This week’s Top 5 comes from Terry Baucher, director of tax advisory business Baucher Consulting.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz.

And if you're interested in contributing the occasional Top 5 yourself, contact gareth.vaughan@interest.co.nz.

1) Top five most important tax-reforming finance ministers.

The role of a finance minister is hugely important as they together with their Treasury department set the direction for an economy. Tax is a major part of any finance minister’s responsibilities, but for some finance ministers tax reforms are the key part of their legacy. Here are five finance ministers with a huge tax legacy.

Jean-Baptiste Colbert was the finance minister (Comptroller-General of Finances) for King Louis XIV of France between 1661 and 1683. His quip "the art of taxation consists in so plucking the goose as to obtain the largest number of feathers with the least possible amount of hissing" remains as true today as it was in the seventeenth century.

The entrenched interests of the French nobility prevented Colbert’s attempts to raise taxation to fund Louis XIV’s wars. He could not raise direct taxation on the French nobility, but he increased indirect taxation from which they were not exempt – an early example of broadening the tax base.

Henry Addington succeeded William Pitt the Younger as British Prime Minister and Chancellor of the Exchequer in 1801. Pitt introduced the first income tax in 1798 to help fund the Napoleonic Wars, but Addington repealed it in 1802 following the Peace of Amiens.

Addington’s repeal was short-lived because war broke out again in 1803 and the tax was re-imposed. Addington’s income tax is significant for two reasons: firstly, it introduced withholding at source with the equivalent of a resident withholding tax on interest paid by the Bank of England. Secondly, it adopted a schedular system splitting classes of income into separate “schedules” which remains the case in Britain today. Addington’s income tax was more broadly based than Pitt’s - doubling the number of taxpayers with the result that although the original maximum rate at 5%(!) was half that of Pitt’s income tax, the tax take more than doubled.

Income tax was abolished after the Battle of Waterloo and all records were destroyed to protect privacy a measure rather foiled since duplicates had already been sent to The King’s Remembrancer (yes, really).

Sir Geoffrey Howe was Margaret Thatcher’s first Chancellor of the Exchequer. He was the first finance minister of modern times to start the trend of reducing very high income tax rates in favour of higher taxes on consumption. In his first Budget in 1979 he lowered the top rate of income tax from 83% to 60%, whilst raising the standard rate of Value Added Tax (GST) from 8% to 15%.

Howe did not have a reputation as a sparkling wit. His Labour predecessor Denis Healey, famously quipped that debating Howe was “like being savaged by a dead sheep.” However, it was Howe’s devastating resignation speech in 1990, after falling out with Thatcher over her approach to Europe, that precipitated the revolt that ousted her.

Don Regan was President Ronald Reagan’s first Treasury Secretary, the American equivalent of a finance minister. Regan was a supporter of Arthur Laffer’s supply-side economic theory. He tested the hypothesis by introducing the Economic Recovery Tax Act in 1981 which cut taxes by 2.89% of GDP (and the top rate of income tax from 70% to 50%). These are still the largest tax cuts in American history. (It appears however they were too big, as tax increases were required almost immediately to bring the budget deficit under control).

Regan later laid the groundwork for the Tax Reform Act of 1986 which further reduced the top income tax rate to 33%, but also broadened the tax base by eliminating deductions and tax shelters (sound familiar?). The enduring legacy of Regan’s support of Laffer’s then revolutionary supply-side theory is that it is now a key plank of current Republican Party thinking on tax.

Sir Roger Douglas. In the New Zealand context, it is impossible to look past Douglas as the finance minister with the biggest tax legacy. In fact, he is probably the most important tax reformer anywhere over the past forty years. That’s because unlike Howe and Regan (and for that matter Paul Keating in Australia), he, together with his Revenue Minister Trevor de Cleene, achieved far more comprehensive reforms in a staggeringly short period of time. Within four years the New Zealand tax system was overhauled, the top income tax rate halved from 66% to 33% and introduced the world’s most comprehensive GST. Douglas’ overall legacy remains controversial but the fact the basic structure of New Zealand’s tax system has remained largely unchanged since his reforms is a clear measure of his standing.

2) Arthur Laffer.

This week President Donald Trump presented economist Arthur Laffer with the Presidential Medal of Freedom, America’s highest civilian award.

In the 1970s Laffer developed the theory that lowering taxes would boost economic activity - the Laffer Curve. He famously outlined his theory, complete with curve, on a napkin during a lunch with Don Rumsfeld and Dick Cheney in 1974 when they were part of President Gerald Ford’s administration.

Laffer’s theory is not unreasonable. The controversy around it is that proponents believe deep cuts in tax effectively become self-funding because of the resulting economic expansion and investment boom. The evidence for this is less clear-cut: America experienced significant budget deficits after 1981, which eventually required tax increases under Presidents Bill Clinton and George Bush Senior to close. More recently Kansas had to reverse ambitious tax cuts introduced in 2012.

In a New Zealand context, the Tax Working Group’s interim report in September 2018 noted;

“The two most recent reductions in the company rate in New Zealand – in 2008 and 2011 – were not associated with an increase in foreign investment. In fact, the stock of foreign direct investment as a percentage of GDP trended down slightly in the following years. There was also no increase in the level of foreign investment relative to Australia, whose company rate was unchanged during that period."

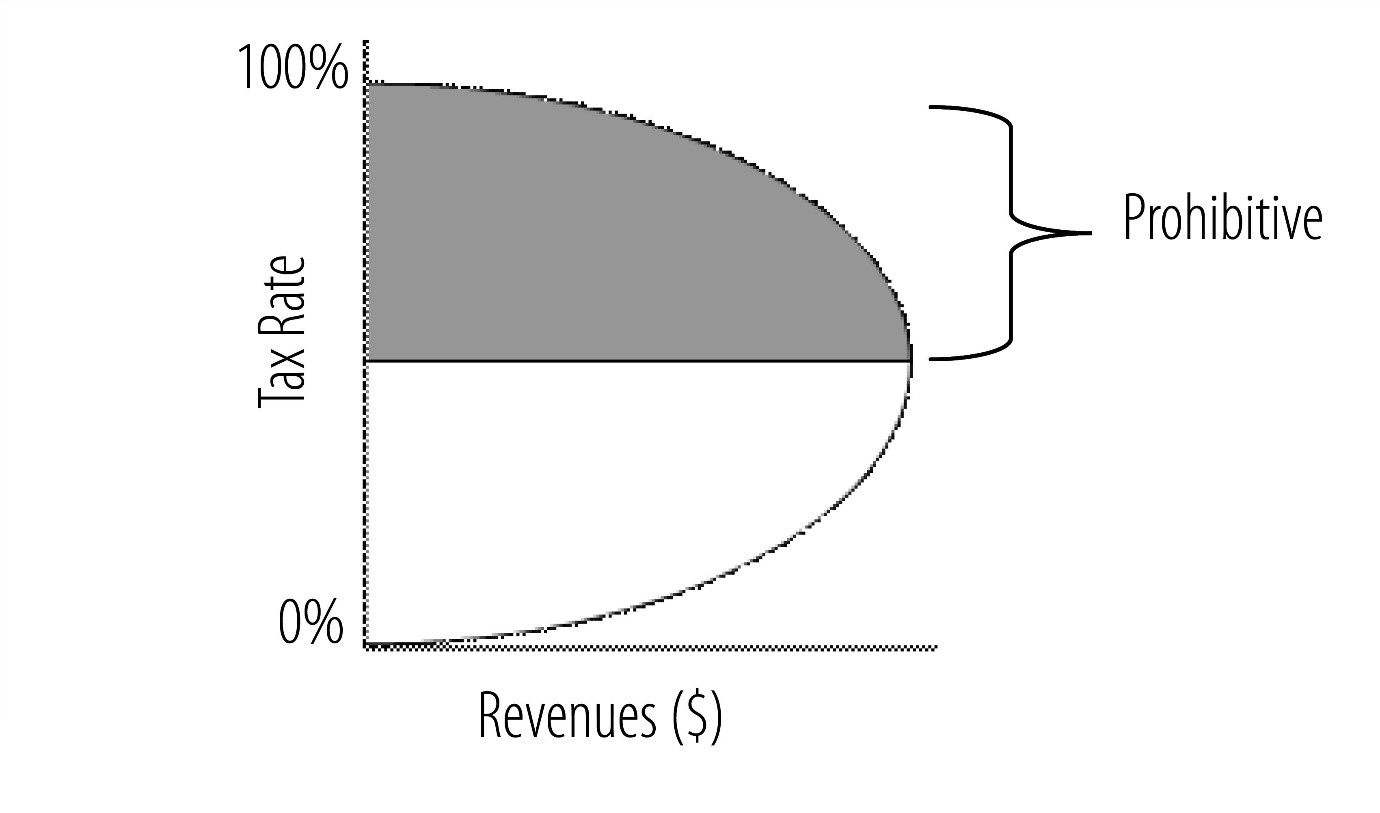

If the jury remains out on the effectiveness of the Laffer Curve and supply-side economics, the influence of Arthur Laffer should not be understated.

The ACT Party’s recent flat tax proposals are built on Laffer’s theory. However, they don’t appear to address the most overtaxed group – those receiving some form of social assistance. As this paper prepared in February by the Productivity Commission notes, the interaction of tax and abatement rates mean that many people face effective marginal tax rates way in excess of 33% - in some cases as much as 101.4%! Major reform here could provide more proof of Laffer’s theory.

3 “They haven’t gone away, you know.”

Rather like Gerry Adams’ grim retort about the Provisional IRA, the same is true about the various demographic and environmental issues outlined by the Tax Working Group (TWG). Capital Gains Tax might be dead, but those issues and the pressures they entail remain.

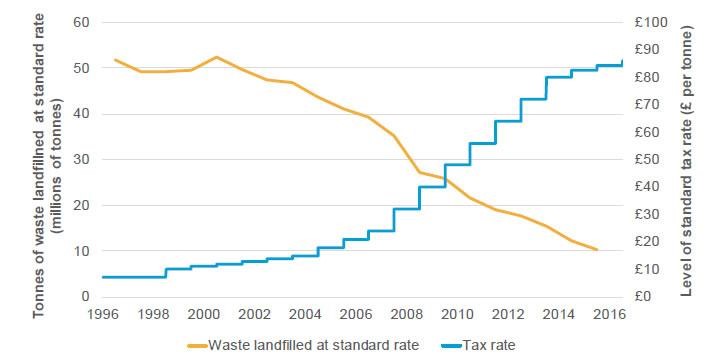

One of the environmental taxes the TWG suggested was increasing the Waste Disposal Levy from its current level of $10 per tonne. This wasn’t so much as a long-term revenue raiser but as a means of changing behaviour and reducing waste.

As the graph below illustrates this is what the United Kingdom has achieved with quite dramatic effects. As the tax rate increased, the level of waste dumped in landfills fell. (This, incidentally, is an example of the theory behind the Laffer Curve in action). The TWG heard one estimate that a similar approach here could lift the annual amount of Waste Disposal Levy collected from $30 million to perhaps $200 million.

For the demographic reasons I recently expounded, expect to see environmental taxes make up more of the tax base in future years.

4) Digital Services Taxation.

The Government recently released a discussion document on its options for taxing the digital economy and the tech giants.

The TWG suggested the Government should be ready to implement a digital services tax (DST) if other countries such as Australia move in that direction. In fact, Australia has backed away from a DST although the UK has announced a 2% DST to take effect from April 2020. Austria, the Czech Republic, France, Italy and Spain are all looking to introduce DSTs either later this year or in 2020.

India, however, has gone beyond threats and actually implemented a number of measures which tax the digital economy. In 2016 it introduced an ‘Equalisation Levy’ of 6% on the value of digital services charged by a non-resident entity. In the year ended 31st March 2018 this levy raised more than 5.5 billion rupees or about $121 million.

India’s action doesn’t seem to have slowed the supply of digital services there and it will be interesting to see whether the various European countries proceed with implementing their own DSTs over the next year or so.

5) Gone to pot?

We will have a referendum on the decriminalisation of marijuana next year. What could that be worth in additional tax revenue? One estimate prepared for the Drug Foundation suggested the annual tax revenue could be perhaps $240 million.

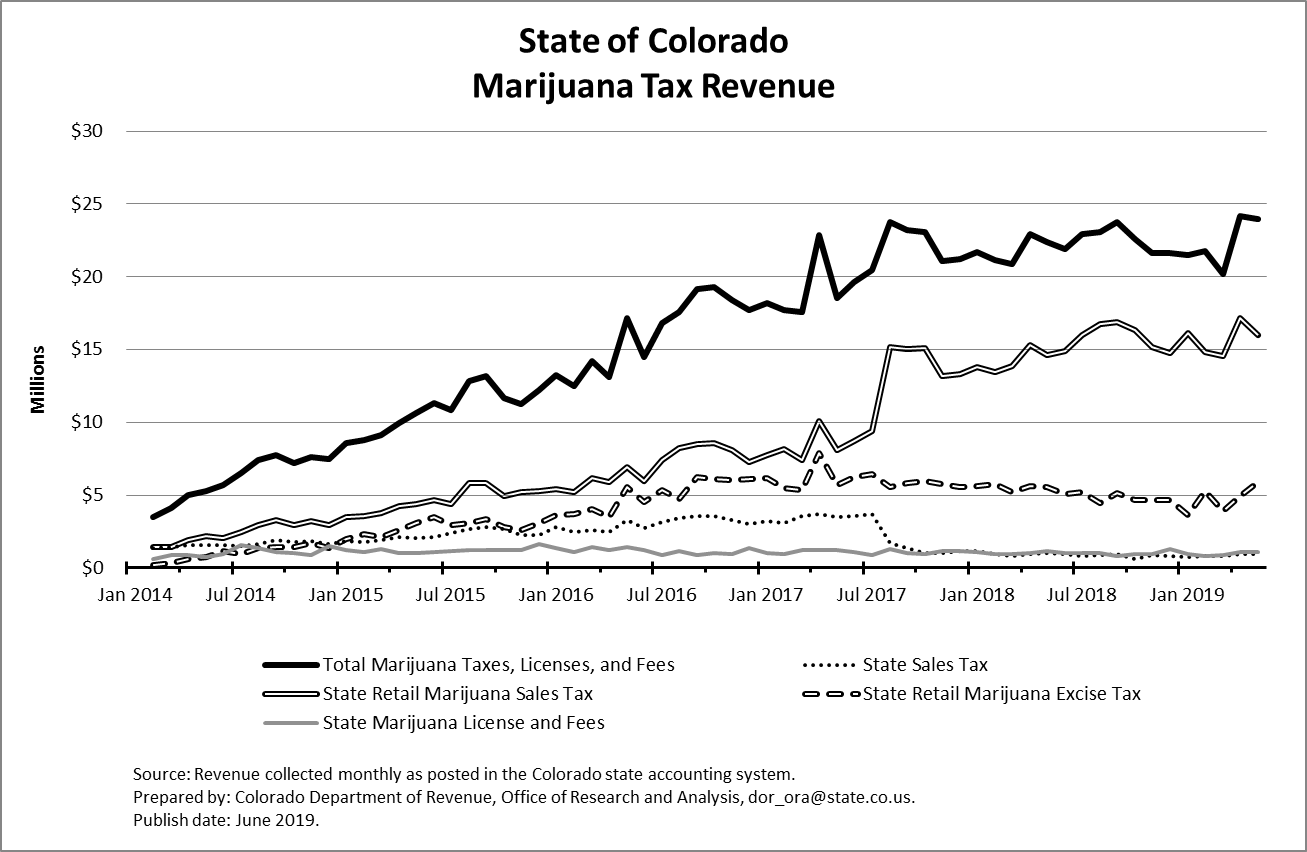

That doesn’t sound unrealistic based on Colorado’s example. The US state with a similar sized population (approximately 5.6 million) legalised cannabis from the start of January 2014. The total marijuana tax revenue the state has collected since then has just crossed the billion-US-dollar mark.

As the latest official statistics show, Colorado has seen steady increases in its marijuana tax take since January 2014. In the fiscal year ended 30th June 2018 marijuana tax revenue was US$266 million, about 1.7% of the state’s tax revenues from all sources.

Opponents of decriminalisation cite mental health risks as one reason against. Those risks are real particularly for the young, but they exist now even though the drug is illegal. An extra $240 million a year in tax revenue could go a long way in dealing with the potential fallout.

6 Comments

Common theme - the absolute inability of Politicians to live within a budget (tax take)

.. another common theme amongst politicians is their 100 % failure to tax capital effectively and efficiently ... thereby skewering the tax take against workers and business , the productive engine of the economy .

Meanwhiles .... speculators and rich land owners get a free ride ..

We need a land tax .... and water , and air ... tax those who own , use or abuse our natural resources ... please !

Yep, owners and the bankers get the benefit of this current paradigm, hence politicians walking into banking jobs after their tenure. Productive enterprise comes last and we wonder why productivity isn't improving.

Still pushing outright theft I see.

Such taxes would hammer asset values as well as impoverish many folk, especially older ones with little cash flow, a double whammy disaster for them after a lifetime of hard work and saving. Politicians are smarter than they appear.

The perfect tax is the one that encourages & rewards endeavour & creativity, whilst gathering enough to provide those essential services needed to run a functional civilisation. Of course, almost every word I've written could be debated until the cows come home, which is both the problem & the opportunity.

The Laffer Curve is just one of many economic theories that should be consigned to the dustbin of history. in evidence,I would cite the following books;

Misbehaving-The Growth of Behavioural Economics by Richard Thaler.

Doughnut Economics by Kate Raworth.

Econned by Yves Smith.

Licence To Be Bad-How Economics Corrupted Us by Jonathan Aldred.

It may seem cruel to say so,but perhaps the world be be in better shape had an avalanche hit Mont Pelerin on a particular day in 1947. We would not have felt the malign and pervasive influence of Hayek, Friedman and others.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.