By Jenée Tibshraeny

If I was doing my due diligence on a property I wanted to buy, consulting different insurers would be top of my priority list.

Since the 2010/11 Canterbury earthquakes, we’ve seen insurers use more comprehensive data to price earthquake risk.

This has seen some property owners’ premiums sky-rocket – disgruntled Tower customers making mainstream media headlines.

Looking to the future, I believe insurers will use increasingly sophisticated data to price flood risk in a more granular way too.

I recently spoke to Robert Muir-Wood – the chief research officer of one of the world’s leading risk modelling companies, RMS.

RMS has provided the earthquake risk modelling used by the major insurers in New Zealand and according to Muir-Wood is looking at doing more work on flood risk.

While insurers already have tools to measure flood risk, one can only imagine the availability of additional data would prompt them to be more specific about the areas they hike premiums.

We are of course already seeing this, with property owners in parts of Dunedin, Napier and Wellington in particular, struggling to get insurance cover.

But my guess is, even better data will equal even more granular pricing.

There is of course an argument that more flood risk-based pricing is a good thing, in that it would encourage developers to avoid investing in coastal places prone to flooding and make councils more aware of where they’re consenting building.

However as KPMG NZ’s sustainable value director, Charles Ehrhart, pointed out when I recently spoke to him, risk-based pricing has social repercussions policymakers should keep an eye on.

In other words, what happens if entire neighbourhoods can't get insurance, so then have to default on their mortgages? Are these poorer communities living in lower lying areas to begin with too?

Both the Commerce and Consumer Affairs Minister Kris Faafoi and the Reserve Bank are aware of these issues.

In its biannual Financial Stability Report, the Bank warned: “While more risk-based pricing may be an efficient response to having more data, if taken to an extreme it could reduce the risk-pooling benefits that insurance provides.”

Reserve Bank Governor Adrian Orr also warned in a media conference on the Report that the Bank was looking to ensure insurers were thinking long-term and not just seeing risk-based pricing as a money grab.

Deputy Governor Geoff Bascand added the Bank was going to start talking to both insurers and banks “more purposefully” to make sure climate risk was built into the way they managed risk long-term and at board level. He said their response couldn’t just be an immediate price one.

Interestingly, the Reserve Bank in its Report said it wasn’t sure whether the insurance pricing we’re seeing now is reflective of where the market cycle’s at, or a more permanent change of approach from the industry.

“In the case of earthquake risk, the prevalence of risk-based pricing partly reflects some insurers having limited capacity to take on additional earthquake risk,” it said.

“Their capacity is influenced by a combination of their (i) level of catastrophe reinsurance, (ii) appetite for earthquake risk, and (iii) earthquake risk exposures from existing policies (particularly in Wellington).

“More generally, higher insurance premiums and more stringent underwriting criteria are typical of a tighter phase of the insurance cycle, and tend to coincide with reduced risk capacity and less competition, particularly for higher-risk insurance business.

“At this stage it is not clear whether recent changes in the earthquake insurance market reflect these cyclical factors, or whether they represent a structural shift towards higher premiums and more restricted cover.”

Evaluating risk looking forward, not back

Right, so it’s quite possible that I’ve jumped the gun by assuming that when RMS does more flood risk modelling, we’ll see premiums change like they did when new earthquake risk modelling was applied.

I would still be paying much more attention to the risks insurers see before buying a property, as more broadly speaking, the Reserve Bank is “coercing and/or incentivising” more long-term thinking from insurers and banks when it comes to climate change.

In its Report it said: "Lenders protect against the risk of losses on loans by assessing the value of property security, assessing the capacity of borrowers to service their loans, and requiring ongoing insurance coverage in loan contracts.

“To work effectively it is essential that these processes are calibrated to longer-term risks, including climate change.

“This may mean placing less reliance on backward-looking valuation models, strengthening serviceability tests to incorporate the potential future variations in insurance costs, and investing in systems to monitor ongoing insurance coverage and exposure to physical risks.

“The Reserve Bank will engage further with banks and insurers to understand how they are incorporating these and other climate-related risks within their businesses."

Put in other words by Orr: “What we are seeing is financial institutions talk about what they’re doing around their own personal carbon footprint, but not necessarily about how they are then putting that into their lending and borrowing thoughts.

“And this is where we have to move rapidly. There’s going to be regulatory impost, there’s relative consumer price impost, and part of that will come through financial pricing, and it has to hurry up.”

So there you have it. The Reserve Bank is pushing financial institutions to factor climate change into their business models.

I am taking this as a signal to factor climate change into my personal financial decisions.

39 Comments

All are welcome in Hamilton, possibly one of the safest parts of NZ, low risk of quakes, floods and other natural phenomenon.

I remember when they were looking at where to build a north island electricity control centre, that Hamilton was selected because it did come out ahead.

Now, regarding property insurance, I suspect that many people when faced with a ridiculous premium, would just not insure their house. (If their bank would allow it). Because the previous govt showed that after the Chch EQ, it didn't matter if you had insurance or not.

Bit of a risk for other issues. But by upgrading to RCD fuses will remove the electrical fault causing a fire, one.

Then there is always the fallback beg-a-little option.

Bollocks re CHCH. what it showed was insurance Cos could make really stupid decisions and the insured could go for the lowest premiums and when the hit the fan the government would bail everyone out.

On the other hand The government thought they could just take uninsured s property , courts said no.

Orr needs to read the AR5. “In summary, there continues to be a lack of evidence and thus low confidence regarding the sign of trend in the magnitude and/or frequency of floods on a global scale”

Indeed. It's all been a bit of damp squib really. Global Cyclone Energy trend for last 45 years (inconveniently flat): https://www.thegwpf.com/content/uploads/2017/11/global_running_ace-1-10…

{kind=link}

Lack of evidence does not mean it is not happening, but rather there is insufficient historical data at a global level. Rainfall distributions are changing and some places are getting drier. SR15 has more detail and is more up-to-date than AR5.

No Simon it does not have more detail or up to date information. Almost all of it is the opinions of a small group of scientists often using the impossible RC8.5 or altering assumptions in new models that can't even hindcast properly.

https://judithcurry.com/2018/10/18/remarkable-changes-to-carbon-emissio…

"floods" yet other physical events such as wind, drought can also cause huge losses and deaths.

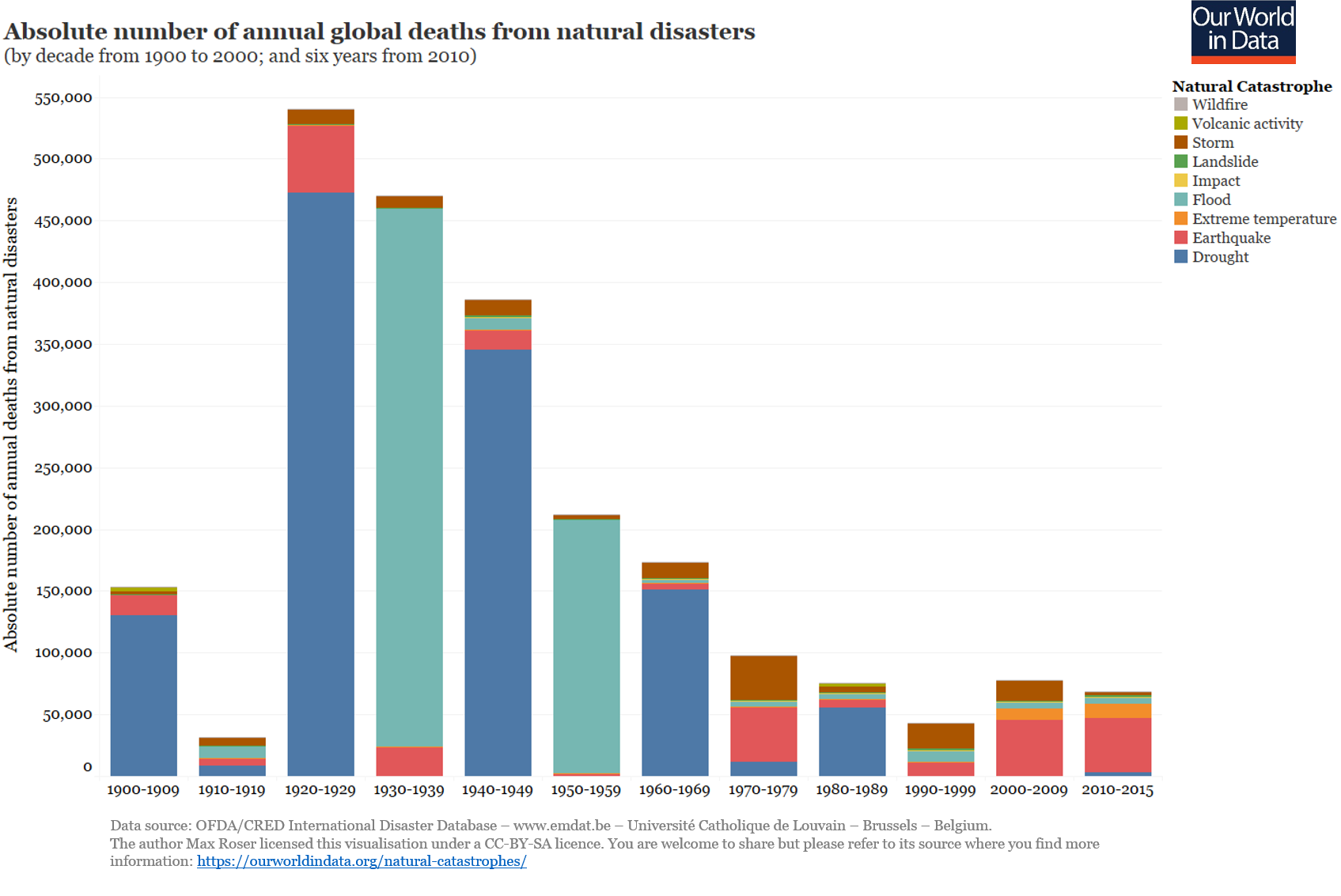

Absolute deaths from natural catastrophe has plummeted over the past century even as population has increased. Humans are very adept at mitigation. Losses when normalised - like with the hurricane data - show no trend.

https://ourworldindata.org/wp-content/uploads/2014/06/Absolute-number-o…

{kind=link}

What is the back pocket hit?

Orr has spoken. Climate change is real and hitting our back pockets

and how much is that back pocket hit?

The americans are saying climate change could reduce a 300% increase in GDP by 10% (300% - 10%), or (300 * 10%), in 80 years time. 80 years is a long time,

whats the calculation for New Zealand?

because we gotta do a feaso,

what (resources+people) and when (time) we spend on

what are the outcomes we are buying (type) + (value)

https://nypost.com/2018/11/28/the-media-got-it-all-wrong-on-the-new-us-…

Even more dramatic was CNN’s headline, screaming that “climate change will shrink [US] economy” by 10 percent, a figure also repeated on The New York Times front page.

Actually, the UN’s climate scenarios envision US GDP per capita will more than triple by the end of this century, so this 10 percent reduction would come from an economy 300 percent larger than it is today. A slightly smaller bonanza, in other words.

But the 10 percent figure is itself dodgy. It assumes that temperatures will increase about 14 degrees Fahrenheit by the end of the century. This is unlikely. The US climate assessment itself estimates that, with no significant climate action, American temperatures will increase by between 5 and 8.7 degrees. Using the high estimate of 8.7 degrees, the damage would be only half as big, at 5 percent.

Gotta love the tease lead-in for this opinion piece (one needs to remember that the "opinion" designation provides a complete clearance for factual or non-factual reporting... "opinion" means that it is just the writers opinion, regardless of any inconvenient facts that are in opposition to the opinion of the article. The primary two sentences for the title of this opinion piece... "Orr has spoken" with the second sentence "climate change is real and is hitting our back pockets". Well, these two statements are entirely unrelated, regardless of the salacious headline intimation of linkage between the two. Fortunately, this screed is filed under "opinion". Sadly, some readers on this site may not apply appropriate discrimination between "opinion" and "news".

There may be some serious issues in regards to the effects of climate changes as to how insurance costs may change for some locations. Sadly, this screed does not discuss the reality of how this may happen. Yes, prior issues with earthquakes may have large influences on future insurance costs. This is *entirely* unrelated with climate change, whether anthropogenic or otherwise influenced. The headline for this opinion article is rather silly...

Thanks for sharing your "opinion" Yankiwi.

Sadly there are likely to be credulous people out there that would believe from this article that Orr had stated a connection between climate change and increasing insurance costs. There is a misrepresentation of truth, which is apparently okay if filed under "oplnion".

The extrapolation for finer insurance discretization for flood coverage is good, I hope that it happens as I appreciate appropriate accountability. The association of Mr. Orr with increasing insurance costs due to climate change is bereft of fact.

That's your take on one headline Yankiwi. You appear to read way too much into headlines, in my opinion.

You are in the business Gareth. You should know just how much importance a headline has in opinion shaping. To invoke a modern equivalent of Godwins law, I saw a headline recently that stated (paraphrased, I do not remember the precise wording, but I think this is correct) "NFL player dies after hunting trip with Trump Jr". The article actually had the truth, which was that a bit over a month and a half after doing a hunting trip with Trump Jr, an NFL player succumbed to complications from injuries received during his days playing gridiron. This was a case of a factual headline that implied something entirely unrelated to the underlying truth. Headlines matter. To pretend differently, well... my opinion differs! :)

I'm not saying headlines don't matter. They are there to give a summary of the story and entice readers into reading it. But they are not where a story starts and finishes. I agree your Trump Junior example is a nonsense but that has nothing to do with interest.co.nz. Must be getting late in the year as I am getting irritated by things I would normally ignore!

Gareth, so you are okay with the headline that says "Orr has spoken. Climate change is real and is hitting our back pockets." This headline has a fuzzy reference to the stated opinion in the above article that flood insurance may change in the future if insurance companies use more accurate data on local flood risk.

Orr made explicit mention about financial company carbon footprints, as well as a more vague comment about assessing climate related risks. So far I have not seen anything about current insurance price increases due to the increased insurance risks from a changing climate, or that Orr has spoken anything close to the claim made in the click headline.

Yankiwi - read the quotes properly in the opinion piece, the RBNZ's latest Financial Stability Report, and this speech Orr did in September. Also watch the press conference on the Financial Stability Report. You will see the RBNZ is increasingly recognising that if banks and insurers don't consider climate change in the way they lend, insurer properties, etc, this could affect the stability of the economy.

For example, if insurers decide they no longer want to provide cover for a seaside community, or that they're going to start charging really high premiums for cover, because sea surges mean it keeps getting flooded, then property owners in that community may have to default on their mortgages as a condition of getting a mortgage is having insurance. This could leave banks exposed, as they'd struggle to sell the properties.

These issues are all front of mind for banks, insurers, reinsurers, and local government. My headline said - Orr has spoken - because the RBNZ is speaking more about climate risk under Orr's leadership. I said climate change is hitting our back pockets because upping prices is one way financial institutions will try to reduce their exposure to climate risks. Seaside communities affected by rising sea levels are already paying more for insurance and in some cases struggling to get cover.

See these stories for more on this topic:

https://www.interest.co.nz/banking/96859/reserve-bank-climate-change-st…

https://www.interest.co.nz/insurance/89029/how-longer-term-insurance-po…

https://www.interest.co.nz/insurance/82617/environment-commissioner-war…

https://www.interest.co.nz/insurance/85037/banks-dont-know-how-vulnerab…

The link between bank mortgages and insurance availability should not be understated. An example: as soon as the extent of land elevation reduction (and resultant increased flood exposure) in eastern CHCH became known, the banks were quickly onto the implications. They took a detailed interest in repair strategies, particularly whether the house was going to get new foundations elevating the finished floor levels. I understand at least one bank had a dedicated unit that reviewed each such case with an emphasis on the debt to equity position and the extent the bank wanted to remain exposed for the future and imagine they will have built on this expertise and experience since the CHCH sequence.

We have some commonality in viewpoint. I agree with the commentary from Adrian Orr that the financial industry needs to have long term planning for the effects of climate change (that is, in the future). At present there are no discernable increase in costs due to climate change here in NZ, insurance or otherwise. The financial stability report notes this via descriptors such as "long-term" "will", etc. The September speech touches upon this long-term planning need. There is a question as to just how far out these costs will start to accrue. At present, the other financial risks listed in the report have far greater importance in the near term, orders of magnitude greater. Fifty years from now is another issue. As to current costs incurred due to climate change, those are negligible at present.

Some of the coastal insurance issues predate or are unrelated to climate changes. Coastal erosion here in Hawkes Bay is a serious issue, and sea level rises in the future may increase the erosion issues. Some of the causes are very much man-made, although not due to carbon emissions or sea level rise, but instead interruptions to the shoreline material migration. Also, we should understand that the shoreline is not unchanging, People should not expect the shoreline to remain in a fixed location despite there being very strong evidence to the contrary in the distant past, due to natural forces outside of anything anthropomorphic.

To your last para: I am regularly amused at the articles and TV clips about properties at imminent danger of being lost the sea or river flooding, almost always overlaid with portentous pronouncements that never quite state global warming is responsible, but its malign causal influence is always implied. The same locations are almost always a roll call of place names that were intimately familiar to me from decades ago in a previous life as an underwriter. They flooded back then and continue to do so.

and that (orr's position) is an entirely correct position based on the weight of scientific and loss data ie evidence, supporting that "opinion"

In terms of facts the re-insurance industry clearly sees increasing risks and costs due to climate change and hence that is actual facts.

This is economics based the very first graph shows the move....

https://www.youtube.com/watch?time_continue=24&v=44yyedSX6XU

Top 10 US hurricanes if hit in 2018

1-1926 Miami $235.9B

2-1900 Galveston $138.6

3-2005 Katrina $116.9

4-1915 Galveston $109.8

5-1992 Andrew $106.0

6-2012 Sandy $73.5

7-1944 Florida $73.5

8-2017 Harvey $62.2

9-1938 New England $57.8

10-1928 Florida $54.4

I assume that you are quantifying the ferocity of these historical hurricanes in terms of their financial damage, discounted up into 2018 terms. OK. But there would have been some others which didn't hit major population centres, or before these population centres were so developed.

Also its US only and only east coast at that.

The venn diagram the two elements, "west coast US hurricanes", and "significant damage" is rather empty. In the past century, there were a total of four tropical storms that made landfall. No hurricanes (or cyclones for that matter).

You are right - 3 of the 10 worst occurred in the last 13 years is statistically unlikely so likely caused by an extrenal factor rather than randomness.

So lets change that order a bit into a timeline.

8-2017 Harvey $62.2

6-2012 Sandy $73.5

3-2005 Katrina $116.9

5-1992 Andrew $106.0

7-1944 Florida $73.5

9-1938 New England $57.8

10-1928 Florida $54.4

1-1926 Miami $235.9B

4-1915 Galveston $109.8

2-1900 Galveston $138.6

Between 1992 and 2017, 25 years averaging a major event every 6.25 years. ***edit*** If we include PR in 2017 that is a major event every 5 years.

Between 1900 and 1944 44 years and average a major event every 7.33 years

Or between 1900 and 1925 25 years, 2 major events

Or between 1926 and 1950 25 years, 4 events.

Or lets average a bit between 1900 and 1950 50 years and 6 events / 2 = 3 events per 25 years..

Kind of points to bad news when even using your own data points an acceleration on events and costs looks clear.

This also is cherry picking US land based events only and not the entire hurricane basin.

By extreme cherry picking you are missing some big ones, eg Puerto Rico, 2017 $91Billion. Arguably should be included as an American dependency, except by Trump supporters I guess.

The US has the best data. You don't go to Puerto Rico for it's historic weather data. Drop the authors a line and tut tut them on their "extreme cherry picking". "Consistent with observed trends in the frequency and intensity of hurricane landfalls along the continental United States since 1900, the updated normalized loss estimates also show no trend."

https://www.nature.com/articles/s41893-018-0165-2

The writing was on the wall back in the mid 70s with the ozone layer stuff..

Since then this climate warming / change thing prediction has changed in predictions, but basically, more storms higher sea levels etc has been constant.

Now apply simple common sense.. who would buy a home , or build

on a moving river sand bank with know history of moving?

Or on a hillside that has slipped badly?

or on a river side in a position that is known to flood?

Or a clift sight, know to be slipping away for the last 30yrs at least?

OH yeah an ex long term Auckland mayor to retire to..then complain his backyard and house has fallen over

So what id the difference in someone buying in these places having read newspapers for the last 40 or 50 yrs continuously talking about rising seas, big storms etc?

Plain bloody common sense that eventually insurance will become a problem in their lifetime, and therefore future financing.

Yet here we have people, and most of them should know better, now complaining about insurances etc

Insurance companies, banks should have been upping and refusing clients in suspect areas for at least the last 30/40yrs...

If they have , those of us with a little common sense in buying with common sense would now be paying far less

And of note: so many of these ppl with lack of basic common sense happen o be business/ government , even ex PMs multi millionaires...

Go figure.

And the headline conflates CC and tectonic risk. It matters not one whit how much or little we attempt to influence the weather in 2118, to them Tectonic Plates sitting underneath us all. They go PING at intervals and in places that no 'Science' is able to predict, let alone mitigate. Poster child Kaikoura, which is proof against rising sea levels for the next few centuries at a minimum.....1.5-6 metres of land uplift in a single event.....

"proof against rising sea levels for the next few centuries at a minimum." A huge call on your part Waymad.

The older lower Kaikoura business area on the banks of a flood prone estuarine river remains exposed to sea level rise. But a good chunk of the residential and more modern commercial areas of Kaikoura weren't and won't be thus affected. South Bay on the other side of the Kaikoura peninsula experienced significant uplift and has probably enjoyed the reprieve Waymad postulates. But in almost all other areas of this impressively altered coastline, there is only a tiny number of people that would have been/will be affected.

Insurance companies accept that human-influenced climate change is real and are willingly refusing business - that's all the verification people should need. Money talks.

I note this GWPF link posted in the comments above has the tagline "Common sense on climate change" - so they are the self-described arbiters of this thing called common sense, eh? Sounds more like a front for conservative think tanks invested in fossil fuels who have an interest in obfuscation and doubt.

In other words, what happens if entire neighbourhoods can't get insurance, so then have to default on their mortgages? Are these poorer communities living in lower lying areas to begin with too?

=====

This will be coming, if nothing else the re-insurers will refuse to re-insure. At that point yes ppl who bought in areas with high CC risk find their premiums either take off or they can get no cover.

Not so sure on "poor" areas as beach fronts etc tend not to be poor spots and also many poor rent?

======

Both the Commerce and Consumer Affairs Minister Kris Faafoi and the Reserve Bank are aware of these issues.

======

news to me, yet they dont seem to be saying much

======

In its biannual Financial Stability Report, the Bank warned: “While more risk-based pricing may be an efficient response to having more data, if taken to an extreme it could reduce the risk-pooling benefits that insurance provides.”

=======

So the careful people who for 20+ years bought with an eye to the effects of CC are expected to in effect pay more for insurance to subsidise ignorant or wilfully so climate deniers purchases in now becoming really obvious high risk areas.

I kind of expect that the Govn of the day will be forced to provide state insurance for the un-insurable.

It's irrelevant whether already occurring climate change is increasing premiums or if Orr was simply observing a truism that underwriting capacity is determined by the cost and availability of reinsurer capital which in turn is strongly influenced by investor perceptions of the risk of climate change; whether justified by evidence or exaggerated by the global warming industry. The net effect in terms of underwriting capacity is similar and Orr is right to call the risk out.

"why you should spend more time talking to insurers before buying a property "

indeed, councils have been knobbled in court by the developers and current owners of properties not wishing to see the value of their investment plummet. This is effect means a would be buyer has little he can do but ask the insurance company, if they will give an answer though.

The climate is changing as it always has.

Never included with these sensational statements is how much of the current changes is caused by natural effects. It is immediately assumed it is all anthropogenic - a most unlikely scenario.

Stating that temperatures have risen by ~ 1º since the start of the industrial age - mid 1800's is quite correct - but to not add that this was in the middle of the little ice age is grossly misleading.

Why not take a longer period and state the temperature today is very close to that experienced in the medieval warm period circa 13-1400.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.