Low interest rates are likely to drive investment strategies for the foreseeable future.

If you are sitting on cash and waiting for a return to interest rates at 7%, 8% or 9% you had better make yourself comfortable – you could be in for a very long wait.

This is important. Interest rates do not just drive our KiwiSaver returns or the way that retired people get their income. They dictate the health and direction of the economy, whether and how we should borrow, if we will have jobs and how our businesses are likely to perform. Just about everything economic hangs on the level and direction of interest rates.

Despite central banks around the world trying to get some inflation into the system, inflation has stayed low. In some countries interest rates have been pushed down so that they are negative but, even so, businesses do not feel that they can push up prices.

One day interest rates will rise again but not for a good while and, even then, probably not very much. Those halcyon days (for savers) of high interest rates may not come back any time soon.

This is based on consideration of the factors that have pushed down rates. It seems to me if we consider what has brought interest rates to these levels, we can then think about whether these factors will persist and continue to hold them there.

However, before we think about those factors, we need to acknowledge that although interest rates are low compared to what we have become accustomed to, they are not super-low by historical standards.

Many older people, those who lived through the high inflation of the 1970s, 1980s and the 1990s, think that the interest rates that they had during this time are normal. They were not. By long-run historical standards, interest rates were exceptionally high during this period and, although people became accustomed to these high levels, interest rates were, in fact, far beyond the historic norm.

Some of the fall in interest rates over the last decade is a reversion to the mean. Certainly, current interest rates are lower than the historical average, but they are much closer to that average than the 26% I paid on my mortgage back in the 1980s.

Interest rates work in cycles and, especially, inflation. Some economies around the world (including New Zealand) have seen good times but, unusually, this has not been accompanied by inflation. Why is that?

There are many explanations for low inflation, but, for me, two of them stand out: technology and demographics. These two prime factors give us a long-term, secular trend where interest rates are much lower.

Technology has held back inflation for a number of reasons: although we do not see much of automation in New Zealand, in other countries (and in some industries) automation is holding down wage costs. For example, many cars are now made in factories which barely see a human. This means the Subaru that I bought in 2004 was about 10% more expensive than I could buy the same model today.

Technology has helped global supply chains keep costs down as manufacturers can buy or make their components from anywhere in the world, wherever is cheapest.

Moreover, consumers are no longer limited to purchasing locally. The world is now a global marketplace and any of us can scour the world to find the item that we want and have it delivered to our doors at the cheapest price.

Demographics have also played a part in keeping down prices. In many places around the world, populations are ageing. Of course, as people age, they spend less, reducing demand for many items and thus lower prices.

These are big, well embedded trends of our age: neither technology nor our demographic makeup are going to go away anytime soon. In spite of healthy economies with full employment, it seems to me that that there will be little inflation and interest rates should stay low for a good while yet.

Those relying on a long-term strategy of rolling over term deposits for their retirement income are especially vulnerable and may need to think again: at current levels there is unlikely to be any real return from such a strategy and those returns may well get worse before they get better.

*Martin Hawes is the Chair of the Summer Investment Committee. The Summer KiwiSaver Scheme is managed by Forsyth Barr Investment Management Ltd and a Product Disclosure statement is available on request. Martin is an Authorised Financial Adviser and a Disclosure Statements is available on request and free of charge at www.martinhawes.com. This article is general in nature and not personalised advice.

42 Comments

Vary narrow minded to think the only means of investments are within the borders of this country.

A large percentage of term deposits are invested, one would think, from the senior sector. Retired, mortgage free, life savings on hand. Those people have little rope to play with, no ability or time left to make up for bad investments. The best return on capital for any investment is the return of that capital. So where else can they go, risk free as best as able, that guarantees that? Managed funds make no guarantees for obvious reasons and levy quite some fees while they are about it. That leaves property possibly, but not many retirees would be looking for the hassle of tenants and maintenance etc.

My post was targeted to central bank governors who implied at the last monetary statement that monetary policy is a " Blunt tool" and those looking for income should seek alternative forms of investments. Was he thinking of retirees when he said that? There is a large population who are/were the back bone of this country. They deserve the most respect and consideration and after sacrificing so much and working so hard, our bankers are keen on letting them down during their retirement years. For those who do have choices, those statements, only validates alternative investments offshore. If only as retaliation for Mom and Dad.

Where is this magical offshore risk-adjusted improved yield you speak of? I'd like some.

Currency risk on short-term returns is too large for the those seeking certainty of income.

A few ideas seem backwards. Automation appears to be the result of high wage costs. Pay has gone up with minimum wage increases at supermarkets and now they use more self-checkouts. Compare this to the US with low minimum wage and they hire a lot of staff and don't seem to have an interest in automation.

The comment that central banks have been trying to create inflation but cannot. They lower interest rates to get more money in the system that is paired with debt. That's not as effective as printing money with no associated debt. They could get inflation if they really wanted it. Shifting to high interest rates would make many zombie companies go bankrupt and a lot of debt would be written off. That would also free money from being pair with debt servicing requirements, but the down side has been deferred with low interest rates.

Perhaps it's time for banks to take a little advice from Zimbabwe and print some $100 trillion dollar notes and then get the government to pay for goods and services with them. Instant inflation.

Automation could also be a result of low worker productivity

It could, yes, but every example I've seen in the manufacturing industry in the UK and here in NZ, automation is always the result of reducing costs as profits shrink due to heightened competition from overseas.

Rather than demographics and technology, the reason for low term deposit rates over the past decade - and the seemingly likely future - is a world awash with cash resulting from QE/money printing and central banks cutting cash rates.

The fall in interest rates - both in term deposits and borrowing - followed actions by central banks in response to the GFC and, despite much of the central banks' gunpowder already being used, it appears that this strategy is again the one they seem to be going to follow in response to the poor outlook for the global economy. The RBNZ recent surprising 0.5% cut is indicative of this and consequently a further fall in term deposit rates in the last month or two.

As a retiree with some cash, I have had to already move from what was previously perceived as reasonable and safe returns from term deposits. Investors need to look to assets - but the quandary is which one(s)?

"real returns from term deposits will likely get worse"

...and Real Return includes the future purchasing power of today's maturing Term Deposit dollar. As I've suggested before, 'investing' at minus 5% gives a positive Real Return if the future dollar buys goods/services that cost 5% less, or lower, than today's prices.

That's what lower interest rates are telling us - that tomorrows World will be Deflationary. The only questions are (1) how much lower,and (2) when?!

Your logic is sound, however it doesn't tell the full story. Price falls are in consumer discretionary (tvs, cars = wants) whereas prices in things we need (land, rates, education, food) are going to keep rising and outpacing inflation. We're just not in that paradox of thrift style cycle and I don't see it eventuating. If you have your needs sorted though, I agree with the point you made.

Could be. But what happens to the Price of those Consumer Necessities you note ( land, education, rates, food etc) if wages fall, and people work for less and less ( wages and hours), just to keep a job? My suggestion is that the prices of those, too, will fall as Costs get translated back into prices. Maybe they'll lag the Discretionaries ( that will bear the brunt of the price falls) but people work, selling Discressionaries. In fact, I'll suggest that in a Services Based economy what we sell is dominated by Discretionaries and so as they lose their jobs/get paid less what they can spend on Necessities, falls.? (eg: people will stop insuring their cars, houses ( if they can) and buy lesser quality/quantity of food etc)

Always a possibility but I personally just don't see it happening. A big part of the Japan deflation story was demographic's and NZ has some of the highest per capita net immigration on the planet. That and a central bank that will go all in to stop it happening. I'm talking buying RMBS and corporate bonds, buying NZGB, cash rate to -0.5, Govt guaranteeing housing and infrastructure loans etc etc

You might not agree with it, but there are plenty of weapons still available. Immigration is one of these being used right now.

I absolutely agree!

Every 'weapon' available and some we haven't 'made up' yet will be hurled at 'what's coming'.

That, in itself, should tell us how desperate the situation is - and 'they' know it.

Immigration, today's' favourite 'saviour', is doomed to failure. That's propably why Japan doesn't embrace it - although culture probably has more to do with it than that. But importing todays' workers in the name of GDP growth when those same workers become a drag on GDP growth tomorrow ( requiring a rinse and repeat of the same failed policy) is a disaster in the making.

That's why 'they' want One World - so that countries don't exist in anything but name, and migration is borderless.

Maybe that's what's coming and New Zealand is just a state of the United World. Who knows. But if what I see on the TV each night tells me something, it's that citizens are against that - across the globe.

Anyway. It's going to be fun to watch what happens! Some of us are going to be big winners, and some wiped out. Which side of the equation I am on remains to be seen! Cheers.

You are referring to what is known as "corporatocracy" I think, where corporates becomes so large and multi-national they become geo-political in their own right. Look at Nike, NBA and China over a tweet about the HK protests. Facebook etc, they are all very left leaning and my theory is they realise future growth is going to come from emerging markets and China.

A big part of the Japan deflation story was demographic's

Rubbish. Deflation in Japan was largely caused by asset prices receding and consumer prices adjuating to match falling incomes as companies malinvestment took hold.

NZ has some of the highest per capita net immigration on the planet

So greater downward pressure on wages and income. This does not necessarily support inflation.

If you don't think high levels of immigration is inflationary, there is nothing left to discuss.

Regarding Japan, of course the asset bubble collapsing was the principle source of deflation. In the context of this discussion however, Japan's demographics played a significant role and contrast starkly to NZ.

What you're trying to say is that immigration has impacted housing costs. You're trying to contrast that with Japan where you're suggesting that the imapct of house price deflation would have been more benign with immigration. The idea that an ageing population is synonymous with deflation has been debunked by the Japanese themselves. The main drivers of deflation have been falling income levels and debt consolidation. Nothing to do with demographics.

No, that's your intepretation of what I said. Here is a 2014 IMF study linking an ageing population in Japan to strong deflationary pressures. Feel free to post yours.

https://www.imf.org/en/Publications/WP/Issues/2016/12/31/Is-Japans-Popu…

A link to a paper you haven't read. Furthermore, if demographics is a primary driver of property price inflation, it is a logical fallacy that the Japanese bubble could have existed in the first place (population dynamics are frequently modelled in timeframes of 50 years or more [only approx 30 years separate us from the end of the Japan bubble]). Japanese deflation has existed primarily because of what I identified: falling incomes (even with some of the lowest unemployment in the developed world) and corporate debt consolidation (Japanese h'hold debt to GDP never got the scale as it has in NZ and Australia). It also has to do with behavior. If young Japanese were being thrown mountains of cash to speculate on house and land prices and were inclined to do so, there is no doubt bubbles would exisit.

Now you're just being a twa+

We're watching the downfall of fiat currency as interest rates fall through the floor backed by the collective mis-managemnet of the global economy by not allowing capitalism to run it's course. We've bailed out companies that should have failed, and tried to print our way out of a corner.

The big question is what comes next? Looking at technology life cycles in light of blockchain it's not usually the first cab off the rank that wins the race. So unlikely bitcoin will be the system to replace fiat. But blockchain as a theory is sound, and with the likes of facebook getting into crypto it's only a matter of time. Fortunes to be made and lost in between.

So unlikely bitcoin will be the system to replace fiat.

Not sure it was ever intended to replace fiat currencies. However, as a store of value, it's proving to be quite robust.

For now. Proof of work block chain solutions are horrendously expensive to maintain. It could happen that Bitcoin gets prohibitively expensive to mine. And there's some speculation that a small group own a large chunk and manipulate the price. https://www.theverge.com/platform/amp/2019/7/4/20682109/bitcoin-energy-…

Lending out stablecoins now paying anywhere up to 10% p.a.

https://cryptobriefing.com/stablecoin-lending-may-interest-recession-wa…

Those relying on a long-term strategy of rolling over term deposits for their retirement income are especially vulnerable and may need to think again: at current levels there is unlikely to be any real return from such a strategy and those returns may well get worse before they get better.

All too true. Term sovereign interest rates are indicating low returns as far as one would want to forecast. Hence:

Yet the iron law of investing is that a security is nothing but a claim on a future stream of cash flows. Valuation is a crucial determinant of long-term returns. The higher the price an investor pays for those cash flows today, the lower the long-term rate of return earned on the investment..

The corollary is also true. The lower the long-term rate of return demanded by investors, the higher the price moves today. So clearly, changes in investors' attitudes toward risk will strongly affect short-term returns. If investors become more willing to take market risk, it is equivalent to saying that they are demanding a smaller risk premium on stocks (that is, a lower long-term rate of return). Prices rise as a result. Now, the fact that current stock prices are higher also implies that future long-term returns will be lower, but that's part of the deal.Link

Pension investors may not only have to vacate their deposits, they will have to increase the capital commitment to their pensions to generate the returns consistent with the desired retirement income, since the present value of the liability increases with each official interest rate cut.

ACC has such a dilemma given it's recent declaration:

ACC has posted an $8.7 billion deficit for the year, with record-low interest rates taking a major chunk of out its long-term forecasts.

But the public accident insurer says that loss is just on paper and there's no need for entitlements to change after also running a $570 million cash operating surplus.

The corporation presented its 2018-19 financial results to Parliament on Wednesday, with a huge increase in its "outstanding claims liability" (OCL) producing its highest-ever deficit and overshadowing other results.

The OCL is the amount of ACC estimates all its current claims will cost over the next 100 years. Lower interest rates mean the fund has to invest more now to cover costs down the track. [my bold] Link

Indeed. To generate $40,000 income at 4% takes $1m invested. At 2% return, you need $2m invested. This is made wore by the fact that accumulating the capital is also slowed by the lower return in the accumulation years.

Below a certain % return, just eating your capital is the only option - taking out $40,000 per year from your initial $1m will last you for 25 years if you can keep up with inflation.

It's a dangerous world

https://wolfstreet.com/2019/10/28/redemptions-rip-through-uk-equity-fun…

Do you get tax back when you go in to negative interest rates?

A fund manager recommending avoiding term deposits; how unusual...

It is a right royal mess, created by the greed and corruption of capitalism. There is not going to be an easy or painless way out for the next decade or so.

May be the Governments will come up with an idea to gather all private wealth of retired people and dish out all the necessities to them, till they pass away.

A new state managed retirement care.

Even if this sounds a bit socialistic, may be that is part of the solution ?

Ok, let's start with your parents.

theyll just take their wealth offshore to a country that won't seize it

Risk free investments don't deserve a high real return. That's the point. High real interest rates were an aberration.

Term deposits are now a nominal wealth preservation tool, not a way to grow your personal capital. Probably the way it should be.

You can now get the same or better interest rates in the US which means less investment into NZ from US and other sources, which means the exchange rate will make NZ $ worth less as it will be in less demand. Maybe when it gets down below NZ50c on the US $ Ill think about buying real estate in NZ again, although it is still way overpriced as an investment. Ill bide my time and see how that plays out.....

The cost of imported goods into NZ continue to increase as the value of the NZ $ falls and that might create inflation?

Of course the fly in the ointment are the inconsistent and erratic administration policies in the US right now from which will be thrown into turmoil as next year the US goes into one of the most divisive election campaigns in its history. The country under trump is in so much increased debt that something may happen where the US$ falls more than the NZ$??

The problem is that those without enough money in TDs when they retire will have to take more risk. This is the same group who cannot afford to take more risk. Those with a million in the bank are still doing fine.

... yes .. exactly where finance companys came into play 20 years ago ... offering high interest rates through mezzanine finance ... expect history to repeat to some degree , as a significant amount of grey money is looking for better than bank TD rates ..

The new saying..A saver and his money are soon parted.

"Those relying on a long-term strategy of rolling over term deposits for their retirement income are especially vulnerable and may need to think again: at current levels there is unlikely to be any real return from such a strategy and those returns may well get worse before they get better."

All very well to keep saying that, something elderly people already know, but what else are we supposed to do with our lifetime savings? We have enough shares, Kiwisaver and TDs. Any suggestions as to what to do next would be helpful - we could have another 15-20 years, if we're lucky.

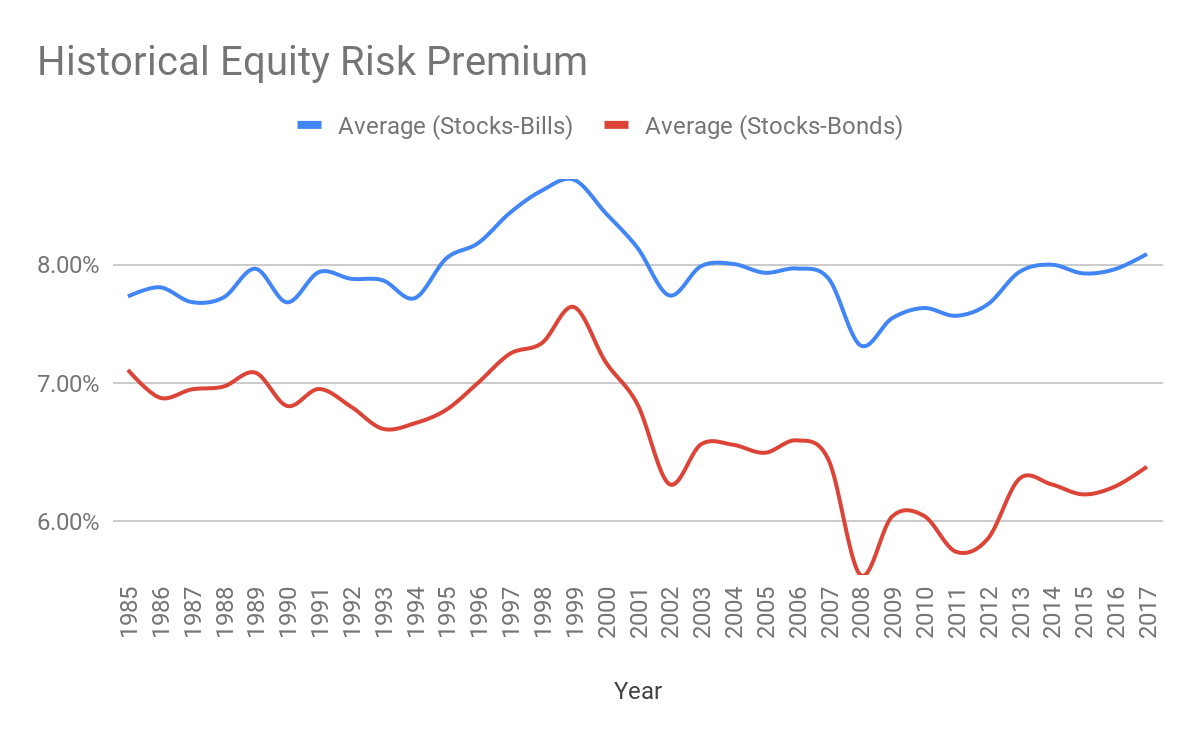

The real risk premium for equities remains consistent even in low interest rate environments. So that's where my money will go. Even at 65, you are investing for potentially 30 years so the extra return will win out over the variability.

https://static.seekingalpha.com/uploads/2019/2/2/saupload_JPkZS0GfyOJks…

{kind=link}

Much of this is a statement of the obvious,but pointing out that the high interest rates many of us remember all too well were an historical anomaly is useful.

I wrote a piece in late 2014 stating that low inflation was structural rather than cyclical and referenced not only technology,but globalisation and the reduction in unionisation as factors . The fall in inflation is not recent. It started several decades ago in the US and the UK,while here it dates to the very early 90s.

Stealing takes many forms.

Bankers and poll-lies have it down to a fine art.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.