Here's our summary of key events overnight that affect New Zealand, with news both China and Germany are adjusting to live with the US tariff challenge.

But first in the US, gradually rising interest rates have yet to dent Americans’ appetite for borrowing, with the total stock of household debt climbing to a record $13.3 tln by the end of the June quarter, up +3.5% in a year - which incidentally is less than the nominal growth in US GDP which grew +5.4% over the same period. Mortgages are more than two thirds of the total and these grew +3.5%. Student loans are a bit more than 10% of the total, but they grew at the rate of +4.5% pa. Car loans represent a bit more than 9% of the total household debt, and grew at +4%. Credit card debt is a smaller proportion (6.2%), but it grew at a +5.7% rate pa. the only component to grow faster than GDP.

In China, consumption is slowing, even if it is still at a high level. Retail sales rose +8.8% in July from a year earlier, but well below the +9.1% growth expected and down from +9.0% in June. And it is more than retail activity that is slowing. China industrial production in July came in at +6.0% growth, also well below expectations and the June levels.

To keep domestic demand up, China is loosening its recent debt rules for banks, and it is raising infrastructure spending, especially on high-speed railways.

China's data is in sharp contrast to that from Japan where industrial production actually fell -0.9% in the year to June.

The German economy grew faster than expected in the second quarter, driven by higher household and state spending, suggesting that it is powering ahead despite the threat of a major trade dispute with the United States. (Germany is also considering more infrastructure spending.)

This data helped the overall EU GDP growth rate, which was revised up to +2.2% real for the June quarter.

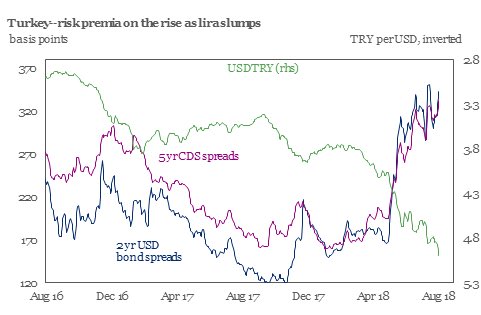

Overnight, the Turkish currency has a small rebound. But Indonesia's currency is the latest to take some depreciation hits, and they are preparing to shore it up.

In Sydney, residential vacancies have hit a 13 year high. Property investors have been hit with falling rents from these rising vacancies as the country's largest city gets an unexpected boost in supply of new dwellings. Econ101 at work. And the change is being reflected in how professional commercial property investors are acting.

The UST 10yr is firmer at 2.90%, with the US 2-10 curve still at just +26 bps. The Aussie Govt 10yr is at 2.59% (up +1 bp), the China Govt 10yr is at 3.58% and down -2 bps, while the NZ Govt 10 yr is at 2.60%, unchanged.

Gold is still down at its 18 month low, holding after its sharp drop yesterday and now a just at US$1,194/oz in New York.

After a small jump late in the day yesterday, US oil prices are softer today and now just at US$67/bbl. The Brent benchmark is now just on US$72.50/bbl. T

The Kiwi dollar is starting today little changed from yesterday at 65.8 USc. On the cross rates we are a little firmer at 90.9 AUc, and at 58 euro cents. That puts the TWI-5 at 70.1, and rising for the first time in a week.

Bitcoin dropped below US$6,000 yesterday but is now just over at US$6,032 which is -1.6% lower than this time yesterday.

This chart is animated here. For previous users, the animation process has been updated and works better now.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

15 Comments

Falling residential property rents in Sydney, right on que....

Yeah, not a good sign at all. FONGO will start to bite. It’s such a crazy bubble over there, surely their luck has run out. It may be the beginning of a major property bust. The idea you can support asset prices at the top of a bubble solely by cutting rates is about to be tested to destruction

https://www.domain.com.au/news/rental-vacancies-in-sydney-hit-highest-r…

In Japan’s case, as anyone’s might be in the same situation, there should be no stone left unturned when confronted by such a substantial break in economic function. A dislocation of that magnitude, meaning length of time if not depths to some 1930’s trough, demands emergency thinking rather than stolid patience almost to the point of indifference.

To be so relatively passive would be a crime, especially if the results were to be losing a decade of actual economic sufficiency. Dr. Bernanke argued for thinking way outside the box, for what else would be demanded by this sort of situation?

Federal Reserve Chairman Bernanke, by contrast, was apparently unimpressed by his earlier urgency. I wrote just a few short weeks ago that though the Bank of Japan was run by clowns, I’d prefer the clowns every time to the corruption that has so thoroughly inundated “our” central bank.

You see, the Japanese at least acknowledge their problem, meaning that they still have one. Western Economists have taken a far darker path, one begun under the self-induced paralysis of one Ben Bernanke. They haven’t made recovery so much as erase the problem from the official canon.

Yesterday, we spotlighted Brazil’s economy as perhaps a leading indicator for where things stand. Today, it’s China’s turn. Neither are very encouraging. Both offer instead only growing concern. The reason isn’t just the possibility of the world economy rolling over in 2018, rather it’s from what level any deceleration might have begun.

Despite the characterization of especially the US economy as some powerhouse reborn from supply side do-gooders, Reflation #3 never really got going. Markets were up but none outside of stocks actually did all that much, most only having retraced a small part of the “rising dollar” collapse.

Many of the world’s national economies performed in exactly the same way, not that that has been surprising. One follows the other. Brazil has behaved like that, being utterly devastated by the global downturn in 2015 and 2016. They have proved the “L”, an exclamation point further provided if their economy is indeed on its way down again already.

The same for China. Globally synchronized growth was supposed to speak Chinese more than any other language. And yet, there wasn’t near enough momentum at any point along the way. Now, like Brazil, the downside re-emerges from a far shorter peak than anyone has been able to imagine.

http://www.alhambrapartners.com/2018/08/14/ugly-chinas-american-mirror/

No, a country with monetary sovereignty cannot issue all the debt it needs without default.

Countries don’t borrow in foreign currency because they are dumb or ignore MMT science fiction, but because savers don’t want gov’t currency debasement risk. The first ones, domestic ones

Daniel Lacalle

https://pbs.twimg.com/media/DkjRuyQXgAAMOj0.jpg:large

{kind=link}

Keep an eye on these guys

https://www.businessinsider.com.au/indian-rupee-turkish-lira-crisis-ris…

I will ask again. With current uncertainty In NZ economy which way for interest rates. While RB talks flatline with options up and down. My bank just raised my business floating rate so what is the real relevance of the OCR? How bad do things need to get for overseas investors to take their money home and push our rates up? Or does uncertainty mean interest rates can only fall.

The OCR is largely irrelevant especially in extremis. Rates are already very low, making them lower won't do much, banks have no interest in passing on the discount and anyway it makes it very difficult for them to make money when interest rates are so low as it puts so much pressure on their spreads between deposit rates and loan rates.

We are a tiny economy very much at the mercy of large global forces. The NZD has fallen considerably this year so it is likely we will import inflation. The USD continues to strengthen. That coupled with the amount of industrial action, governments wish to increase minimum wages, and the reduction of the importing of cheap labour is likely putting upward pressure on wages.

Expect inflation because no one else expects it and that is when you get it. No one in the main stream is predicting a surge of inflation here. And the herd is always wrong at the inflection point.

The OCR may well be forced to raise interest rates, to shore up the NZD, which will of course put pressure on mortgages as eventually the banks will raise as well.

I have no certainty of what will happen 10 minutes from now. But if I had to say, my pick is rates will rise suddenly and by more than expected.

Thanks for your reply. Unlike residential loans our loans are structured with our floating rate being lower than any fixed term offer over six months. It means if we take the security of fixing even for 2-3 years it comes at a cost to our business.After reading the previous RB governor's comments about interest rates we fixed and got burned as rates continued dropping. Try to learn from my mistakes so treading carefully this time. But I agree with the sentiment that when everyone says the same thing the opposite is likely to occur.

Hi Wilco

Reserve rate will stay low for as long as it can, but my belief is that the 'forward guidance' by the Governor is aimed at weakening the dollar to aid exports and tourism. The import of inflation will be the counter-balance which will be accepted for a while as a necessary evil. But rates, both the reserve bank and bank rates will be going up again by second half of 2019. You probably still have a bit of time before you commit to a position either way.

Yep, you make a prudent call there Nic.

I would expect inflation to start coming through in the next 3-6 months. So you probably have time.

I guess fixing is like insurance though at the end of the day.

Yeah you pay more, but you know exactly what you will get over the term of the fix. My personal view is that that certainty is more valuable. The property I own was fixed at the beginning of the year, but for me the difference between fixed and floating is not very large.

And of course Wilco, you will understand your own circumstances better than me.

In addition to my comment below. Central banks are not in control of the trend, but can meddle around with the peaks and troughs within it.

Agreed. They have little power in extremis. If they cut now banks won't pass that on why bother? It is already difficult for them to make money on the spread between deposits and lending.

The same when interest rates are very high the banks may not pass on rate rises as it would choke their ability to loan and make money.

But they can tinker that is true.

It has been my call since 2013 that interest rates will trend down. This is an international prediction, not just New Zealand. But within a trend there will be cycles of up and down. So the question to you is what is your time frame for consideration?

Another part of the equation is the supply of money, since interest is the cost of money and reflects the quantity available. Also be very clear that all money is introduced into circulation as interest bearing debt. So the full equation is that interest rates are inversely reflected in the availability, or expansion rate, of credit. You can look at the data from either for your analysis of the trend, and the point we are at within the trend. For local rates the quanitity of mortgage lending would be a reasonable proxy for where interest rates are moving.

Local rates are very much affected by the international situation. So the FED raising rates is tightening up on credit everywhere. The FED being the largest, but not only, player in this game. The ECB, BOJ BOE, and PBC can all move the credit markets.

Now for the good bit you didn't ask about, what drives it all. My prediction is partly based upon the nature of compound interest, or its close cousin compound debt. Interest compounds as a portion of the money supply. As money become less affordable it has to be made cheaper. Eventually rates will get to zero as debt will be completely unaffordable. All asset classes that command a yield behave like money, so all asset classes will also head towards a zero yield.

The whole system is of course based on the exponential consumption of resources to pay the rent, a situation that is, by the laws of physics, impossible to underwrite indefinitely.

Additionally for your consideration is that we are in the middle of a credit fueled asset bubble bursting. A bubble caused by too much money being available (at low interest rates) that have flowed almost exclusively into housing in this country, but all asset classes pushing up their prices.

{kind=link}

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.