We know the cost of insurance premiums is rising, but Interest.co.nz wants to get a better idea of just how much.

Official data confirms insurance costs are rising fast. The Insurance Council releases data – on a very delayed basis – that shows Gross Written Premiums (what customers pay) rose almost 11% in 2022 from 2021.

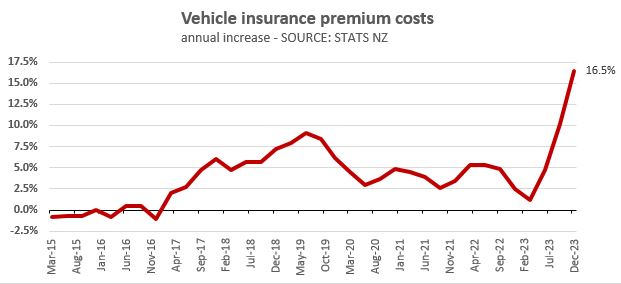

Statistic New Zealand’s Consumer Price Index (CPI) data shows insurance generally up 11.9% in the year ended December 2023.

Although this data is useful, it’s also out of date.

While the official data confirms the rapid rise in costs, detailed information about specific types of insurance, such as car, contents, and home insurance, remains scarce.

We also know that understanding one’s insurance needs requires significant effort.

This often leads individuals to rely on insurance brokers, who are ostensibly free but are ultimately paid by insurers – meaning there will always be that nagging feeling they don't ‘really’ work for you.

We understand a proper insurance decision needs to primarily focus on coverage, not the premium cost. But as households are suffering from increased premium costs right now, we want to start there.

This means, during March 2024, we are running a first crack at seeing if we can pry open some meaningful detail that is actionable on the household kitchen table.

We’re asking readers to help us paint a better picture of what insurance costs look like for you right now through our first reader survey.

Our aim for the survey is to provide actionable insights into insurance premiums, starting with car/vehicle insurance.

We want to see if we can address that lack of consumer-related information and we’re keen to hear which insurers charge what, where, and by how much premiums are increasing for readers.

In the survey, we are asking readers just about price/premium information. Interest.co.nz can find the information needed about the coverage/conditions/policy details to round out the reporting on the issue.

No personal identifying details are required or collected – we neither need or want to know your name or address, for example.

If this survey gives us useful results, we plan to conduct this project annually, expanding coverage to other insurance products.

The survey will remain open throughout March 2024, with results analyzed in April and reported in May.

Your contribution matters. You can take the survey here. (Opens in a new window.) We would love it if you can share the survey among friends and family.

Interest.co.nz is committed to providing unbiased information to empower consumers in their insurance decisions.

19 Comments

The survey page has a pop up requiring me to log in with a Google account to complete it. Is that necessary, given you aren't collecting e.g. names and addresses? Cheers

Thanks for letting us know that was popping up, we didn't realise that setting was on! We've just turned that setting off so you should be able to access the survey without needing a Google account to complete it now

It does get complex - faced with a 15% higher premium in December I of course looked around and wanted to go with Cove, but on review the scratches on our 10-year-old car caused them to cancel the offer to insure.

I adjusted the agreed value to get the premium down of course and stayed with the same insurer - eventually on the phone I asked about my ~50 y.o. brother driving the car, since it was more than 3 days a month he was added to the policy. This brought the premium down about $50, so... guess that's ok after all.

Would be good to be able to lodge more than one entry for multi car households

This is a survey that wants me to log in to a Google account that immediately means the results will be read by Google and tracked.

While I understand you do need to establish that you aren't getting flooded by bots or farmed accounts, Google is likely not the way to do it because of the trust and anonymity issues with them.

Thanks for pointing out that the survey was asking submitters to sign into their Google accounts as we didn't realise until now. We've just turned that function off which hopefully helps

Definitely :-) And done it. Interested to see the results - do you build in a service rating for the insurers?

Just a hint for people looking around trying to minimize the premiums they're paying. Two questions:

1. Do you really need the cover?

2. Do you really need such a low excess?

Both questions are related. They require you to think about what level of loss you can wear before the insurance policy you've bought starts to cover further losses.

For example, we barely use our car and its worth (as an insurance write-off) less than $8k and we could get a replacement tomorrow using the RCF. The only cover we have is 3rd party and the excess - what you pay before the insurance starts paying - is $30k. The premium is tiny. The same goes for our home. We can wear the first $100k without much trouble so the excess is $100k. The premium is likewise tiny. The same is done for our rentals. And life insurance? What's that? ;-)

In essence, we are 'self-insuring' with the policies acting as Excess of Loss cover (a re-insurance term for an insurance company buying cover for itself should a sizeable claim be made). Businesses do this all the time.

Alas, poor Kiwis aren't taught this at high school so they just buy whatever insurance companies choose to sell. "Shopping around" when the insurance oligopoly are all selling the same crap products makes no sense.

(Do I need to mention, once again, that Kiwis aren't that bright? But I may be being a tad unfair here as I have 15+ years exposure to high-end commercial insurance where policies are individually written and re-insurance arrangements are either custom bought and/or are part of billion dollar treaties, etc. Amazing what you learn doing stuff like that.)

Did you have to go offshore to obtain effective XOL on the house? I can't image any of the majors here in NZ would entertain a $100K deductible on a home policy. And if you don't mind me asking, how much are you actually saving that it's worth taking on such a large layer yourself? Surely the cost of a policy from a major NZ insurer with a lower excess (say ~$2500) would end up being mostly EQC & Levies. I'd wager that you're saving yourself a few hundred dollars a year in exchange for taking on a substantially larger risk.

You're not a kiwi by any chance are you...

We took a 5k excess on our house years ago. Premium dropped from 2k to around $1,500. At the time I asked if I could get a higher excess. 5k was the max. It may have changed.

re-read this bit: "Shopping around" when the insurance oligopoly are all selling the same crap products makes no sense.

If you don't know anyone involved in writing this sort of business, I'd suggest finding an insurance broker. They do this stuff all the time for businesses and will be able give more advice and help even more.

Where can you get cover for Home insurance in NZ with a excess that high. I cannot find anywhere

Contents coming up for renewal very soon ...looking at the invoice they are asking near 20% more ... Am pondering having a garage sale....and switching to the minimalist lifestyle.... empty beer crates and reworked pallets for furniture.... lol

Work retail building, liability and work vehicle up 56%. Got more quotes from other brokers and they were all higher. Now paying more in business insurance than our buildings council rates! That is a first.

Ouch. Are your somewhere high risk of flood events or similar?

Not really. Not earthquake area. Not in flood zone.

Hi Ella,

There doesn't seem to be an option for 'Not Insured'. There should be as there is no compulsory 3rd party (the minimum in most countries) in NZ.

Many young people (and growing number of older people) have no insurance as it costs way too much. (And the insurance companies don't provide policies with large excess options so the premiums are less. They should do!) Obviously they run the risk of causing 3rd party damage and then having the insurance companies come after them and they're paying back the balance for years. Alas, far too many in this situation. It was never taught in schools back in my day. Is it now?

Insurance premiums are up - a lot. One of the main reasons is alleged 'global warming' and catastrophic weather events.

I can tell you for sure, the weather where I live is quite normal.......normal temps, normal rainfall, no flooding, no storms. This summer was colder than last, and winter 2023 was colder here than in 2022.

We're all being gouged. Anyone noticed the exaggeration on the internet weather sites? "heavy rain, slips, hazardous driving conditions, electrical storms, severe thunderstorm watch", etc.

Poorly designed survey didn't finish as it seemsed more like a data base collection .

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.