The NZ Super Fund has managed to sail its way through the extremely turbulent seas of a Covid-wracked financial year and ended up posting a modest gain in value.

The fund, designed to partially pay for the country's superannuation needs in future years, posted a return of 1.73% for the year to June 2020 and stood at $44.8 billion at year-end (after costs and before NZ tax).

The year-end result demonstrates a marked recovery in fortunes for the fund after global markets were hammered earlier in the year.

In March the fund said it had lost about $8.9 billion in the year to date, or nearly 20% of the value of the fund due to the massive falls in markets.

However, markets recovered sharply after the turbulence in February and March - and so did the value of the fund.

"Over the past financial year we have endured a profound and globally far-reaching crisis," NZ Super Fund chair Catherine Savage said.

This had presented a hugely challenging environment that put the fund's resilience to the test, she said.

"Given the NZ Super Fund has a long-term horizon with no substantial withdrawals until the 2050s, the fund’s portfolio is heavily weighted towards equities and with a market shock like Covid-19, we expect the value of the fund to fall sharply. Yet we also expect the fund to earn back these losses – and then some – in subsequent years as markets recover.”

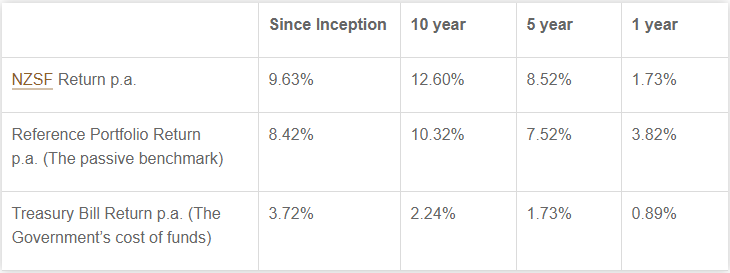

In the financial year to June 2020 the fund underperformed its 'benchmark reference portfolio', which returned 3.82% for the year, by 2.08%. Since inception in 2003 the fund has returned 9.63% per annum, adding value of $7.75 billion over the benchmark reference portfolio.

Since the start of the fund, Treasury Bills have returned 3.72% per annum.

What that means is that the Crown is $26.12 billion better off than what could have achieved by paying down debt.

Fund chief executive Matt Whineray said in recent years the fund had been upfront about the potential for it to suffer reductions in value when markets drop.

"That was clearly apparent in March when the Fund saw the second biggest monthly reduction in its history, of 12.27%," he said.

The fund had, however, gone into that period in a strong position.

"Our long-term horizon meant when risk sentiment was at its lowest we could lean into market opportunities via counter-cyclical strategies such as dynamic asset allocation and accessing stressed credit and funding markets, to take advantage of the corresponding recovery. The fund added significantly to its equity and credit positions as markets fell, and has progressively reduced those positions as markets have recovered.

“Through challenging investment and operational conditions, the team was able to deliver a strong result for the year. It highlighted the importance of sticking to our investment strategies, good governance and carefully managing our levels of liquidity."

Whineray said the low interest rate environment and constrained economic conditions point to a difficult period ahead, and the uncertainty in the economic outlook is reflected in continuing volatility in global markets.

"As always, we’re constantly reassessing what constitutes fair value for the various markets we operate in, so as to most effectively invest the Fund for the good of New Zealand.

"Market pricing indicates interest rates will remain very low for an extended period, meaning that expected returns on all assets are below our long run expectations."

4 Comments

Why do they tax the super fund? and for that matter benefit payments?? its just a giant circle jerk that increases inefficiencies the more times you handle the same money.

It would be good to see the comparison to the reference portfolio on a risk-adjusted basis (e.g. Sharpe Ratio).

Returns on a passive investment over 2003-2020 could have been increased through simple leverage... ex ante of course the problem is you increase the risk as well when you leverage-up. Hence a comparison on a risk-adjusted basis is called for.

Hi Lesnakey, I work in the Super Fund's comms team. We report on our Sharpe Ratio in our full annual report. The 19/20 report should be out in October and you can find previous reports here: https://www.nzsuperfund.nz/publications/annual-reports/

Thanks

Matt Whineray is a good CE. Gareth Vaughan interviewed him a while back, well before covid was around. They discussed the next recession. Things have played out exactly as he anticipated.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.