Activity remains robust at Barfoot & Thompson's auction rooms with 349 properties going under the hammer last week, but the sales rate has been in steady decline with less than half selling under the hammer at last week's auctions.

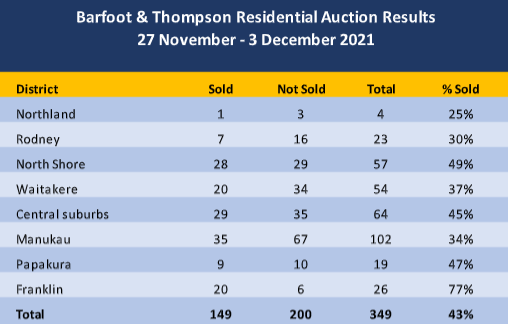

Of the 349 properties offered,149 were sold under the hammer, giving an overall sales rate of 43%, with the rest being passed in for sale by negotiation.

Around the Auckland region, properties in Rodney had the lowest sales rate at 30%, while those in Franklin had the highest sales rate at 77%.

However, Franklin was the only district where the sales rate was above 50%. (See the table below for the full district breakdown).

Last week was the sixth straight week that the overall sales rate has fallen at Barfoot's auctions, with the weekly sales rates listed blow:

- 16-22 October 68%

- 23-29 October 67%

- 30 October - 5 November 62%

- 6-12 November 59%

- 13-19 November 54%

- 20-26 November 50%

- 27 Nov - 3 December 43%.

Details of the individual properties at all of the auctions monitored by interest.co.nz and the results achieved, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

34 Comments

That's pretty normal for December. If we factor in the lockdown, this can also be viewed as a good result. The season has still a long way to go.

There is plenty of room for downward valuation.

Be patient!

Heard that almost everyday and as for today, you're the first.

25 years on and I haven't seen the tooth fairy you and your kind promised.

The signs are there for those not willfully blind to them. Might want to get yourself down to Specsavers.

Be quick!

Na, CWBW is right, those 1 bedroom with study shoe boxes under the power pylons will be selling for a cool $1 Million soon. I mean, who wouldn't want one? Get in quick!

CWBW may be right. It depends what else the Reserve Bank and govt have up their sleeves to keep the housing market pumped.

Allow 35 or 40 year mortgages so we can extract more from younger generations, perhaps? Not so long since they did the same from 25 to 30 years.

While our wealth is based off what debt we can pass to younger generations we'll always need to find new ways to maintain that.

Then extend to inter generational mortgages.

Because it hasn't happened in the last 25 years, makes it more likely to happen. Pressure must be released at some stage, but timing the pop is very difficult.

Unfortunately, that's not true people who are waiting will keep waiting, this is not going to South by any means.

Wishful thinking cannot change reality.

I fear that rents will rise in early-2022 .....

TTP

However, the new rules mean landlords cannot raise rents more than once a year. That will limit rent increases. More importantly, the direction of market forces don’t indicate significant rent increases are likely. For example, the number of rentals on the market in Auckland at present is quite high, and rents are already as high as most people’s incomes can bear. Also people are leaving Auckland, whilst house building is going ganbusters. This all suggests an oversupply of houses in Auckland at least is imminent.

Nah you can't use season as excuses anymore, lockdown is no more too. If it's not summer, spring and winter the good time to buy houses. What are the best seasons to buy houses? ;)

Ain’t really in the mood for houses, everyone is waiting for their holiday getaways. Maybe after Feb.

Sentiment has definitely changed, how long will it last though? Is this just a blip before the madness continues?

Sometimes we're too quick to draw conclusions but 7 weeks of continuously lower sales clearance is a clear trend and' it's down. To those who expect lower prices now, it won't happen yet, vendors will hold off discounting for a while but I do believe prices will soften come May 2022.

PS, it's mostly the lower end houses that are getting passed in, prices are too high for FHB, investors are holding off and many can't get finance. The higher end is still selling well. I expect this to show in the REINZ figures released next week, average and median prices will still be up, the HPI may well be flat.

Correct. The impending credit crunch will take out the market from the bottom first.

I think you're probably right. Inventory will be interesting to watch.

How long will the credit crunch last, seems very much in banks control at the moment...

Hi Chebbo,

When inventory goes up, prices go up.

When inventory goes down, prices go up.

In short, house prices are not beholden to anything.

TTP

That may be how it works down at Property Brokers.

https://comcom.govt.nz/news-and-media/media-releases/2017/property-brok…

In a free market, however, an excess of inventory will usually lead to an easing of prices.

Indeed, a flat period is approaching due entirely to credit control. We are in the process of getting mortgages renewed and it is as hard as it has ever been. There are multiple new controls and increased discount rates to income. Not before time perhaps.

The new normal is one of slowing sales. Speculators and owner occupiers are finding it very difficult to qualify for finance. So it will be like the last couple of years with one very important exception, interest rates are rising, not declining. Those that used central bank manipulated lowering of rates to hold on last time will be facing a very different debt servicing picture.

Kaaarrrkkkkk.

It’s under 50% because buyers can’t go unconditional with the tougher lending criteria. They are all selling not longer after with a subject to finance offers for crazy prices still.

NZD sinking inflation and interest rate up and who knows how high they’ll go average wage earners cannot afford to buy home. You don’t need to be a rocket scientist to see this combination is going to effect housing price just by how much.facts are facts no FOMO can help people pay the debt any one who has purchased a house in last 3 years will be in negative equity this is best case scenario

“….. any one who has purchased a house in last 3 years will be in negative equity in the 18 months this is best case scenario “

And they will lower the rates again to save the economy and people will be buying again. Up down up up down up up up down…

Indeed. I'm predicting 18 months of very difficult debt extensions as some take their medicine. Unless the banks change their lending policy's, who will bail people out at the current prices. Then its the run into the next election so Government will ease off the pressure to win votes.

We are only a small fish in large point if inflation and interest rates are trending upwards in US our government has no choice but to raise OCR the NZD is already under pressure. We all know this housing market has reached the top and it only got there because of ridiculous low interest rates this has cause people to borrow more than they can afford.If interest rates go up 3% which is still low a lot of people will struggle. I think every 1% raise will knock off 10% of house price. It will be the biggest correction in housing ever and this government will not be able to do anything about it and will probably blamed on COVID with a shrug of her shoulders and a sigh.

Housing downturns (assuming we are on the edge of one) usually take years to unfold, with rallies in some area along the way.

Don't eat all your popcorn now - you'll be needing it for later.

This is the impact of the banks tightening up, so we will have to wait until the new year when the banks realise no one qualifies for a mortgage anymore and bring in version 2.0 of the new lending calculators so they actually write some mortgages again.

They didn't tighten up because they wanted to, they tightened up because thats what the new CCCFA laws made them.

You think banks are willing to push against regulations in the face of an increasingly aggressive RBNZ?

Yeah CCCFA but...Banks didn't have to self impose DTI, suddenly stop all over 80%LVR applications or reduce the amount they'd take for rental income etc... They're definitely in control here and are choosing to limit credit....

You clearly don't know much about CCCFA and its interpretation. 2 out of 3 of the things you mention above are reg driven.

CCCFA has got nothing to do with the self imposed restrictions I mentioned...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.