How investors relate to benchmark bonds in secondary markets is the economic canary-in-the-mine.

Investors signal their intentions through the yield they will buy or sell such bonds. As a group, they arbitrage variances and watch the curves.

A yield curve is a line that plots the interest rates, at a set point in time, of bonds having equal credit quality but differing maturity dates. The most frequently reported yield curve compares the two year and ten year government debt. This yield curve is used as a benchmark for other debt in the market, such as mortgage rates or bank lending rates, and it is also used to predict changes in economic output and growth.

The shape of the yield curve gives an idea of future interest rate changes and economic activity.

There are three main types of yield curve shapes: normal, inverted and flat. A normal yield curve is one in which longer maturity bonds have a higher yield compared to shorter-term bonds due to the risks associated with time. An inverted yield curve is one in which the shorter-term yields are higher than the longer-term yields, which can be a sign of upcoming recession. In a flat (or humped) yield curve, the shorter- and longer-term yields are very close to each other, which is also a predictor of an economic transition.

As has been noted before, New Zealand's place in the global economy is quite specific. We are a suburb of Australia who is a province of China, the main supplier of consumer goods to the vast global economic engine that is the American middle class. Their political leanings may seem a bit odd but they have massive buying power. And that drives economies that are highly interrelated.

The American middle class demand (as represented by US retail sales) is growing in a healthy basis, but another engine is rising; the Chinese retail market. This year it will surpass the American one in absolute size even if the per capita metrics still greatly favour the Americans. But what has been a trade from China to satisfy the Americans will now change and be increasingly diminished as China's demand keeps on rising. Given both are at the same size now, you can get an indication of the way things will change by understanding the American retail market is growing at +4.2% per year nominal while the Chinese one is growing at +10% per year. The change will transition quickly.

So from a New Zealand policy and economic point-of-view, we need to watch both economies closely because these trends will affect us. Watching doesn't mean we approve of what either is doing politically or economically, but the only advantage we have in our tiny size is specialisation and nimbleness in the face of their enormous size.

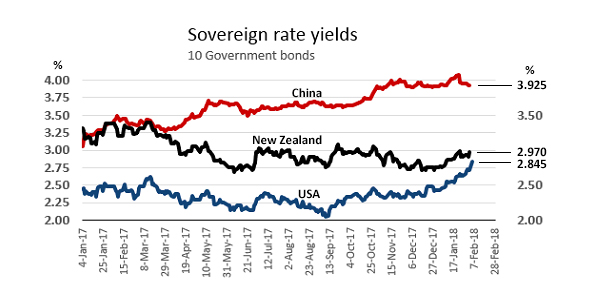

Firstly lets look at the recent trends in the benchmark bond yields of all three economies. Investors have applied the lowest risk premiums to US Treasuries. Rates have been stable all through 2017 as the US Fed came to grips with how it would taper its quantitative easing. Now that is embedded, investors see rising inflationary risk in the long term, not only from the populist fiscal turn and its implications for a sharp growth in long-term debt levels, but because the underlying economy is improving especially on the jobs front, and the long-awaited wage pressure is finally evident. Skill shortages and rising demand will be inflationary and investors see higher interest rates long in to the future. They are starting to respond; and if bond prices start to fall, all the more reason they need a higher return. And if the US Treasury comes to market for more funds they will need to entice investors with higher rates.

Since September, these rates have risen +75 bps.

China's rates are harder to articulate because officials actively manipulate markets. But markets are growing and more and more debt is being held in the open secondary markets. And these markets have bid up yields +70 bps since the beginning of 2017. Investors are getting to accept that China is successfully transitioning to services and consumer demand, away from command fixed asset investment, and that is making them more comfortable. Still, investors still want at least 100 bps above US equivalent rates for the 'interference' risk.

New Zealand is different to both. We are not seeing significantly rising rates yet. But by implication investors are very happy with the relative fall in rates compared to both the US and China. Demand remains strong for NZGBs and credit default swap premiums are bumping along at historically low levels. The signal seems to be that current prices fairly reflect the low risk the New Zealand economy poses. If you take the 10 year bond as an indicator if risk, the premium between the NZ and US rates has never been lower and it is at such a level now that a discount seems entirely possible. That is, the US poses more investment risk requiring higher rates than New Zealand. Odd, but the charts reinforce that possibility.

But there is more to this story than just rate levels. As we noted above, rate curves tell their own stories.

You can look at these curves as a way to see what markets are signaling about the future. A flat curve suggests investors see the future as 'more of the same'. The interest rates for short and long durations give a fair premium for the time-value of money.

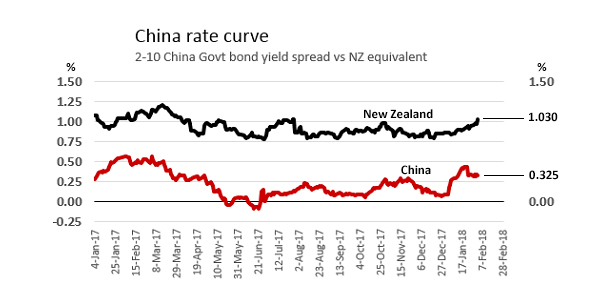

Interest rate inversions - where investors want higher returns now because they see short term risk more challenging than long term investment - suggests coming economic troubles. Chinese markets started suggesting that in mid 2017 and when Chinese officials noted the signal, there was an unusual sudden 'correction', to the signal that The Party is trying to impose. These markets are large however and investors aren't usually fooled by such manipulation, although they will happily take the government's mis-pricing pressure. But when it became clear that the investment-to-services transition is a real thing, peace broke out. Having said that the 2-10 premium is tiny and indicates well-founded lingering scepticism.

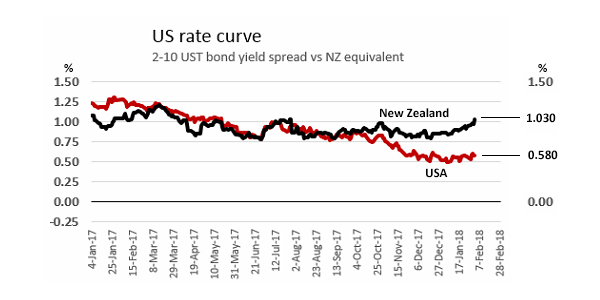

Perhaps even more sceptical are investors in the new, odd American markets, where policy makers are trying to replace basic economic wisdom with bluster. The 2-10 yield curve is on a downward track reinforcing that scepticism. In simple terms, investors may be accepting higher rates but they want sharply higher short term rates for the sudden new short term risks.

Are market signals always right? Of course not. Crowd wisdom is based on what they know today. If the underlying facts change, market signals can (and do) change. Equity market signals tend to focus on the very short term 'crowd wisdom' while bond market signals tend to focus on much longer views. Even so, bond market signals can realign even if they don't have a habit of doing so quickly. One of the longest bond market signals is the UST 30yr yield. This one is ignoring today's rapid changes, remaining entirely sceptical.

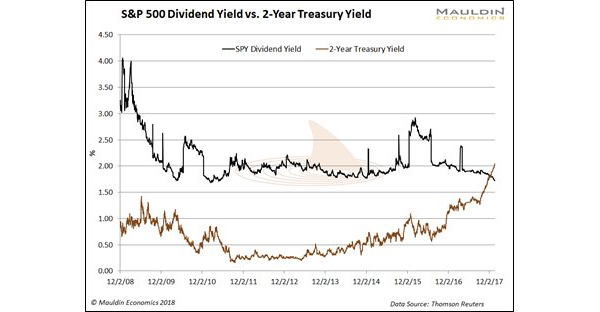

And here is something else. The S&P500 dividend yield is now below above the UST 2 year yield for the first time since August 2008.

Risk premiums

Select chart tabs

26 Comments

Fantastic article, thanks

Yes, interesting article, & good insight into our global interconnectedness.

Interesting how the GFC in 2008 did not affect NZ as severely as the rest of the world, other than the drop in interest rates as an insurance measure against recession. If NZ mortgage rates had stayed at 8/9% from 2009 to 2017 how much lower would house prices be?

Not much lower. High interest rates between 2000 - 2006 didn't slow house price growth.

Much, much lower today indeed, the reduction in Interest rates is the main driver of house price inflation.

You can look at these curves as a way to see what markets are signaling about the future. A flat curve suggests investors see the future as 'more of the same' [my link addition]

{kind=link}

Indeed.

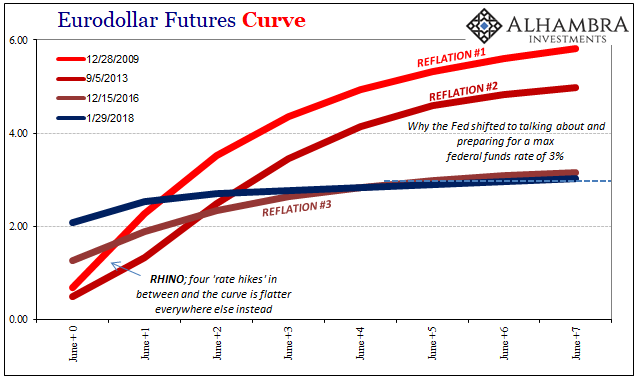

What the Fed is doing now isn’t hawkish one bit. They are still confused and nervous, confounded by always the “transitory” disturbances. The last downturn is two full years in the rear view, and yet they still have no confidence to act in an upfront and determined manner. That’s on top of ten years since the initial emergency began.Time is the ultimate arbiter.

The reason they hesitate is 2%. Inflation matters because it signals to policymakers that there is a more than trivial chance they are wrong, and that the economy hasn’t shifted out of its uneven, no-growth paradigm. The FOMC, I believe, knows it, too. They are using once more their patented fingers crossed strategy, the one where its members just hope for the best because you never know, the world could strike upon nothing more than random good luck (which is the term I hear instead whenever someone says “globally synchronized growth”).

That’s what “hawkish” means in 2018. Like the economy itself, the very idea is appropriately shrunken. Read more

Great article!!!thanks!!!

Good article, helped clear up some things. Just a quick comment:

The S&P500 dividend yield is now above the UST 2 year yield for the first time since August 2008.

I think it's the other way around.

Gulp. Quite right. Fixed now. Thanks.

David C at his very best. Well done !

A very well written article - love the graphs - not too long - clear with very good analysis. The reason I visit interest.co every day !

Whether or not the recent panic sell off is justified will be revealed in the next US inflation release. One strange thing is that the USD has continued its weakness despite the run up in bond yields.

Taint just Bitcoin that is tainted. Taint just US stock market is tainted, Taint just Awkland real estate market that is tainted. Tainted economies can borrow themselves into oblivion. Taint obvious to some.

Tis to me.

But when they each expect a rise out of the average man, woman and child, then they should think twice.

Even Mr Trump thinks that another trillion in tainted debt is gonna make America great again.

Mr Trump relies on debt. That is so rich. That is so stupid.

But then the sheeple may not realise, it is due for a haircut, starting with Mr Trump.

America is dropping the hint. ..to one and all...It is broke. It needs print like never before.

And the money from Asia that dried up coming to Awklands markets may give Awkland a haircut too. Just like what Mr Trump needs, but never imagines.

Any fool can borrow money, but repaying sub prime debt, with sub prime means, means the money go round may stop and the stocks slide, when the tide goes out, the Landlords expect the common man to pay the not uncommon debt, they actually incurred, always expecting a raise...papering the cracks.

The common man did not get one. A raise that is..They is laying orf people, left, right and centre. Even Banks are doing it.

Get real.

Your debt, is not mine. So stop trying to pass it on.

The buck stops...here.

My name is Bond, .....and my word is my...Bond.

Well said Alter Ego. Unfortunately, when the GFC occured bankrupt companies WERE bailed out by the common working man, insterad of letting these companies die and all suffer for a short time and be able to move on. I see the problem of having the taxpayer pay for the bust companies two-fold: 1) It is obviously wrong spending good, hard earned money on ill-managed, failing companies/individuals 2) The lesson it teaches is: get into debt and don't worry, if you fail you will be supported, which is understandably the attitude of many today.

For crying out loud, it does affect people...other peoples money. This is just one of many.

https://www.marketwatch.com/story/xiv-trader-ive-lost-4-million-3-years…

Of course it affects people, very much so, Ididn't disagree with you

I was just making the point, it was that bloke crying out loud....I was not getting at you.....

What is a few million...between friends. Maybe a trip of a lifetime...cos someone tripped up...big time.

What is a few Trillions to a Yank....They can make money, coming and going...ripping orf us mere mortals.

I only print on here...what I see as the biggest fraud in History...And it is getting bigger.

Time to shift your Kiwisaver to a Cash Fund?

Can you do that?

Sure, within the same provider you can shift from Growth type Fund to Conservative for e.g., or from Balanced to Cash. You can do it online with many Providers, without the obligatory 30 minute 0800 wait!

Thanks, I'll check it out. Hopefully I wont cause the market to crash even further if I decide to do that!

Don't switch it! Ride it out. Besides you now have the opportunity to buy more shares at a much lower and fairer value. Those shares will outperform cash and mortgage backed securities over the next few years. And why would you want to switch to a fund that is mainly invested in residential mortgages and or cash? I think that is where all the risk is with the amount of debt that people have racked up. You would be getting high risk for low return and it should be the other way around.

I took some profits off the table over the past couple of weeks, but won't be selling any more shares. Too late now that's it's going downhill, and I'll be able to buy while it's down. Mine are spread around all the world's markets, so I figure if it all goes to zero we'll have bigger things to worry about.

Zachary Smith, transferring to a cash fund is not immediate. I transferred my Kiwisaver to a cash fund 9 months ago and it took a month. It's an opportune time to point out that subject to this correction evolving into yet another GFC, house prices are next for massive declines as this is the trigger many commentators have warned about. Central bank toolbox is bare.

Best not panic Zachary, shed that debt and ride it out.

not a good idea, you need to look at your time line, ie when you intend to retire and set for the long term.

if you are retiring in five years, yes go more conservative cash , bonds very little shares

if longer than ten years set accordingly.

we know there is a bear market coming and a correction plus interest rates should rise but history shows us over the long term international equities outperform most other investments

also depending on provider you may be able to set a percentage in each fund,

my fund manager does so i can adjust percentages for growth, balanced and conservative

my fund manager also shows me what i am invested in which helps set my levels

The rise of the Bots...must have been a Power Outage...get with the program.

https://www.bloomberg.com//news/articles/2018-02-05/robo-adviser-websit…

Don’t panic apparently – Cramer calls it just another “flash crash” type of event – certainly no fan of his but he may to some extent be right.

Bit of a clue might be reflected in a rather muted response from the bond market.

A bit late but I still wanted to praise David Chaston for a great article, very well written, clear, informative and well balanced. Thanks a lot DC

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.