Here's our summary of key events overnight that affect New Zealand, with news the world's largest economy seems to be losing its growth momentum.

New orders for American durable goods fell at a sharp rate in October from the previous month, a decline that analysts weren't expecting. Year-on-year however, the levels are up +8.7%. The monthly decline suggests an economy slowing faster recently than has been assumed. The Atlanta Fed's GDPNow model has the rate of growth pegged back to +2.5% pa in Q4 and way down from the Q3 rate of +3.5%. Momentum seems to be leaking away, and quite quickly.

Telling the same story of a slowing is the latest consumer sentiment survey. And American home buyers filed the fewest applications for mortgages in almost 18 years last week even as mortgage rates drifted lower in step with bond yields.

Perhaps that is not so surprising because existing home sales are still quite low, down in October -5.1% from the same month a year ago.

Wall Street is up today, a bit of a bounce-back from yesterday's sharp fall. The S&P500 is up +1% in early afternoon trade. Whether this is a genuine turn up will depend a lot of holiday season retail results. That equity rise comes after Shanghai managed to close even yesterday.

Closing even is a good result for China. But investment funds are struggling with the previous writedowns in equity valuations. Private funds have had a hard time attracting money this year as China’s financial markets wrestle with a bear market in stocks, tough new asset management rules, and a national campaign to reduce debt. These funds are seeing net outflows.

In the EU, Brussels has pushed back hard against Italy's plan to ignore its debt level commitments. It notes at 131.2% of GDP in 2017, the equivalent of €37,000 per capita, Italy's public debt exceeds the 60% of GDP reference value it committed as part of the EU, and it doesn't want to see Italy go further into a hole it will never get out of.

The OECD has revised down its growth forecasts worldwide. For New Zealand they say economic growth is projected to edge down to 2.6% by 2020, mainly reflecting slowing private consumption as the boost from increased financial support for families passes, net immigration diminishes and housing wealth gains subside.

In Australia, there is a lot of silly posturing going on at the Hayne Royal Commission, some of it by the Commission itself. But one positive thing may come of it all - removing the inherent conflicts from mortgage broking. It looks increasingly likely that mortgage brokers will need to charge their clients directly for their services rather than taking 'commissions' from banks. Brokers claim customers value their services, but the evidence is that they are fundamentally conflicted. Hayne may force a restructuring to do the right thing. Whether this reform ever arrives in New Zealand is uncertain; the regulator here has shown little interest in addressing the inherent conflict of interest by mortgage brokers.

The UST 10yr yield is starting today higher at 3.07%. However their 2-10 curve is still lower at +25 bps. The Aussie Govt 10yr is at 2.70% and unchanged, the China Govt 10yr is at 3.40%, up +1 bp, while the NZ Govt 10 yr is at 2.74% and unchanged.

Gold is up +US$4 to US$1,226/oz.

US oil prices have bounced back up today, recovering a good part of yesterday's big drop. But today they are still at only US$55/bbl. The Brent benchmark is now just over US$64/bbl.

However, the Kiwi dollar is starting today marginally firmer at 68.3 USc. On the cross rates we are unchanged at 94.1 AUc, and at 60 euro cents. That puts the TWI-5 at 72.8.

Bitcoin is lower again today, now at US$4,394 and -2.6% lower than this time yesterday. At one point in the past 24 hours it dropped to US$4,164. This rate is charted in the exchange rate set below.

This chart is animated here.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

48 Comments

A sprinkle of nuts on my silage. Thankfully Squirrel's mortgage brokers do not receive commission.

Couldn't even catch a bid at 45% under RV...

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12…

22.000 corporations. They all startout looking like hockey sticks, they all bend over and they all die.

A 2011 talk. https://www.ted.com/talks/geoffrey_west_the_surprising_math_of_cities_a…

I have seen the effect called the Sigmoid Curve when applied to business but really it is the Seneca Effect. The whole world is slowing down because that is the way it works. It is more biology and physics than maths, but this guy has worked the maths.

You won't see a return to growth, you will see a continued slowing as we hit the peak of the curve, then a slow decline, and eventually a rapid decline. The slowing started in 1961, your guess as to where the peak is.

The question is how much slowing can the financial system take?

I would put the peak at 2008ish.

Although the world recovered from the GFC the means in which it was achieved was like addressing cancer with a band aid.

The borrowed time is coming to a close, and to me so is capitalism.

The patient is concious.. hang on, i'll give him another shot of adrenaline. See, now he's awake again...

Cities are just a symptom. Too many people is the cause.

indeed

https://www.youtube.com/watch?v=PUwmA3Q0_OE

fast forward to 4min and those 1million pop increases start to look somewhat like a virus

Nice link. I don't think it points to a system-wide crash though. I bet there are companies starting right now that you have never heard of, that one day will be bigger than Google.

The point is that it won't be a huge crash. It is a fast taper to start with, then the taper slows. That is followed by a slow taper off that will increase to a very rapid taper. The underlying mathematics is exponential growth, which I don't think you understand is the cause. Sure you might have another google. What you won't get is a 22,000 corporations of a similar size as there isn't the resources left to do it. If you read up on the Sigmoid curve you will find the time to do something about the slowing of growth is at the inflection point when it occurs, not after the peak. We are already too late, 55 years too late.

We are still in the slow taper before the peak. The solution to the problem so far has been to print money, which has to finds its way into a an economy where little growth is occurring. That just causes asset price inflation. The next step, when we move from low growth to zero growth is you have to sell your assets to pay live.

When you say ‘there isn’t the resources’ are you considering that your current view of resources is constrained to one planet. Even in the solar system there are orders of magnitude more resources and of course just shear space to be exploited. I’m not saying our growth model doesn’t have issues but there is a lot we haven’t exploited yet.

What's the EROEI for mining in space and shipping back to earth?

Huge.. A small nudge to get the product moving in the right direction, wait and let gravity do its thing. Or use solar sails to move the product from the inner system outwards. Lots of opportunities, but we just aren't there technologically yet. And probably won't be in my lifetime.

Hardly is probably too optimistic about the rate of our progress, but PDK and scarfie etc are too pessimistic. As a species we adapt and invent rather quickly when the need arises.

Human innovation and behaviour put us on the Seneca Curve. That is simply statistcs, or observation of the status quo. What about human nature gives you cause to believe we will behave differently and deviate from the curve?

I don't accept your foregone conclusion we are on the Seneca curve. Lots of other curves, like the good old S curve. And then we innovate, and a new S curve begins.

https://i0.wp.com/robotwatch.co/wp-content/uploads/2016/08/s-curve.jpg

{kind=link}

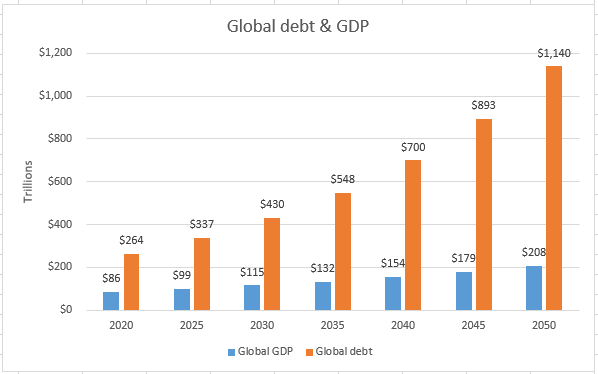

Then explain why global GDP is on a long trend downwards and how each injection of debt gives a lower boost than the last.

https://www.statista.com/statistics/268750/global-gross-domestic-produc…

Downwards huh?

You two are the ones making the claim we are on a Seneca Curve, you provide the evidence of your claim.

it certainly is growing ... (i think you forgot to show the growth in aggregate debt )

https://static.seekingalpha.com/uploads/2017/4/5/791977-149140892604258…

https://seekingalpha.com/article/4061686-global-debt-set-reach-1140-tri…

"Global debt measured in US dollars has been growing at a rate of 5% per year, while global nominal economic growth has been expanding at 3% since 2007.

{kind=link}

I was responding to some pie in the sky claim that global GDP was falling. Obviously it wasn't.

fair enough

GDP isn't a measure worth taking any note of. Look to energy consumption or population growth. Hard figures, not man made ones. A rise in GDP is possible on just the price side and in the face of production declines with money printing.

To get heavy mining equipment into space is a lot of rocket launches - to escape earth's gravity, the maximum payload achieved to date is 6 tonnes. Also the energy to escape the gravity of the mined planet is many magnitudes greater than sailing it through space.

Space travel is just too expoensive. There is a reason why no-one has been to the moon in 46 years.

Also note that the fastest ever plane was in 1976 and has not been surpassed. Commercial plane speed records were set in 1968 and have not been surpassed.

Innovation is no longer econimical in these spaces/

How bout fuel burn per passenger/payload ton mile 1976 vs today? Going faster in the atmosphere was too expensive, so instead they went further for cheaper, and safer, and more reliable. Its still progress.

Concorde used 14L/100km per passenger - about the same as an SUV on an Auckland commute

Couldn't come up with a sane argument so you'll go off on a wild tangent?

...And a 787 gets about 2.5L/100km

I think you proved pragmatist's point..

I have a background in aviation and my sources tell me that there has been a cost in reliability for that extra economy. They pushed the limits of materials and are paying the price.

Sorting out the teething issues with a new generation of engines. Nothing unusual. But you can't deny that engines.. piston, turbine, electric are all getting more reliable, more efficient and longer lasting in general as engineering gets better. Better materials, tighter tolerances, better design from better instrumentation and building off a bigger knowledge base.

Well I just reported to you that they have become unlreaiiable. https://www.theguardian.com/business/2018/jun/11/rolls-royce-engine-pro…

As a person that has traditionally fixed his own car I can also report that the reliability of engines is past its peak. Some thing, the drive for efficiency has seen engines become less reliable and more expensive to fix. Common rail diesel causes issues with expensive replacement of the injectors likely at couple of hundred K.

The bastion of reliability, Toyota, have lost that in their engines since about 2005. I think that is pretty much the case across all makes.

A conversation with an autosparky recently while I was doing research for someone else looking at buying a european car. The sparky said that cars out of Europe are only designed to last 5 years and then be recycle, hence the electrical systems are junk. Even Japan are only designing for 10 years now. Sorry you are wrong, reliability did increase but the peak was about 1990-2005. The Japs had the tolerances pretty good by the 1970's, advances since there were in fuel systems.

Yes, a new generation engine with teething issues as I specifically mentioned above. Its nothing new, it happens with every new generation of technology, and then they engineer a change or two and things get fixed. Applies to car engines, transmissions, electronic devices.. first generation CVT gearboxes were complete rubbish, and expensive to fix, newer ones are better engineered and reliable as hell.

Doesn't change the fact that a 1970s car was very unlikely to make it 15 years, & 200,000 kms without serious issues, and now your average japanese used car with the very barest of maintenance does it regularly, I'm wondering if I can get mine to 300,000kms. just ticked over 200k, time for its third set of spark plugs. Chances are the body will start falling to bits before the engine does. Not to mention it makes double the power, of the equivalent 70's motor, and is better on gas when not being abused.

"And more expensive to fix" Yeah, thats called inflation, $20 of copper spark plugs every 5,000kms might seem cheap (and were probably only $3 back in the 80s), and $130 of spark plugs every 80,000km feels worse at the time, but is actually cheaper in the long run.

And your assertion that advances are in fuel systems.. what a load of rubbish. Pretty much every car in production now has variable valve timing, variable lift, electronic throttle. And thats just the engine, body systems are miles ahead too.

You can assert your opinion as much as you want, but it simply doesn't match reality. Reality is the trend if for better performing, more reliable, and cheaper (once you adjust for inflation).

Mining planets? Are you nuts. The asteroid belt, comets etc. Bugger trying to lift crap out of a gravity well.

The basics will be built on the moon, the heavy stuff in space, within an asteroid belt. The only stuff shipped off this planet will be the little bits needed to get started.

Are you also building spacecraft to transfer materials back to earth while in space?

In Australia, there is a lot of silly posturing going on at the Hayne Royal Commission, some of it by the Commission itself. But one positive thing may come of it all - removing the inherent conflicts from mortgage broking.

David, your tone towards the banking Royal Commission appears to be that it is a bank beat up, or in this case posturing. Have you looked in detail at the issues being covered and the conduct of not only the Australian banks, but their regulators? The issues go to the core of the Australasian banking system and the massive tightening of credit since the commission started is an obvious outcome.

Perhaps the commission has been posturing this week. I agree that the questions to Catherine Livingstone about CBA board minutes looked more like posturing or a warning shot more than anything else. But the underlying issues are very much real and problematic.

Yep, not like the brokers could do it all, or do any of it without the banks.

synchronised debt

https://www.youtube.com/watch?time_continue=117&v=9kiU305_Smg

That was it...the relief rally?! Dow flat before the holiday doesn't look good to me.

Drill Short baby, drill short.

Global financial markets fear the junk tsunami

https://www.welt.de/wirtschaft/article184164968/Anleihen-Es-wird-chaoti…

Quite relevant to my post and link above. Companies will move to junk uninvestible status in ever increasing numbers. Slow at first, then it accelerates.

Fletcher Building? Down 25% in the last 10 days, and no sign of it stopping.

By writing about this I may have answered my own question further up the thread, what outcome for finance.

The slowing of growth is going to be inversely proportioned by the rate of companies going junk status. Just testing the idea.

Scarfie, what do you think of this?

http://professorfekete.com/articles/AEFHowFedBankruptedInsInd.pdf

I always like Fekete, he makes complete sense. The way I was already aware of what he says is in the cost of borrowing to do business. If you borrow at 5% and five years later a competitor comes in with borrowing costs of 2 1/2% they automatically have an advantage. The existing capital has become compromised, or less efficient as he would say. Note he believes like I do that interest rates must come down. I think where I might diverge from his thinking is that a gold standard is any better. I think with a gold standard it just happens more slowly.

To investigate, we test the received belief that lower interest rates result in higher growth and higher rates result in lower growth. Examining the relationship between 3-month and 10-year benchmark rates and nominal GDP growth over half a century in four of the five largest economies we find that interest rates follow GDP growth and are consistently positively correlated with growth. If policy-makers really aimed at setting rates consistent with a recovery, they would need to raise them. We conclude that conventional monetary policy as operated by central banks for the past half-century is fundamentally flawed. Policy-makers had better focus on the quantity variables that cause growth.

https://www.sciencedirect.com/science/article/pii/S0921800916307510

"Delusions are often viewed as reflecting some deficiency in reasoning ability. The risk of thinking about delusions in this way is that it encourages the belief that logical, intelligent people are incapable of delusion. An examination of the history of financial markets suggests a different view. Specifically, faced with unusual or extraordinary price advances, there is a natural tendency (particularly in the presence of crowds, feedback loops, and potential rewards) to look for explanations. The problem isn’t that logic or reason has failed, but that the inputs have been distorted, and in the attempt to justify the advance amid the speculative excitement, careful data-gathering is replaced by a tendency to confuse temporary factors for fundamental underpinnings."

"What has been most extraordinary about extraordinary monetary policy is the

awkward denial of uncertainty in defense of extraordinary actions. Wanting so

badly to manipulate our expectations, the central bankers did not want to leave us

any room for doubt.

As I said at the outset, the Fed and other central banks appear to have avoided being

candid about the uncertainty in order to maintain their credibility. But this is

backwards. They cannot regain their credibility unless they are candid about the

uncertainty and how they confront it. "

http://www.grantspub.com/files/presentations/FISHERGRANTSREMARKS15MAR17…

5 times average daily volume through Fletchers today and it’s closing on its lows.

Yes, for every seller there is a buyer, but if those buyers get nervous and see a better re-entry point lower down, and regurgitate what they’ve just picked up, it could get unruly.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.