By Craig Simpson

The Brexit vote came and went, and while the initial volatility had investors in a bit of a flap, markets have since settled.

Even through the aftermath of the Brexit vote, the NZ share market showed incredible resilience. The NZX50 Gross index was down 2% for the month, but was up 2.1% for the quarter.

Many of the KiwiSaver funds we examined immediately after the Brexit vote showed there was little exposure to the UK. In fact, most of the allocation to equities was to the US.

The US market represented by the S&P 500 index eeked out a positive 0.1% return for the month.

While some of the equity components within the various Default Funds may be showing a loss last month, most of this will have been absorbed by stronger global and local bond returns.

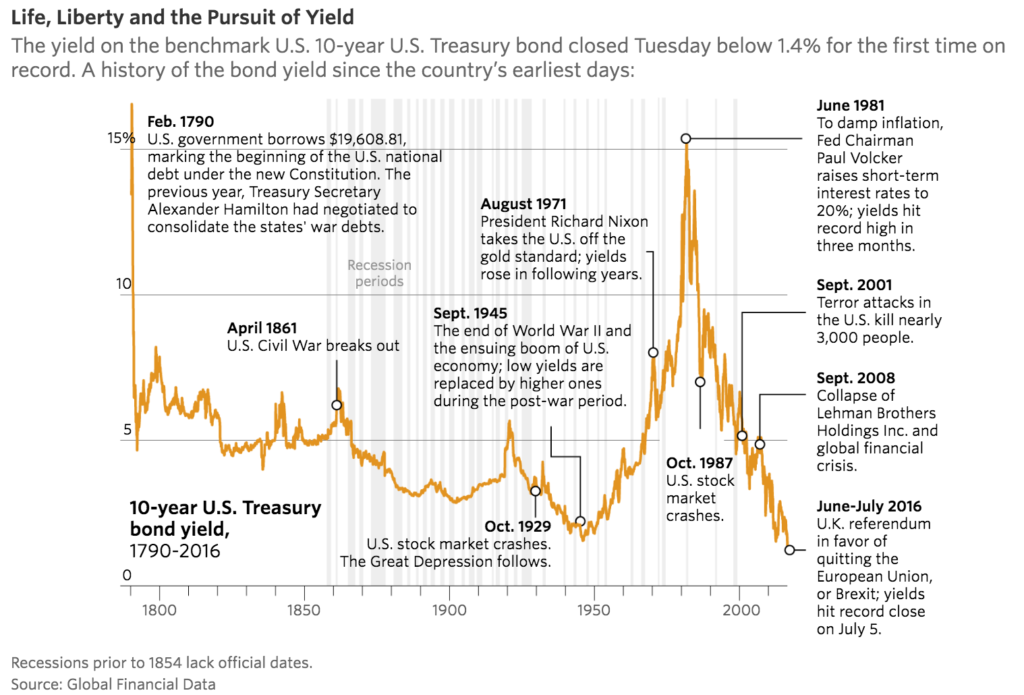

US 10-year bonds are trading at yields last seen during the World War II era. New Zealand Government Bonds with short-term maturities have been trading below 2%.

source: Next Gen Personal Finance

Long term KiwiSaver returns have continued to hold at previous levels and providing stable and somewhat predictable returns quarter on quarter.

ANZ's dethroning of Mercer short lived

The difference in accumulated wealth between the Mercer Conservative Fund and the average of the top 5 Cash funds was previously $5,013 - it is now $4,711. The margin over the cash funds has stopped expanding for now but any large upswing in markets will see this situation change.

Our performance table below looks specifically at the performance of the current nine Default options available. The bottom four funds in the table were either added recently or do not have a long enough track record to allow for meaningful comparisons against those funds which have been in KiwiSaver since April 2008 when our analysis commences.

Since inception, on a regular savings basis, the average compound average annual return of the five Default funds that have been in operation since April 2008 is 5.7% p.a. (a small decline from the previous quarter's 6.0% p.a.). This rate of return on an after tax and fees basis is still well ahead of what investors are getting on longer dated term deposits at present.

We have noted a high degree of return stability across the main Default funds and they continue to hover around the 6% range since inception. The last three year returns have come down and are sitting below the longer term returns.

Assuming you had been invested for the period April 2008 to June 2016, the difference between the average return of the top and bottom Default fund since our analysis began is approximately $2,703 (previously $1,633). We have see a sharp reversal in the previous contraction in margin between the top ranked and fifth ranked Default fund.

After not awarding the best in class title last quarter due to sagging short term, we are able to reinstate this award this quarter.

The Mercer Conservative is awarded our best in class title this quarter with the fund has the highest return over the full period of the review and has the three-year return.

We note that ASB's Default fund has the best three-year return across those funds that have sufficient data. Of the best performing funds ASB has the least variance between long run and shorter term returns.

Here are the full comparison to June 20, 2016 for Default Funds.

| Default Funds |

Cumulative $

contributions

(EE, ER, Govt)

|

+ Cum net gains

after all tax, fees

|

Effective

cum return

|

= Ending value

in your account

|

Effective

last 3 yr

return % p.a.

|

|||

| since April 2008 | X | Y | Z | |||||

| to June 2016 |

$

|

% p.a.

|

$

|

|||||

|

|

|

|

|

|

||||

|

C | C | C | 27,378 | 10,918 | 6.7% | 38,296 | 7.0% |

| ANZ Default Conservative | C | C | C |

27,378

|

10,492 | 6.4% | 37,870 | 6.9% |

| ASB Conservative | C | C | C | 27,378 | 9,986 | 6.1% | 37,364 | 6.6% |

| Fisher Funds Two Cash Enhanced | C | D | C | 27,378 | 9,566 | 5.9% | 36,944 | 6.5% |

| AMP Default | C | C | C | 27,378 | 8,216 | 5.1% | 35,594 | 5.3% |

| BNZ Conservative | C | C | C | 10,720 | 2,357 | 5.7% | 13,076 | 5.1% |

| Westpac Defensive | C | C | C | 6,405 | 1,438 | 4.7% | 7,842 | n/a |

| Kiwi Wealth Default | C | C | C | 6,405 | 1,410 | 4.4% | 7,814 | n/a |

| Grosvenor Default Saver | C | C | C | 6,128 | 1,503 | 5.8% | 7,631 | n/a |

| --------------- | ||||||||

| Column X is interest.co.nz definition, column Y is Sorted's definition, column Z is Morningstar's definition | ||||||||

| C = Conservative, D = Defensive | ||||||||

Default Fund observations

Our recent story examining the top 10 investments in Default Funds and some of the insights and conclusions we drew from the data can be found here. The data to 30 June is not available however we don't expect too many changes to the overall position of the funds compared to the data used in our article.

A couple of conclusions from the article we wrote were that property and alternative exposures were adding value. Also, Mercer is the only manager that stated a specific exposure to alternatives which will include commodities and infrastructure. Commodities such as oil and gold have both outperformed other assets in USD over the quarter. Adding a further boost for Mercer's returns this quarter will be their hedging position. For global bonds and real assets (property and infrastructure for example) they are 100% hedged.

We noted in our article Fisher Funds Two's Default Fund has a substantial exposure to bond markets and will have benefited from the fall in global bond yields. Their exposure to cash and equities is considerably smaller than their peers. The fund also has a property exposure which is outsized compared to the other funds in the category. There has been a substantial increase in the three year return for this fund compared to the same return in the previous quarter. An increase in the unit price is evident with a rise of 1.75% for the last three months and this was one of the best returns for a conservatively managed fund across similar funds.

Factors impacting on KiwiSaver portfolios

The Brexit vote has some negative impacts on portfolios immediately after the result became clear but most of this volatility and sell-off has now dissipated. Most equity markets are pushing higher and the S&P 500 index is trading around record levels.

Falling global bond yields will be providing a pick up to portfolios with substantial fixed income holdings. The returns from bonds have had a calming influence on portfolios and reduced some of the volatility although bond yields have been flicking up and down frequently but certainly not in the same way equities were.

Currency hedging will be playing a part in the returns with the NZ dollar soaring to just on 73 US cents. Aussie/Kiwi dollar parity party talks are doing the rounds again in the media but there is a fair way to go between the current level of mid 95c to parity. Two major bank economists are tipping parity will occur, its just a matter of time. Strength against the British Pound and Euro will be hitting some portfolios with unhedged European exposures. We have seen marked improvement in the Yen as investors sought out safe havens assets to park their cash.

Equity portfolios with a bias towards the US should be doing better on the whole. The US market has not really been impacted by the Brexit vote, apart from the initial shock. The UK share market rose following the Brexit vote and posted the best gains for the month across the main global indices. Japanese shares in contrast have been hit the hardest with a 9.6% drop in (JPY terms). For the first time in a while the NZX50 gross index recorded a 2% loss, but was still up by 2% for the quarter. Australian shares were on a par with NZ equivalents for the month and quarter ending June 30 (in Australian dollar terms).

Property, infrastructure and commodity holdings have provided some portfolios with a leg up this month.

----------

KiwiSaver default funds are only part of a broader range of conservative funds available. Many of the 'traditional' Conservative and Cash funds are underperforming the Default funds. We will look at the rest of the Conservative funds in another article.

For explanations about how we calculate our 'regular savings returns' and how we classify funds, see here and here.

There are wide variances in returns since April 2008, and even in the past three years, and these should cause investors to review their KiwiSaver accounts especially if their funds are in the bottom third of the table.

The right fund type for you will depend on your tolerance for risk and importantly on your life stage.

You should move only with appropriate advice and for a substantial reason.

2 Comments

Conservative may not be that safe when we finally get and increase in rates. It won't happen overnight, but it will happen. Portfolio structuring thinking predates QE and today's freakonomics.

I think portfolio construction techniques have moved on a little since Markowitz's 1950's paper. The managers have the ability to move assests around within the various allocations to minimise the downside or any interest rate increase. They have shown in the past that they do know what they are doing when it comes to generating consistent returns so there is no reason to doubt this ability going forward.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.