The Japanese will continue on their merry way doing their own thing and not listen to mainstream economists.

And in the process they have fantastic things like a universal school meals programme with very healthy food and low childhood obesity. (Unlike here). Giving your future generation health is more important than worrying about financial debt.

It will continue because it is functional - the government is deficit spending to offset the private domestic sector's saving desires without spending so much it causes rampant inflation by hitting capacity constraints.

Anyway, time will tell I guess!

Well in the case of Japan, the public debt is largely owed to their own citizens.

I won't debate whether that is really as important as some believe - foreign savers, domestic savers, they both need to park their wealth somewhere if they are net saving in your currency.

It is pertinent to remember that the BOJ owns a giant chunk of the Japanese public debt. So the government owes itself in a currency it can create. Why would you ever bother paying off such a debt to yourself if it was going to cut aggregate demand and cause a recession? If there is no inflation from the fiscal deficits and the money is well spent for public purpose why would you worry?

Fiat money needs not be seen as a scarce resource like gold but rather as a useful social technology to further public purpose. From the POV of the state, its the outcomes of the use of it that matter, not the accounting.

Now I really am giving up interest.co.nz for Christmas! Have a good one.

There is much to agree with Mr Palley on - his heart is the right place about the use of fiscal policy - and some "structural Keynesianism" in action would be fantastic at this juncture.

But I'd like him to explain Japan - "the place where mainstream macro goes to die."

For what is new about MMT read this:

http://bilbo.economicoutlook.net/blog/?p=34200

At the risk of repeating myself, deficits are not financially constrained in a country like NZ but they are constrained by real resources and inflation.

I will not bore everyone again with my views further, but MMT is worth a read. Merry Christmas!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.