This Top 5 comes from interest.co.nz's Gareth Vaughan.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing a guest Top 5 yourself, contact gareth.vaughan@interest.co.nz.

1) Albo sharpens elbows for new nationalistic competition.

In a speech on Thursday Aussie Prime Minister Anthony "Albo" Albanese unveiled plans for his government's answer to US President Joe Biden's behemoth, the Inflation Reduction Act. I recently watched a Financial Times film How Biden's Inflation Reduction Act changed the world. It's worth a watch to get a sense of just how significant the Act is as the Biden administration uses federal government money as it seeks to compete better with China and meet climate change commitments.

Here's what the FT says about the film;

The US was for decades the exemplar of free market globalisation. That changed with Donald Trump’s 'America first' agenda. President Joe Biden’s landmark Inflation Reduction Act continues the push for re-industrialisation by using tax credits, loans and grants in a bid to create a domestic clean energy supply chain. The FT looks at three companies using IRA incentives to invest in the US and examines whether the legislation signals the end of globalisation.

According to the Australian Broadcasting Corporation, the Aussie government's Future Made in Australia Act will bring together existing policies like the A$15 billion National Reconstruction Fund and critical minerals strategy with investments to be announced starting from next month's budget.

Australia going down this path could get interesting for New Zealand. Albanese spoke of mimicking a range of countries investing in their industrial base, their manufacturing capability and their economic sovereignty. An investment boom in Australia will almost certainly attract New Zealand workers and businesses. So will our government respond in any way?

Here's Albanese in his speech;

We need to be clear-eyed about the economic realities of this decade.

Recognising that the game has changed - and the role of Government needs to evolve.

Government needs to be more strategic, more sophisticated and a more constructive contributor.

We need sharper elbows when it comes to marking out our national interest.

And we need to be willing to break with old orthodoxies and pull new levers to advance the national interest.

We have to think differently about what Government can – and must – do to work alongside the private sector to grow the economy.

To boost productivity, improve competition and secure our future prosperity.

Combining market tools, with government action - to create wealth and create opportunity.

We need to take a fresh look at how government can support small business and start-ups and service industries to diversify our economy and our trade.

Also;

This decade marks a fundamental shift in the way nations are structuring their economies.

A change every bit as significant as the industrial revolution or the information revolution – and more rapid and wide-ranging than both.

Domestic economic policy settings are being re-shaped by a new set of global economic imperatives.

And domestic economic priorities are re-shaping trade policy.

In the years following the Cold War, people spoke about ‘the end of history’.

The benign assumption that free trade would spread unchallenged and globalisation would guarantee peace and prosperity for all.

Yet even in countries like Australia that have benefited enormously from the opening-up of our economy and engaging in our region, opportunity has not been shared evenly.

In other parts of the world, the fault lines are far wider.

Strategic competition is a fact of life.

Nations are drawing an explicit link between economic security and national security.

The so-called ‘Washington consensus’ has fractured - and Washington itself is pursuing a new direction.

The United States has implemented the Inflation Reduction Act and CHIPS Acts and pursued what they call a ‘small yard, high fence’ approach to critical industries.

The European Union has introduced its European Economic Security Strategy.

Japan has the Economic Security Promotion Act.

The Republic of Korea is re-framing its economic policy around a National Security Strategy.

And Canada has brought in new rules to tighten foreign direct investment in their significant critical mineral reserves.

All these countries are investing in their industrial base, their manufacturing capability and their economic sovereignty.

This is not old-fashioned protectionism or isolationism – it is the new competition.

Speaking to the ABC, Albanese talked up the opportunity Australia's resources offer the country in the renewable energy transition push to net zero greenhouse gas emissions.

When we look at the resources that will power the global economy this century we have copper, vanadium, lithium, nickel. We have an abundance of all of those. We have the best solar resources in the world. We have an incredible opportunity but we must seize it. We can't just sit back and watch and hope for the best because if that happens we will continue to export our resources overseas, see value added, see jobs created somewhere else in the world and then import it back at much higher value. This is about engaging in this global competition in Australia's national interest to create jobs and opportunity right here.

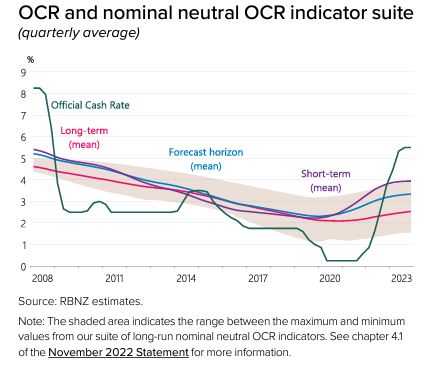

2) Where's r* gone, and is it a blurry guidepost?

The Bank for International Settlements (BIS), the central banks' bank, looks at what central bankers and economists refer to as the natural rate of interest in its latest quarterly review. BIS asks where the natural rate of interest, or r* (the "r-star"), is it at, how has it evolved, and where is it heading?

Inflation targeting central banks, such as the Reserve Bank of New Zealand (RBNZ), look to their stars to help them determine how tight or how loose monetary policy is and should be.

In its Monetary Policy Statement last November, the RBNZ said its estimate of the neutral (natural) Official Cash Rate (OCR) had increased to 2.50% from 2.25%. The OCR's currently at 5.50%.

The neutral OCR, as explained by the RBNZ is;

the rate that, on average over time, would neither stimulate nor constrain the economy, and be consistent with no over- or under-utilisation of resources and stable inflation in the economy.

Based on our neutral OCR indicator suite, we have revised our estimate of the long-run nominal neutral OCR from 2.25 percent up to 2.5 percent from the December 2023 quarter onwards. The increase in our neutral indicator suite primarily reflects that long-term interest rates have increased substantially since the end of 2021. The OCR remains contractionary at its current level based on this revised assumption. Taken on its own, the upward revision to the neutral OCR creates gradual upward pressure on the OCR over time.

BIS, meanwhile notes; "the uncertainty around r* estimates at the current juncture is very high."

The sharpest and most synchronised monetary tightening in decades has lifted [monetary] policy rates from their decade-long historical lows. Against this background, there is an increasingly lively debate on whether policy rates adjusted for inflation (“real rates”) will converge back to their pre-pandemic lows or to a higher level.

So what do the BIS boffins conclude?

The analysis in this special feature suggests that r*, or at least perceptions of it, may have risen post-pandemic, but that its assessment is surrounded by a very high degree of uncertainty. These findings caution against over-reliance on r* as a guide for monetary policy.

The uncertainty surrounding r* suggests that it is a blurry guidepost for assessing the monetary policy stance and hence the tightness of monetary policy, in particular at the current juncture. In this context, it appears advisable to guide policy decisions based more firmly on observed inflation rather than on highly uncertain estimates of the natural rate.

Uncertainty about r* also underscores the need for robust monetary policy frameworks. They need to be fit for purpose regardless of the broad economic environment and associated estimates of r*. The expectation of the persistence of a very low r*, and hence of a high incidence of the effective lower bound, was a key consideration behind the review of monetary policy frameworks pre-Covid. The last couple of years have highlighted how quickly the environment, and associated views of r*, can change.

A good point is made there, I think, in terms of it being "advisable to guide policy decisions based more firmly on observed inflation rather than on highly uncertain estimates of the natural/neutral rate."

3) Mossack & Fonseca go on trial 8 years after the Panama Papers.

It's now eight years since the International Consortium of Investigative Journalists (ICIJ) and its global media partners brought us the Panama Papers. A major money laundering trial stemming from the Panama Papers has kicked-off in a Panamanian criminal court.

Being tried are 27 people, including Jürgen Mossack and Ramón Fonseca Mora, the founders of the now defunct law firm at the centre of the Panama Papers.

As the ICIJ puts it;

Based on a trove of 11.5 million files leaked to German newspaper Süddeutsche Zeitung and shared with ICIJ, the Pulitzer Prize-winning investigation exposed the offshore financial secrets of world leaders and other powerful public figures, triggering protests, government probes and the resignation of Iceland’s prime minister.

New Zealand, of course, wasn't immune. Mossack Fonseca had a NZ offshoot. Our government was forced to make changes to foreign trust disclosure rules. In 2019 I spoke with the ICIJ's Will Fitzgibbon in a video interview about NZ's role in both the Panama Papers and another ICIJ investigation, the Paradise Papers, about what he described as; "very clear, intentional and excited use of New Zealand as a clean tax haven."

Here's more on the trial from the Associated Press;

Mossack was present in the courtroom, and said “I am not guilty of such acts.”

Lawyers for Fonseca said he was in a hospital in Panama.

The case centers on allegations the firm set up shell companies to acquire properties in Panama with money from a sprawling corruption scheme in Brazil known as the Car Wash, or Lava Jato in Portuguese.

Fonseca has said the firm, which closed in 2018, had no control over how its clients might use offshore vehicles created for them. Both Mossack and Fonseca have Panamanian citizenship, and Panama does not extradite its own citizens.

There was even a film made about Mossack Fonseca, The Laundromat starring Meryl Streep, Gary Oldman, Antonio Banderas, David Schwimmer and Sharon Stone. Here's the trailer.

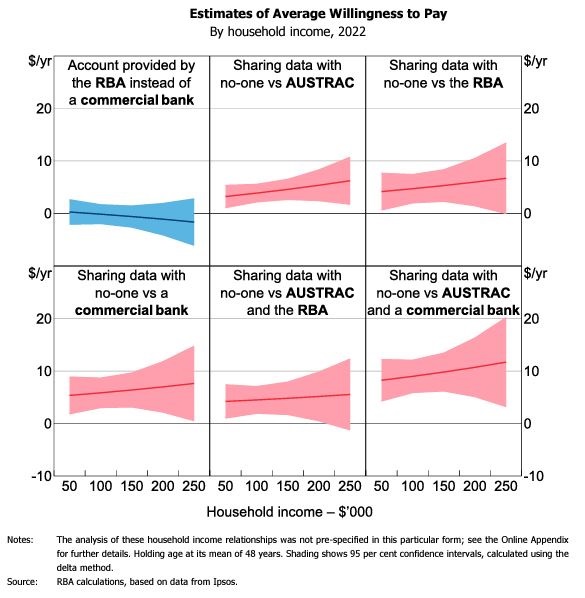

4) Could privacy attract consumers to a CBDC?

In a new research paper on its potential use of a central bank digital currency (CBDC), the Reserve Bank of Australia (RBA) says privacy settings offered by a retail CBDC could appeal to consumers. A CBDC is the digital form of a country's fiat currency such as the NZ or Aussie dollar. Some countries have already introduced them and the RBNZ and RBA are both investigating their potential use

The RBA paper suggests privacy settings for a CBDC appear to be more consequential for its uptake than any incremental safety benefits.

The average consumer values transaction anonymity and, to the extent that transaction data do need to be shared with other entities, the average consumer cares about who those entities are. For example, we estimate that, on average, Australian consumers would pay $5 per year more for access to an account that makes transaction data available to the RBA instead of a commercial bank, assuming that AUSTRAC [Australia's anti-money laundering regulator] can access transaction data in both cases.

Aggregated over the adult population, this equates to around $100 million per year, a figure that would likely rise a little further if the account also offered anonymity for small transactions. This result is consistent with survey evidence from the Office of the Australian Information Commissioner (2023) about attitudes of Australians to privacy in a more general context. Respondents to that survey placed a lot of importance on their privacy when choosing a product or service and were generally more comfortable sharing data with federal government agencies than with private financial institutions.

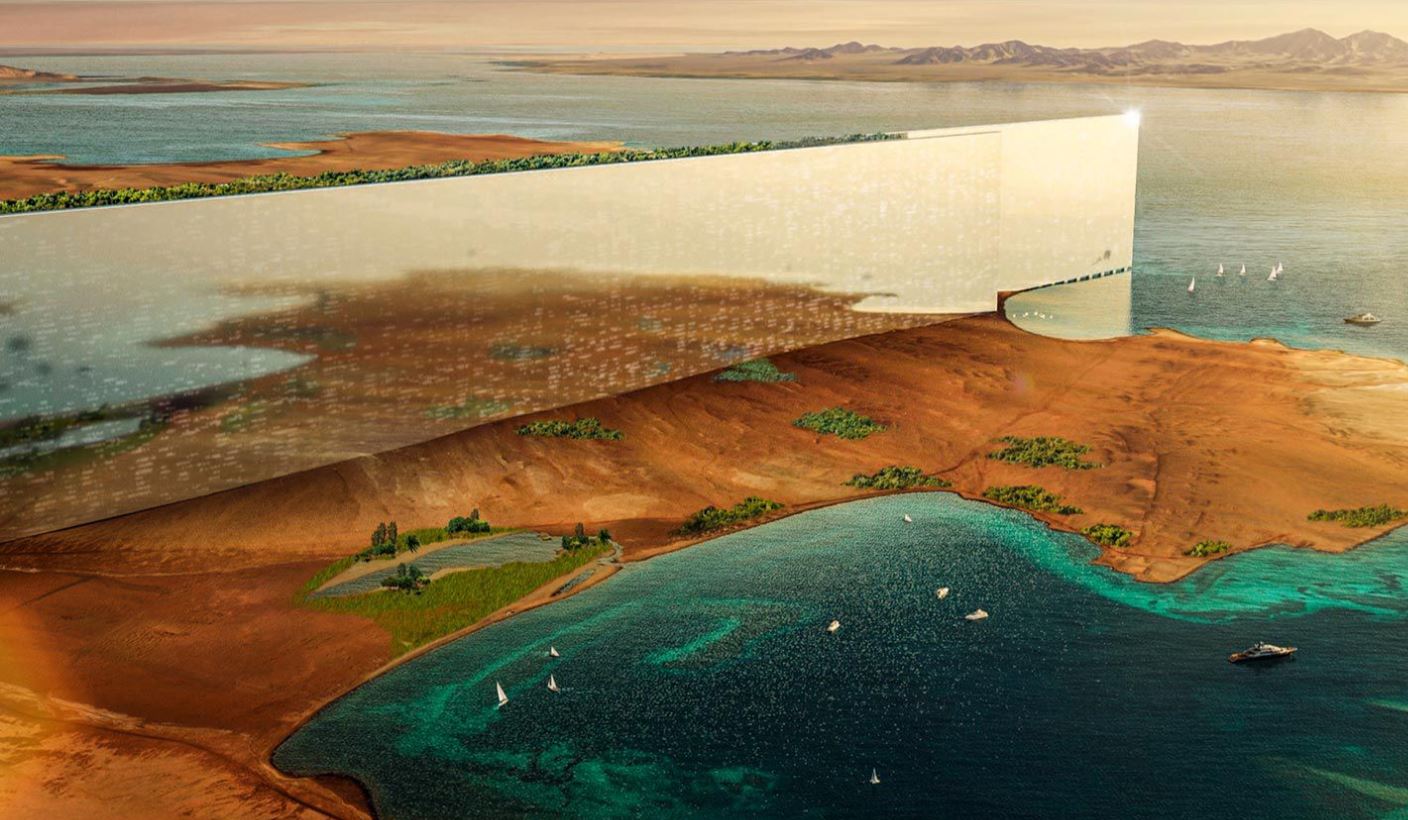

5) Saudi Arabia's new megacity may be behind schedule.

Oil rich Saudi Arabia has scaled back its medium-term plans for Neom, Bloomberg reports. Neom's planned as a showpiece by Crown Prince Mohammed bin Salman of how Saudi Arabia's economy can be diversified away from oil dependence and is aimed at serving as a testbed for technologies that could revolutionize daily life, Bloomberg says.

It includes The Line, a futuristic city planned within a pair of skyscrapers, plus an industrial city, ports and tourism developments.

By 2030, the government at one point hoped to have 1.5 million residents living in The Line, a sprawling, futuristic city it plans to contain within a pair of mirror-clad skyscrapers. Now, officials expect the development will house fewer than 300,000 residents by that time, according to a person familiar with the matter.

Officials have long said The Line would be built in stages and they expect it to ultimately cover a 170-kilometer stretch of desert along the coast. With the latest pullback, though, officials expect to have just 2.4 kilometers of the project completed by 2030, the person familiar with the matter said, who asked not to be named discussing non-public information.

Budget approval is awaited, Bloomberg says.

The pullback on The Line comes as the kingdom’s sovereign wealth fund has yet to approve Neom’s budget for 2024, the people familiar with the matter said. It shows that the financial realities of the trillions of dollars of investment are starting to cause concern at the highest levels of the Saudi government as it tries to fulfill its ambitious Vision 2030 program, the overarching initiative tasked with diversifying the kingdom’s economy.

Already, officials have said that some of the projects outlined in that program will be delayed past 2030.

MBS’s [Crown Prince Mohammed bin Salman's] ambitions for The Line have captured the attention of city planners and architects from around the world. Renderings have shown he’s conceived of a city that’s longer than the distance between New York and Philadelphia and is all contained within mirrored structures that would be taller than the Empire State Building. At one point, officials had hoped The Line would welcome its first residents this year.

Promotional material for The Line describes it as;

A cognitive city stretching across 170 kilometers, from the epic mountains of NEOM across inspirational desert valleys to the beautiful Red Sea. A mirrored architectural masterpiece towering 500 meters above sea level, but a land-saving 200 meters wide. THE LINE redefines the concept of urban development and what cities of the future will look like.

It's to have "no roads, cars or emissions," and "run on 100% renewable energy and 95% of land will be preserved for nature."

THE LINE will eventually accommodate 9 million people and will be built on a footprint of just 34 square kilometers. This will mean a reduced infrastructure footprint, creating never-before-seen efficiencies in city functions. The ideal climate all-year-round will ensure that residents can enjoy the surrounding nature. Residents will also have access to all daily essentials within a five-minute walk, in addition to high-speed rail – with an end-to-end transit of 20 minutes.

Images of The Line in promotional material are certainly spectacular, as you would expect.

27 Comments

Good on Albanese.

To answer your question - NZ drank the neoliberal kool aid more than anywhere else, and continues to do so. We don’t believe in government having a massive role in investment.

Just look at the Kiwibuild debacle. Originally David Shearer’s idea, it was an idea of government building housing en masse, making big use of prefabrication (which would have involved investment in plants etc).

Then Ardern and her clowns, especially Twyford, turned it into an underwriting scheme.

If Shearer’s big idea had won out, we would have certainty for years around housing supply, construction jobs, apprenticeships etc. etc.

But………………….no

Maybe -Muldoon's think big remains instructive

As does NZ Rail run by the Crown as a money sink for at least the last 60 years

NZ Rail is going nowhere while successive governments invest in roads while making car and light vehicles subsidize the damage done by heavy vehicles. i.e. socializing the costs while privatizing the profits.

Just another thing NZ's leadership thinks is grand but in actual fact is daft. Why do people vote for this nonsense?

Light vehicles are not subsidising heavy vehicles, heavy vehicles are charged for road damage according to the forth power rule. We are all subsidising light vehicles due to too low petrol tax, and maybe light vehicle RUCs.

Light vehicle users and other taxpayers are subsidising heavy road transport because what heavy vehicles pay isn't sufficient to cover the damage they cause and the extra cost of building roads to cater to that extra weight.

But yes, we are subsidising roads in general.

are subsidising heavy road transport because what heavy vehicles pay isn't sufficient to cover the damage they cause and the extra cost of building roads to cater to that extra weight

Please provide evidence. Several reviews of the RUC system have not concluded this is the case.

Albo talks of "sharper elbows" about Australia's self interest.

New Zealand should take the same approach. We need to get a little more selfish about our ownership, where profits disappear to etc.

New Zealanders first.

Thats a god idea for a political party :)......

Wait a minute, wasn't the ole Winnes idea?? Oh well, nice while it lasted - Since he got captured and since de- testacaled by the Nats LandLording agenda.

KH we do need to get smarter but I dont see getting govt involved in "business" as the answer - they could however ensure its the best place to operate

If Australia is intending to compete with China and the rest of the world on an own country first agenda it could easily be a race to the bottom given the deep pockets of the others - particularly China. An alternative could be to build your country using their state subsidized products to your advantage

and let the Europeans be the protectionists as they love to be

Horrors Grattaway, that you thought I advocated more government in business. Less of that please. Government need to be more referee, less player.

Another example where we need more "sharp elbow" in New Zealand interest is tax. eg the Google/ Facebook revenue streams. We should be 1. all over those and 2. if there is a balance of fairness then let's have more fairness for us than them

You know "sharp elbows"

A good point is made there, I think, in terms of it being "advisable to guide policy decisions based more firmly on observed inflation rather than on highly uncertain estimates of the natural/neutral rate."

This is what Milton Friedman called the interest rate fallacy, and it indeed refuses to die. We can tell what monetary conditions are in the real economy, as opposed to financial liquidity, though the two can be linked, by the general level of interest rates. When money is plentiful, interest rates will be high not low; and when money is restricted, interest rates will be low not high. The reason is as Wicksell described more than a century ago:

[The natural rate] is never high or low in itself, but only in relation to the profit which people can make with the money in their hands, and this, of course, varies. In good times, when trade is brisk, the rate of profit is high, and, what is of great consequence, is generally expected to remain high; in periods of depression it is low, and expected to remain low.

When nominal profits are expected to be robust, holders of money must be compensated for lending it out by higher interest rates. Thus, the same holds for inflationary circumstances, where nominal profits follow the rate of consumer prices. During the Great Inflation, interest rates weren’t low at all, they were through the roof well into double digits and higher by 1980. At the opposite end in the Great Depression, interest rates were low and stayed there because, as Wicksell wrote, the rate of profit was low and was expected to be low well into the future. High quality borrowers were given as much money as they could want while the rest of the economy was deprived of funds; liquidity and safety being the only preferences in what sounds entirely familiar. Link

{kind=link}

The ABC is taking a wider range of views on Albanese's comments

PM heralds dawn of new manufacturing era, but what does it actually mean? - ABC News

"Dr Hamilton said Australia should have "learnt the hard way over many decades" that reaching the head of the pack was difficult.

"We have spent many billions of dollars before cruelly tying the working lives of tens of thousands of young Australians to an industry with no real future," he said, citing the car industry.

"We spent decades ignoring the long-term unviability of the car industry in Australia, pouring billions of dollars of subsidies into it, and it never became an industry that could stand on its own.

"I thought we'd learned these lessons, but apparently not. The bad old days are back.""

Gareth, thanks so much for 'front and centering' the r* issues.

Hopefully the more people that understand the huge amount of influence central banks have over their daily lives - and it is huge! - the more people will demand better solutions. The ongoing boom / bust cycles really isn't helping most people as the rich are still hoovering up the wealth. Or put another way, exactly who are central banks actually working for?

The natural rate of interest (r*) is around 3.6% to 4.7%. Anything lower will boost current asset prices relative to income, which is unsustainable. Any higher will mean stagnation because the current asset price-to-income ratios will fall.

Was.

Not is.

Global supply-side scarcity is mounting exponentially - as is required maintenance effort. Albanese is echoing Trump, who found a niche that was opening up; someone was going to exploit it, he was just first-in.

We are witnessing increasing pull-back behind borders, increasing attempts to make everything within them; realisations that spending on defense needs to be more, given what is coming. Many made false assumptions; Russia is actually thriving on a war-footing, not being throttled. And we're heading for a showdown - or a series of same - over 'what's left'.

So both globally, and locally (via higher wages doing the making now it's local) inflation is here to... rise. In lockstep with rising inability to repay debt. Going to be a fascinating period now-2030.

" Thriving" is embellishing the Russian situation more than a little. Anyone that's a fan of living in a totalitarian state would be ok with the limited thriving going on I guess? Having your primary kids learning to disassemble an AK47 and being taught dying for glorious leader as a patriot is divine destiny, could be hard to stomach for others though?

Compared to before the 'invasion', they are humming along. And those who forecast them failing via 'sanctions', were wrong.

Same folk who think money is worth something, and is more important than energy.

The US won WW2 'floating to victory on a tide of oil'; just remember that the biggest stock left on the planet, is in Russia.

:)

As to relative appraisal, get a copy of Douglas Reed's Insanity Fair (I can lone you a copy). Fascinating.

Loan ? Lend - lease?

Potential however for there to be huge stocks of oil in Guyana and still Venezuela is heavily underutilised due to their inefficient government and corruption.

When r* was first invented the * referred to a footnote that read 'this is complete nonsense of course.

LOL. To be fair, the rate is massively difficult to pin down, and moves all over the place, all the time.

But as a concept, I think it makes sense. And with central banks tweaking their views on where it is, we get a better(?) feel for how restrictive or expansionist the rates they can control, e.g. the OCR, actually is, according to them. But yes, it is indeed their 'reckons'. The RBNZ recently raised their reckons for this rate by 0.25%. I went looking for their empirical data for this change but they gave little to none. Not good. Without it, they should have just left it where it was.

The best evidence for an r* is the fact that over decades it has been coming down. I put this down to information technologies facilitating much better information being available, in the blink of the eye, which reduces the risk premium that was built into previous rates. It could also be economies of scale as lenders have become huge over this time. It can't continue to fall forever obviously. But I do expect it to continue for a few more decades until it bumps around an equilibrium.

"The natural rate of interest (r*) is around 3.6% to 4.7%. "

Could you explain how you got to that range? (If it's just a 'reckons' then please say so.)

I look at the creation of money created by leveraging of assets in a market with low elasticity of supply. For equilibrium, the demand for money to allow rotation of these assets (e.g. every 15 or so years in the NZ housing market) must be equal to supply of money created by the leverage. If demand is greater, asset prices go down, if supply of money is excessive ("savings glut") prices increase. At the natural rate of interest, the stimulus matches the constraint. In short, I derive it from the turnover of assets. The higher the turnover of assets the higher the natural rate of interest (in an equilibrated market) e.g if the turnover of assets were every 7 years that would entail a natural rate of interest of about 9%.

Money is created in other ways beyond the 'leveraging of assets' so the system you're using isn't as closed as you're suggesting.

Yes, I do recognise that there can be other ways. But one can hardly go into all the details in one post. I emphasise the leverage of existing assets in a market of low elasticity of supply because that is where the r* matters from a financial stability perspective. Otherwise, in an asset market of high elasticity, r* is expressed in the rate of growth, -the higher r* the higher the growth.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.