This content was supplied by realestate.co.nz

The latest data from realestate.co.nz suggests that national housing stock (the total number of homes available for Kiwis to purchase across the country) has gone up by nearly 30% since December 2020—an increase of about 4,000 properties.

Vanessa Williams, spokesperson for realestate.co.nz suggests that this data confirms an earlier theory—that the market is becoming more palatable for property seekers. “Buyers across the country have more choice coming into 2022. This could mean less FOMO (fear of missing out) and perhaps even more properties hitting the market,” said Vanessa. “If sellers are confident that they’ll be able to purchase after they sell, we could see this number continue to climb.”

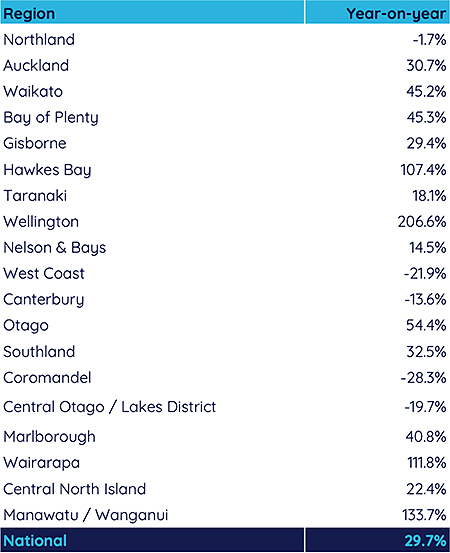

Four regions saw their housing stock more than double year-on-year—Wellington (up 206.6%), Manawatu/Whanganui (up 133.7%), Wairarapa (up 111.8%) and Hawke’s Bay (up 107.4%). Other regions, including Otago (up 54.4%), the Bay of Plenty (up 45.3%), Waikato (up 45.2%) and Southland (up 32.5%) saw notable stock increases.

“It’s heartening to see more housing availability coming into 2022. It looks like there’s an exciting summer ahead for buyers and sellers alike.”

Nine regions hit record-high average asking prices

The national average asking price hit a 14-year record high in December; up 23.4% to $985,245 when compared to December 2020. Nine regions led—Hawke’s Bay (up 36.9% to $865,209), Wairarapa (up 30.1% to $827,766), Bay of Plenty (up 29.1% to $999,978), Central North Island (up 28.8% to $825,617), Canterbury (up 27.6% to $674,222) Manawatu/Whanganui (up 27.2% to $671,958), Otago (up 20.0% to $652,839), Taranaki (up 19.6% to $617,466) and Central Otago / Lakes District (up 19.1% to $1,398,407) all hit 14-year record high average asking prices year-on-year.

“Typically, more stock would result in cooling prices because buyers have more choice, but we haven’t seen that happen yet,” said Vanessa. “If stock continues its upward trend into 2022, it’ll be fascinating to watch the impact on asking prices.”

Central Otago / Lakes District, now nearing a $1.4 million average asking price, holds a firm grip on its reign as the most expensive region to purchase a property in the country. Auckland (up 18.5% to $1,225,265) and the Coromandel (up 25.2% to $1,110,512) follow in second and third place respectively.

Green shoots of new listings spring up across the country

Although December is often a quiet month, when compared to 2020, new listings on realestate.co.nz saw a 5.6% increase. “December is usually a “short” month for the property market—Kiwis are winding down for the holidays, so we usually only see activity to the middle of the month,” said Vanessa. “But with significant restrictions still in place in December, it was heartening to see vendors active right up until the festive break.”

In fact, several regions saw new listings increase year-on-year. Most notably, Wairarapa (up 25.7%), Manawatu/Whanganui (up 22.8%), Hawke’s Bay (up 18.6%) and Southland (up 18.2%), while others, including Gisborne (down -34.9%), the West Coast (down -18.6%) and the Coromandel (down -18.4%) saw new listings decrease year-on-year.

“New listings in each region were very mixed last month—some regions saw significant increases year-on-year, while others seemed to quiet down for the holidays—resulting in a moderate increase in new listings nationally,” said Vanessa.

How to spot a buyer’s market

New Zealand has been in a bona fide seller’s market for about a decade, and the country is a good distance away from anything that looks like a buyer’s market. But there have been several recent reports from experts that predict a range of outcomes for the housing market, including a dip in prices and even a “correction” that would result in a buyer’s market.

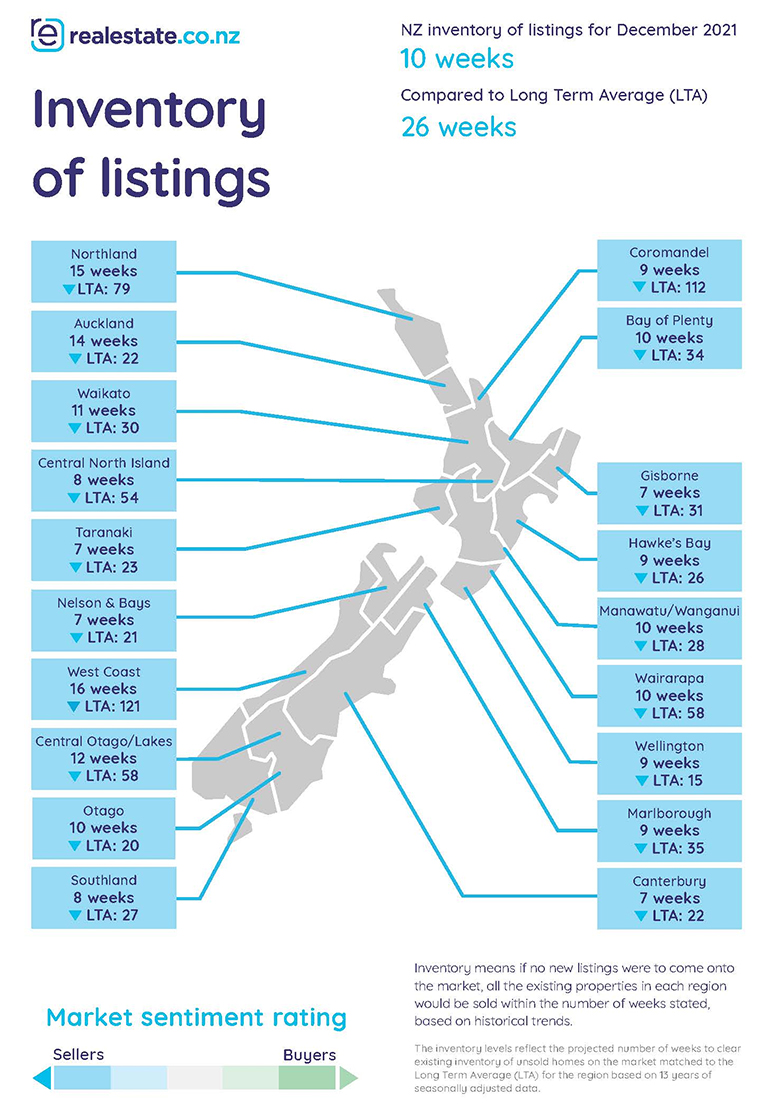

But how do we spot a buyer’s market? realestate.co.nz measures this regularly through our inventory of listings to monitor market sentiment.

“We use sales data from the Real Estate Institute of New Zealand and our own stock data to find the inventory clearance rate and compare it to our long-term average.”

“This gives us a good indication of how each region is tracking—for example, Wellington’s current inventory clearance rate is nine weeks, but the long-term average is 15 weeks. Because December’s clearance rate is lower than the long-term average, this indicates a seller’s market,” says Vanessa.

“This measurement is a reliable indication of market sentiment.”

Housing inventory

Select chart tabs

93 Comments

Would love to see an article on "How to spot a housing bubble".

Could be another quantum year for the housing market……

TTP

https://lmgtfy.app/?q=%22quantum+year%22

Nobody knows what a "quantum year" actually means because it's just spastic estate agent gibberish.

Re “quantum year”, Brock, think of the 2021 housing market….. and you’ll get the drift.

TTP

Then invert it.

In the quantum world, things can appear and disappear in the blink of an eye. Perhaps this is what TTP is predicting for the windfall gains seen in the housing market last year?

Or perhaps a version of Heisenberg's uncertainty principle? If we focus too much on current values, we lose sight of the direction they are heading.

I am wondering how Auckland, Wellington are doing on asking price month on month...

Auckland down 3.6% to $1'225'000

Wellington down 2.5% to $983'000

Full report here: https://www.realestate.co.nz/blog/news/more-choice-buyers-2022-nearly-3…

Thanks Yvil!

Edit *Oh its just an asking price decrease, feel like we saw this last year too...? Let's see if this eventuates into decreased sale prices.

Perhaps a bias to cheaper places hitting the market?

Interesting that de color blue is used instead of red is used for price decreases. I wonder why

Thanks Yvil, that's good info.

Most of the clever investors have sold at or near top.With interest rates raising and inflation high the housing market will have a downturn. I think each 1% raise in rates around 10% will be lost on house price’s.

Time-in not Timing. If I was being clever I may have sold out last March. But instead I did not get my act together so still hold. My sometimes quote is "doing the right thing by doing the wrong thing"

HW2 You would have been to early if you sold last March and a bit late if you sell this March.Like I said November, December was the top not sure how quick it will go down this depends on interest rate and inflation.

Its amazing how quickly Trademe has turned from Auctions to listed prices. The number of listings is marching forth rapidly, every time I refresh the numbers jump up. If you are having difficulty paying that epic mortgage off, or if your genius investment property is making you look like a bit of a fool then there are plenty more just like you. Don't let them beat you to the market, because the NZ housing market has become a game of musical chairs. Don't be left holding that million dollar lemon.

Be Quick.

Yes its a buyers market only when the PBNs and auctions are replaced by a price. Hasnt happened yet.

Depends what area you look. Coming to a town near you, Sooner than you think!

https://www.trademe.co.nz/a/property/residential/sale/nelson-tasman/sea…

Can't remember who shared this website https://propertyprice.co.nz/ but it's certaintly interesting. Some eye watering asking prices in Auckland, clearly Agents/Vendors still have high expectations through Trade me...

Those 3 month old Wellington CV's are already looking ridiculous. All those extra rates being paid for nothing. Councils loving it.

Homes estimate $1.28 million

Sept 2021 CV $1.17 million

For sale $859 thousand (and it is a site allowing townhouses)

https://homes.co.nz/address/wellington/island-bay/6-carlisle-street/DLb…

It looks to me like that is a home that has significant issues - the third option given under build or develop on the ad is "Restoring the current home (full builders report available)." Both the suggestion and the fact that the vendor is providing a builder's report seem unusual to me.

Yeah agree.

As far as I am aware CV's aren't specific enough to take into account leaky building issues.

In 2020/2021 many 'as is/where is' homes sold to desperate FOMO's for 300k and 400k over CV. Not happening no more.

Rates don't work like that - councils essentially decide how much money they need and divide that among all residents based on your house value as a share of the sum of all house values. If all houses double in value it makes no difference to the amount each household pays.

You are highlighting an example of financial illiteracy that I see so often.

Gen X

These are the most happy comments that I have seen you post . . . . this news has been more effective for you than a couple of much needed "happy pills". :)

P.S. Mind you, this frame of mind is not consistent with you owning "multiple properties in a number of countries".

Thanks mate, I am just over the moon that I am not over leveraged here. Some people are about to find out the hard way that borrowing large amounts does carry risk after all. Who would have thought?

"'If sellers are confident that they’ll be able to purchase after they sell, we could see this number continue to climb... Typically, more stock would result in cooling prices because buyers have more choice, but we haven’t seen that happen yet,' said Vanessa."

The problem with the assumption is that there's an expectation on property upgrade or downgrade when there appear to be more inventory available in the market. However, due to credit constraints concurrently created by both RBNZ and the Labour government, that transition may be only a pipe dream for aspiring movers.

Housing in this country is not a normal good; therefore, basic demand and supply do not apply.

With these in consideration, rising inventory availability is likely short-lived and the talk on major prices cooling are unrealistic.

If you have just received your pre-approval to buy an average Auckland house, that option in your hands by itself is worth about $29.6K- yes, that email or letter you got from your bank is worth money, don't see it go to waste!

January-s are usually the dip month for residential real estates in the country. Your opportunity to buy the dip is THIS MONTH. If you're serious about moving into a lovely home to call your own, it's time to cut short your holidays and get out there to find something before Summer comes along and wipe your hopes away.

Be quick!

Reads like an advertisement disguised as an article in msm.

Housing in this country is not a normal good, therefore, basic demand and supply do not apply.

Exactly. Housing is a speculative asset.

Driving round regions there's building going on everywhere and from the sounds of it people are fleeing cities esp Auckland, so you'd expect the listing count to increase.

Could bode well for Auckland prices to rationalise but then again I imagine the immigration tap will be turned on in 18-24 months.

Bit of a crapshoot really, if I were to gamble I'd say the global economy will take a fall first and take us with it.

Lots of rookie developers, with no building experience, using substandard materials due to lack of availability and increased costs, all realizing that they need to rush the job to recoup some losses as prices crash. What could possibly go wrong?

Yep!

Supporting evidence needed to back this up.

Where do you buy substandard materials ? In my experience there are just no materials to be had at short notice. The timber producers are taking the piss (when you consider log prices are 33% down from the 120 a T they were getting), gib is a 12 week wait, gib bought all of Elephant boards stock to keep the ball rolling. The whole sector is maxxed out. I think you will see a lot of vacant sections with consents/plans coming to market shortly.

Wholesalers are using these conditions to jack the prices, best opportunity ever to crank it with little whining from the crowd.

Yeah now is not the time to be going for consent on a new build with the intent of hocking it off for 20%

Pa1nter,

"if I were to gamble I'd say the global economy will take a fall first". Why do you think it might and what will be the catalyst?

NZ has relatively more gas in the tank, as in, lower public debt, and room to move on interest rates (albeit not much), and half decent fundamentals to survive in the short term.

Covid is like a cattle prod that is and will shake vulnerabilities in economies across the world. We can see fractures in the Chinese economy already, many parts of Europe were already on the ropes, you've got countries like Lebanon and Turkey suffering eye watering inflation. Covid relief monies are coming to and end, and were more needed elsewhere to prop up economies.

As for the catalyst hard to say.

EROI. Already happening. Like the boiling frog.

Agreed. We are but a dot on the vast ocean of global printed speculation. China and or the US are emitting popping noises, and Europe continues to be a mess. What could happen indeed.

How you you spell yield again....?

Anecdotally a lot of small builders going bust or just shutting up shop due to severe materials shortage.

One builder I know has told his staff that they are welcome to take casual or seasonal employment for now as there just isn’t enough timber to do any jobs with.

Not to mention materials destroyed by the weather due to lockdown/border controls. There is a half built house getting demolished around the corner from me due to the framing being weather damaged. I suspect that will cost the builder and the first home buyers who were building it very dearly.

There are many reasons the framing should be H3 treated, this is just one of them. We never learn in New Zealand however and continue to build potential rot boxes.

Auckland leads the way...in up as well as when falling.....

https://finance.yahoo.com/news/fed-vice-chairman-to-leave-two-weeks-ear…

Fed Vice Chairman Richard Clarida will leave the central bank two weeks earlier than planned, following increased scrutiny into financial transactions he made ...

......Will they and do they work for economy and public at large or for for self. In USA it is stock and house, whereas in NZ it is mostly housing...how many of those decession maker has used their power to increase their wealth.

Great news from the stables says the "Crazy Horse" .... let's see if we can get the total stock of all NZ residential property to have a market cap. of say at least 5 trillion kiwi pesos ! .....happy daze are indeed ahead for all you "astute" investooors out there ! .... neighhhhhhhhhhh ! he says, diving back into that bucket of oats !

I did the sums recently and If house prices doubled every ten years then the average NZ house will be "worth" $1 billion in 100 years time. From memory the average wage would be something like $1mil P/A at 3% inflation from here, so houses would be 1000x income. There are people that honestly believe that will happen. I guess some people will believe everything they hear from a Church...

Unless there is a civilisation ending event it could end up something like that, with almost everyone dependent on the govt (so house prices irrelevant) and a minority of robotics geniuses earning 9 digit salaries (or profits or something) competing with each other for real estate in safe pockets with no view of the slums.

Fossil fuel dependancy will do the trick just nicely. We are so far off sustainable its not funny.

It all makes a lot more sense when you realise that:

- The lower quartile of the housing market is now propped up by accommodation supplement ($30m+ a week of Govt money going into sustaining current prices!)

- The top half of the market depends on (a) what buyers can afford to pay, which is a function of interest rates and equity levels, and (b) buyer confidence in future prices

Higher interest rates will slow the growth down, but, given home owners have $1 trillion in equity, and accommodation supplement is being thrown out of the door, how likely is a drop of more than a few percentage points?

The accommodation supplement affects rents, yet at current prices and interest rates rental yields are pretty bad. Unless the supplement increased significantly it won't prop these prices up very long.

..it affects rents and mortgages. Home owners get it to.

Add to this other govt efforts such as Kainga Ora buying up existing homes and one can see how govt is encouraging this housing ponzi balls up.

Surely the current levels of subsidy can sustain current prices - unless a significant % of landlords are still on very low (or negative) yields because they were banking on capital gains?

The average house is now $1 million. The average rent would need to be 50k a year (1k a week) to get just a 5% yield before expenses. No one is investing in property for the yield anymore.

In fact the median rent in NZ is now $560 a week ($29,120 PA assuming fully occupied), the median house price is $1mil, so current average yield is 2.9% PA before expenses. Take out rates (say 3k), insurance (say 2k), maintenance (say 5k), empty periods (say 1k), and it is 1.8%. Without capital gains (and now without tax advantage), why would you bother?

Why for altruistic reasons of course. Where would people live if we didn't have landlords?

We have some fine upstanding citizens in this country, they deserve something special...

Yes, I was specifically talking about the bottom quartile of the market. My hypothesis is that the floor price for a small family home in low decile urban areas ($500k - $600k) is determined by what people on low wage and / or benefits can afford to pay in rent. This in turn depends on accommodation supplement. If you run the numbers the yield comes out at a bit over 4%. Take out rates etc and this drops to about 3%. It is pretty crap, granted, but a major drop in prices at this end of the market looks highly unlikely.

Correct.

The accomodation supplement is a huge part of the problem.

You are not wrong with your reasoning.

But a minor caveat would be that the peasantry occupy the slums, so the "price" of the average rental will be a bit lower than the average price for all houses.

But the point still stands, indeed, it is a speculative mania and it can only end with serious wage inflation (currency debasement) or a serious asset correction.

You've owned the property for more than 36 months?

How many properties are actually leveraged¿ Bernard Hickey recently reported only around a third but I cannot find that reference. He also reported the 'collective LVR' is only around 20%.

Will still be appealing because its 1.8% leveraged off your fantasy equity?

Not 1.8% on your actual cash/savings?

Same old comments from the same old people as prices just continue to rise. Some people need to react to change and adapt instead of living in denial. BOP has had some of the highest gains over the last year and had I "waited and watched" on the sidelines then I would have been screwed.

Carlos the same old people will be right one day, I guess the question is when. The longer away the "when" is, the bigger the collapse.

Some people (and I know many) cannot react to this change - they are in a poverty trap. You need to mingle a bit more with the have nots.

No thanks. I think you find most people tend to mingle with those of a similar social standing. You find that friends come and go in life because of it.

Have most of your friends been on the gone side, it must be tuff being so high on social standing ladder (anyone for tennis).

I didn't realise they played a lot of tennis down in ten dollar Tauranga.

..which explains your ignorant attitude to the plight of those who are stuck - and the govt policies that are keeping them there.

No. We need houses prices to go down. We are hands down the most expensive place to buy in the developed world with one of the lowest population densities. Its manipulated and purely credit based speculation.

Anyone arguing against this comes from a place of Greed. Or just having being engrossed in this way off life for too long. Or just has the blinkers on. But either which way it's a national embarrassment we've let it get this far ahead of us.

Like any impending revolution or Disaster, we can head off the worst effects with relative small changes now. Rather than wait for the social or economic explosion that will follow. Here's hoping the cccfa is the catalyst for the correction we need.

A lot of places being removed, or demolished around the place. Then nothing, but an empty section. Building is slow around here! So we get a reduction of homes, while we wait!

There's blood in the water for sure based on the emerging property data shared in some posts here. I thought the interest rates would be the main head wind but it looks like the tightening of credit is eclipsing that by some way at the moment.

It feels like we're approaching a tipping point. If the interest rates go up again at the next review then we may see a run as investors in particular decide to pivot out of residential property.

Omicron may have other ideas and we may see a postponement all of this due to a change in Government behaviour around rate rises, border opening, subsidies and so forth.

If I was a betting person, I'd say the traffic light system will endure with us remaining domestically pretty open to the vaccinated, and Orr will have to respond to the inflationary pressures with modest, slow upward changes in the OCR. This will signal investors that the chances of more cheap money is now too small to expect a revival of the housing furnace and the exodus will gain momentum.

A house is only worth what a bank will lend for it.

West coast of SI stock of 4 months. Sounds bad? Nope, the usual is ten years inventory! Crazy.

I'm putting Auckland market keeps a nice steady increase all year, most likely around the 1.2 to 1.8% monthly, got the last two years bang on so going for a third year... Come on baby

~18% rise in the face in increasing interest rates, hostile credit markets and hostile regulations? I'll bet against that all day long.

Yeah is he up for a wager?

Past performance is no guarantee of future results

New Zealand manages to out-bubble even Canada.

https://www.youtube.com/watch?v=mEgCI5fd5s4

Trudeau and Arderp are so alike with their uselessness and waffle it is uncanny.

Add Macron to that list seems like a mummy’s boy takes he’s ball home if you let him score

Great Vid. Don't they just ooze insincerity. Trudeau could be a really slick North Shore agent. Funny how they mention Canada as being the second worst bubble. NZ punching above its weight again.

A match made in heaven! The king and queen of phoney virtue signaling!!!!!!!!

Have Yachts and Have Knots

Mate, Vaxinda made me cringe even more after that very early, awkward exchange by her about Trudeau was mentioned. It was like an awkward teenage crush. Gross. She's shameless in her posturing and virtue signaling. I hope she leaves.

Border reopening is coming... eventually.

New year, same headline. Property the only game in town. Brock and his DGM crew remain in the mud. The majority of these comments are misery merchants trying to speak a crash into existence. Zoom out from those charts and the price direction only moves one way! Buy the house or get left behind, it really is that simple. No sympathy for those who can't get this.

Looks like we have a fresh minted real estate agent in town?

Its so boring all the sheeple ness in this country. Everyone go and do something meaningful with your life, one day youll be dead - Epitaph - the best housing BBQ chat - Did not achieve.

I find your lack of brain cells disturbing.

B727 - I have been on both sides of the property investment fence so your characterisation of my thoughts on the property market are as accurate and polished as your other “views”. Your post has the whiff of desperation. When you have to resort to trying to whip up investor interest on a site like this you should just be honest with yourself and sell before you drown.

B727 I think you do have to appreciate there is now a huge separation gap between those that are in and those that are locked out. We now have a very divided society and you would have to make some pretty big compromises to get into a house that the next generation are not prepared to make. The end result is a percentage of the population that are now pissed and DGM struck.

20 years time. A Melinial dominated parliament votes in a death tax. 33% of your estate thank you very much.

They will need it to pay back the govt debt and help fund the cost of climate change. Which present generations are doing thier best to ignore.

Social revolution doesn't need to Come with guillotines.

EXACT detail needed and is missing.

Total stock is to what is available.

Stock OTM is what they mean.

Also and crucially, WHAT is OTM.

In Orewa 75% of what is listed is not built yet and price is not what it will cost in end if developers having trouble finishing them.

People who currently live in the house to sell are the crucial variable and this is not separated out.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.