Here's our summary of key economic events over the long holiday weekend that affect New Zealand, with news that global manufacturing indicators have turned quite positive.

First in China, their official March PMIs have set a bullish tone to start the week. Their official factory PMI rose to 50.8 from 49.1 a month earlier and export orders also recovered. The official services PMI rose to its highest since June. These were followed by the private Caixin factory PMI and that broadly confirmed to improved outlook and new expansion, actually a 13 month high.

This apparent recovery energised the Shanghai stock exchange yesterday.

In Japan, industrial production fell and their jobless rate rose, both not expected. But that data was for February. For March, their central bank sentiment survey of mostly large businesses remained broadly positive.

And in South Korea, industrial production rose and by more than expected.

Back in China, the slow motion real estate sector crash rolls on with more troubles at both Vanke and Country Garden. It is more than them of course. And banks that responded earlier to Beijing's call for them to support the sector are trapped in growing bad loans. Asset quality pressure is "immense" said one major bank.

In India, we should note a new ILO report that shows the jobless rate for Indian graduates at home was a massive 29%, almost nine times higher than the 3.4% for those who can’t read or write. The unemployment rate for young people with secondary or higher education was six times higher at 18.4%. This data reinforces David Hargreaves point that even if New Zealand's local labour market struggles, it will still look attractive to Indian immigrants. It isn't our attractiveness that draws them, it is the job pressure at home that pushes them out.

In the US, the widely-watched ISM factory PMI has been shifted into expansion mode on the strength of new order levels. It joins the internationally-benchmarked S&P Global (ex-Markit) one which already moved to expansion the previous month. But it was the size of the ISM shift that got market attention, enough that the view formed it will keep the Fed from cutting any time soon. Both showed prices are no longer falling.

It is not all good news in the US. 'Extend & Pretend' is back, especially in US commercial office markets and particularly for office buildings. The US Fed is on watch for financial stability risks although they claim it is an issue for small and mid-sized banks, not the systemically important big banks.

Twenty percent of all commercial real estate loans on the books in the US face deadlines for repayment this year. That is a massive NZ$1.5 tln or nearly four time New Zealand's GDP, ~75% of Australia's GDP. But coming on the heels of a dismal 2023, when hundreds of billions of loans coming due got short-term extensions, experts are on high alert that 2024 may not go better. More specifically in one corner worth watching, more than US$17 bln of commercial mortgage-backed security (CMBS) office loans are coming due in the next 12 months, double the 2023 volume. And three in every four of those could be hard to refinance.

And staying in the US, Fed Chair Powell said that PCE inflation data for February was along the lines of what the Fed wants to see and broadly expected. However, the latest readings aren’t as good as what policymakers saw last year and the Fed can wait to become more confident before cutting interest rates. In fact, he said policymakers don't need to be in a hurry to reduce borrowing costs. The Fed's base case is for inflation to come down but if the base case doesn't happen the Fed would hold rates where they are for longer, he said. Today's PMI's reinforce that position.

But he was responding to PCE inflation data for February which rose +2.5% and that was following a January 2.4% rate and a December 2.6% rate. Core PCE inflation rose 2.8% after being 2.9% in the prior two months. Powell and his colleagues won't be unhappy with these levels but they aren't seeing downward progress either.

Meanwhile American personal incomes were +1.7% higher than a year ago and personal consumption is +2.4% higher on the same basis. This is the first time income growth trailed spending growth in a long time. It is too soon to know whether this is a turning point, or just a data blip.

However US Q4-2023 economic activity came in +3.4% higher (real) in their third and final 'estimate'. This was better than the prior estimates and means the US economy is running at an annual rate of US$28 tln, nominal, and of course a new record high. With IMF estimates that the world GDP hit US$105 tln, the US accounts for 27.6% of that. The US grew +US$1.5 tln in the year, the world +US$5 tln, so 30% of the global growth was from them. ($870 bln on expansion was from China, half the US level.)

So perhaps it will be no surprise to know that the University of Michigan sentiment index rose more than expected to its highest level since July 2021.

In Australia, inflation expectations, which had been stuck at 4.5% since December, actually slipped in March to 4.3%. While this may be its lowest since October 2021, it does emphasise just how sticky Aussie CPI inflation has become.

Meanwhile, China has dropped its tariffs on Australian wine after years of sanctions that crippled the billion-dollar export industry.

The UST 10yr yield is now at 4.33% and up +14 bps from the end of trading last week. The key 2-10 yield curve inversion is less at -37 bps. And their 1-5 curve inversion is also a lot less at -75 bps. Their 3 mth-10yr curve inversion is now at -106 bps and significantly less as well. The Australian 10 year bond yield is now at 4.00% and unchanged. The China 10 year bond rate is up +1 bp at 2.32%. The NZ Government 10 year bond rate is now at 4.64% and unchanged.

Wall Street has opened its week down -0.3% as it seems the Fed rate cuts may not come soon. Most European markets didn't trade overnight. Tokyo ended its Monday session down -1.4%. Hong Kong didn't trade, but Shanghai was up +1.2% on the bullish PMI data. Of course neither the ASX nor the NZX traded yesterday.

The price of gold will start today firmer by +US$7 from yesterday at US$2240/oz, but -US$26 below its new all-time high reached over the past 24 hours.

Oil prices have risen +US$1 to just on US$84/bbl in the US while the international Brent price is now just over US$87.50/bbl.

The Kiwi dollar starts today at just on 59.4 USc and -35 bps lower than this time yesterday. Against the Aussie we are unchanged at 91.6 AUc. Against the euro we are holding at 55.4 euro cents. That all means our TWI-5 starts today just on 69 and down -20 bps from this time yesterday.

The bitcoin price starts today softer at US$68,671 and down a sharpish -3.7% from this time yesterday. Volatility over the past 24 hours has been moderate at just on +/- 2.4%.

Daily exchange rates

Select chart tabs

The easiest place to stay up with event risk is by following our Economic Calendar here ».

79 Comments

I think we are diverging from the US. We had a bigger stimulus, with less price efficiency, and therefore a bigger crash is coming, hence Labour arranging for GR to not be in opposition and a visible target when the bill comes due. It's going to be a rough winter. Batten down the hatches, folks.

The crash is coming because:

- Higher rates in NZ do actually suppress demand (unlike in the US)

- Labour (and now National) Govt throttled spending

- We are running a trade deficit, which drives offshore savings in NZD / NZ bonds

When net bank lending + deficit spending slows for any length of time, we go into a recession. It's the same for any country with a trade deficit.

We will now see unemployment climb and welfare spending increase but that won't be enough to stop continued job losses and escalating pain until either private debt starts climbing aggressively again, or govt starts spending big (including secret spending through PPPs).

I follow your comments, and tend to agree with the overall "theme" of them (if only because through anecdotal observation, for example, I can see clients I work with who were generating good work via participating in government projects now having that revenue stream dry up, and turning to laying off staff or reducing their expenditure in other ways).

However, if "big spending government = good" why ever bother with even the smallest amount of restraint in terms of public spending? And surely some enterprising government would have figured out this "cheat code" and just spent like there's no tomorrow and we would be living in economic paradise because of it (and they'd probably get voted back in forever and ever amen). Like why not start building high speed rail between main centers, and a new hospital in every city, and give anybody who wants a government job a job on a big salary, because presumably the government could if it wanted to do so, and if what you're saying is right there'd be no downside to it?

I ask this without the slightest hint of facetiousness or sarcasm by the way.

"I ask this without the slightest hint of facetiousness or sarcasm by the way." I would never have guessed!

Not sure if you're taking the piss or not, but I am genuinely interested in the answer here. In case my username doesn't give it away, my intellect is on par with microbial lifeforms found in the bottom of ponds.

Concepts like counter-cyclical government spending make perfect sense to me (as a government has levers it can pull and buttons it can push that private enterprise doesn't) but surely if ramping up public spending is the easy way to achieve good economic outcomes, then that would be more "self-evident" in terms of what the average pleb out on the street experiences.

I'm not doubting the theory so much as wanting to understand the practical impacts, that's all.

No sarcasm perceived!

Just turning Govt spending 'up to 11' is a pretty terrible idea. I think there are three big reasons (these apply to countries with a sovereign currency like NZ)...

- Look what happened to Labour when they came to power in 2017. They thought that they could just increase the budget and make houses, supported accommodation, community mental health services etc appear out of thin air. Govt can only buy what is available to purchase. That is not to say that Govt can't invest in extra productive capacity (to increase supply) but when they start out-bidding the private sector for real resources there is a real risk of inflation (building materials costs in 2019?) Similarly, if Govt just start 'giving everyone money', they will push demand above supply, and, again, you have inflation risks. In wartime, Govts requisition whole supply chains and use rationing to reduce that inflation risk, but that is pretty unusual thankfully.

- When Govts (or commercial banks) pump money into an economy with a trade deficit, consumption of imported goods increases, and the trade deficit starts to blow out (see NZ here). This leads to increasing offshore ownership of domestic currency and Govt bonds. This erodes a country's monetary independence, leaving them vulnerable to a run on their currency if markets perceive it to be over-valued. RBNZ are preparing for this scenario now because they will have to drop rates before the Fed.

- High Govt debt + high interest rates lead to an ever increasing flow of Govt interest payments into the economy, which work against any central bank efforts to use those higher interest rates to reduce demand in the economy. Higher interest payments could theoretically drive a mutually reinforcing 'debt doom loop' - interest payments > bigger deficit > more interest payments > bigger deficit etc. Obviously if a country has a smart central bank, no issue with excess demand / housing ponzi, and a trade surplus (lowers risk of a currency run) then they can just drop interest rates to avoid this risk. See Japan for the last 20 years.

Anyhow, my view is basically that Govt spending and the deficit should 'float' at the level required to keep demand in the economy at the level required to maintain full employment, build / maintain infrastructure, and invest in the future (education, R&D etc). This would require a much more strategic use of policy and taxation - to ensure that money is kept moving within the domestic economy and not used to inflate asset bubbles. But, that's another story.

Ok thanks for the explanation. That makes sense to me (the concept of the spending 'floating' to achieve a certain outcome). This is as opposed to what we seem to be stuck with at the moment, which is an ideologically/politically-driven game of 'govt spending always good, irrespective of outcomes' from Labour/Greens, or 'govt spending always bad, irrespective of outcomes' from NACT.

Kiwibuild should have been:

- Trades training/apprenticeship scheme targeted at school leavers/beneficiaries

- Investment in on shore manufacturing capacity

The houses could have been built using apprentices with oversight from retired qualified builders (extra pocket money), just not 100k in 10 years that's a ridiculous number.

Sensible ideas from my perspective. As you say, the initial goal was always too high and perhaps Kiwibuild should really have been positioned as a program/policy of "building NZ's capability to build" by upskilling school leavers, by reducing dependency on imported materials etc.

The upskilling aspect interests me, as a general trend across all industries seems to be that nobody wants to take on the risk and cost of training Kiwis (either young, changing career pathway or unemployed but wanting to work).

I had breakfast with a sort-of competitor last week, and he straight up said his company will no longer hire anybody entry level under any circumstance and that he expects his competitors or industry peers to take that hit, or he will just import staff from overseas who are already sufficiently skilled (his reasoning being that a lot of younger hires don't have much in the way of loyalty ... I suspect there is an element of that needing to be a 'two way street' of course).

I understand the growing reluctance among employers to train Kiwis, especially in engineering and trades. Attitude is also a major reason, given the typical school leaver isn't exactly the professional, go-getter kind.

Hard to even expect decent productivity out of university grads in many workstreams to be honest, with the scales so heavily in favour of grads.

Funny that comment. You expect a graduate to have senior engineering professionalism without any training or receptive community in their company. Do you even know what engineering professionalism entails because a lot of that is the ongoing training and peer mentoring standards included (also as part of good project management and governance).

In case the professional standards try reading up on them, we have several professional standard orgs that NZ engineers apply and register too (both local and international). Then we get to the codes of ethical conduct which have many public reporting requirements of failures which many NZ companies are known to rather sweep under the rug and ignore. To the point it is the NZ company managers that are failing the industry. Often shown in the churn and low approval of experienced staff.

Often staff from overseas have less experience of modern competencies then the graduates but it is a continual lower pay in comparison to inflation that is the benefit of hiring them. Just remember you also have to provide continuous training, peer mentoring and improvement of them as well.

I agree with the two way street mention. Loyalty gets you nowhere these days when you can change jobs every 2-4 years and add anywhere from 20-40% each time to your salary plus negotiate better conditions into the contract. I wish employers would see that investing in their staff can keep them on and benefit them longer term, but sadly this seems to be the way of the world out there when looking at entry level roles. Employees will leave if they feel they are not valued or have better options to develop elsewhere when their role stagnates. Retention should be front and centre focus for any organisation that relies on skilled employees that take time and effort to get to full capacity, which has been a struggle in certain areas such as govt dept's with all of the salary hikes since 2020.

This.

It is common in engineering that the move every couple of years is to get the expected pay rises and increases in benefits that previous companies fail on. With the more experienced staff taking with them all the keystone knowledge to keep the company working in the background. New hires fail exceptionally (those from overseas are especially of the lower skill low pay end and fail much faster) and lose traction when they do not have the experience and operational knowledge. However it is always funny to see that companies that have rats leaving the sinking ship have a rapid exponential crash as significant employees pull out. In NZ tech this is part of the grind and why NZ has exceptionally low quality tech projects, billions lost to tech project failures, and super low tech productivity. Faithful loyal employees who started with a company from the old guard often take a lot of complete BS from managers, (worthy of many ERA winning cases), before they budge but they rapidly do once they see how green the grass is. With recruiters doing calls to staff almost daily and SM sites publishing employee reviews and pay comparisons there is even more visibility of the greener grass nowadays. Add to that in tech we are competing with international companies offering full WFH with added health insurance support and paid travel. NZ is quite backward and while all in engineering can say they early on had experience with the few major companies most left them quickly.

Whereas health is a grinding path of terrible work conditions and low pay to get enough experience to move overseas. If you haven't left for overseas either there is something restraining keeping you here e.g. family commitments, extreme poverty, or you don't have enough experience yet. In NZs health sector the biggest crisis is the staffing failures and trying to plug the holes with new people (complete mugs either with low work experience or new to NZ or those who see NZ as a stepping stone to elsewhere). Often those who don't know how terrible the industry is and how poor the pay is in comparison to the cost of living & housing.

Any govt jobs are a cash cow though where consultants & managers can fail upwards continuously with no repercussions and easy benefits. It is easy to see why the employee numbers for govt depts (local & national) are booming with the costs excessive, the failures quite costly and embarrassing, and why they fight so hard in media to retain and increase the amount of the easy unskilled work that obviously outputs from them. Pay increases in depts for admin, consulting and management are prioritized above that of frontline staff (hence the exodus of the frontline staff in health and engineering).

100% this. The metric for success shouldn’t have been houses built but improvement in our capacity to build houses.

We need a lot more quantitative analysis on cost benefit for longer term projects. Let’s work out the GDP improvement for increasing the average speed cars travel on roads by 15%. Let’s work out the fiscal improvement getting 1 family off welfare and hence providing income to the government rather than cost. Let’s be specific on the benefits of keeping kids at school in terms of their contribution to future government revenues from tax. How much productivity is gained with a better health system if we have less absence from work. Once we see a dollar value to these issues then investment can be made. With the data we now have and with the level of computing sophistication via AI and programming this isn’t as hard as we want to think.

100% agree!

We have that data and reported on it frequently to all those measures. This has lead to endless cycles of "reviews" that get ignored and promptly shelved for the next review. The data is there, it is often publicly available and held with several orgs. The general public people just don't see it and have trouble absorbing data and numbers itself. Then on top of that the review process with no actions or outcomes just leads us to govt dept clusterfk that never ends. The govt dept review process being equivalent to a pig at the trough eating its own sh.t or to a human centipede.

"We have 44% more Ministers, 282% more portfolios and 156% more departments than countries of similar size"

https://www.kiwiblog.co.nz/2024/04/the_complex_and_bloated_executive.ht…

For some reason they didn't share the NZI structure diagram showing the true scale of the mess:

https://www.nzinitiative.org.nz/reports-and-media/reports/cabinet-conge…

Jfoe, you really are an absolute gem. Taking the time to explain it in a NZ context is way beyond the call of duty.

I'd have just said "Hyperinflation" and posted a link. https://en.wikipedia.org/wiki/Hyperinflation

yes, I too appreciate his comments.

my view is basically that Govt spending and the deficit should 'float' at the level required to keep demand in the economy

Reminds me a little of the ideas of Dierdre Kent (https://deirdrekent.com/). Insofar as I recall the basic idea being that the role of creating new money should be limited to government and matched to economic growth.

The US is doing it right now

And the mega-rich are hovering it up.

It’s about the quality of that spending. For example the Ferry upgrade was expensive but necessary. It would have given short term stimulus and long term economic value. Same with building schools. A lot of stuff national is cancelling to save money will have to be done later at higher cost so you miss out on the short term stimulus and long term infrastructure benefits.

Some of the public service cuts - biosecurity, police, courts, prisons, inevitably health, strike at areas that are valuable to people. The biggest lie the right told was that labour had wasted money. Most of the money labour invested went into things that are important to you. Cutting comms jobs and the Ministry of Pacific Peoples is small bikkies.

The Clifford Bay ferry terminal looks really cheap right about now, thanks Gerry.

The cost/benefit case didn't quite stack up at the time. Worth another look now tho.

That said, it provided bigger ROI than many of the "roads of national significance" that the NACTF threw our money at.

why ever bother with even the smallest amount of restraint in terms of public spending?

For a start, not all spending is of the right type. Also, many are ideologically opposed to even the right type of spending because they view it as impinging on private interests and discount the value of government providing infrastructure to support productivity.

The RB must cut rates to a new base holding level ASAP. We cannot maintain our cash rate with the US Fed Funding Rate and we can not wait for them to cut!

The RB can not commence an easing cycle because that would crash our dollar and inflate asset prices again. What is required is an immediate reset to a more sustainable holding level for our OCR.

The longer the RB waits to cut, the bigger the easing will need to be and the greater the fallout to our dollar and to our asset prices.

I'm not sure what you're saying? On one hand you write: "The RB must cut rates to a new base holding level" and in the next paragraph you write: "The RB cannot commence an easing cycle because that would crash our dollar".

What do you mean by "a new base holding level" ?

Makes perfect sense to me.

1st para - what the RBNZ should be doing

2nd para - the reason many believe they are not (and they themselves have hinted as the reason)

3rd para - what will happen because they're not doing what the should be doing

Sorry, I understand the confusion...

The predicament the reserve bank are in is that they have painted themselves into a corner and can not commence an easing cycle for the reasons spelled out. However they have increased the cash rate too high where it is not sustainable so they must cut it. Conundrum?

I don't see any other option available to the RB except to cut rates as a one off with a commentary saying that this is not the start of an easing cycle, and it is just bringing the OCR back in line what they perceive to be a long term sustainable level.

Thanks for explaining, I get you now. A one-off drop in the OCR is an interesting idea, but not one that a I believe the RB will consider seriously.

I agree with you 100% as that would require our good friends at the RB eating humble pie and accepting they overcooked the tightening... however, I just don't see any other practical option.

The longer they wait, the worse their situation (and ours) gets.

What do you think they should do? They can't hold without massive downside risk and they can't start an easing cycle without obvious risks communicated on this board.

hmmm...

So New Zealand has to move into trade surplus. Along with all the related things Jfoe describes with his double entry accounting.

Hard to do, but we are not helpless. Let's get to work.

Thanks (I think). Yes, I think we need to get into trade balance / surplus. There are of course two ways of doing that - increasing exports or reducing imports. I think we should lean more towards the latter,

Hard to rebalance our trade account with our people imports running at such high numbers.

Every worker (plus dependents) moving here to work for anything other than in export businesses is increasing our trade deficit, given almost everything consumed by people here other than basic food items have to be shipped in from overseas.

Targeted migration and investment policies could help but there is complete lack of interest from all sides of our political spectrum.

I wonder how many of these new people are sending money back home to families (remittances). I need to have another look at that. Probably another small hole in our trade imbalance.

The largest hole by far is Oz owned banks remittances to their parents

We have proven over the last 4 decades or so that we are incapable of the former to any great degree therefore the latter is the apparent path...however that is likely to require regulation/disincentives which may not be politically viable....that is until all semblance of choice is removed by the markets.

"There are of course two ways of doing that - increasing exports or reducing imports. I think we should lean more towards the latter, "

Nothing like cutting the OCR, having the NZD tank, and having imports become way more expensive to achieve that outcome ... ;-)

Over time - it would reduce the trade imbalance with less interest flowing overseas to lenders. (And with some pending changes - less profits flowing to overseas banks.)

One of the great things about having a floating currency, ay!?!

"One of the great things about having a floating currency, ay!?!"

Only great if you have the ability to function with said reduced import capacity....the briefest examination of the NZ economy reveals we are not.

Dunno about that.

We've continued functioning before when there has been other sharp drops in the NZD. And we've often emerged out the other side in better shape than we were in before, albeit the NZD was worth a tad less.

If we want long term appreciation of the NZD - we've got a huge number of very big changes to make.

"Dunno about that."

Apparently not.

Consider the effect of NZD @0.39 USD as it was in 2000....theory would suggest that exports would increase and local industry would expand due to increased price competitiveness....did our export base expand? did we increase our local capability?...indeed the opposite happened, our local capability continued to decline and our exports consolidated. Instead we embarked on the folly of expanding our money supply through real estate....and witnessed the entrenchment of inequality within the NZ economy.

Now the housing ponzi appears to have reached its limits.

A floating exchange rate is a fair weather friend....it is useless in a storm.

it has long been held that to balance trade over time your currency needs to move in flux with that. the NZD at the moment should probably really be at < 50cents to reflect the imbalance and that the weaker dollar will make us more 'competitive'.

it would mean a short-term spike in tradeable inflation, but unfortunately any drop in the OCR won't be put to productive use. the fixation with investing in housing over productivity is our biggest hindrance.

it's part of the reason the US will forever into the unknown future struggle to run trade surpluses as the strength of their currency, along with others holding USD to deflate/peg their currencies to maintain their trade surpluses.

"it would mean a short-term spike in tradeable inflation, but unfortunately any drop in the OCR won't be put to productive use. the fixation with investing in housing over productivity is our biggest hindrance."

LVRs and soon DTIs. If the RBNZ really wants to they can cure the fixation real fast. Do they want to though? (They should want too. The inflated value of houses in NZ is a serious 'financial stability' issue.)

Likewise government has the levers but they're either too weak and/or too ideologically driven to ever use them.

There are lots of ways of cutting the amount of money flowing out over the border. Some not commonly discussed.

Just one is the "ownership technique".

Somebody below pointed out the big outflow of the big four Aussie Banks. So that would change if we bought them. Or even if we bought the Aussie based portions as well we would get an inflow. (acknowledging many here own bank shares already)

Not talking about nationalising. But if New Zealanders owned their own stuff, our balance of payments would increase.

Hard to do, as individuals would have to generate a surplus, and invest it. Not been the kiwi way - so far. But we can.

Furthermore, Bank balance sheets are flat to contracting

Yes, another 'is it 1991 or 2009' graph!

Bingo!

I really think that whenever the government enters a PPP, the contractually obligated payments should immediately cause an equivalent amount of debt be added to the official government debt figure.

PPPs these days rarely have any risk for the private enterprise and are mostly a method of hiding government debt so that a government can say they have been fiscally prudent while locking future generations into repayments just like plain debt does.

As far as I understand it, that will be the case in NZ unless National mess with the rules. If they come up with a workaround to avoid the debt being appropriately counted, they should be shamed!

Really?? So e.g. transmission gullys PPP private sector debt is included in our national debt figures?

https://www.nzta.govt.nz/projects/wellington-northern-corridor/transmis…

Aye nkt, GR and others are no longer. It would be really good if TVNZ ran a series of that old TV show “Where are They Now” for our exited politicians. We the viewers, the Fukawi tribe, would be interested to know, likely to lift those ratings too.

Growth is a runaway train, and there is always a peak and a down-side when it's physical.

Don't blame either team of alternating drivers - they aren't the train. That misidentification stems from misidentifying the problem as a non-physical one. Note the graph in the growth/debt thread; the world trend. Extrapolate it, even linearly.

There's the problem. Nobody could have done 'better' than Robertson, given the circumstances. To have done really better, he would have had to accommodate increasing degrowth; no pollie can do that, given the ignorance of most voters.

The runaway growth train is the choice of politicians but not because of the ignorance of voters. The less educated voters and the more elderly voters are generally in favour of the status quo or a return to a less congesed past - it is those such as the Greens and labour representing the young, educated voters (that is an academic not real-life education) who want to speed up the growth train with ever more immigrants because they are essential to provide services for the previous wave of immigrants. NZ politicians are more influenced by the opinions of who pays for their political party than those who actually vote for it.

There is no doubt that the average voter is not especially bright, but considering Dumbthoughts comments above (despite the obvious sarcasm) I suggest it is possible for a government with a vision (not poking around with a white cane like most do) to spend a deficit budget to create efficient infrastructure with a planned population decline, and a national resilience plan to support economic and environmental sustainability.

DTs comment re the government employees is really less about the government itself, but the empires created within government departments at their respective national offices. It is those empires which bleed resources from the front lines of those departments by having significantly too many over paid drones not doing one jot to help those departments deliver the frontline services they are actually paid to deliver. That is where most government wastage occurs.

We had a bigger stimulus, with less price efficiency, and therefore a bigger crash is coming

Along with Canada and Australia, we largely avoided the post GFC crash in our property market. Relative property prices got kind of absurd to the point that you could buy a large cliff top piece of land in Hawaii for the same price as a lot in a subdivision in Alice Springs! At the time I remember thinking 'this doesn't bode well for the future...'

I also remember reading a theory as to why Australia, Canada, and NZ largely avoided the worst of the GFC (relatively). All three are commodity economies. Canada and Australia, hard commodities, NZ soft commodities. As the GFC took hold early on this showed in consumer demand from the west. Then Chinese manufacturing slowed in response. Finally, that should have flowed through to inputs (which it did to some extent), but at each step the pricing signals take time to propagate and by the time China was adjusting its demand for inputs QE had largely played its part and future demand looked better. In other words, being towards the end of the supply chain delayed the effects long enough to flatten things out for Australia, Canada, and NZ.

We never got the correction we deserved. And here it is.

Sold BTC in the weekend. Will see if I regret it

Surprised Wolfie...stocks ? Apart from the magnificent 7 what is worth buying? Also only down a mere 4% today and back into recovery...however at least you can sleep better I suppose?

Sold my last proxy tulip

just before April 1.

Apt.

Sold BTC in the weekend. Will see if I regret it

Do what you gotta do Wolfie. Can't imagine ever selling BTC. Would be good if banks allowed us to sell units of our property back to them for instead of having to sell assets like ratty.

Yeah but I have 1 BTC left in IBIT / FBTC. Happy to add more in the future in dips.

Its all about personal security and wellbeing. And paying my taxes lol.

Yeah but I have 1 BTC left in IBIT / FBTC. Happy to add more in the future in dips.

All power to you then. You have at least 1 BTC. That puts you in a special club. Generally speaking, you're in the top 10% of BTC owners by amount. With only 1 BTC.

Personally I prefer to be my own sovereign. Philosophical reasons included.

"In Australia, inflation expectations, which had been stuck at 4.5% since December, actually slipped in March to 4.3%. While this may be its lowest since October 2021, it does emphasise just how sticky Aussie CPI inflation has become."

How well do inflation expectations actually track future CPI releases?

One wouldn't want to be selling infant formula or population bomb books.

"...Fertility is declining globally, with rates in more than half of all countries and territories in 2021 below replacement level . Trends since 2000 show considerable heterogeneity in the steepness of declines, and only a small number of countries experienced even a slight fertility rebound after their lowest observed rate, with none reaching replacement level.

...Future fertility rates will continue to decline worldwide and will remain low even under successful implementation of pro-natal policies. These changes will have far-reaching economic and societal consequences due to ageing populations and declining workforces in higher-income countries, combined with an increasing share of livebirths among the already poorest regions of the world.

...Overall, fertility has declined steadily at the global level and across almost all countries and territories since 1950 and is likely to continue to do so until 2100, from a global TFR of more than 4·8 births per female in 1950 to approximately 2·2 in 2021, with TFRs of approximately 1·8 and 1·6 projected in our reference scenario in 2050 and 2100, respectively. Only six of 204 countries and territories (Samoa, Somalia, Tonga, Niger, Chad, and Tajikistan) are projected to have above-replacement levels of fertility by 2100, and only 26 will still have a positive rate of natural increase (ie, the number of births will exceed the number of deaths)."

https://www.thelancet.com/journals/lancet/article/PIIS0140-6736(24)0055…

https://www.aljazeera.com/program/fault-lines/2023/11/17/do-you-want-to…

Carrying capacity of the planet has been vastly exceeded. A population drift down for a few centuries is a good thing.

"Carrying capacity of the planet has been vastly exceeded." If that was remotely true you would be seeing starvation and and infant mortality going up, not down. Innovation capacity negates any "carrying capacity" metric dreamed up but failed peak oilers and population bombers.

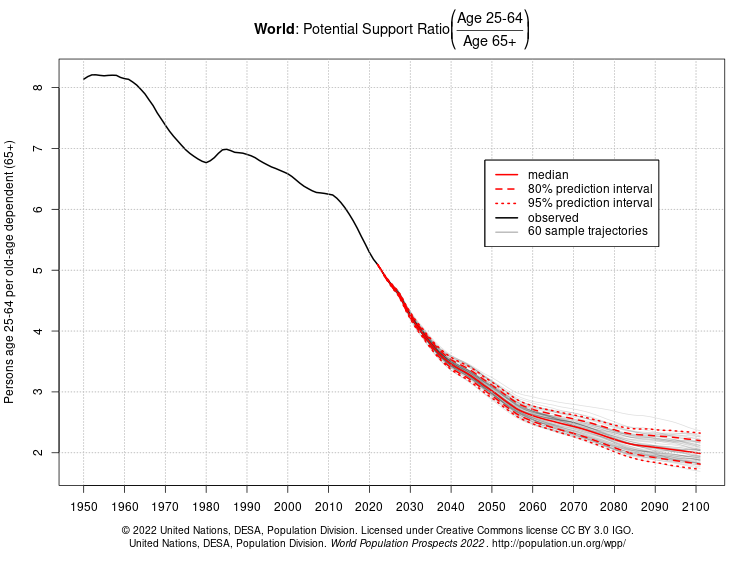

A population drifting down is neither here nor there, but a plummeting populations makes things tricky for the elderly and infirm. Right now if you are 65+ you have at least 5 punters to look out for you - by 2100 that drops to 2. People born in 1950 had 8, So the baby boomers have 8 supporting them when they were born, down to 2 for their grandchildren.

"So, within not too many hundreds of years, and depending on the TFR, there are likely to be less than one billion people alive, and possibly only one-tenth of that, lower than it was 10 000 years ago.". It is laughable that handwringers rabbit on about "infinite growth" when the writing is already on the wall for any growth - not due to lack of fossil fuel but due to lack of people. Makes the whole net zero fad seem rather moot also.

https://insightplus.mja.com.au/wp-content/uploads/2024/02/Picture4-1.png

{kind=link}

https://ourworldindata.org/grapher/malnutrition-deaths-by-age

LoL. Of course we will disagree Profile but in my view New Zealand is well over it's desirable population. ( and yes other placs are worse )

I grew up in Mount Eden. When I look at it now Auckland is so over capacity it's near unliveable. Sadly in one of the most benign environments you can find.

Living well is my preference.

As for 'innovation'. yes it can be done. Exponential population growth solves your aged care issue. Plenty of descriptions in SciFi about the world covered in a single building 20km deep. It can be done, but is it a good idea?

There is no exponential population growth, quite the reverse. It is going to very difficult to manage a rapidly declining population. We have similar views on NZ's population.

You're looking at it through too narrow a straw Profile. Human impact goes far beyond the need for food and health. We have to consider our total impact on the environment and the evidence is that as we are today, the planet is past it's "carrying capacity". But it is also accurate to suggest that technology may be able to ameliorate or relive the degree of that impact, but as PDK is wont to remind us the EROEI has reached the point where that is now consistently negative. He argues that we are past the point where all we can do is fiddle with the rate of decline towards collapse. So going back to your point, where we can see the impacts on food supply and health impacts, when that is clear i would suggest we are then on the free fall to total collapse with no available parachute.

Interesting post. Slightly different experience in the market potential though - I invested in an Indian business through a contact here in NZ that manufactures and distributes toys globally.

No surprises here but millennial parents clearly tend to go overboard when buying stuff for their only child, often more than previous generations spent on an entire litter.

The business, as I understand it, does an impressive job at taking inspiration from a toy that has been around forever, making some minor design changes, putting it in an attractive box and slapping catchy terms on the label such as STEAM, sensory, interactive, promotes creativity/critical thinking etc. on the box.

Commercial RE is extremely sensitive to interest rates. I'll say it again, IMO, the next crash will be caused by commercial RE loans being upside down and unable to be refinanced. Some banks won't be able to carry these bad loans...

Was looking over the Speculative Vacancies Report (PDF - 2019) for Melbourne the other day. What really stood out were the vacancy rates determined for commercial properties - far beyond residential. If that's any indication of the market here I'd be very concerned.

CRE tremors in Aussie. OK, only 17% off peak book value. But you have to remember this qualifies as an A-grade asset in RE parlance. Media trying its best to downplay the potential threats.

Mirvac, the ASX-listed fund manager, investor and developer, has sold a half stake in a major CBD tower on Sydney’s George Street for $364 million at around a 17 per cent discount to its peak book value, setting a clear benchmark for valuations in the battered office market.

Office tower values around the world have tumbled, in response to the shift to remote work, uncertain business conditions and surging interest rates. That shakeout arrived a little later in Australia and some experts anticipate values could drop 25 per cent before it fully washes through, potentially later this year.

https://www.afr.com/property/commercial/mirvac-s-364m-sale-of-tower-sta…

Core Crown tax revenue hits 30% of GDP. Expenses 1/3 of GDP.

Synlait hits the reality check, as predicted by many here

https://www.newshub.co.nz/home/money/2024/04/dairy-company-synlait-post…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.