To what extent could, or should, KiwiSaver default funds be used to help bolster New Zealand's struggling capital markets?

This issue is raised in a Ministry of Business, Innovation and Employment (MBIE) and Treasury consultation paper reviewing KiwiSaver default provider arrangements.

"Many countries use retirement savings schemes to develop domestic capital markets. The majority of OECD countries have some restrictions on the amount that retirement savings or pension funds can invest outside the country. For example, Canada allows up to 30% of the fund be invested in foreign investments. One of the stated goals for many of these restrictions is to develop domestic capital markets," the paper says.

"The KiwiSaver default settings could be used to promote liquidity in New Zealand capital markets and encourage increased flows of capital into under‐serviced parts of New Zealand’s capital markets ecosystem. This could support KiwiSaver default members to accumulate long‐term retirement savings, to achieve their financial goals and to allow them to have a similar standard of living in retirement to what they enjoyed pre‐ retirement, consistent with the purpose of the KiwiSaver Act."

The look at KiwiSaver's role in the local capital markets comes with share market operator NZX and the Financial Markets Authority (FMA) overseeing an industry-led review of New Zealand’s capital markets. FMA CEO Rob Everett says the review is a response to concerns about the overall depth and breadth of NZ's capital markets.

"From early-stage capital raising and investment opportunities all the way up to main board listings and institutional investor appetite, we felt the time is right to plan for the future. We are keen to see the industry take this forward and take a good look at how the system is working," Everett says of the project that aims to deliver a 10-year vision and growth agenda.

The MBIE and Treasury paper asks what limitations or problems exist in relation to NZ's capital markets, how could the settings for KiwiSaver default providers be changed to support capital markets development, and how could liquidity and pricing rules affect default provider investment in alternative NZ investments? It also asks how default settings could be used to develop NZ's capital markets, what parts of the capital markets are most in need of development, and whether default funds should take an active role in helping develop NZ capital markets.

'Minimal investment in New Zealand unlisted alternative assets'

MBIE and Treasury note that KiwiSaver currently has $58 billion funds under management with strong year-to-year growth and more than half the value of KiwiSaver default funds invested in NZ, primarily in listed assets.

"Given the level of KiwiSaver investment in New Zealand assets, limitations or weaknesses in New Zealand’s capital markets could have a significant effect on the balances of KiwiSaver default members. The size of KiwiSaver funds under management also means that the KiwiSaver default settings may have a role to play in the health of New Zealand’s capital markets."

"KiwiSaver funds currently have minimal investment in New Zealand unlisted alternative assets (including infrastructure assets, early stage companies and private equity). Exposure to these assets could increase with a more growth oriented investment mandate and as funds under management increase (as fund managers look for more growth assets in which to invest). Globally, two thirds of pension funds invest in domestic early stage companies or in private equity investment strategies. In contrast, only three KiwiSaver funds explicitly invest in these categories," the consultation paper says.

The paper suggests two options to ensure default funds contribute to NZ capital markets development. These are requiring parts of the management be NZ based, and introducing a requirement that a small percentage of default funds be directed to a particular area of investment such as early stage NZ businesses.

Chapman Tripp partners Penny Sheerin, Tim Williams and Mike Woodbury note the review is asking whether credit should be given for investing in local, small investments.

"But we would be surprised if this idea is supported because it would be inconsistent with a customer-centric model and the statutory obligation on and fund managers to act in investors’ best interests, if these investments do not stand on their own merit," the Chapman Tripp lawyers say.

The consultation paper doesn't include an option to require providers to invest a certain percentage of default funds in NZ. MBIE and Treasury argue that wouldn't address a problem in NZ's capital markets because default funds are already heavily invested in NZ. Additionally they argue this option could lead to over-exposure to the NZ economy and/or materially impact on a fund manager's ability to invest in a prudent financial basis.

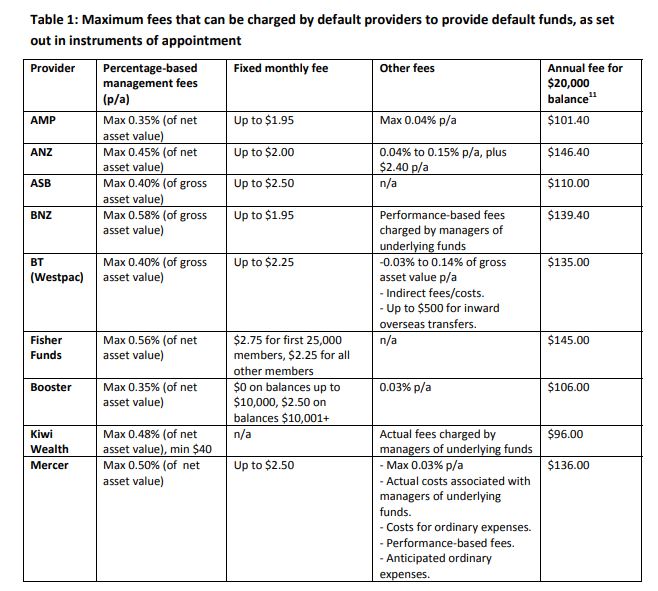

Fee reductions sought

The paper does, of course, feature a section on fees.

"While we accept that fees are only one component of a value‐for‐money service, we want to see reductions in fees for default funds as a result of this review and subsequent procurement process. Default providers get a steady stream of new customers and reputational benefits as a result of being a default provider. Given these benefits, the government expects that providers will offer more competitive fees in order to enhance outcomes for members," it says.

Change the settings?

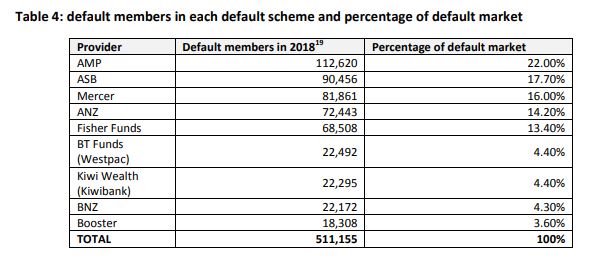

MBIE and Treasury note that many people are automatically enrolled in default KiwiSaver funds when they start a new job, and about 715,000 stay in those funds. One proposal is to change the settings for default funds from conservative risk to higher-growth investments. They say that before they start the process next year of appointing new default KiwiSaver providers, they want to make sure they have the right settings for the default funds.

“The conservative risk setting was intended as an interim arrangement for members while they considered moving to another fund. However, after over 10 years of the KiwiSaver scheme large numbers of people are staying in default funds, despite the potential gains from moving to a higher-growth fund," Sharon Corbett, manager of financial markets at MBIE, says.

The consultation paper also asks for feedback on proposals to ensure KiwiSaver default providers are investing responsibly and ethically.

The terms of the existing nine default providers will expire in 2021. Consultation is open until September 18. The government could appoint more or fewer than nine providers, and some existing providers may not be reappointed and/or new providers may be appointed.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

7 Comments

People, knowingly or unknowingly, are in Conservative Funds, because they are risk averse and don't want their funds to be gambled in the capital markets, right ?

Then how is it fair to use these funds to prop up the share/capital market ?

This proposal is simply hijacking of their funds, without consultation/consent.

Will there be any assured return to the KS a/c holders and assurance of safety of their funds ?

Also changing the default to Growth Funds would be against the principles of Customer Protection.

Will there be a government guarantee, for the principal and return, if the Ministry is backing this idea ?

Your raise a valid point. However the fix that I see is to allocate people to a default fund type by their age, ie. if they are under 45 when joining they should by default go into a growth fund of some sort, then as they get older they should be moved to more conservative funds automatically (say at 45, 55 and 65) if they haven't taken care of changing their plan.

The proposal is effectively political direction of a slice of investments. That's a slippery slope indeed. Best not set foot on it....

I agree totally. If I knew my savings were being manipulated for some political end rather than being invested for my best interests, I'd scarper from KiwiSaver to greener pastures.

"But we would be surprised if this idea is supported because it would be inconsistent with a customer-centric model and the statutory obligation on and fund managers to act in investors’ best interests, if these investments do not stand on their own merit," the Chapman Tripp lawyers say.

Well I guess public manipulation of private funds is done in another form through lowering interest rates, this is almost an extension of that.

Private wealth/savings?? Nonsense, it should be used for the collective good... definately sounds like a slippery slope.

Socialism by stealth . Green slippery slope. What's the success rate for new business again?? Pretty sure it's somewhere near the OCR.

the problem with all of this is that it simply assumes that investors have remained in default funds thru neglect however some investors may have chosen to stay in the default fund they were allocated because they are:

- conservative and risk averse

- approaching 65

- intending to use the kiwisaver proceeds for a first home purchase and therefore have a shorter investment timeframe

I think the question that should be asked of providers is why do they have so many investors remaining in default funds and what have they done to educate investors on the right fund option for them. I am sure it was part of the last default manager review... so I think the MBIE should be asking each manager how many investors have switched and what communication with the default investors has been sent out.

In terms of using default funds as a tool to support capital markets.... it fails as the first hurdle... its the investor's money and has to be invested in their interest.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.