With the Reserve Bank clamping down on banks' high loan-to-value ratio (LVR) lending to residential property investors, non-bank lender Resimac Home Loans has been inundated with loan applications from property investors.

Adrienne Church, Resimac's general manager of mortgages, told interest.co.nz the firm had been receiving about $40 million of new loan applications per month, but over the past couple of months this has at least trebled. And of the applications, about 70% are from investors and just 30% from owner-occupiers.

In mid-July the Reserve Bank announced plans to ramp up its existing LVR restrictions, which major banks adopted immediately. From October 1, no more than 5% of bank lending to residential property investors across New Zealand will be permitted with an LVR of greater than 60%, i.e. a deposit of less than 40%.

Church says Resimac, which uses residential mortgage backed securities and wholesale money for its funding, targets a balance of about 50% owner-occupier lending and 50% investor lending.

"We're not restricted but we do have expectations that we have a balanced portfolio," she says.

Thus from Monday September 26, Resimac says although it will continue doing investment loans with LVRs of up to 80%, it will also require borrowers with loans on owner-occupied properties to bring that business to Resimac too.

"The people that we can help are mums and dads who are trying to get ahead or they've got an investment [property], or they want two. It's not the [people with] 10s and 20 investment properties," Church says.

"We [non-bank lenders] are not the silver bullet, we're never going to pick up everything that the Reserve Bank has carved out."

She says Resimac's New Zealand mortgage book is now worth a "couple of hundred million" dollars. When the Reserve Bank first introduced restrictions on banks' high LVR residential mortgage lending in 2013 Church says Resimac saw an increase in business, but some of these customers left once they could get their loans refinanced with banks. This meant Resimac experienced customer "retention issues" with the business coming in due to the Reserve Bank LVR restrictions proving something of a distraction from Resimac's "value proposition" around low doc, self employed, life event types of borrowers.

Another area the big banks have pulled back from is loans to overseas-based residential mortgage borrowers. Church says Resimac does some loans to offshore buyers but not many.

"We're looking for rent to cover the mortgage payments, so if it's an investment property and it's self servicing then we'll look to help with those ones," says Church.

Resimac's also formalising income servicing policies. Church says Resimac looks at rival lenders' income servicing policies and aims to place its own ones in the middle of the range.

(See all bank and non-bank carded, or advertised, mortgage interest rates here).

The following information was released by Resimac

Income Servicing Changes

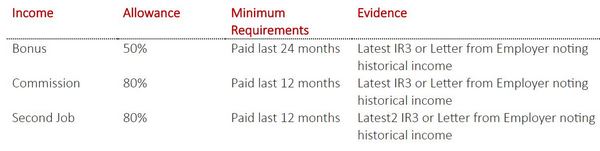

Resimac has updated some allowable incomes, for Prime loans we will now accept the following;

Living Expenses Changes

There is an improvement in our Basic Living Expenses with House and Contents insurance now being included in the minimum monthly expenses.

Servicing Other Debt

To ensure clients can continue to service their loan without financial duress we have added assessment rates to other home loan and second mortgage repayments for servicing outlined below;

Servicing other Home Loans – to be assessed at P&I at minimum assessment of rate 7% for the remaining term of the loan.

Servicing Second Mortgage Loans – Variable to be assessed with a 1.75% margin.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

7 Comments

"We're looking for rent to cover the mortgage payments, so if it's an investment property and it's self servicing then we'll look to help with those ones," says Church.

If that's the case they can't be doing much investor lending for houses in Auckland.

If they're interest only mortgages I imagine they would...

Isn't it a sign that the end is near when non-bank lending begins to seem attractive?

bigP, what a load of nonsense, you must work for a Bank!

Non Bank lenders, especially Resimac, have been around for years and provide a viable alternative to the Banks especially at the moment when the RB is holding people back. At least with non Bank lending both Investors and First Home Buyers stand a chance of getting into the market. Rates are near to Bank and there is no greater risk to the borrower.

The RB is only holding back investors from making extremely poor investments. With a rental yield of 4.5%, and operating cost (maintenance, rates, insurance) of only1%, then it is hard to see how any responsible lending institution would lend more than about 50% LVR, - i.e. it is the earnings from the investment and not the new LVR limit (of 60%) which would govern responsible lending.

Even more reason to tax investors a vancouver tax when buying existing homes as they are just skirting the LVR rules by shifting to non bank lenders.....

Are these non bank lenders going to be bailed out again like the finance companies during gfc?

If LTI were to come in would it apply to them also ? If not why not ?

If I've read the above correctly we're going to see another GFC .This outfit is probably not any different to any other non bank lender in NZ and it says it's funding is wholesale money and residential mortgage backed securities.I googled this and got:

"Residential mortgage-backed securities (RMBS) are a type of mortgage-backed debt obligation whose cash flows come from residential debt, such as mortgages, home-equity loans and SUBPRIME MORTGAGES"

Doesn't sound like very secure funding and given their lending isn't too secure,it doesn't paint a pretty picture.An outfit like this is likely to call up their mortgage a lot faster than a trading bank if things get a bit wobbly.

Not a problem if there aren't a lot of people borrowing from non bank lenders but there may be now.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.