The number of properties being auctioned by Auckland's largest real estate agency is down by half compared to a year ago, and the sales rate is down by two thirds.

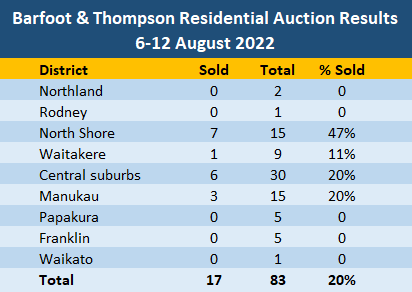

Interest.co.nz monitored the auctions for 83 properties put under the hammer at Barfoot & Thompson's latest auctions (6-12 August), compared to the 163 residential properties the agency auctioned in the equivalent week of last year (7-13 August 2021).

That's a decline of 49% in residential auction activity compared to a year ago and the sales rate has taken an even bigger tumble.

Of the 83 properties offered at Barfoot's latest auctions, 17 were sold under the hammer, giving an overall sales rate of 20%.

That compares with an overall sales rate of 61% in the equivalent week of last year.

At the agency's latest auctions the number of properties on offer ran into double digits in just three districts - North Shore, Auckland's central suburbs and Manukau, while none had sales in double digits.

The table below shows the district-by-district results.

Details of the individual properties offered at all of the auctions around the country that have been monitored by interest.co.nz, including the prices of those that sold, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

91 Comments

Brutal. Who’s wasting their time going to auctions these days? Much better to wait until the sale changes to ‘deadline sale’ then ‘by negotiation’ and then wait a few more weeks before starting negotiation.

House down the road from us sold at auction a few weeks ago, not sure how much although I was told the venders were willing to meet the market (I’m sure they always say that). I was expecting it to sit around for months.

Auction is still the way to go if you have cash, but I guess for many people a house is just a house but if "The One" you really want goes to Auction you go to the Auction. Some pretty smart cookies still buying at auction, watched one last week not get a single bid then sold by negotiation straight after. Its all tactics now, you let the seller see there was no interest and they lower their price expectations and you swoop in and pay just a bit over the June 2021 RV now.

If you paid above 2021 RV in Auckland, you've most likely paid too much.

I'm starting to see a few places sell below 2017 RV, such as this one:

Interestingly, put up for rent at the start of August - so probably bought by a cashed up investor:

Err house is North Shore / Rodney area that's hardly Manukau is it. Decent relatively new builds so modern building codes with double glazing and a decent North facing aspect with north facing decks and a view. You still get what you pay for that hasn't changed and it will never change.

Looking at the REINZ data for Auckland, it is relatively safe to say that if you bought last year November, you didn't "get what you pay for". You paid too much for what you got.

Who knows what the future might bring.. but we might be having a similar discussion about those North Shore / Rodney area houses you mention in a year's time.

P.S. People living in Mellon's Bay will argue that Mellon's Bay (where this property is situated) is hardly Manukau. East Auckland and Papatoetoe are rather different in many ways.

Howick Pakuranga is definitely part of Manukau. It's right there. Just cause some pretentious people think of manukau as Otara, Manuela and Papatoe doesn't stop the fact of Howick and Pakurangas location. Which is miles from Rodney. That house looks oldish as well.

You really don't get what you pay for in New Zealand. To put it into real estate speak it's a beer lifestyle on a champagne budget.

Something to enlighten you about 'Manukau':

"Rodney is made up of 11 suburbs. The most expensive suburb is Red Beach, which has a median house price of $1,397,400."

"Manukau is made up of 39 suburbs. The most expensive suburb is Mellons Bay, which has a median house price of $2,209,600."

- December 2021 data Source: https://www.opespartners.co.nz/property-markets/auckland#section-17

If you're hoping to 'get what you pay for', you should consider buying in Melllons Bay in Manukau (yes, Manukau!) rather than Rodney.

Yes perception of ‘Manukau’ seems to be merely the poorer suburbs of Manurewa, Papatoetoe etc. Much much wider than that, incorporating some quite high value suburbs.

Yep lots of really nice areas of manukau, lifestyle blocks, sea views.

Sold at below RV seems to be the new normal. Definitely more and more listings, and I suspect not the "spring" factor. Buy and flip is not the theme, for whatever reasons.

A decline in auction numbers is normal for a soft housing market…….

But the tight labour market and wage growth combined with much lower than anticipated mortgage interest rate increases explain why the housing market correction is proving less arduous than the usual suspects here would have us believe.

Make the most of discounted prices and good choice while you can. Don’t be too surprised if the housing market firms up through early/ mid 2023.

TTP

Oh Timmy - i don't often read the comments just for laughs but when i do i love reading your troll like hyperbole.

Mastery of the Art of Trolling requires walking a fine line so the trollee does not realize that they are being trolled.

Tim The Pricefixer is more like the Comical Ali of the Great Property Crash.

we all know the tune 'cos we've heard it ad infinitum spamming the airwaves : "property brokers cuntry ... robbing me with pride"

Another daily dose of hopium. You’ve picked the worst time to do the whole “contrarian” shtick TTP, especially considering the macro still has more pain to come. NZ’s economic and property nose dive is far from over there captain.

Nevertheless, keep up the floundering damage control, it’s very amusing.

Tim says "Make the most of discounted prices and good choice while you can"

The resident "cut n paste" bot with a vested interest in fleecing the naive just made another buy now recommendation. Lock it in folks!

"buy-now pay later"

Retired Proppy

You would have seen the story how a 26 year young man now owns over 50 properties. He is the exception but it is still a possibility for gen z. He is looking to buy more

If you're suggesting this person is a role model to aspire to then did you also read about the disgraced, bankrupted fraudster now jailed ex-Real Estate Agent and the money hungry Church Pastor. These were once role models too. All have one thing in common - GREED.

Owns 50 properties at $20m, $400k each average. $11m debt, could be paying $550k interest alone per year unless locked in a low interest rate over the last couple of years. Where are these $400k apartment/houses, how much do you think they rent for?

If the market drops 10% from there he’d be below 40% LVR, would the bank let him refix or is this considered low equity high risk?

Put it this way, you buy one $20m property with a $9m deposit. If that one property value drops to $18m, you’re below 40%. The bank isn’t going to loan you more money. Would they let you refix or force you to sell?

I don’t think I’d like to be in his shoes with that more than everything you have invested in property, difficult to get rid of if you need out.

Could also be a chance he is just lying his ass off.

lol

Its a bit of a slap in the face for many kiwis having this promoted around the news. “You too can own 50 properties! You just have to get off the job seeker benefit, claim your free grand incentive, and buy up!”

He's a symbol of excessive leverage built on lofty property valuations. All appears good on the surface until one day its not.

I can imagine you trying to achieve half of what this young guy half your age has done if you had half the chance. Those "lofty" valuations have to fall by about half to have totally lost out. Seriously as long as he continues to pay his mortgage he has no worries.

Being up to date with mortgage payments does not insulate oneself from bank enforced consolidation in a declining market. This debt junky is nothing more than a caretaker of his banks security 💲⬇️

Who do you think holds the upper hand here?

Sir, "Who do you think holds the upper hand here?". Thank you Great One. Your opinion really matters to me.

The fact that someone so young and so dumb could have borrowed so much money just shows how far removed from reality this market has become.

This young "success symbol" is losing something like 50k to 70k a day, and seems oblivious to just how much trouble he is in.

It might take him months to realize that all liquidity has gone out of the market. Good luck finding a buyer for your 50 crappy rentals, dude.

Two points Fitzgerald

Losing 70k per day amounts to 25.55m over 12 months on a portfolio worth 20m.

Those "50 crappy rentals" as you eloquently describe them seem to evoke some strong emotions from others who feel left out from owning just one of them

So how can we work out how much he is losing a day? How much do YOU think he is losing everyday? Let's spitball this.

Ive now read the article... although life is too short to make a habit of reading the Herald... and it says his average unit costs $400k. So obviously what the Herald calls a "property" is some cheap kind of joined unit. The technical term is "crappy."

The national House Price Index (HPI) was down 1.4% in July. IF he owned 50 median priced houses he'd have lost 1.3k on each of them, every day in July. But he dosen't. So let's use the (probably bulls×t) numbers the Herald gave us. His portfolio is "worth" 20 million so if he lost 1.4% on that in July that it is $280,000 this month. Roughly $9,300 a day.

But medians and averages can be a bitch. Do they directly apply to this guy? Probably not. And the Herald numbers are suss. He could be losing 18k a day or "only" 8k a day. Won't know until he goes to sell. Or try to sell. In an illiquid market.

How much money do YOU think he is losing every day? How much money are you losing every day? Is there an exit plan? I highly recommend one because it will be getting harder and harder to escape the black hole that is being formed in the nz property market. Need that buyer, otherwise you're stuck on a fast ride to the bottom.

I am sorry to break this to you snowflake. He probably knows how to add value to a property... so therefore lost little to nothing and may have made a gain. Providing he keeps serving his mortgage and his equity stays greater than 20 percent he would not have anything to worry about. By the time he is 50 he will have a mortgage free income stream.

OK, so you don't want to talk numbers. You want to just hurl random insults around.

Possibly it is too painful for you to look at the numbers. I'm sorry if that is the case.

Problems generally don't just go away if we ignore them. They generally get worse. Anyone who is losing 1k+ a day would do well to face the problem square on and work on an exit strategy. Be quick though because it is getting harder and harder to cash out.

Are you the guy from the article HW? Or an associate from the property investor association?

He's probably former commentator "Houseworks". There's a builder with a company in Auckland called "Houseworks", wonder if it's the same person.

Haha nice try Nzdan. There's someone here by the name Nzdano, is that you?

HW stands for HeadWinds as that is what its been and the 2 is for the squared sign. Apology if its ambiguous

Unfortunately not!

"Now is probably an easier time to get equity because there are less people buying and less competition," he says.

Heh, well, less people buying, less competition, less capital gains. What equity is he "getting" anyway when he leverages 100% of the purchase price? Does he think values are moving up? Or is he a Dunning Kruger that thinks every purchase he makes is well below market rate and then tells everyone he's made xx% equity from such a smart buy?

https://www.nzherald.co.nz/nz/aucklander-jonathan-brownlee-owns-51-prop…

Another way to look at it is to realize that if he "owns" 50 median priced properties and they are all falling in value by 1.3k a day (as per latest market data), then he is losing 50k+ a day.

Monopoly money.

Hopefully he knows he is in a declining market and leverage does work in reverse. So based on what happens in the next couple of years he is going to continue to triple down on debt and more houses, or ....be bankrupt. I had a friend in a similar position before the GFC and he tripled down. He got wound up owing around $20m...

Gambling.

Don't you think there is something very wrong in somebody that own 50 properties and "need" more of them?

I for some reasons deal with several gen z and I assure you that none of them ever expressed admiration for something like that. You might have a different experience.

You assume that is envy, if/when people like me feel bad in knowing about those situations.

The reason why I feel bad is because that challenges my value system, not because I want what they have.

Surely I desire a nice place to live and where I don't have periodic inspections, possibly debt free. The reason why I want that is because that would help me in spending time in things that matter to me more (working less, playing piano, growing vegetables, holidays with family, fishing, studying, drawing, writing, meditating).

The problem is also that the kind of greed that enable the behaviour of that guy (and probably you) is an obstacle for people with way less needs.

I'm not even sure why I am commenting, you obviously are from a different planet than me. You can't understand why I consider toxic that behaviour.

This is a brilliant comment and I wish I could cut and paste it to use as a reply over and over again.

Using the "you are just jealous" line is a bit like saying that the kid being beaten up by Sam Uffendil is just jealous that he dosen't get to do the beating. Like he is just jealous because he also wants a bed leg to use against smaller kids.

In reality, there are many good people who just want to live a good life, and want to see others have the same opportunity. Not everyone is a greedy controlling narcissist. And it really does seem that most landlords are blind to the social harm they cause.

Rather than focus on the personal character of someone who owns multiple properties, I'd rather focus on policy: should we, as a society, allow one individual to own 50 properties? There is nothing written in stone that says we have to, and many good arguments against it. And that, of course, is only one aspect of the legal property framework that has seen values explode to a point that they are completely out of line with average incomes. No reasonable person denies that this has been a terrible thing for NZ society at large.

A good first step, in my opinion, would be to institute a property register for all landlords. Let's see who owns what, how many mega-landlords, how many mum-and-pops, etc. After that, we can start thinking seriously about how to redirect largely speculative property investment into more productive areas of the economy.

You are focussing on the wrong thing. And by the way it would be very easy to spread ones investments across multiple entities.

There is basically not enough properties available to satisfy need. The reasons for that are 1 under-investment in drainage infrastructure by councils. 2 Idealogues who got voted to councils in the 90s and 2000s who basically torpedoed intensification. If that had not happened there would have been decades of extra homes built. I don't know if you noticed but the thousands of home units built from the 1960s to the 1980s and even though some were not maintained well, have served us incredibly. Households have got smaller over the years and the one and two bedroom units have been pretty useful

"There is basically not enough properties available to satisfy need"

There are enough properties....just not enough properties to satisify the greed of people who think its their right (and need) to own more than one (at the expense of people who simply just want to own one to raise a family in and have security).

Sounds like what a ticket scalper would say. Well if they don't want me scalping tickers, they should hold more concerts. 27% of NZers are born overseas, we must have built a fair amount of houses as everyone I know lives in one.

That is just a mean spirited response pal. The rental shortage is the reason the govt is reversing its interest deductibllity rules

(behind paywall)

How landlords reacted to the Government U-turn on tax breaks for long-term investors

https://www.nzherald.co.nz/business/how-landlords-reacted-to-the-govern…

The article says that "tenants have been vocal in expressing how their rental prices were increasing and they do not have a good supply of rental accommodation to meet their needs"

Property values are affected by a raft of policies including interest rates, independently of supply and demand. Indeed, such investor-friendly policies have been a huge driver on the demand side of the equation. Imagine how much (less) demand from property investors there would have been over the last 20 years, holding supply constant, had their been different policies such as CGT, no interest deduction, bright-line tests, etc. It's a big over-simplification to say that current values are a result of low supply.

I didn't mean to suggest that mega-landlords are the main driver, either; that's just the issue that I was responding to. And totally agree that under-investment in infrastructure and nimby-led aversion to densification have contributed to the problem.

One just needs to look at RBNZ C31 Total Borrowers see the demand in action. 2014/2015 the average amount borrowed by investors frequently rose higher than FHB by up to 12%. From 2016 to today investors average borrowing was $0.88 on every $1.00 FHB.

- 2014 (Aug to Dec) - 8,138 FHB vs 23,465 Investors

- 2015 (Full Year) - 22,254 vs 65,419

- 2016 (Full Year) - 23,506 vs 62,832

- 2017 (Full Year) - 21,685 vs 41,032

- 2018 (Full Year) - 26,486 vs 40,605

- 2019 (Full Year) - 28,719 vs 36,371

yes,plenty of old dungers on big sections languishing on trademe now that landgrabbers have lost their appetite.

While I feel the odds are stacked against TTP, I have seen plenty of other commentators being laughed at for similar comments and then being proven right. I commented at the start of the pandemic that I thought Covid would increase housing demand and got about 100 comments saying that I was an idiot.

There is definitely a chance that TTP is right and this is close to the bottom, particularly if interest rates continue to track down.

I’ve been sitting on a thought for a while. What would sentiment be in the market if house prices and interest rates are both comfortably retreating? Tomorrow is always a better time to buy, a cheaper house at a lower rate? A couple of people I’ve been talking to (one investor and one FHB) were in a hurry to get their finances together and buy before interest rates really took off.

Affordability at an all time low still, either we roll back to emergency OCR levels or house prices continue to fall to meet the market.

Advised a guy at work to avoid going large on debt for a bigger house middle of last year. He is now stoked, as he would have lost circa $40k per month since if he had.

He will wait longer and continue to watch, building cash and no debt.

Kaaaarrrkk.

Wow I got 5 likes. TTP must have logged in with all his accounts.

Would be funny, if only it wasnt so sad.

Now that the truth is allover the main media it must hard work posting such all over the place, and liking multiple times. Perhaps his agents are using their increasingly spare time to help...?

Its a fizzer more like it. At best it may recover, at worse expect it flatline for a few years.

I am picking mid 2023 too. The returns are still shite, if you were buying now for investment , what will be your buying criteria be ?

I won't take your word for it John.

To be fair I don't want a recession, but unfortunately the prices are to high for average incomes, prices still have a long way to go. Be great when some of these landlords who are over leveraged need to firesale quickly, then maybe prices will be more affordable.

Weren't you on above average income with the high sales revenue from your business products. To me it seems the outlook looks a bit brighter than it did six or eight months ago. I know the median says that prices are still dropping

No just a bit over the RV for a really nice place is the current normal in Auckland. Give it another couple of months and who knows, will most likely be below RV then.

Down down down ... is the theme in recent days..

Be it auction numbers, sales numbers, immigration numbers, job growth and finally House prices....

Not a bad theme if you ask me!!!

Soon it may be employment numbers that are down.

Might be time to sell some of those rentals Markus.

Still the fall is not as much as it should be.

Till the fall is between 20% to 30% will be cosmetic keeping in mind the Big and fast rise.

Still a long way to go.

It has only just begun

6-B63-A0-C2-C953-413-E-B5-E6-20-C2366-E7-DF1 — ImgBB (ibb.co)

As per chart Manukau city is just 2% away from being officially termed as crash

If anywhere deserves to have a massive drop in value it's Manukau, what were people thinking...

Yep: Manukau, Hutts, Palmy, all we’re selling for prices similar to much better areas. They have to go down the most surely.

No that’s not correct. Even during the silliness of the boom places in Manukau were still significantly lower than ‘better areas’.

Depends what you mean by better areas. Places going for like 1.5 mil in bad parts of south Auckland, you would get something ok on the shore for that, not in a flash area of course, but much better.

As per chart Manukau city is just 2% away from being officially termed as crash

Sorry, taimaiakka0, but there's no "official" definition of a crash.

The only thing that's crashed around here is the credibility of the DGM - which is lower than low.

TTP [MNZM]

It's a crash when I say so

DGM

Tim reminds me of Orwell's Ministry of Truth from 1984. Only he gets to decide what the truth is and if the way reality is playing out doesn't meet his own personal agenda, then he get to change what the definition of the truth is.

'A property crash used to be agreed to be more than a 20% fall in prices, but because this would mean that I've been wrong all along when I said that property prices could never crash in New Zealand, I've decided to change the definition of a crash to a fall of 80% or more...now get back to buying houses please from my property brokers agents because I've got money to make from this market....and remember its always a good time to buy property from property brokers because house prices never crash in New Zealand!'.

I’d call it a crash when a large percentage of people are forced to sell. Until then I’d call it a correction of crazy Covid prices.

And to that extent, the key question is what happens with unemployment. If it goes to 5-6% by mid 2023, then I think there’s every chance of a further 10-15% fall from here.

Tim (MNZM) - do you still hold the NZ order of merit after the pricing fixing scandal? Must be a pretty low bar these days...order of merit one day...fleecing people of their hard earned money the next with deceptive trade practises.

Then employing 700 people in the property industry, then spending time on interest.co.nz (and other online forums) trolling people and potentially misleading buyers into thinking that house prices could never fall so that they continue to buy more property and improve your company's profitability (and your personal wealth).

Nothing deceptive about this sort of behaviour eh (again) - like what you have already been found guilty of by the NZ legal system....

The cruel irony is that he paid for his NZ Order of Merit, using gains from deceptive trade practices.

taimaiakka0, but there's no "official" definition of a crash.

For NZ's house market to avoid a crash, we'll have to continuously redefine the term 'crash' over the next few months/years. Similar to the way the house price growth forecasts are now constantly changing.

TTP, like the US democratic party, will be like the Ministry of Truth from Orwells 1984. They will change the definition of what a recession is or what a property crash is so that they can say 'see look, the Ministry of Truth is never wrong - we told you there will never be a recession or a property crash and there never was a recession or a property crash'.

It all about controlling the narrative - that is where the 'elite' politician or property investor type has got to (perhaps not just in NZ but across the western world)...its all about trying to control the thinking of the people so that they can continue to enrich themselves at the expensive of others.

You start thinking...are we actually any better than the CCP that we like to look down upon for spinning lies and pushing them onto people as 'the truth'?

Unfortunately there are still a few people around who can see through the BS and that is why they have to be silenced....hence why I've found myself being ridiculed by the likes of TTP, P8 and CWBC on here when you point out their mis-truths that they try to push upon people (for their own financial gain).

Auction...fail. Price by Negotiation...no response equals fail. Deadline sale....fail. And the finally a rediculious price listed. All that happened is 2-3 months have been wasted on a falling market, and potential buyer conditioned to wait for ever lower reality.

Must be frustrating for agents who can see the truth.

The covid boom of cheap debt is being unwound, and fast. Please recall that price was already artificial due to previous high debt tax avoidance stupidity. Will not be surprised if we get to 50% off peak or thereabouts.

The only real question is when the banks start shooting the overly speculative...?

Some forgot the key rule in realestate over the last couple of years: 'location, location, location'... unfortuantley some will learn the hard way if they have to sell shortly...

Shoeboxes in the middle of low value suburbs like Papatoetoe will be vulnerable. Anywhere close to a train station in low value suburbs might be a bit more resilient.

I think the All Black v RSA win tells you NEVER follow the crowd. The ZB Friday night sweepstake with Marcus L, was for a RSA win but look what happened the ABs beat them well. Same in property market when everything looks grim follow your own instinct and make your own luck.

So the propertyganda market is all just a game based on luck? One thing is fer sure, it's a game of two sides.

With such an ability to spin a line I think you should be a lawyer. And parliament is full of bs talking lawyers who no one trusts.

The reference to making ones own luck is based in someone's ability to work hard and produce results. Enjoy the day

But wasn't the story when prices were going up is to follow crowd, and the mantra was be in quick before it goes up. Now its never follow the crowd. I definitely won't follow crowd. Some people have made money buying property, but as a whole its not great for country having all disposable income going toward property. If people are not following crowds lets look at productive businesses, that get income virtually from overseas, outside box thinking not low low low real low hanging fruit.

Yeah I agree wholeheartedly. Tbh we will never compete on the world stage of trade apart from agri mainly. Our hunger to compete stemmed from the 80s free market mantras and user pays. Trouble is there's too many lazy sods now who are not really contributing much, there is a lot of absenteeism from school so the next generation of adults will be lost

Not so sure about that. Being absent from the current school system might well be a great advantage amongst the next generation of adults!

Faaar out

So auctions are going badly , no surprises there....

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.