Content supplied by Westpac

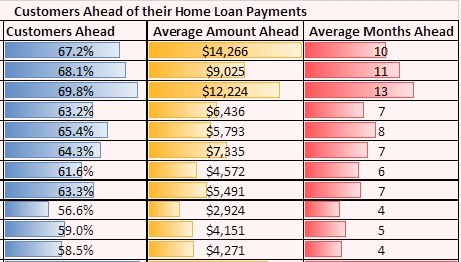

Two-thirds of Westpac home loan customers are ahead in their mortgage repayments, with customers living at the top of the South Island furthest ahead and those living in the main centres following closely behind, according to data released by Westpac.

Westpac NZ’s Chief Product Officer, Shane Howell, said home loan customers had been making the most of the low-interest rate environment to repay their loans faster.

“We’ve seen some of the lowest interest rates over a sustained period in New Zealand for some time. It’s good to see customers are using this opportunity to pay down debt more quickly.”

In the main centres, Wellington has the highest proportion of customers ahead on their repayments at 69.8%, a median average of $12,224 and 13 months ahead. This is followed by Canterbury at 68.1%, a median average of $9,025 and 11 months ahead; and Auckland at 67.2%, but with the highest median average of $14,266 ahead.

The three regions at the top of the South Island with the highest proportion of customers ahead on their repayments is Tasman at 71.1%, a median average of $10,942 and 13 months ahead; Nelson at 70.2%, a median average of $10,942 and 13 months ahead; and Marlborough at 69.4%, a median average of $9,719 and 14 months ahead.

The regions with the lowest proportions of customers ahead on their repayments include Southland at 56.6% and a median average of $2,924 ahead; the West Coast at 55.7% and $3,319 ahead; and Taranaki at 58.5% and a median average of $4,271 ahead.

Customers needed to be at least three months ahead in their repayments to be included in this data. The median customer was eight months ahead and over $8,000 ahead in their repayments.

Mr Howell said many people had come off higher loan rates during a high rates cycle a few years back.

“They’ve kept making the same level of repayment even though the cost of the loan – the loan rate – has fallen. This has allowed them to make real progress on paying down their loan faster and saved them thousands of dollars in the process.

“Alternatively, if people are able to increase the amount they repay each fortnight or month by $50, $100 or even $200 when they come to refix, it can make a substantial difference to their interest savings. It’s a smart move if they can afford it,” Mr Howell said. “We’ve seen an increase in the numbers of customers choosing to float a portion of their loan. It gives them the flexibility to pay off their loan faster.”

Mr Howell gave the example of someone paying off a $300,000 mortgage over 30 years at an interest rate of 5%.

“If that person pays the minimum $743 per fortnight that’ll take 30 years to pay off and cost $279,418 in interest.

“But by paying off an extra $50 a fortnight, they can take three years off the mortgage and reduce their total interest by more than $42,000.”

Westpac customers with floating mortgages are able to pay down their debt faster by making payments at their discretion, while those on fixed-rate mortgages can arrange to increase their regular payments at the point of refixing, or pay a lump sum at the end of a fixed rate term without break costs to achieve the same outcome.

Westpac NZ data:

The table above shows the regional breakdown of home loan customers ahead in their repayments, ordered by the number of home loan customers in the region.

*Average amount ahead and average months ahead are median averages.

73 Comments

I think this report would be much more useful if it included latest percentage of those past due and also included agricultural lending! Historical information would be nice too!

I guess that's only on a need to know basis ;-)

https://www.stuff.co.nz/business/money/83262206/Mortgage-arrears-down-b…

Fill your boots - Note 14 https://www.westpac.co.nz/assets/Who-we-are/About-Westpac-NZ/Disclosure…

98% of Westpacs retail mortgages are neither past due nor impaired.

99.6% of Westpacs retail mortgages are neither past due more than 30 days past due nor impaired

I imagine they are having many sleepless nights.

Ex Expat, gosh even after interest only, refinancing to longer terms and mortgage repayment holidays there is no steering around the 1.8% past due mortgages aye. There is no buying time for the insomnia that will erupt as the security situation slowly deteriorates in the years ahead.

Feb 15, 2007 Ben Bernanke said this; 'Despite the ongoing adjustments in the housing sector, overall economic prospects for households remain good. Household finances appear generally solid, and delinquency rates on most types of consumer loans and residential mortgages remain low.'

Thanks for the info :)

Retired Poppy, you are a poor advertisement for a fulfilling retirement. This Government is so certain of the economy they expect to take extra $4 billion each year in tax. Maybe their rapacious appetite will suck the workers dry so they can’t afford their mortgages? Otherwise, you really seem to be a broken record. Prices high, must go down, yet you can’t cite the trigger. Might as well toss a coin.

Ex-Expat, I sense an element of latency and disillusionment contained in your comments. Besides that, if your such a good judge of what a fulfilled retirement is then why do you still have to work?

It’s all here http://www.labour.org.nz/fiscalplans-forecasts. Taxinda has high hopes, she’s got high Apple pie in the sky hopes....for your money.

If you haven’t got the gist for my posts yet, I couldn’t care whether the market goes up or down. I just challenge those that position themselves as seers or gurus as in my experience those traits are nigh on non existent in the real world. Confirmation bias is strong on this forum. If the doomsayers can’t cite the trigger now for the collapse to the housing market then despite all of the posturing they’re simply saying it’s too high and must go down. That’s toss of the coin stuff. Listening to the same advice in 2008 would have screwed my life financially as the home I live in now is outside my affordability range. Not that it matters as I own every piece of it.

For the record I expect to get royally screwed in the coming years on my deposits as the government looks after the mortgage belt. I’m aiming to get into some private equity investments when the time is right. Multiples are far better in a recession. Right now I’m biding my time as there is too much positivity out there. Witness the sheeple at Sylvia Park sales on TV.

Its pretty clear that overseas money (hot or not) has driven up prices. On the back of that kiwis levereging up debt for tax relief have also played a major factor in driving up prices. NZ is not alone in this with Aussie and canada experiencing similar trends.

I acknowledge the supply side issues retard council costs and delays, material duopoly, lack of tradies. That said are you expecting the incoming policy of no foreign buyers, extended capital gain window and tax loss fencing to have little to no impact on prices at all?

I can cite a trigger for you.

To unwind the property market, you need a recession.

What do 3 out of 3 recessions in the last 30 years have in common? Falling housing volumes and slowing mortgage credit growth of the exact magnitude we have seen this year, in the 3-4 months prior to each recession starting.

It should be fairly clear to all at this point that the economy has been on the backfoot since April, but surprisingly to me, the most interesting thing is not that we are heading into a textbook recession / property bust, but the level of complacency (still) amongst market players.

A significant trigger for recession at this point would be something like a drought, a low liquidity event in the NZD similar to August 2015 (JPY, USD) that forces offshore liabilities higher, or the government doing something completely stupid like banning offshore property sales, which further deteriorates credit / volume turnover in the domestic markets, dramatically increasing the likelihood of recession (given the recession / volume sales correlation). Or maybe a combination of all three.

The residential property market is 450% of GDP. To put that in perspective, Ireland was 330% at the peak, and reverted to 80-120% of GDP in a bust. Most markets seem to long term trend around 100-150% of GDP, thats a 70% fall, nationwide in residential property prices from here, if that doesn't seem possible to you, I think you need to run the numbers and take a look at what actually drives property cycles.

Roughly 50% of property booms around the world turn to bust, and all major banking crises have had property busts associated with them. So yeah, in a way, you might as well toss a coin, just hope it doesn't land on tails ;)

Yeah, I follow NIWA numbers each day to keep finger on the pulse. Cheers for the link though

I also wouldn't be surprised by a low liquidity event.

I think its starting to look a little more than just a coincidence; http://www.treasury.govt.nz/economy/overview/2010/04.htm

"The New Zealand economy entered recession in early 2008, before the effects of the global financial crisis set in later in the year. A drought over the 2007/08 summer led to lower production of dairy products in the first half of 2008. Domestic activity slowed sharply over 2008 as high fuel and food prices dampened domestic consumption while high interest rates and falling house prices drove a rapid decline in residential investment"

Instead of high interest rates its tighter lending conditions!

Yes, the housing market doesn't drive droughts, but droughts can drive the housing market.

The domestic money market has tightened up as banks have moved to onshore funding (see rising term depo rates lately). There is not a lot of natural depth in the Kiwi anymore, banks moving to onshore funding reduces depth, as well as a lack of a carry premium 0.19% p/a doesn't compensate for any slight risks, or tail risks.

Exactly, couldn't agree more. Lots of aspects of the NZ economy are looking rather precarious and vulnerable. We can say that everything is fine, tra la la, there is no sign of a trigger tra la la, but only a fool would be feeling so confident at this time. All I see are risks in the medium term.

Yeah there are quite a few risks, the biggest and most important being (I feel).. Private sector debt, the housing market at 450% of gdp, the stress in the rural sector, and (probably the most important), there is a major correlation since 2008-9, between the number of houses sold each month (REINZ) and the changes in deposit growth at local banks, means bank deposits may actually be originating from fresh household mortgages, think about that for a moment.

The housing market is such a major cock up its not funny, a 10% drop in residential prices, wipes out as much in household wealth than twice the current government debt. I don't think people actually understand the threat it poses to the nation

Yeah, don’t worry, we get it alright. Well, some of us do.

Lalaland

"50% of property booms around the world turn to bust, and 100% of those busts have had banking crises accompanying them."

It depends on the proportion of bank assets that are related to residential property, and their exposure relative to bank capital. Typically in most countries residential property mortgages are the largest proportion of bank assets, however there are exceptions. During the Asian Financial crisis in the late 1990's, banks in Singapore, Hong Kong were able to ride out the storm and there was no banking crisis. Hong Kong banks had limited their exposure to property related lending to around the 30% level.

Residential mortgages represent about 60% of assets in NZ from memory.

Yes, spot on, residential mortgages are roughly that give or take. I'm not sure around the figures during AFC, will have to look into that.

I said it wrong, its that all of the major banking crises had housing busts associated with them, not the other way round. My mistake will edit it.

Lalaland,

FYI, the recent Greek and Cypriot banking crises were the result of a different asset class going bad - both these banking crises were caused by the default of Greek sovereign debt.

Which was a result of the property market two years earlier. Unfortunately. The debt shifted from private sector to public, and the public sector defaulted.

Here is your 30 year mortgage Mr & Mrs 35 year old, your payments come to $889.59 a fortnight, shall we just amend that to an even $900 to make things easier?

Of those kiwis ahead of their mortgage repayments ,how many own a cat or dog and how many of them are left handed.

NZ is becoming obsessed with surveys,studies,reviews and evaluations and the data is being pedalled as news.

So what happens if a customer is 3 months ahead? Does that mean that if things get tight the customer can take a 3 month holiday until things get sorted?

Try it, and see what the bank says to that!

" Umm...sorry. But you chose to 'get ahead' with your payments. We still require you to make the scheduled payments as required Mr & Mrs Mortgage ( nice phrase that!)"

Banks ARE the Status Quo. They ARE The System.

Readers often ask me to post something hopeful, and I understand why: doom-and-gloom gets tiresome. Human beings need hope just as they need oxygen, and the destruction of the Status Quo via over-reach and internal contradictions doesn't leave much to be happy about.

The most hopeful thing in my mind is that the Status Quo is devolving from its internal contradictions and excesses. It is a perverse, intensely destructive system with horrific incentives for predation, exploitation, fraud and complicity and few disincentives.The era of debt-based consumption as the engine of "growth" and "prosperity" is coming to an end. Adding debt via credit no longer creates growth; it actually detracts from the economy by expanding debt service (interest payments).

The vast majority of developed-world people have had the basics of life since the late 1960s -- transport, food, shelter and utilities. The "growth" since then depended on cheap, abundant oil and a consumerist mentality in which one constantly re-defines and renews one's identity by consumption.

Not coincidentally, this dominance of consumption as the only metric for "growth" (as opposed to, say, productive activity).

The end of credit-based consumption will be a very positive development, ( it is at its) peak and is starting its inevitable slide down the S-curve.”

(CH Smith)

Banks....give you a financial umbrella on a fine day, and take it back when it rains.....

Well we have paid very little off loans to buy rental properties.Prices have doubled! Any paying off loan would have been slight to inconsequential.In our case, its better to keep the Loan.

Most converts to The Property Cult capitalise any revaluation gain. So 'not paying off the interest' is part of The Plan.

That's fine IF prices keep going up ( as they have until recently?). Once the revaluation gains stop/reverse, the loans are still at the minimum collateral level required by the lenders ( say, 40% LVR). That...is when things get iffy...... if valuations drop. The capitalised revaluation' gain' disappears, and come next roll-over time.....it's also...Top Up time....

(PS: Is that why the RBNZ has eased the LVR's recently? To keep those on maximum loan/value above water when the Revaluation tide, goes out? Probably....)

bw, well said. It's the leveraged ones that are responsible for giving the downward correction unwanted velocity. They pose a clear and present risk to the financial system. Now, I wouldn't know if PKchew or TM2 would fall into this category but a great many certainly would! So that said, the opportunity may still be there to convert some eggs to cash so to survive any worse case scenario.

PKchew, you are correct that if you have positively geared rental property there is not a lot of point making repayments to your loans, providing your equity is such that the Banks will,continue to lend to you.

If you don’t have great equity then you should be making payments to buy the next property thru leveraging.

You make your money when you buy rather than waiting for capital gain to happen.

Some of us know of holders who have paid down their mortgage to zero but left it open so they can buy a car or boat without having to apply for an expensive personal loan.

Are they included in the Westpac figures.

Lies, damn lies and statistics?

I am amazed that many people, especially those without mortgages, don't have large revolving credit facilities. For a very small monthly fee you can have access to 100k plus immediately at very reasonable interest rates. I guess it needs great financial discipline as it truly turns your house into an ATM. I wonder if this facility has had a large influence on the property market as it makes paying the deposit for that new rental property particularly easy. Something that I have only ever used it for.

Good idea Zachary which I implemented but in a conversation with a commercial manager was told the Bank may change their criteria on income requirements as a way to effectively renege on the contract without consequences for the Bank.

Things are looking very stable at the moment. TradeMe listings have been steadily decreasing over the last few weeks and Auckland is now down to 10,623.

The November results for residential house values are now viewable at QV revealing a far from crashing market:

https://www.qv.co.nz/property-trends/residential-house-values

The outer suburbs of Auckland have largely experienced a small correction but the old Auckland region is looking particularly healthy with a 3% rise for the year. It should be noted that in 2016 values rose proportionally much higher in the West, North and South than they did in most parts of Auckland Central. Even so the North and West have rallied along with Central in the closing months of 2017.

Seems to me that the places where houses are cheap (mortgages low), people are not that worried about getting them paid down; whereas in places where the mortgages are high people seem to be keen to get them down to a more comfortable level. All seems pretty rational and sensible behaviour.

Listings are down because properties are not selling. Vendors taking them off the market. They will all come back on again next year in higher volumes.

Tui12, I agree with you entirely. There are many out there that want to cash in the paper gains but can't in wanting a bigger fool. As the months tick by, more and more will find they have to sell as the buyers retreat further.

A stable market is one with healthy clearance rates, reduced days to sell. I deplore any tactic the manipulates the days to sell because I suspect what's being reported is a spin.

A lot more agents will soon revert bank to selling Kirby vacuum cleaners door to door.

I have an evangelical colleague who describes the coming rapture with similar conviction. I think he’s genuinely upset that he has to push the prediction out each year.

Ex Expat, Why is your colleague wanting to escape another year on this earth with you? I am confident you provide regular counsel that each year will be the same as the one previous ;-)

He wants to meet the Lord. As positive an influence as I am, I can’t compete with that ;)

As for the final comment. Just like the turkey cliche, some day he may be right, but I’m willing to take a positive attitude and live each day for what it is, even if the end is tomorrow.

The two properties I know of that were on the market but are now no longer showing on trademe are simply off the market for the xmas break while the owners are out of town, and both will be back on the market mid-jan. Both properties need to sell, though not in the short term, but I expect they will drop their prices early March as their respective deadlines draw closer.

Hardly seems logical behaviour as they would have to pay over $500 to re-list on trademe. Anyone who really wants to sell would leave the property listed on the market, worst case scenario you can take their details and arrange a viewing in the new year. Just because it is listed does not mean it has to be available for immediate viewing.

In one case their exclusive contract with the agent had expired and they weren't impressed with the lack of offers. She will relist in the new year with a different agency hoping for better results. Needs to sold by end of May (iirc) to downsize to one of new build apartments going up at Avondale racecourse. Drove past earlier today and the sign was gone, and it's off the real estate companies website. The cat didn't care, she was still sunning herself in the middle of the driveway :)

Will keep an eye on trademe and see if it sells in the new year, and what price (if any) it gets marketed/sold at.

Geez, it is Xmas New Year period and still many of you are bitter and twisted about the price of houses.

The market will do what it will do without any of your influence.

I would be more worried if I had recently bought a Bitcoin.

The only reason the markethas slowed is due to the Reserve Bank altering the LVRs and nothing to do with demand.

Providing you are buying attractively, that is House is a great buy then you would be stupid not to be buying if the figures stack up.

There will be some incentive for first home buyers introduced this coming year which will keep prices very stable.

Opportunities in ChCh present every week for the City that is going to be the most desired in Australasia going forward.

" that is House is a great buy then you would be stupid not to be buying if the figures stack up." Which begs the question: Then why is the seller, selling? If it's such a good buy, then why sell it?

The answer in almost all cases boils down to - debt, and the capacity to access it or willingness to take it or more on. Remove the debt capacity ( the RBNZ LVR changes were a first, but poorly executed, first attempt) and The Game grinds to a halt.

Once debt is no longer productive ( and housing is consumptive, no matter which way it's viewed) it firstly becomes counterproductive ( $1 of debt creates 50 cents of output) then it becomes down right dangerous ( $1 debt gets wiped out -ie: negative equity to property owners) and at some stage 'dangerous' is going to happen, if it hasn't already......

There are many reasons for people selling. An investor may get the hard word from "her indoors" to upgrade the family home and thus sell a property to get more cash. Happened to me, sold a "great buy" for someone who subsequently made 300k. People move to different cities. People move to the countryside. Upsizing, downsizing, moving to a retirement home, divorce and so on. Sometimes investors just want a bit of churn. It's quite good to sell and pay off a mortgage. Banks may like to see this from time to time. Shows you are in control of things.

Inflation is always going to be a factor in house prices as is gentrification of areas, the tendency of cities to expand and small towns to decline and so on.

Why sell a great buy? Often it is very hard to detect a great buy and it is only apparent some time afterward. THE MAN 2 fancies himself as someone who can sniff out such things and he may well be right.

Correct. Usually a person who has fallen on hard times and has to liquidate in order to placate the financiers, their wash-up will be conducted away from the spot-light. Spivs are like sharks smelling blood. They make their own luck. And we can all be certain there are long-time Christchurchian residents who have capitulated and decided to liquidate and depart, putting their house on a market that is now less than effervescent. If they are committed elsewhere and have a timeframe you can be sure a spiv or two will be circling. Good pickings.

I understand all of that, but my point remains "Why would a seller, sell? ( if they knew that time would up the value of whatever it was they were selling). I wouldn't; you wouldn't - even if we 'didn't want it' for all the reasons you mention above. IF the price is going up - guaranteed - and debt is available, then who would?!

Before about 1985, you HAD to sell, to move. The Banks didn't extend loans beyond one house and they had to adhere to all sorts of ratios (LVR's + DTI's in effect), and for the general population upsizing or downsizing meant 'selling the house'. It changed in the 80's with the free availability of debt ( otherwise why would anyone have sold a 70's house! - They were 'going up' at nearly 30% p.a.at one stage, and most people were free and clear of the original debt, even then).

The only reason to sell, no matter what it is or where is, is lack of the capacity to hold it IF the price is going to escalate. The uncertainty of that 'guarantee' is the reason of course, and that is going to be a bigger reason as prices 'plateau'. As prices stagnate or fall, more sellers will sell....That...is what 'they' are trying to avoid, and they may, but if they don't.......

It is more than likely that house prices will continue to fall in New Zealand in 2018 ,especially in Auckland and Christchurch. There are now houses on the market in Auckland including the leafy areas which are simply not selling as the buyers are not there and of course Christchurch has a huge oversupply as people do not want to live in such a dire cold disaster prone spot away from where the real action is. There was a time when one should have reduced one's exposure in both spots but that time has passed and now we only hear from angry property investors who simply cannot handle the government and RB intervening in their domain. And they fool themselves by saying bricks and mortar is safe from outside intervention.

Tells you something if the RB and government have to intervene though.

gordon, I'm a believer that skilled investors make money in a falling market - they are certainly not buying in this one.

It's easy expanding ones wealth on the way up. The cafes were full of success stories and even my taxi driver handed me tips. Soon a lot of the cafes will close.

As the saying goes "a fool and his money are soon parted"

6000 properties sold last month. Many to investors.

Zachary Smith, in the absence of capital gains, do you think gross rental yields of say 3% before expenses is a viable business proposition?

If not, then your comment should read "6000 properties sold last month, many to naive speculators"

The only reason the market has slowed is due to the Reserve Bank altering the LVRs and nothing to do with demand.

Really? LVR's have nothing to do with demand and had no influence on demand

Har Har Hardy HarHar

Of course the LVR has to do with the demand!

Most buyers have been affected by the LVRs!

Gordon, thank Christ you don’t live in Chch we wouldn’t want your moaning type in such a lovely city.

You know nothing about living in such paradise.

Auckland has so much going for it. Plenty of jobs, great beaches and lovely weather. No wonder it has a big population that is growing.

Yes it has, so called unaffordable housing, shocking traffic, rains all the time, large families, crime, very poor sporting teams and many other great things Gordon!

“Large families.” The fact you think like this says everything about who you really are. I feel sorry for you.

Everyone seems to want to live in Auckland because of its great weather and excellent work and business opportunities. It would be good for New Zealand if some of the immigrants and New Zealanders went to the South Island and those parts of the North Island which are struggling to grow their population and are stagnating economically at best. Let’s hope in 2018 we see a turn a round.

Why do we want to grow our population? The world is already over populated. We truly have to get over this.

... actually ... if you squished the entire human population of the planet into one spot , and gave each person one square metre of space ... we'd nearly fit the whole of humanity onto the East Falkland Island !

And , quite frankly , that's a bloody good place to leave them ...

But the East Falklandese wouldn't think so! Imagine what would happen to the price of property there.....even 1 square meter bits.....I'd better get in early, I guess. What's the phone numbers of the Harcourts office in Stanley?...

You can pack 'em and stack 'em as tightly as you like, but they still need land and ocean for food, as do other species. Our species has "need" for other resources, mostly finite as well. Then there is the wee matter of, well, wee and poo.

Yes. Population stable is best for us.

No, keep them in Auckland! Build a wall. Why ruin the rest of the country. We do not want to be Aucklanders, we do not want to live in Auckland, we do not want to think like Aucklanders and we certainly don't want to talk about houses and sunglasses all the time.

Each country has cities that immigrants move to. The locals that can then move out as they can afford to live somewhere much nicer on the money they made from their house. Haven't you seen "Escape to the Country"? Do you think the word Escape is accidental? Jeez.

Yes indeed - all newconers want to live in Auckland - in about 5 years the migrant percent of the Auckland population will exceed 50%

An unfortunate event in the past week demonstrates the appeal

A 20 year old sub-continental from Mt Roskill driving a 1 year-old Mercedes-Benz smashed into the side of a mini-taxi driven by a sub-continental also from Mt Roskill killing him instantly. The 20 year-old sub-continental from Mt Roskill was 3 times over the breath alcohol limit. He and his passenger did a runner. The deceased sub-continental had been in country for 2 years on a work-visa. He leaves behind a widow and a 6 month old child. The widows visitor visa expires in February 2018. She will return to India for a ceremonial internment. She wishes to return to New Zealand. No Family. She and the child will be on NZ welfare for 16 years. It is unlikely she would get a job as a 40 year old widow of a taxi-driver. What has not yet been revealed is how a taxi-driver obtained a work-visa and then managed to bring a in a wife.

http://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=11966239

The risk of our legal system allowing internationals out on bail

Don't they ever learn?

In an identical car smash in 2008, International Student Puneet Puneet was drunk and driving at 148km/h in Melbourne's Southbank when he hit two pedestrians, killing one of them. Puneet Puneet, an Indian international student in Australia fled to India while he was on bail in a hit-and-run case. He was allegedly drunk and crashed into two pedestrians, killing one and badly injuring another while driving at 148km/h in Melbourne’s Southbank in 2008.

https://www.sbs.com.au/yourlanguage/punjabi/en/article/2016/09/28/stude…

He did a runner while on Bail

Puneet is now facing extradition proceedings in a court in Delhi in India

The Australian legal system has been trying to extradite him back to Australia from India since 2008 without success. And they are still trying to get him

It would have been less expensive to keep him in jail

Check out some of the delays offered up by Puneet who is now in a wheelchair

https://www.google.co.nz/search?q=puneet+puneet+2017&ie=utf-8&oe=utf-8&…

Only people who come from even worse congestion, pollution and over-population think Auckland is a great place to live and could use more of the same, them and anyone with enough money to negate the problems. Would not want to live there ever again.

This is all very good – but economics 101.

It would seem demand overall may be held somewhat in check for the moment – and is I drive around this fair city, although now frequently at a crawl thanks to all and sundry, I do believe supply appears, visually anyway, to be on the upswing.

Do be careful all those new carefree investors – it’s far from often a one way street – congested or otherwise!

I grew up n Auckland for the first 22 years of my life. Auckland has so much going for it when you are coming from Shanghai or Mumbai but when you go and live in places like London, Sydney, Melbourne, Vancouver or the States you realise how little Auckland has going for it. And Auckland gets 2/3 months of good weather a year at best so I certainly wouldn't have that as a factor unless you're from Invercargill.

And it's house prices are up with the best of those cities! Nonsense really..

Im all for moving out of Auckland, its what I want to do, move to the country and the beach, but I do like Auckland along Kohimarama and St Heliers, plus Devonport all the way along the coast down to Orewa. Including Browns Bay and Whangaporoa. Bucklands beach, Maraetai, Beachlands are good also. Eastern beach across from Waiheke is great to go for a windsurf then have a coffee afterwards.

I have lived all over in London for 16 years and give me a pub in Browns Bay with a sea view, watching the skateboarders or having a BBQ. Then the grotty buildings of london and the huge population. London was a great place single and loved the pubs, but not great for kids and doing outdoor things. In Auckland while working across from viaduct, my friends and I took half a day off, and went straight from work and fished over in Waiheke, as my friends boat was moored across the road. Something impossible to do in London. Once your fishing around Auckland with a chilly bin full of beer, catching some fish, London just can't compete.

Also if your into your Watersports its easy to go windsurfing, kayaking and kitesurfing.

Look at average temperatures London and Auckland, the coldest Auckland is 11 degrees there are 6 months in London that are 11 degrees and lower.

Also London averages approx 1480 sunshine hours a year, whilst Auckland averages 2008 sunshine hours a year, over 500 hours extra.

http://www.holiday-weather.com/auckland/averages/

http://www.holiday-weather.com/london/averages/

Are the property prices excessive for NZ incomes, absolutely, but Auckland is still a nice city in some areas, traffic not withstanding.

Myopic much..compare actual like to like...an international city Auckland is not...compare an actual international city with a coast line if you must. London has so much more diversity of interest and creativity...it does not pretend to be what you compare it with....there is a real reason one attracts six time the population to the same general area...it just may not be the reason that would attract you...

Eff off Tui...im from Invercargill...it has its good points and the weather isnt one of them but if you like getting out and about and enjoying the natural attributes of our lovely country you cant beat Southland...

What drunken monkey decided on the order in that list? Must have been a hell of an xmas part at Westpac.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.