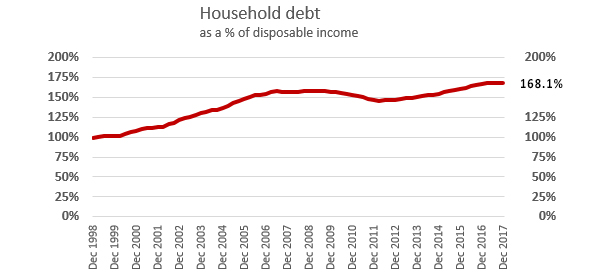

The latest update to the widely referred-to series "Household-debt-to-disposable-income" has been released and that shows it stable at 168%.

It has been at that level for four straight quarters, and is a record high. It is the source of public angst. Its most quoted source is here.

But actually, it is not as dire as it is sometimes made out to be.

The data is used as evidence about how stressed households are under the load of housing debt. It is often compared to similar metrics in other countries* to confirm how elevated this stress is in New Zealand.

However, many readers may not realise the debt figure includes property investment debt and not just owner-occupier housing debt. That extra debt is in there because it is not possible to separate out the liabilities of these unincorporated businesses from standard household finances.

This distorts the understanding of what this 'household' data is revealing.

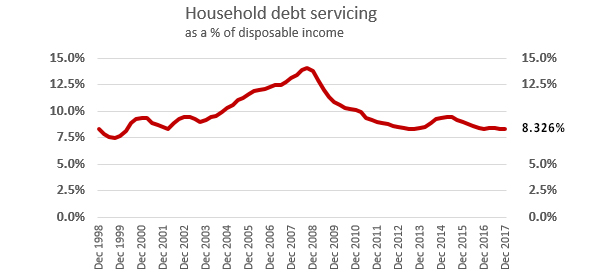

And there is another issue, one glossed over by many. The 168% is seen as a proxy for household budget stress. But household budgets don't use their 'income' to purchase houses. They actually use their income to make loan payments, mainly for interest. Real stress will come when these loan payments eat up increasing proportions of disposable incomes.

But not only is that not occurring, the load is getting lighter. The optics of the debt-to-income ratio may look bad, but inside households themselves, the debt-servicing-to-income ratio gives a completely different picture.

So, even after including the national business liabilities of household ownership of rental properties, the servicing load on household budgets is near its lowest level in 17 years.

The servicing load rose from 1999 to 2008, and has been generally in decline since, and by the end of 2017 reached its lowest point since 1999.

This is a narrative quite at odds with the normal public discussion about household debt levels.

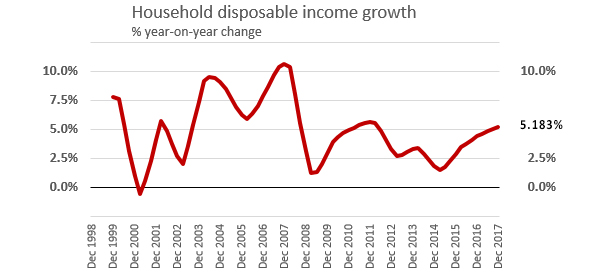

One reason why the servicing load is getting easier is that incomes are rising steadily, and the rate has been increasing in the past three years.

Another point worth noting is that household liabilities are not only for housing; they include consumer loans as well.

| Household debt stress | Dec-2007 | Dec-2012 | Dec-2017 |

| $ bln | $ bln | $ bln | |

| Consumer loans (C22) | 13.9 | 12.9 | 16.5 |

| Housing loans - owner occupier (C22) | 110.0 | 126.8 | 175.5 |

| Housing loans - investment properties | 54.6 | 64.1 | 84.3 |

| ------------------------------------ | --------- | --------- | --------- |

| Total household debt (C21) | 178.5 | 203.8 | 276.3 |

| - Household debt to disposable income ratio | 156.7% | 147.2% | 168.1% |

| - same ratio excluding investment properties | 108.8% | 100.9% | 116.8% |

| Annual household disposable income | 113.9 | 138.4 | 164.4 |

| Annual household debt servicing | 14.5 | 12.0 | 13.7 |

| - Debt servicing to household income ratio, for qtr ending | 13.105% | 8.525% | 8.326% |

This table points out clearly how much lower the servicing load is at the end of 2017 than it was ten years ago.

As a marker for household debt stress we should talk more about the servicing ratio rather than the debt-to-income ratio. The servicing ratio is the pointy end of where we will observe real stress, whereas the debt-to-income ratio is academic.

* The ability to borrow against Australian self-managed superannuation funds has pushed their ratio to almost 200%.

27 Comments

What? Wait, under Labour, household debt servicing cost went up from 7.5% to 14% of income, and under National it went DOWN from 14% to 8.3%? What have we done? Bring back Bill English!

Under Labour the economy was booming and the reserve bank had to raise interest rates several times.

Interest rates dropped significantly under National due to the GFC. John Key loved to bang on about how National were holding rates low (he didn't mention through low growth and high unemployment)

Is having mortgage debt in a lower percentage of households,undoubtedly more affluent households,who should have the financial capability to adjust if necessary, better ? Does the concentration in debt as seen by the fall in home ownership rates provide possibly a better outcome if interest rates were to rise significantly.

Isn't all of this to say that households/borrowers have hit the prudential and affordability 'stops' in the system?

Those "wealthy" enough to borrow have borrowed heavily to buy property (owner occupied and investments).

Those not "wealthy" enough to borrow spend a significant proportion of their income servicing their landlord's mortgage.

How is the debt concentrated? (i.e. Auckland mega mortgages).

Where does interest only borrowing figure in all of this?

How has the length of mortgages changed over the period shown?

How would a 100 basis point increase in wholesale rates (~20% increase in servicing) impact?

How would an increase in unemployment figure in all this?

If 168% isn't stressful then why don't we try our luck with 180% 200% 300%?

Australia is seeing increasing levels of mortgage stress despite record low rates. Caps to interest only lending are now flowing through the banking system and it is starting to hurt. Not to mention that Australian house prices are falling.

"Household budgets will only be stressed when the servicing costs rise", you sure hit the nail on the head DC, yet the majority of people can't see this.

You see Debt to Income comparison isn't smart, because Debt is a fixed Liability and Income is cashflow. Any accountant will tell you we should compare Debt with Assets (financial position at a given time) and Income with Expenses (cashflow over a period of time) but not cross over and compare Debt with Income.

Let me put that in a simple example; let's say we agree a DTI ratio of 5 is acceptable. What happens if interest cost go up 50% (from 5% to 7.5%) ? Well according to the DTI everything is fine, actually the DTI is exactly the same because the "D" hasen't changed nor has the "I", yet people will definitely struggle to meet their expenses.

DTI is a fraught measure

Neither ratio tells the full story.

What is more interesting is the amount of household income left over after all expenses (in dollars). Once that approaches 0 then you get stress.

Think Emperors and clothes ...............and thank you David for pointing this out .

So while household debt as a % of disposable income is at a peak in your first Fig , it seems most households don't appear to be under stress at the moment.

We have employment in the 90's as a % of those looking for work and there is no shortage of work opportunities .

There are always exceptions , but for the most part we have likely never had it so good , and many people are spending money like drunken sailors . In so doing some are likely to be stretched financially .

The purchase of motor vehicles is at all -time records, Banks are declaring record profits with the lowest provisions for bad debts in years , mortgagee sales seem restricted to shonky property developers facing jail sentences,, flights to Aussie and the islands are chokka with tourists , and a visit to any waterfront precinct in New Zealand over a weekend will provide sufficient anecdotal evidence of an economic boom .

But as those of us who have seen terrible downturns will attest , it can change with the click of the thumb when the cost of money rises .

And I would not be a punter willing to bet on when its likely to happen , but it will .

These figures are quite useless for any risk analysis as I have stated previously. They include all households - roughly one third who don't have debt. Confirmed by RBNZ.

Analysis of this issue requires segmentation into say deciles and analysis of each.

A very different picture will then emerge - some not so pleasant I suspect.

@JB you are probably right , many families dont have debt , and as Baby Boomer we have no debt , and have assets that generate income and spare cash that we may never need .

I would suspect that families on welfare , those using any one of the number of cash and payday lending shops scatterred around Otahuhu , or those with 3 or more kids and a single income are stretched .

Many of these folk don't have access to normal funding from main street banks

Segmentation by age , or where you live or family size , education level , or employment would paint a clearer picture .

The overall picture is clear however , that Kiwis are for the most part managing their debt quite well

Agree our generation (boomers if you like) has had two major advantages. Firstly in being able to buy into housing 60/70’s when the market was pretty much static. Secondly we were prudent and conservative by our very nature and that was helped by scarcely having any ability to incur personal debt, aside from HP. But man how that has changed. Would see one of my children plugging along in much the same manner as we did in terms of life style, but she hasn’t a hope of being mortgage free, just an average family home, by the age of 65. So DC’s article here, and his weekend’s comment on debt, are in my opinion ominous warnings that statistics in this area of concern will rapidly alter for the worse

i think you also need to look at the ways banks lent back in the 70's and how that has changed to today to see the creation of debt and the need for more and more debt customers and with that the change in attitude to taking on debt.

many older folk see debt as bad and would save to buy what was needed, many younger folk see debt as good and a tool to use to get things

Yes indeed. Recall a cartoon during that particular time of generational change, that depicted something like a banker reflecting that while it was the ambition of the previous generations to pay of the mortgage, it is the ambition of the current one to get one. That development got strapped to a rocket!

What David says is correct to a point in terms of debt servicing but household stress also includes what net discretionary disposable income services. So if increased costs in other expenditures increases ( Eg Energy/Rates/Taxes) then other discretionary expenditures become stressed, paying the mortgage and other bills is fine to the point when what is left leaves nothing for non essentials and a rollercoaster to disaster as the Jobs and business's relying on discretionary spending see their business decline.

Rumpole. Taxes haven't gone up. Because proposed tax cuts were for 'only the rich', they were cancelled. Fiscal drag hasn't impacted middle NZ homeowners - you are simply recycling a rightist myth in asserting otherwise.

Middleman- I think you have largely missed my point that financial stress occurs when expenditure equals or is greater than income. the taxes I was referring to mainly were specific duties (Fuel/Alcohol/Tobacco) and Rates which are subject to GST on the basis they are a service but if you are forced to pay something in my view that is a tax.

Nice work David, and an interesting view point - yet not entirely black and white as Rumpole correctly pointed out in the above ... but very good piece - thanks

We hope that borrowers will be able save a bit to store enough fat before the next round of interest rate rise.

I disagree with this analysis. Not because it’s wrong but in practical application I think there are some fishhooks in high debt-low interest-low inflation environment that aren’t obvious. People may have no trouble servicing their debt but that is not the same as having no trouble paying their debt off. If the question is will people pay their loans, I agree it’s probably easier. If the question is will people have the financial freedom to make life decisions and spend in a way that drives the economy, I say it will be harder. We are loading people up with record amounts of debt in an environment where inflation will do less work in eroding the value of that debt. The consequences of this won’t be fully evident until 5-10-20 years down the track.

So true. In the Labour years inflation was around 4% and interest around 7%, so the servicing cost was high, but wages were going up every year and after a few years it seemed pretty easy. Inflation of <2% is a different ball game.

As you can clearly see in the chart under labor the percent of disposable income going to housing was rising, so you are exactly wrong. That is not necessarily a reflection of labor but your point is just hilariously incorrect.

The full impact of higher interest rates is not so one dimensional as simply not being able to afford to pay the higher rate on your “current income”, It is highly likely your current income will not go as far as it once did in the higher interest rate environment and your “current income” may in fact be less in a higher interest rate environment.

Higher inflation if I’m not wrong goes hand in hand with higher interest rates, then there is the general slow down in business activity due to higher costing money and risk associated with borrowing it which then results in less work for people on “current income”. Then there is the large sector of business’s particularly service sector business’s that have never experienced a down turn because they started up in the last 10 years. These service providers (whom all have new Utes & vans!) service industry sectors that use debt as an operational business tool, not an asset procurement tool. When finance / debt becomes less feasible as a business operational tool so will the viability of a lot of service sector business’s…… less “current income”.

AEP

Hong Kong Two flats here on Hong Kong's Mount Nicholson sold for $200m CREDIT: PROPGOLUXURY “Hong Kong looks increasingly vulnerable to financial stress. A potential trigger could be an accelerated Fed rate hiking cycle,” said Mr Subbaraman. This is exactly what is now coming into focus. The Bank for International Settlements says Hong Kong’s ‘credit gap’ - the overshoot above trend - surged to record highs last year and is in a league of its own, even by the frothy standards of China and East Asia.

Nomura warned clients to braise for a lot “dead wood rising to the surface” among Asian firms as the tightening cycle bites in earnest.

Hong Kong’s banking system is 8.3 times GDP - akin to the Irish banking system on the eve of the 2008 crisis - and is a contingent liability of the territory. The HKMA has imposed strong safety buffers. The liquidity coverage ratio is 146pc, easily meeting stress tests under the Basel capital rules.

Yet the banks have seen a surge in lending to entities in mainland China that exploit the offshore hub to circumvent curbs at home, or to finance an opaque ‘carry trade’ into yuan assets. The HKMA raised raised the ‘countercyclical capital buffer’ from 1.25pc to 1.875pc in January but has signalled that this may have to go to 2.5pc. “The risks associated with credit and property market conditions have not abated,” it said.

The territory’s property boom is officially out of control. Carrie Lam, the chief executive, said eight rounds of mortgage controls have failed to stop the speculation, and may even have been counter-productive. “The government really has no way to curb property prices,” she said.

In December, a mystery buyer paid $200m for two flats at ‘The Peak’ on Mount Nicholson, designed by Alexandra Champalimaud. The development is a favourite among Shanghai’s super-rich. Chinese investors now account for 40pc of all land purchases in the enclave, despite a 15pc stamp duty for outsiders.

https://www.telegraph.co.uk/business/2018/03/04/hong-kong-risks-becomin…

Ireland was forced by the ECB to nationalise the debt and bail out the banks when their bubble burst. Who's going to bail out the financiers in HK's case?

Good point and in HK's case probably the Chinese central Bank will and can rescue them but Globally the same situation exists and there is no white white to rescue the world unless you believe Aliens will come and fix it for us!

When we hear about household debt stress, David Chaston wonders whether we are looking at the most relevant data.

Not just David. I would think that the only way to really understand this properly is to understand "qualitatively and quantitatively" about h'holds. That means continuous tracking of h'hold budgets and how h'holds actually perceive their own level of stress. For ex, how have h'hold spending habits changed? Are h'holds going without goods or services because they're more concerned about their debt? To what level do indebted households feel secure? What is their level of discomfort with their debt?

As far as I know, no organization in NZ is really tracking this.

Staggering that this article doesn’t mention low interest rates in explaining the drop in the debt servicing ratio. Rises in wages have been minimal in the overall scheme of things and the drop in debt servicing cost has been massive in comparison.

Every reader would have known interest rates fell in the period since 2008. Interest paid didn't however. It was particularly high between Dec-06 and Dec-09. But I am not sure your characterisation between 'minimal' and 'massive' is quite correct.

Using the same data source which only goes back to 1998 (C21), over the 19 years, "household disposable incomes" went up by NZ$98.4 bln, while servicing costs went up by $7.3 bln. Yes, the ratio rose, but only slightly. If anything it is the "household disposable income" number that has gone up "massively" whereas the servicing cost rise more fits your 'minimal' description.

David you are probably correct but debt is only part of the disposable income equation and if the other areas of household expenditure have increased more than income then debt stress will still exist. All our arguments are subjective and only time will prove what if any are correct but in the meantime being over cautious carries less risk.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.