Tower Insurance premiums are set to change, as the insurer uses more detailed modelling to price flood risk.

Nearly 90% of Tower customers can expect the flood risk portion of their annual premiums to fall by an average of $25 when their policies next come up for renewal.

The remaining 10% can expect increases; the majority of these hikes being worth less than $50 a year.

However, around 250 Tower customers will see increases in the flood risk portion of their annual premiums worth hundreds of dollars.

Tower chief executive Blair Turnbull told interest.co.nz the insurer will contact these customers to see if they can make savings by watering down their cover, by committing to paying a larger excess for example.

Turnbull said Tower would also consider spreading the premium rise across a few years, to prevent customers having to absorb the hike in one go.

He assured, Tower isn’t pulling cover from flood-prone areas, saying it isn’t “embargoing any regions or areas”.

However, Turnbull suggested the insurer wouldn’t regret it if the price hike prompted high-risk customers to drop off its book.

“There might be some specialist providers out there that provide you with better cover,” he said.

Note, the change relates to the flood risk portion of premiums, not home insurance premiums in their entirety. So, while a Tower customer might pay less for flood risk, their premium might still rise overall.

Change signalled

As technology improves and the cost of natural disasters increases, New Zealand’s major general insurers have been using more granular modelling to price risk.

They made headlines in 2018 when some customers saw their premiums jump as risk-based pricing was applied to the earthquake risk portion of premiums.

The change was such that it prompted some Wellington apartment owners to ditch their earthquake cover altogether. Others are paying astronomic body corporate fees to account for the rise in insurance premiums.

Tower’s move in a similar direction, when it comes to flood risk, has been signalled for years.

In 2018, interest.co.nz spoke to the chief risk officer of Risk Management Solutions (RMS) - a risk modelling giant that works with insurers around the world. Robert Muir-Wood said RMS had provided New Zealand’s major insurers with quake risk modelling and was doing more in the flood risk space.

That work is now being used by Tower. Turnbull said the RMS model is built using data obtained from the likes of the National Institute of Water and Atmospheric Research, Land Information New Zealand, local and regional councils and the Insurance Council of New Zealand.

“The benefit of using the RMS model is that it is so detailed that neighbouring properties can have very different ratings, depending on the camber of their land, whether they have a flood wall, and other factors,” Turnbull said.

“It means we can predict the impact on the individual property based on how it is constructed, height, number of floors, materials, and flow of the water.”

Vero already using risk-based pricing for flood risk

Asked by interest.co.nz whether someone who struggles to get affordable cover with Tower will likely struggle to get cover from one of the few other general insurers in New Zealand, which are likely using the same modelling, Tower’s chief underwriting officer Ron Mudaliar said different insurers have different risk appetites, so will use the data in different ways.

Interest.co.nz asked the country's two largest general insurers to explain the extent to which they're using risk-based pricing when it comes to flood risk.

Vero's consumer insurance executive manager Sacha Cowlrick said the insurer has been using a risk-based approach for some time, but it is only one factor that influences premiums.

"Models are also only part of the equation, as flood risk can depend on a number of things including the style of a home, the location, claims history and surrounding environment," she said.

"Our understanding of flood risk is always evolving and we continually review our approach..."

IAG's chief financial officer Alistair Smith said, “We regularly review our pricing to ensure our customers are paying a fair and appropriate amount for their insurance...

"We are closely monitoring the evolution of the external environment. Our priority is to continue to be there for our customers when misfortune strikes.”

Risk shifted to taxpayers

The Reserve Bank is mindful that changes in insurers’ risk appetites could expose parts of the housing market and thus the banking sector. This is partly why it's focussing more on risks related to climate change.

The situation also poses a problem for the Government, which might ultimately have to step to support households or institutions in the event of a disaster.

Accordingly, last month it announced it’s taking on a whole lot of risk from the private insurance industry.

From next year, the Earthquake Commission (EQC) will cover the first $300,000 of damage to a residential building in the event of natural disaster, leaving a homeowner’s insurer to cover anything above this level. Currently, this cap sits at $150,000.

From October 1, 2022, EQC levies will accordingly rise from a maximum of $345 to $552 per dwelling per year. Private insurers collect these levies on behalf of EQC by tacking them onto the premiums they charge for fire cover.

Hikes in EQC levies should technically be accompanied by cuts in premiums charged by private insurers.

Transparency key

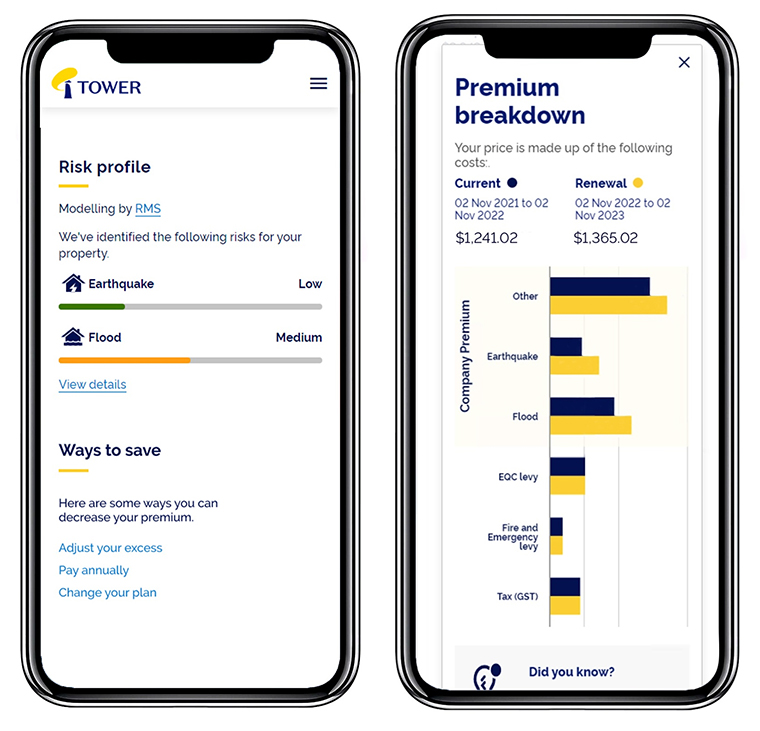

Put to Turnbull that all the moving parts in the insurance pricing space could see unreasonable price hikes get lost in the wash, he said Tower was committed to being transparent and clearly communicating the composition of premiums with its customers.

Tower customers that log into their ‘My Tower’ online portal, as well as prospective customers who request a quote, will be told in plain English what their flood and earthquake risks are, and how their premiums are composed.

Here’s an example of what they’ll see:

15 Comments

Risk shifted to taxpayers

...anyone else sensing a theme these past 4 or so years? Or is it just me?

chebbo,

Perhaps some of the risk could be placed directly on the consent granting authorities-on a personal basis and on the developers.

In an article in the Herald in late Sept. there was this; "Head of Auckland Council's Healthy Waters Dept., Andrew Chin says that they would prefer development not to occur on floodplains, but the demand and pressure from from the housing market makes that unfeasible. 'With land being in such short supply , there's a lot of pressure to be able to modify floodplains and create more housing', Chin says".

Perhaps if he and those above him knew that they could find themselves personally liable for permitting building on known floodplains, they might be less inclined to do so. The developers could be similarly at personal risk.

This is an interesting emerging story. I think (but cannot be sure - so it could be useful to get a comment from them) that it is not only freshwater inundation that is included in their definition of "flood risk" but it also includes coastal inundation/erosion risk. And (again this is a guess) they (Tower) may be applying this to all properties identified as being within the coastal environment as defined by the NZ Coastal Policy Statement (NZCPS) and mapped by local authorities under the RMA/NZCPS district planning rules.

The thing is, a coastal environment under this RMA/NZCPS legal definition is very wide For example, in the Kāpiti area, nearly the whole of the district is defined as part of the coastal environment.

A friend nearly a km inland with a house sitting many meters above sea level was charged this new risk premium by Tower. Their property is not mapped in the district plan as being in a flood nor a coastal hazard area (two quite different mapping requirements undertaken by councils). They successfully changed insurers (who did not see them as a flood risk) as a result.

My point is that coastal environment as defined under RMA/NZCPS will capture a significantly wider area in many cases, than a mapped flood or erosion hazard area/zone.

It looks like the definition of "Coastal Environment" needs to be clearly defined by all users Kate. Misapplication of the term could equate to abuse of it and customers if, as in this case, insurers are using it to justify additional premiums.

But my concern is how insurance companies work. When calculating premiums, they include the likelihood of events including 1:10 year, 1:100 year, 1:200 year and so on. And these all add a factor to the premium, some only cents but others dollars. Insurance companies pay out claims from the pool of premiums collect, plus rely to varying extents (mostly a lot!) on reinsurance to cover large claims. Indeed as I understand it, insurance companies re-insure their entire risk portfolio, and make claims against that reinsurance for all payouts, and it is the premiums which fund the reinsurance. Any money not paid out in any one year is raked off as profit to shareholders. and this is where the problem lies.

Others have identified that there is not enough money in the world to cover all the risks that insurance companies have taken on, but where they factor in rare events, which don't occur, they should retain those portions of the premiums in a fund to build up over time to enable them to cover the risk they take on. An obvious benefit is less reliance on reinsurance, but other benefits would also be transparency that would enable customer to better assess the viability of the company, and for regulators around integrity.

Definition of coastal environment under the NZCPS

- the coastal environment includes:

- the coastal marine area;

- islands within the coastal marine area;

- areas where coastal processes, influences or qualities are significant, including coastal lakes, lagoons, tidal estuaries, saltmarshes, coastal wetlands, and the margins of these;

- areas at risk from coastal hazards;

- coastal vegetation and the habitat of indigenous coastal species including migratory birds;

- elements and features that contribute to the natural character, landscape, visual qualities or amenity values;

- items of cultural and historic heritage in the coastal marine area or on the coast;

- inter-related coastal marine and terrestrial systems, including the intertidal zone; and

- physical resources and built facilities, including infrastructure, that have modified the coastal environment.

That's great, but how do insurers define it?

They (I assume) simply use the online GIS/mapping tools provided by local authorities - all that data is stored in these GIS systems and is publicly accessible. So, if you are searching features for "coastal environment" on a GIS mapping tool for most local authorities (NZCPS was implemented in 2010, so most should have mapped it by now) - you will automatically get all the properties defined as such under the NZCPS (that NZCPS definition is above). It (the definition) is much wider than simply flood hazards.

This is what concern me.

I think your assumption is reasonable Kate, as is your concerns. I think insurance has become one of the great rip offs as opposed to a reasonable means to offset risk.

Bob Jones always argued that one should always aspire to become self insured. A somewhat mercurial chap, he was often entertaining in his musings, but his opinion was usually well supported.

Requested a quote form Tower a few weeks ago. Asked if the council had noted anything about my property. If there is its in the LIM and i don't have one. In any event I don't have a natural flooding issue. Also something to the affect regarding natural disasters. I indicated that New Plymouth could be subject to earthquake and volcano eruption.

"...... as well as prospective customers who request a quote, will be told in plain English what their flood and earthquake risks are, and how their premiums are composed......."

So much for their risk assessments. If Tower have already marked out the areas subject to various natural disaster risks they need to let their sales team know.

Insurers, along with Bankers, NZ's biggest gang.

May find this of interest also...

https://thespinoff.co.nz/business/05-11-2021/bernard-hickey-the-100b-cl…

I think it's fair that home owners pay the premium for the coveted sea view.

The general tax payers should not be sponsoring a selected minority who have exquisite tastes for water.

This of course translates into all forms of insurance including ACC, life and business insurances etc. There should be much higher levels of responsibility incorporated into the sources of inputs in universal insurance pools. This would increase costs for those with lifestyles and incomes that are a direct impact on the common good, ultimately shifting behaviour, away from negative societal behaviours towards more conscious lifestyle and business choices overall. I am more than happy to supplement payments for someone else's proactive and preventative healthcare costs eg quit programs, dietitian, mental health supports etc, but less happy to pay for smoking related cancer treatments, lung transplants, or pollution cleanup claims from fossil fuel corporations etc. It would be best then if we could also then give financial breaks to those who are taking REAL proactive action to resolve their negative impacts while ensuring equity for the underprivileged, even if this creates some further complexity. We need solutions that direct behaviour towards the common good.

The real story here is you need to think about more than just which way is North and where your sunshine is coming from. You now want "Elevated" and I don't mean on the edge of a cliff. Anything in a "Hole" or low down in a possible flood plain is a no go. Anything near or at sea level is obviously risky. If you can mitigate severe weather damage then insurance becomes less of an issue.

Living next to but above a flood plain is great. Means I can never be built out or have neighbours. Including 3x 3 storey house next door. I highly recommend it. House fully insured and no issue getting insurance.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.