Here's our summary of key economic events over the weekend that affect New Zealand, with news global inflation pressures seem to be easing off sharply.

First, the benchmark for world food commodity prices dropped sharply in July, with major cereal and vegetable oil prices recording double-digit percentage falls. But meat prices held, and the dairy price fall was modest in the circumstances, both still very close to their all-time record highs. But the retreats for cereals are impressive and will certainly ease global inflation pressure. The overall index fell -8.6% in July from June even if it is still +13% higher than a year ago. Along with the sharp falls in crude oil prices recently, perhaps Team Transitory will have its day yet.

Chinese exports rose +18% in July from year-ago levels, a bit better than expected but very similar to the June result. Imports rose only +2.3% and less than expected suggesting their domestic demand is soft, especially as they fell from June. If it wasn't for the US economy firing on all cylinders and drawing in imports from all over, China's trade result wouldn't have held up. In fact, the surplus they reported was a record high.

They had a trade surplus of +US$41.5 bln in July with the US, a deficit of -US$6.9 bln with Australia, and a deficit of -US$0.4 bln with New Zealand, according to their Customs data. All these three data items are 'larger'; that is, a bigger surplus with the US, bigger deficits with Australia and New Zealand.

In China, all eyes are on signs their moribund property markets are recovering. Cement production remains unusually low, but there are signs high stocks are falling, drawn down as some projects get back underway. But there is no sign that iron ore prices are rising from a demand rise. And at the same time, there is no sign China has yet succeeded in driving down the iron ore price as part of it new bulk-buying program.

The Japanese have reported something of a surprise with household spending rising quite sharply in June to be +3.5% higher than a year ago, up +1.5% from May alone. No analyst saw that jump coming. These are 'real' gains, after adjusting for inflation. True it is only one month and that doesn't make it a trend. But quite a string of Japanese data has been positive recently, so this household data may have legs and underpin the inflation rise the Bank of Japan has been seeking for decades. Separately, they reported better than expected incomes growth as well.

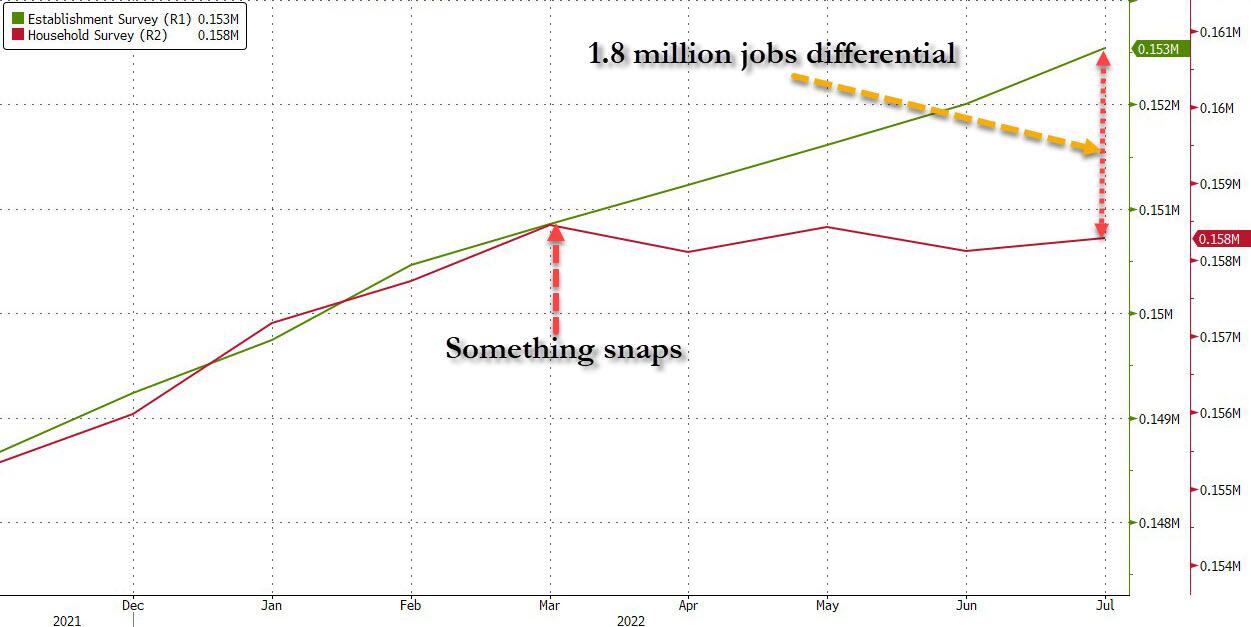

Over the weekend in the US, their non-farm payrolls report for July has heaped pressure on the Fed with a much larger than expected rise. Their labour market remains hot with employers adding +528,000 jobs in the month, double what analysts had expected. This is not data that suggests the US is in recession. July is normally a month when overall payrolls shrink as firms go into their summer shutdown mode. But this year that hasn't happened with the employed labour force now over 152 mln workers, and a hugely impressive +5.8 mln gain from a year ago (or if you like seasonally adjusted data, +6.1 mln more). Apart from the 2021 recovery from 2020 there has never been a July quite like this one. The rise in the number of women being hired is impressing analysts too.

The US jobless rate fell to 3.5% matching the pre-pandemic level, and their best since 1969. Their participation rate didn't change much however.

Meanwhile, American consumer debt rose much more than expected, in fact up +US$40 bln in June from May, that was almost double the +US$25 bln expected, and the May rise was revised up. The June rise was the second biggest jump ever.

The Canadians also released jobs data for July and that wasn't anywhere near as impressive; in fact they reported the summer decline that didn't happen in the US. They lost -31,000 jobs in July on top of the -43,000 they lost in June. (A +20,000 gain was expected.) The July losses were split between full-time and part-time jobs, but in the context of their overall 20.6 mln labour force, it didn't change their jobless rate at 4.9%.

Singaporean retail sales fell in June from May, and that undermined their good year-on-year gains. Apart from fuel sales which were boosted by inflation, the falls were widespread and somewhat unusual for them. If the Chinese posturing on Taiwan is extended, that probably won't help economies like Singapore.

In India, their central bank reviewed their policy rate on Friday. It was 4.9% and markets had expected a +35 bps rise to 5.25%. But the RBI pushed through a full +50 bps hike to 5.4%. It's a sharper than expected rise because they too have inflation concerns, and they need to shield their exchange rate which has come under pressure since war broke out in Europe.

Turkey has reported an 80% annual inflation rate for July (well, 79.6% to be exact). Nothing the Turkish president seem to actually work for him. Now he is talking with the Russians on a new economic pact. We will see how that works out. Its the weak and the weak, and a sign of desperation.

The UST 10yr yield starts today at 2.83%, jerked higher by +16 bps on the US jobs data. The UST 2-10 rate curve is more inverted today, now at -40 bps but their 1-5 curve is less negative at -31 bps. Their 30 day-10yr curve is now at +66 bps and much steeper than this time Friday. The Australian ten year bond is unchanged at 3.26%. The China Govt ten year bond is little-changed at 2.75% and still near its low for the year. And the New Zealand Govt ten year will start today down at 3.33%. A week ago it was at 3.72% so a rather large -39 bps cumulative retreat since then.

Warren Buffett’s company reported a -US$44 bln loss in the second quarter as the paper value of its investments plummeted, but Berkshire Hathaway’s many operating companies performed well suggesting the overall economy they operate in is weathering the pressure from inflation and rising interest rates. The stock prices of three of Berkshire’s biggest investments - Apple, American Express and Bank of America - all fell significantly during the second quarter. But those stocks have all rebounded since the start of July, meaning Berkshire’s portfolio is already worth more than it was at the end of June. And Berkshire’s Q2 earnings were up a remarkable +39% from year-ago levels to $9.3 bln.

The price of gold will open today at US$1776/oz which is up +US$2 /oz from this time Saturday. A week ago it was US$1765/oz, so a +US$11 gain since then.

And oil prices start down a mere -50 USc from Saturday at just on US$88/bbl in the US, while the international Brent price is now just on US$94/bbl. A week ago these prices were US$98 and US$104/bbl respectively, so basically a drop on -US$10/bbl in that time. That is a drop of -22% from early June, and basically back to prices in effect before the Russian invasion of Ukraine.

The Kiwi dollar will open today at 62.4 USc which is -½c lower than this time last week. Against the Australian dollar we are marginally firmer at 90.4 AUc. Against the euro we are firmer too at 61.4 euro cents. That all means our TWI-5 starts today at just on 71. It has been in a very tight range at about this level for three weeks now.

The bitcoin price has moved marginally higher from this time Saturday, up +1.8% to US$23,251. Volatility over the past 24 hours has been low at just over +/-0.9%.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

73 Comments

Worse is over, Good times ahead.

Relax and enjoy before the next data

Time to borrow against the house and treat yourself to that new BMW!

(And repeated experience - sometimes I never learn - tells us to 'sell it before the warranty expires'. Gearbox on both occasions)

We can see you're missing the 'm'

:)

Time to stock up on the prime real estate TTP is offering in the Manawatu ! .....road to riches !

Over the weekend in the US, their non-farm payrolls report for July has heaped pressure on the Fed with a much larger than expected rise.

This is getting ridiculous. One of the two BLS labor market surveys has to be wrong. They've gone too far in opposite directions at this point. CES v CPS. One says all good, the other recession. And this is not the first time, either. Link

{kind=link}

The Fed gets blowout payroll & new low UE rate, though those are misleading (just like 3yrs ago) rate hikes get more room. Actual economy keeps moving toward recession (HH Survey), so inversion blows out. 2s +21 bps 10s +15 bps inversion now massive 41bps Link

I'm pretty simplistic but I really just look at wage inflation because that is permanent.

I would like someone to chart wage inflation to see how much it has caught us up to the inflation that has already happened. Maybe we're only 10 years behind by now.

Over the last 4 years to June quarter 2022, CPI has increased 14.4% and median wages have grown 11%.

Our capital-shallow industries, debt-fueled consumption and dysfunctional markets correlate to the dynamics that businesses have the pricing power to almost entirely pass on their increased costs to end consumers.

I'd guess that the 11% median wage growth in the last 4 years has been boosted to some degree with Covid lockdowns and businesses here being unable to tap into cheap migrant labour.

Labour has introduced a median wage threshold on employers sponsoring work visas. Net migration resuming to previous highs could stagnate wage growth for the lower-skilled workers but not reduce it, unless National-ACT swing to power in Dec 2023.

Some credit goes to the government in maintaining this difficult stance amid immense pressure from business lobbies and every other party in Parliament.

The government has made it much easier for itself by having the entire immigration department grind to a halt over Covid lockdowns, which from what I'm told anecdotally, was basically just a paid leave period for many INZ staff as they did not have the capacity to securely process applications remotely.

I can imagine that INZ and IRD are two departments that might be reluctant to provide access remotely. Would be great targets for corruption.

Global prices easing off sharply, who would have thought… not almost all of the commenters on this website.

Yay, I'm feeling poorer a little less quickly!

Have a couple of TDs due Sep & Nov. Interest rates on offer for renewal flat. That is 4% 1 year rising to 4.5% 5 years. May increase after Aug OCR? What’s the consensus renew, for 2 if not 3 years ?

FG, I'm in the same boat, going for 1 year for all

There is only one way things go; ultimate scarcity vs overpopulation equals over-demand. The only way to collapse that, is to disenfranchise someone. That someone has to be the poor. You do that by having conned them into being levered, then lifting interest-rates. They default, you clean up, demand has temporarily been reduced.

But this time the wave is bigger than the surfboard. Oscillations is what we are - and will be - seeing, but the trend has to be to zero interest (and below), to more competing demand for essentials, and to demand destruction for inessentials.

Well there used to be of course the great benefit of culling the hoi polloi by means of warfare. By means of the RN press gangs for instance. Wellington described his army at Waterloo something like scum of the earth. As a private or a rating your life expectancy was neither considered nor important beyond not so much serving King/Queen and country but expanding power & wealth of said monarch and all the attendees down the line. In some part, the land seizures & expulsions in Scotland, post the Napoleonic wars, demonstrate the difficulty faced if a large body of trained & brutal soldiers return home and then have nothing much to do.

There certainly seems to be a clique of self appointed elitists around the world who appear to be favouring that sort of world.

Central Bankers?

It's just "rinse and repeat" - we are on the road to no where...how much more can they extract from the workers in the western world ???

Inflation is the last tool left in the tool box ......but the debt will still be there ......further driving the gap between the "elites" and everyone else.

When I need to refix July next year I think I will once again get a rate starting with a 2. Whether it is 2.9% (deflation caused by prices dropping back to where they were) or 20% (hyperinflation) I am not sure.

Let's hope that said commenters didn't base any financial decisions on their reckons. Imagine if you'd fixed your mortgage for more than a year recently! Ouch.

People do not appreciate that our CPI moves in lockstep with changes in oil prices - because we live in a global economy that is totally dependent on oil. The idea that RBNZ wiggling the OCR lever around has any real influence on prices (other than house prices) is dumb - based on disproven theories that only live on because economics students still get taught them.

Nothing the Turkish president seem to actually work for him. Now he is talking with the Russians on a new economic pact. We will see how that works out. Its the weak and the weak, and a sign of desperation.

Its the resources:

Alarm mounts in western capitals over Turkey’s deepening ties with Russia

China to step up pressure on US over Taiwan, to enhance ties with Russia — expert

Russia’s proven reserves of oil to suffice for 39 years, gas - for 80 years, official says

There is no doubt about it. There is great power in having the power!

There are some countries in the world where you wonder why they don’t split in two. Turkey is definitely one of those, they are fairly westernised in the west and Arab in the east. Why wouldn’t Istanbul split off into it’s own country and become part of the EU? Surely it couldn’t be any worse?

(I also wonder why the United States don’t split in two with such a geographical political divide too)

The US tried that once - didn't work too well.

That was a while back. Another option might be an economic union similar to the EU (well how the EU should be). Give each state the complete right to set its own laws and spend its own tax money, with the federal government only setting interest rates and only managing the things that must be federal.

Aha into the nitty gritty that the civil war was a little bit about. That war was largely about State V Federal authority. Somehow I doubt they'l want to revisit that one. Not sure that we'd want them too either.

"I doubt they'l want to revisit that one" - I think they will need to if their society continues to get more divided.

You may well be correct, but they need to address the root causes of the divisions because unless they do no good will come from any of it.

Murray - leaning towers of misconception; you weigh social interaction too highly. The real interface was between two energy systems. One relied on cheap human labour. The other was beginning to mechanise, via coal. There is always only one outcome when energy systems clash; the lesser loses. Happened to the Maoris, First Nations, the cannon/musket hurled more/faster/further. Wins every time.

That might be the cloak you're putting on it now PDK, but at the time it was much simpler. The states didn't want to be dictated to by Washington, and yes that included slavery. But even then both sides were running short of bodies to throw at the carnage to the point that Lincoln promised slaves their freedom if they signed up to fight for the north (Federal Government).

A civil war today would be a complex thing, and who knows what side many serving military would swing to?

That social stuff, is always the cloak.

The physics is paramount. The US won WW2 on an ocean of oil, not because it was morally superior, or (questionably) democratic.

WW1 ushered in mechanised ordnance etc & that accelerated the importance of oil to be beyond any crucial introduction to warfare since gun powder. Hence the arrival of the Getty clan & the other oil barons. That criteria certainly sallied forth in WW2 where it is largely overlooked that the Wehrmacht was largely still horse drawn. Take it by now you have absorbed V D Hanson “The Second World Wars” which does detail, well beyond just fuel, how technology in industrial organisation & production, was miles ahead of Germany in the USA & surprisingly the UK too.

The US won the war because of their industrial power, yes energy, but more than that resources too. But it was more democratic then than it is now.

The turmoil in the US and in other western 'democracies' certainly seems to indicate the world is ripe for a major war. The problem is that nukes are now too common. I don't think it will be just 'energy' that dictates who will win, but a total resources aspect. And the US has to be close to the top if not at it. China has 2 million men under arms, the US maybe half that, but technologically the US is superior with more combat experience. If any war becomes attritional, then it all falls back to how many bodies can be thrown in because the technology takes too long to replace when is gets consumed. In the end the war would not be good for any of us.

How about Southland splitting off from the rest of NZ, especially the crowd of freeloaders up in Auckland that produce little for the country other than housing speculation?

The US could split into many different countries. Lots of states produce more than they consume and literally subsidize the poor states. Southland?

Southland - GDP per capita $65K

Auckland - GDP per capita $71K

And GDP is a measure of?

Life-supporting capability per capita?

Southland near 100%.

Auckland nil. Built over its potato patch, much like an adult version of swapping the family cow for five magic beans.

Not that I'd live in Southland; as my old man said of his leaving it: Anyone with any get up and go - has got up and went. Only Shadbolt reversed the trend...

Strawman PDK

North island / south island?

"First, the benchmark for world food commodity prices dropped sharply in July, with major cereal and vegetable oil prices recording double-digit percentage falls."

Wasn't Turkey a major influencer in getting the grain ships out of the blockade? Drop in prices as a result of this? Waiting for Russia to sabotage this.

Cereal and vegetable oil should not be classified as food. Commodity you are correct.

There’s no path out of economic oblivion for Russia’: New report reveals how corporate exodus has already wiped out decades of post–Cold War growth

https://fortune.com/2022/08/04/russia-sanctions-economic-oblivion-yale-…

That's propaganda. Whoever HAS the resources - particularly the energy resources - has everything.

Everybody else has digits in a computer.

You need demand as well as supply.

there is always increasing demand, just wait till the northern winter and we will see if the actions match the words

Hmmm, this is also propaganda.

Pretty obviously, you also need more than go juice.

Unless you had ALL the resources, which Vlad obviously doesn't.

Russia is rich and diverse in resources. What it doesn't have is an economic system than can exploit them or customers to buy them.

True, and if Russia's fundamental ideology hadn't been so anti-western ( a legacy of the USSR?) there would likely have been many western corporations more than willing to help them do that and market the products. Instead they look on the outside wealth and covet it for themselves.

Interesting that there is an obvious flaw in that. To take any place over by force, Ukraine, ends up destroying the wealth they so wanted. So the campaign inevitably costs them a lot in blood and resources, but the gain is lost in the process. I wonder if that is a lesson China is getting from it?

Help? Being rotationally-augered is not 'being helped'.

Name me one corporate which went there for altruistic reasons?

They always get a slice of the pie, but if the Russian Government is clever then that slice is less. In the middle East the US and European (Shell) companies took their technology in to exploit the oil, but the Governments and countries still ended up stupendously wealthy from it.

Unless a country is willing and capable of exploiting that commodity and customers to buy it you only have another Venezuela.

With the exception of Norway, most petro-nations are basket cases.

Any of them with half brains are desperately trying to transition away from their oil economies.

Correct! China understand this, and Russia too. Western countries need to stop focusing on the money and start focusing on how they will collate the resources they need to provision their populations in the future.

China takes the long view that's for sure. Note that they don't sell their land, but provide long term leases. We should have taken this route re. our large tracts of farmland we've sold to overseas companies.

If you haven't worked it out, most of what is written on the internet is propaganda of one sort or another. Welcome to the human race.

More "international rules based order" - The United States responded to Griner’s sentence by kidnapping a Russian

Scraping the barrel with that link Audaxes - (one of the few I have bothered to click on)

The Saker of the Vineyard is a blog by a retired Swiss Red Cross officer, residing in Florida and defending Russia against an enigmatic Empire. The Saker has become a franchise for an international network of pro-Kremlin outlets, with branches in German, Italy, Latin America, and Russia. A Saker is a sort of falcon, falco cherrug, endemic to the steppes of Eurasia. The name of the blog is an anagram of the blogger’s name.

The Saker connects Russian nationalist groups and outlets with North American anti-Semite groups; Russian communists with French and Italian right-wing activist. Devote Christians with aggressive thugs. It’s a successful franchise in disinformation.

you forgot the homophobes, plenty of gay bashing in the saker comments section. The blog author even blames the forthcoming fall of the US empire on granting LGBTQ equal rights.

....and Audaxes is the local franchise holder. Just wondering.

...oil prices start down a mere -50 USc from Saturday at just on US$88/bbl in the US, while the international Brent price is now just on US$94/bbl. A week ago these prices were US$98 and US$104/bbl respectively, so basically a drop on -US$10/bbl in that time. That is a drop of -22% from early June, and basically back to prices in effect before the Russian invasion of Ukraine.

I think there is a good argument for the expansion of the SPR next time we have a recession. Clearly we need more leverage to deal with Russia in future.

Maybe we should also be talking about slavery in our own country as well? https://www.stuff.co.nz/business/129496019/blatant-exploitation-migrant…

I just jumped on seek and had a quick look.

Only Villa Maria offering viticulture cadet ships….all other jobs relating to vineyards seem to be management.

looks like the whole industry relies on contract labour for the growing the grapes bit….

Appalling really.

Truly appalling agreed. We have people in this country who are acting as slavers and we do pretty much nothing to stop it, in fact it appears to be encouraged by the frameworks the inspectors work within. We should self report to the UN Human Rights commission IMO, unlikely we have that sort of leadership in this country though. Most Western countries are the same (do as I say, not as I do).

Yeah and then we wonder why we have high youth unemployment.

Companies don’t want or need to provide pathways because they can bring in foreign labour.

Yeah, there is a real disconnect about providing youth with the oppourtunities they need/want and motivating them into that work as well. Labour cozy's up to them, National penalise them. There should be a general agreement that neither approach fully works, there needs to be a bit of carrot and stick. But Nationals onto it but wrong again with their approach. What they should do is do tax changes for young NZers entering the workforce. Allow the companies that employ young NZers for a year to claim half the tax back for employing the young person AND give the young person half of the full amount back on their tax return, or put it in their kiwisaver...

If you think inflation will start to fall now it will still take 18 months till it’s around targeted levels. If the NZD keeps tanking inflation will take longer to tame. Why would they then lower rates again surely not that crazy to start inflation again, I think once inflation is under control keeping rates around 5% would stabilise economy.

Because they have/will overcook their hiking so will need to drop rates back down to a neutral level.

Rates have only just started going up, so many people predicted rates will go back down why would they lend money out 2% or 3% if inflation is 6% banks are in the business of making money not giving it to average joe, people who have mortgages will be paying banks higher rates for years this is their way of recouping back money of households. House prices will continue to fall as so over valued compared to income.

If prices literally froze now and stayed at exactly the same level for ever, CPI would be 5.0% next quarter, 3.5% the quarter afterwards, and 1.7% in March 2023. Obviously CPI would then be 0.0% from June 2023.

Static rates stabilise the economy - it is moving rates up or down that destabilises things.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.