Here's our summary of key events over the weekend that affect New Zealand, with news of more strong gains in the relative value of the New Zealand currency as our trade gains with China multiply.

China's exports in November shrank for the fourth consecutive month when valued in US dollars but actually rose when valued in yuan, a turnaround they will be satisfied with. But growth in imports was more stronger - in both USD and yuan terms - and may be a sign that Beijing's stimulus steps are starting to work.

And China foreign currency reserves were essentially unchanged in November, holding at about US$3.1 tln and a level they have been at for all of 2019. The trade war is showing no signs of eating into these reserves.

And iron ore prices are starting to rise again, even if imports are down sharply. Prices are up more than +12% in the past month. Meanwhile China's imports of copper and oil are at or approaching record levels.

The same Chinese data showed that New Zealand exported about twice as much to China in November than we imported from them. The politically sensitive trade with the US shows their exports to the US fell -8.4% while their imports from the US fell almost -20% leaving their large surplus with the US little-changed.

In Hong Kong, there was a massive street rally in support of democracy. It is clear the Beijing-imposed administration does not have the support of the people of Hong Kong. This protest was peaceful.

In the US, consumer credit rose +4.8% in October, and more than expected, to a record US$4.165 tln or 19.3% of GDP. That is up from 19.2% a year ago. The October rise was the biggest increase in three months and was driven by a jump in use of credit cards. The rises for car loans and student loans were more modest.

American consumer sentiment also rose, underpinned by good employment numbers.

The US non-farm payrolls survey data for November came firmer than expected. +266,000 new jobs were added and there were minor positive adjustments to both prior month's data. The end of the GM strike seems to have had a cascading impact. However their low participation rate was unchanged at 63.2%, so while the rise will be welcomed, it isn't a sign more people are being drawn back into their labour market. After adjusting for the GM strike, manufacturing employment was flat, it was down for 'mining' (read: the oil patch), unchanged in retail, and up strongly in healthcare. Professional job numbers also rose.

US hourly earnings are up +3.1% over the past twelve months.

All this data supports the US Fed in its stance that their monetary policy settings are about right and markets now don't expect any change when they next meet to review those settings on Thursday, NZT.

Meanwhile, trucking companies ordered -39% fewer big-rig trucks in November compared with the same month a year ago, and that was also -21% lower than for October, a weak start for what is typically the busiest season for new-equipment orders. This comes as US freight volumes fell -5.9% in October compared with the same month a year ago, while freight rates were down -2.5% on the same basis.

You can see what is driving these declines in the latest wholesale trade data, which is -1.4% lower in October than a year ago.

And the Bank of International Settlements has said (page 12) that a combination of a reluctance of four big American banks to lend their cash reserves when some large hedge funds needed secured funding explains the gyrations in the New York repo market that caused the Federal Reserve to have to step up with emergency liquidity.

In Canada, the situation is definitely not as positive for payrolls. They recorded a drop in payrolls of -79,000 jobs in November and a rise in their jobless rate to 5.9%. But over the past year, jobs in Canada have grown by an impressive +293,000 and most of that is for full-time employment. Their participation rate is much better that their neighbours however at 65.6% and that clouds comparisons, especially of the jobless rate.

In Australia, there is more evidence of a steep contraction in their construction industry and it is now at its lowest level since 2013. The contraction dived a worrying -3.9 points in November from October alone - that is a big move.

The UST 10yr yield is at 1.84% and a similar level to this time last week. Their 2-10 curve is much more positive at +22 bps. Their 1-5 curve is more positive for the week at +11 bps. Their 3m-10yr curve is also more positive +32 bps. The Aussie Govt 10yr is at 1.15% and an +11 bps gain for the week. The China Govt 10yr is now at 3.23%, and up +3 bps for the week. The NZ Govt 10 yr is now at 1.49%, up a remarkable +19 bps for the week.

Gold is now at US$1,460/oz and down -US$4 for the week.

US oil prices are up further to just under US$59.50/bbl and that is a rise in a week of +US$4. The Brent benchmark is now just under US$64.50/bbl. Pushing them to this 3 month high has been an OPEC move to curtail supplies further.

The Kiwi dollar is on a tear, now up at 65.7 USC and +1½c higher than this time last week and at its highest since the end of July four months ago. In the past month it is up a remarkable +3.7%. On the cross rates we are firmer too, up at 96 AUc and another +1c gain in a week. In fact since the start of November we have gained more than +3c against the Aussie dollar. Against the euro we are up at 59.4 euro cents and that is also more than a +1c gain in a week. That puts the TWI-5 at just on 70.8.

Bitcoin is little-changed from where we left it on Saturday, now at US$7,527. The bitcoin rate is charted in the exchange rate set below.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

40 Comments

All this data supports the US Fed in its stance that their monetary policy settings are about right and markets now don't expect any change when they next meet to review those settings on Thursday, NZT.

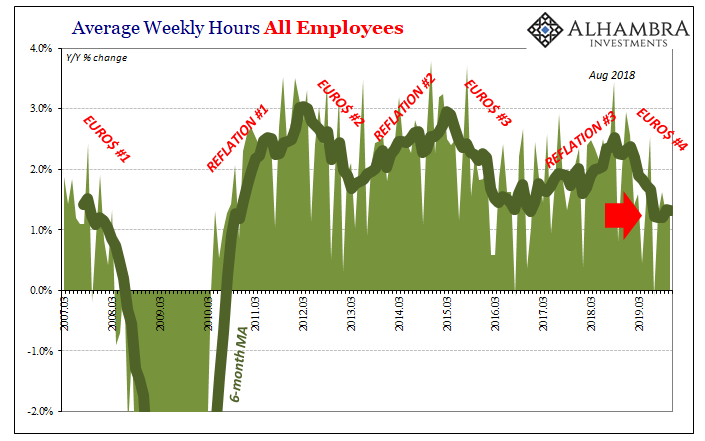

If anything in the details is to spoil the November payroll party it has to be hours. While the highly-smoothed Establishment Survey shows us that potential “V”, the more granular index of total hours worked displays instead the stubborn downshift.

Not just a possible lower level of labor utilization, one that remains at the lowest rate of the last decade. Persistent, stubborn weakness here is a major concern.

That is why average weekly earnings growth has decelerated, as average hourly earnings rates topped out. Companies no longer in much rush for new work (as they were never in one even during the climax of 2017’s labor story inflation hysteria) aren’t assertively bidding up the price of their workforce. Combined with lower growth in hours, that’s less expansion in average weekly earnings. Link

{kind=link}

I'm a little confused by this comment; "Companies no longer in much rush for new work". Potentially it has several meanings; companies don't see a market for more production, but then are they not looking for new contracts(?), they are planning to wind down/lay off, or they have suddenly realised we are in a finite world and need to stop making new stuff (Tui ad).??

I'd like some educate analysis please?

In one word: slack. More of it. As noted yesterday, it’s the same across business prices, things like the Producer Price Index which has picked up a growing disdain for any charged increases.

It gives us a reason for why other indications like the ISM’s various PMI’s refuse to play ball with the recession-is-behind-us narrative. Weakness remains stubborn while, again, whether it leads to recession or not is the wrong focus. The ISM, the inflation data, corporate numbers, etc., they all suggest downturn and that’s what’s really important. Link

Maybe wording is poor? odd and intentionally so? It is implying companies dont want the new work, which seems nuts. I see it as there is still no increase in demand which isnt surprising where most workers have seen no or little increases in pay while costs like rates etc continue to eat their wallets contents. Just looking at my meager pay increase and the 5%+ rates is going to eat 1/2 or 2/3rds of that without any other costs increases to meet. "They have suddenly realised we are in a finite world and need to stop making new stuff" dont be silly only probably 5~15% of the population think maths is real.

This isn’t just a problem for Germany and Europe. Despite today’s awesome payroll numbers in the US, these results from across the Atlantic are more applicable to our own upcoming circumstances than those. Globally synchronized downturn two years in the making and only now just getting more in sync.

Climate Change Emergency over ! ... yes folks... you read it here first ....

.. the polar bears are saved ... the oceans will stop rising ... CO2 levels will collapse ....

Taxcinda has declared that NZ is leading the world ... a ban on those annoying little plastic stickers they put on fruit .... yes Greta , we were listening .... the planet is saved ... here , have your childhood back !

Let us record this as the first instance in history where we have solved an emergency by strategic use of virtue signalling.

Masterful.

.... luckily , Kiwis get most of their food from KFC or Maccas . .. so it won't matter too much if they're in the supermarket and stumble upon an apple or a banana and don't know what the heck it is ...

Our PM is an easy target but this is unfair. On the radio I heard her say we are just following what some other countries are doing. From the Stuff article: ""An August 1 News/Colmar Brunton poll found that 82 per cent of New Zealanders wanted the plastic bag ban extended to other single-use plastics. Green Party supporters were the most behind the move while National supporters were the most opposed. Many have conflated the issue of climate change and waste but the two are quite different. ""

I do criticise her for taking so long to respond to public demand - it is a simple desire to see NZ return to its clean green origins.

No they want to get the headlines for publicity, I agree NZ should not be leading this.

To put NZ plastic bag effort into perspective Japan in ONE DAY uses more plastic bags than NZ did in ONE YEAR !

Whilst I don't agree with some of the greenwashing out there - I think we definitely should be trying to lead the way... Unregulated, our plastic bag consumption was only going to increase.. Now we are seeing some innovation prompted by these laws. Why not continue this into other areas? And why not lead this?

You've mentioned for perspective however left out Japan has ~30x our population...?

No perspective should be necessary to realise NZ is a small player and to know the population of Japan.

30x the population and they use 365x the amount of bags ?

We already had green plastic bags which decomposed, new world had those made from Corn starch.

That example is just Japan, China / Asia is way worse but that is not addressed by anyone. Paris accord allows them to double there C02 in the same time frame.

There's no point in saying 'those guys are worse than us' - we just keep on doing the best we can. Plastic bags with a useful life measured in minutes are a disgraceful waste of a precious resource.

Correct...

The dumbest virtue signalling idiocy of this Govt - adored by un-informed zealots who as usual don't understand the consequences of their emotive choices. The net effect of the ban has been to increase the amount of fossil fuels consumed for packaging - with more heavier multi use bags that take far longer to decompose, but don't last long enough to offset the extra resources used in their manufacture + need for additional bag production (rather than secondary use) for large amounts of kitchen waste, dog crap, lunch wrapping and other household needs. The banned bags used about 5g of hdpe (which could be synthesized from CO2+Water for less than $0.02 electricity if we wanted to). That is about 0.1% of the NZ population's 5kg/day average fossil fuel consumption. A big fat nothing in it's actual impact, and a total irrelevancy in landfill compared to all the other plastic detritus that ends up there.

About bloody time. Should be seriously huge tax on non-biodgradable, non-recycled packaging. So much waste due purely to selfish and lazy generations.

What do you mean, in the past we had paper bags and things were wrapped in newspaper.

Why would you blame older generation for what has been done in your life span most likely.

Why did companies go to plastic bags, well it was cheap, you cant blame older people for what companies chose to do ?

... plastic is an amazing material ... cheap ... plentiful... incredibly useful ...

So , what're Taxcinda & the Greens planning to replace it with !

Plentiful at the moment, but I wouldn't want to be the one explaining to future generations that there's no oil left because we couldn't be bothered to carry our own bags with us when we drove a tonne of metal 1km down the road to pick up a litre of milk.

Don't you realize that banning the lightweight supermarket bags has actually increased fossil fuel consumption needed for making bags significantly?

Own-goal for low information Greens.

Ummm. I don't think I mentioned older generation at all, I actually used the word generations to include all of us currently living and engaging in these wastefull practices. Also I'm blaming companies for what companies choose to do and collectively all.of us for just accepting it.

Apologise then, I had read the "lazy generations" as inferring the past older generations.

Great, just what we needed....absolute Labour genius !

Under the Paris accord we must halve our CO2 while China is aloud to double there output. That's how good our Political class are.

Although I concur that other countries are a significant worry - this double and half comparisons are deeply misleading. What is the per capita emissions is what matters. And no cheating by leaving out international travel, agriculture, imported consumption (buying goods manufactured overseas with significant related emissions). Even that makes for unfair comparisons since my country of origin Britain has been emitting industrial CO2 for about 200 years whereas most of the world is only getting started.

PS I don't see any chance of our meeting the Paris accord while we race to increase our population.

She did say it would be the 'year of delivery'.

What will 2020 be, the 'year of the bribe'?

It’s fun to focus on the absurd to have a Monday morning giggle but in fairness we should note Govt intends banning PVC and Polystyrene packaging as they are hard to recycle. That sounds like a worthwhile effort.

... of course . .. we do enjoy a giggle here at interest.co nz ... but , instead of just virtue signaling , this government needs to come up with some practical solutions ...

.. if we ban PVC and polystyrene ... what replaces them?

More expensive plastics that are recycleable..surprise surprise...

We bought muesli in compostable plastic recently, buried it in the garden but it hasn’t vanished yet.

Is only a week though..

We ate the muesli , you understand.

I suggest doing some research on the compostable plastic. From memory, you can't just put them in your garden compost; they require a commercial high-temperature composting system.

Nope,

The package invited me to bury it in a domestic compost and I have complied with its wishes.

I

It only composts if you bury it with the Muesli inside it.

and it takes 1500 years.

Haha, my argument is that everything is recyclable. It's just the timescale that is the question.

Cardboard!

Agree, halogenated plastics should be reserved for applications requiring durability. Polyethylene is better for disposable packaging - lighter, stronger and degrades to straight water and CO2 - can be cleanly burnt in a waste-to-energy plant. Polystyrene is much less of a problem if you put the waste through a heat cycle to melt it - or burn it, and Styrene is a pure hydrocarbon ideal for waste-to-energy.

"The board and I agreed that this next phase is going to be too difficult to manage alongside my other commitments whilst also managing the health and wellness priorities of my family and me."

Where have I heard something like this recently? From Hiscoe? Perhaps not....

https://www.stuff.co.nz/business/farming/118044514/a2-milk-appoints-int…

I just watched ' American Factory' on Netflix. It's about a Chinese car windshield company starting up in an old GM plant in Ohio. Wow the difference in worker attitudes etc, different planets.

It didn't give me much hope but interesting.

Hey Andrew - watched that as well. If that sums up the typical difference between Chinese and American workers, the US has some serious challenges ahead if it thinks its going to remain the dominant world power. Sums up my experience working in the US though about 10 years ago.

As a result I sold some IVV ETF and purchased some AIA ETF......

Umm.. I would have thought that Mr Trump would have put the breaks on this: BBC Tesla gets the go-ahead to build cars in China. "The electric carmaker, which is run by billionaire Elon Musk, is building a $2bn (£1.5bn) factory in the eastern city of Shanghai. Tesla plans to build at least 1,000 of its Model 3s each week in the Chinese factory, which could be up and running within weeks. The new factory will give Tesla access to China, which is the world's biggest car market. It would also help the company avoid higher import tariffs that are imposed on cars made in the US".

https://www.bbc.com/news/business-50080806

And further rises in long term yields today (9/12). Govt 10 yr up to 1.52%. Getting slaughtered in bonds ... what is this? It cannot be painting a few schools.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.