Some odd things are said and claimed in our comment streams.

But mainly, most discussion threads are useful and add a lot to interest.co.nz.

One useful thing is that some comments cause you to think whether the claim is true or not.

There was one today that had that effect on me:

by sharetrader | Thu, 09/03/2017 - 08:13

yet wages are not rising at the same rate, so those renting will have to forgo consumer spending to afford the roof.

also if a lot of the roofs supplied are with borrowed funds, a lot more will flow offshore.

then what, will the state have to step in with more funding? from where? more taxes? less services?

this is like the train heading towards the bridge that is out, we can see what is going to happen and we are waiting for the people in charge to arrange a fix but they are having a long smoko break instead

Because I can, I decided to check the validity of the general assertion that "wages are not rising at the same rate". In an election year, such claims become freely tossed about in order to promote one political side, or undermine another.

But this one is checkable at a pretty basic level.

We track "take-home pay" as part of our home loan affordability series. And we do that for specific age-groups. First home buyer households are a particular focus of ours, and that involves people in the 25-29 age range.

And this review starts on January 1, 2007, chosen because it is just before the GFC. We could start anywhere, but that is as good a place as any and involves a neat decade's view.

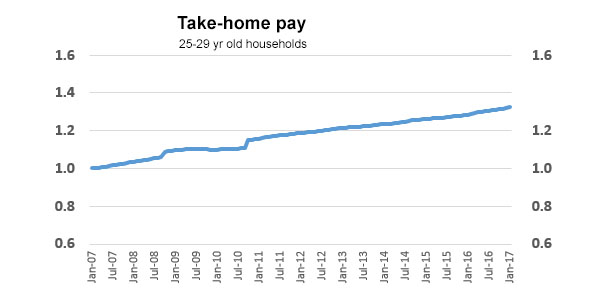

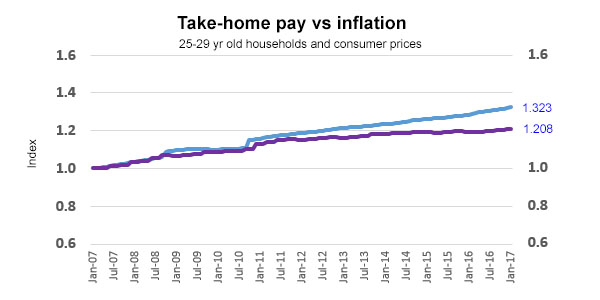

Firstly, here is take-home pay for a 25-29 year old household, national median numbers. This is a median wage for one male and one female, without children.

To more clearly compare changes from disparate data series, we have indexed the data to a 1-Jan-2007 base.

By showing this series by itself, you can clearly see the effect the two tax cuts had on household income in the past decade, and see the quite modest, but steady, rise in after-tax pay.

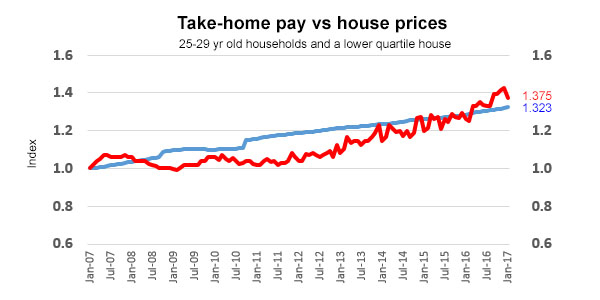

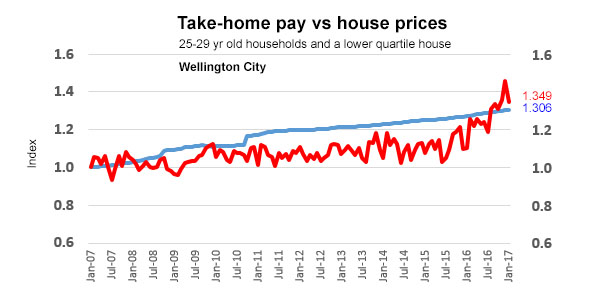

Now, lets look at how house prices have changed over the same period. For a 25-29 year old household, they will be a first-home buyer and purchasing in the lower quartile category. Again, these are national medians.

So, house prices have risen marginally faster than household incomes over this period.

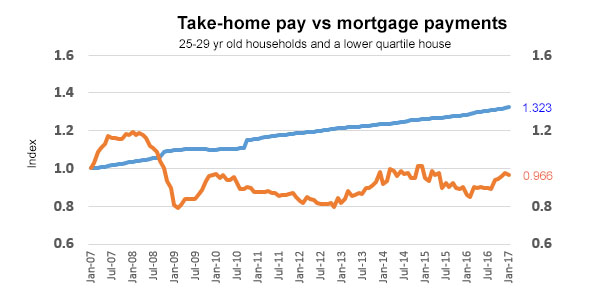

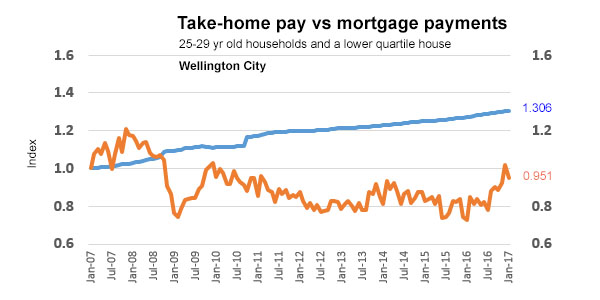

But interest rates have changed a lot over this period, falling to record low levels. That has substantially changed the level of mortgage payments to significantly lower levels.

Over the past year, it is clear that mortgage payments have been rising faster than take-home pay. But that has not been the case over the longer run.

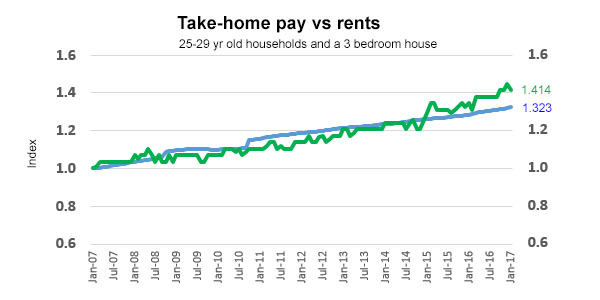

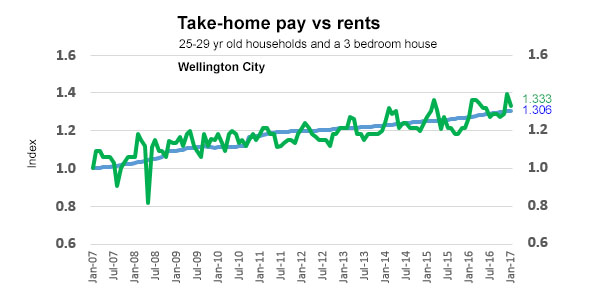

But these households also have the option to rent. Assumed here is they are renting a median 3 bedroom house.

And the story is different for rents. But probably not by as much as you might think.

For the past two years rents have been rising faster than incomes, a change from what happened for the previous eight.

So that makes Sharetrader's comment claim 'correct' - but only just.

Of course, these are all national comparatives. For readers living in Auckland, the story will be different, and worse, in almost all cases.

But for readers living in most other centres, it is likely to be 'better' than the national data.

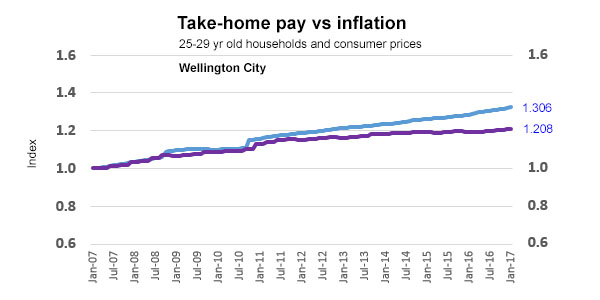

And finally, in this set, here is the CPI compared over the same period.

You can see the impact of the one GST rise in this comparative. But all the same, it is clear that first-home buyer households have made modest gains in real incomes over the past decade.

Feel free to draw your own conclusions from these data series. Mine is that there is there is a lot less to the affordability stress than is being written about (except in Auckland of course).

And our monthly home loan affordability reports pretty much show the same thing; most places are affordable in New Zealand for first home buyers, except Auckland and Queenstown. Auckland's issues will dominate the election campaigning, and discussion volumes will probably dominate the national media coverage.

Feel free to request additional comparatives in the comment section below. I won't guarantee I will add them, but depending on time available I may add some.

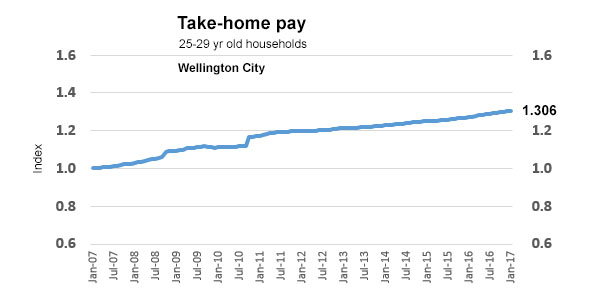

Update: Here are the same chart series for Wellington City.

36 Comments

The mortgage payments and rent comparison seems accurate for Wellington. When I stopped renting in 2014 the price of where I previously lived actually had the rent increased by 42%. Which is substantially above the median but that's CBD Wellington right now the rents are insane.

As you are using median 25-29 year old couple as a comparison where do they sit in relation to the rest of the country? Is this housing for 50% of the population? 65%? I'm trying to get perspective on if this would promote an increase or decrease to home ownership.

Unfortunately you need an INCOME. Without this, lower regional costs are pretty much meaningless

Bill English says everyone in the regions is taking drugs (which they cannot afford) and are not working in jobs (that don't exist).

True, and they're not worth helping - it's better to import a replacement workforce and consign Kiwis to the scrapheap.

I don't quite see how the rents chart shows a dip in it's most recent tracking whereas the other article on interest says that rents are up in all but 3 areas they track. How is there a dip in this graph when your other table says it is up?

Just trying to be consistent within the story. We have all series to January. Rent is the only one with February data at this point. If Feb was in there, the rent index for that month would have been 1.448.

Also, this story is focusing on 3 br houses, while the other report is of all rents - houses, flats, boarding rooms, etc.

Thankfully not all of the country is under the management of our Auckland you-shalt-not-build Council.

Tauranga builds twice as fast as Auckland per capita. Auckland creates economies of scale 10x greater than Tauranga. For Tauranga to build anywhere near as fast as Auckland would require a miracle or a disaster.

Agree, we should go the Tokyo route and put in a simple set of rules that allow people to build quickly without having to worry about silly NIMBYs.

Careful what you wish for You might become a NIMBY one day

Nice work David.

Are you able to break it out into a regional series of graphs? Or do you not have the data at that grain?

It would be nice to see how affordable/unaffordable some of the regions are..

Really great work David ! Thanks a lot, quite surprising graphs. Like Matt 73, I think it would be great to have data for different regions or at least an Auckland data and a "rest of NZ" data, as Auckland is so unique and large. Can you please provide graphs for regions, pretty please ?

Can you add a ledgend to your graphs. Which line is inflation and which is take home pay?

Great stuff. Now let's see Auckland.

One potential issue: If low-income earners are being forced out of Auckland into other areas, reported personal income will over-state wage growth. These compositional effects are tricky to address.

Nice stuff David. Are you able to add one for income vs. deposit required for a lower quartile home as mortgage repayments are irrelevant if the couple can't save a deposit?

It's also worth noting the graphs are based on a 25 to 29 year old couple, not a 25 to 29 year old individual.

This would be interesting to see with the rise in individuals occupying dwellings.

Parent Generations : Dad went to work, wife stayed at home and looked after the kids. One income paid the mortgage

Our Generation: Both Parents work, Kids go to day care /after school carer. Two incomes required to pay the mortgage;

New Generation: Both Parents work, have additonal job / spare room for rental income / Extra income from Trade Me or AIRBNB (Both parent work plus extra cash required on the side plus either selling/renting/other job) to meet mortgage requirements as wages not rising as quick as cost of living.

All this to achieve the same results.

I'm wondering how far below the median income that things get really bad.

All so we can keep investor-voters' nest-eggs growing.

But ah well, young'uns just need to sacrifice and bear the load. Those portfolios aren't going to grow without them doing their bit!

Have you read the article or looked at the graph ?

David, I like what you have done here in general. Others have mentioned a regional breakdown being useful.It is here: http://www.interest.co.nz/property/home-loan-affordability

I don't agree with the assertion that houses are affordable. Given that young people generally need to move from the regions for work. And hence the lower quartile national index stays low, because of a stock of regional housing. Median and quartiles statistics are particularly skewed by datasets which contain multiple independent distributions. For example because a Wellington, Queenstown, or Auckland lower quartile or their surrounding regions, will be much higher than the overall New Zealand lower quartile. It has the effect of spreading the distribution, but fixing the lower quartile due to stagnant regional growth. This is consistent with your regional housing affordibility series. I think it would be more statistically appropriate to use a median or mean national index.

For example compare these indexes

http://www.interest.co.nz/charts/real-estate/median-price-reinz

or

http://www.interest.co.nz/charts/labour/weekly-earnings2

vs

http://www.interest.co.nz/charts/real-estate/median-house-price-growth

also of note 2007 was after a sustained period of house price growth, what would it look like in terms of median price to median household income back to 2000 or 1990.

finity53, I was very excited about your 3 links to charts but... link 1 & 3 don't lead to charts and link 2 is just a labour chart without any connection to house prices...

Well done DC this is quite helpful in understanding the dynamic around housing affordability esp. w.r.t. rents .

My kids ( 2 of the three ) are working in "good" jobs are tertiary educated , but are struggling with high Auckland rents.

We are relatively well off as a family, for which we can be thankful, but I refuse to give them a handout to pay off someone else's mortgage in over the odds rents , particularly when they have jobs .

There is no way they can save a deposit while paying an Auckland rent that is taking a disproportionate amount of their take-home pay .

And their student loans are very small , because I paid a lot of the fees and all the books, accomodation , vehicles and running costs , food etc , so there is no real issue of pre-existing debt weighing them down.

The whole issue is very frustrating , and this is why I am in the anti-immigration camp , its a shambles that we have got ourselves into .

While I understand the value of migration , the rapid addition to our GDP , increased levels of consumption , and a widening tax base , but the disadvantages are such that its no longer worth the candle .

So, does this mean that from now on the stream of 'greedy speculating boomer' accusations on this site will cease, from XY/millenials who live outside Auckland ?

My view is that House prices have risen dramatically faster than incomes....???

David, I think it makes a big difference where the index starts..

Intuitively , with the eye, some of those graphs don't seem right..... ( house price vs income )

To see the true effects of different rates of growth you need a long time series... in my view

Check this chart out... ( I have not put alot of effort into this.... it is the result of a google search..AND... to me it looks right , in regards to what I've experienced over the last 40 yrs )

https://d3n8a8pro7vhmx.cloudfront.net/garethmorgan/pages/269/attachment…

{kind=link}

heres another one;

https://lh3.googleusercontent.com/-C6l1J7bMRfw/Vs4PHCFA2SI/AAAAAAAAe2I/…

{kind=link}

This is Australia:

http://www.rba.gov.au/speeches/2008/images/sp-so-270308-graph1.gif

{kind=link}

interesting first graph but without the source data it is a bit hard to see if you are comparing apples with apples.

the only reason I say that is one source is MBIE whilst the rest are RB and they could be measured in different ways, distorting the end result.

I say all this whilst agreeing with results of the graph as they support my point this morning that rents overall are increasing by more than wage growth and the end result less discretionary spending

that first graph is from TOP site (Gareth Morgan)

http://www.top.org.nz/key_indicators_of_new_zealand_s_inequality_erupti…

Your first 2 graphs are absolutely consistent with David's graphs and show that, over the last 10 years, wages have grown a bit faster than CPI, rent has grown a little faster than wages and house prices have also outpaced wages by a small amount. Have a closer look, same data, same outcome for the last 10 years

Thanks David appreciate your work

it would be great if you could graph the main cities, I would have a expect to see Auckland and queenstown as tough cities to live in for young medium income renters or FHB

Wellington appears to be headed in the same direction but is it, I don't know

whilst Christchurch would be the other end of the scale highly affordable and becoming more so

but how are Tauranga, Hamilton and dunedin faring

Tauranga and hamilton have been flooded with investor buying pushing up prices, so I would expect rents to have flattened but higher entry price now for the FHB

Wellington City in there now.

Thanks a lot! Astonishing really, rent perfectly in line with wages, house prices only just outstripping wages over the last year and mortgage payments significantly lower that wage growth. (although I'm sure these facts won't get in the way of people who "know" better)

Any chance to get same graphs for Auckland ? Pretty please, surely the charts will be quite different ?!

The increase is rents from 2016 is consistent with what I've seen. Over the past two years a lot of people in the living in the CBD have moved further out to seek cheaper rent. It will be interesting to see what happens as the housing shortage in Wellington continues.

Nice... BUT ... when I was in that age bracket, I was moving up the job ladder. Now that I am nearly 50 and renting, I dont think that holds true at all.

Considering 40 - 50 % (?) of people are generation rent, it would be interesting to compare where older age groups stand in relation to these indexes, considering there are quite a lot of us.

Agreed.......as part of that age group the era of me jumping jobs for decent pay rises is long over.

This is really interesting - nice work DC. Some others have mentioned it but I think an important hurdle to keep in mind is that with the rapid increase in house prices the ability to get a ~20% deposit has outstripped real income. So its not that the mortgage payments aren't outrageous on a relative income basis (because of low interest rates) but its been more difficult for first home buyers to save the required deposit (and be it in a low interest rate environment) to purchase where as movers have built equity in their existing residence. This results in them having to continue to rent and to try and save the required deposit. Like others I would love to see this data for other regional centers - Christchurch, Auckland etc. Thanks.

Very Interesting, thanks.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.