• House prices rise when not enough houses are available to meet resident and non-resident demand, and when low interest rates and income growth allow people to bid up prices.

• Recent price declines in Australia have led some to suggest Auckland will follow. But Australia has over-built relative to its population growth over the last decade, as it over-developed for a foreign investor market that is now weaker.

• Auckland has not, which has implications for the relative outlook for the region’s largest cities.

• With Auckland’s economic outlook, prices will likely remain flattish, with limited macroprudential risk, and slow gains in affordability.

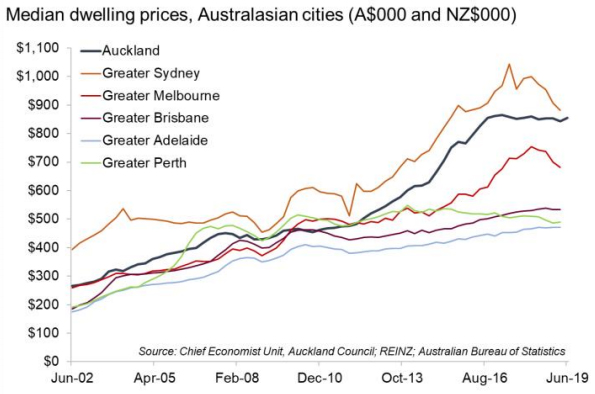

Auckland’s flat house prices

The Auckland Unitary Plan, aided by tighter exchange controls in China and loan-to-value restrictions on investors in New Zealand, reduced land prices by about 6% in Auckland over the two years to 2018. The Unitary Plan was introduced on 15 November 2016, enabling four times the city’s previous housing capacity. The impact of this surge in development potential was immediate and irrefutable, although limited. Auckland house prices fell about 4.5% from their peak in October 2016, to their nadir in February 2017, staying flat since then.

In March 2019, the threat of a capital gains tax took Auckland prices down another (small) step. But with capital gains now off the table, we’ve seen a small resurgence in house prices in this city.

Boom. Splat.

Melbourne and Sydney, meanwhile, saw house prices peak between June 2017 and March 2018. Since then, prices have fallen 15% and 10% respectively. Perth prices have fallen 11% since the end of the mining boom. Brisbane prices have recently flattened out, while Adelaide prices have risen most modestly and uniformly.

The Sydney and Melbourne stories have prompted all sorts of prognostications on whether Auckland house prices will follow, often with little empirical evidence to support the view.

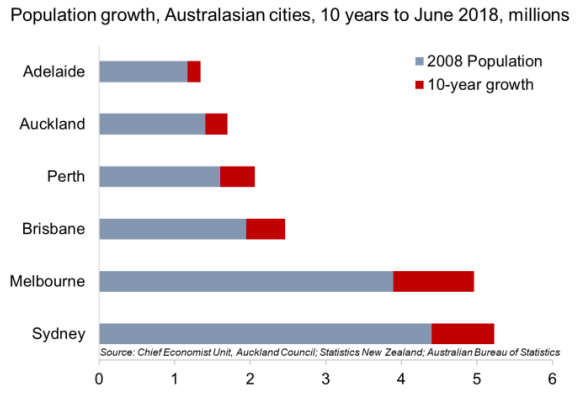

Mixed population growth across cities

While local and international sentiment undoubtedly plays a role in house prices, these Australian cities have overbuilt relative to population growth when compared to Auckland, meaning they just don’t have the housing shortfall Auckland does. This puts them at far greater risk of the kind of price falls they are currently experiencing.

Since 2008, Auckland has grown by 290,000 people, or two Taurangas. Adelaide has grown more slowly in absolute and percentage terms. Brisbane has grown almost twice as much, Sydney by almost three times as much, and Melbourne more than three times as much. In percentage terms, Perth has grown fastest, even though it is now growing more slowly on the back of a weaker mining sector.

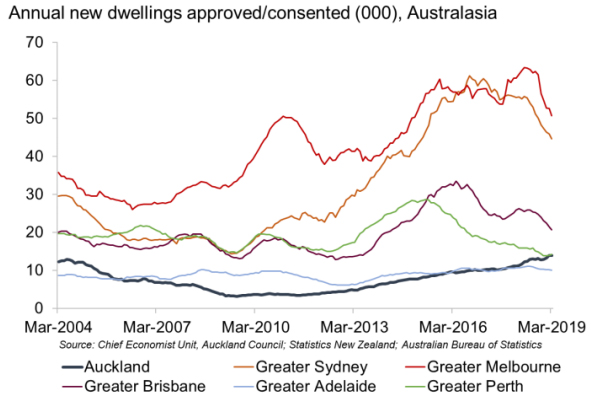

Australia has massively out-built Auckland

So have these major cities responded to this growth by delivering more housing?

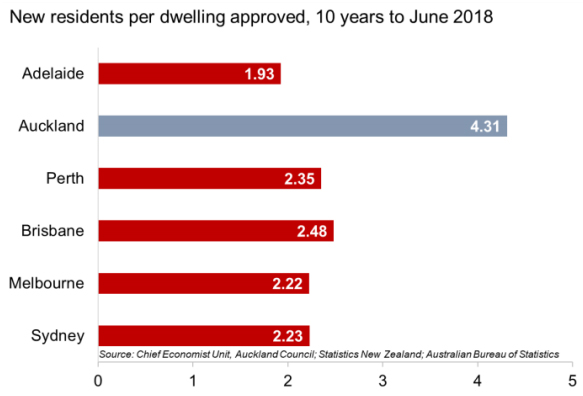

Dwellings approved don’t perfectly reflect what was built and when, but they are a good proxy. Over the 10 years to June 2018, Auckland consented 67,400 new dwellings. Adelaide, with its weaker population growth, consented 90,100. Melbourne consented 482,000, seven times Auckland’s figure.

A couple of Auckland caveats are worth mentioning. First, this lacklustre growth is stunted by the first three years of the decade of analysis, which saw almost no building activity in Auckland; annual dwellings consented in June 2018 were up 260% on the average between June 2008 and 2011. Second, annual new dwellings consented in Auckland have risen a further 12% since June 2018, while falling across Australian cities.

But the percentage decline in Australian cities through the GFC was less severe than in Auckland (where approvals fell 60%). All Australian cities saw a much faster bounce-back in building activity than Auckland, which lagged through to 2011.

How appropriate are these levels of building?

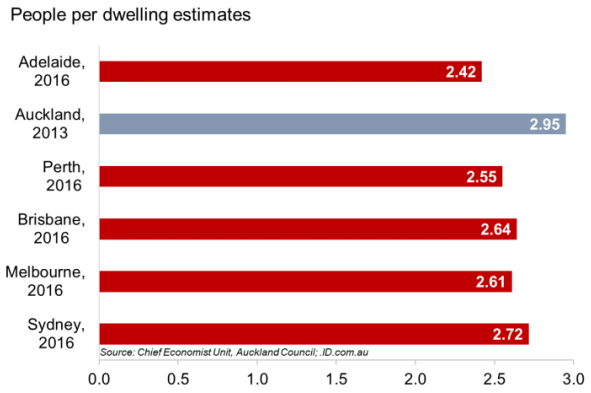

World-wide, the trend is toward smaller numbers of people per dwelling as demographics change. This means even if your population growth is stagnant, you’d need to add to your housing stock slowly. But population growth matters more than population size as the primary driver of demand for more housing in rapidly-growing cities.

As of the mid 2010s, all six cities had an average number of people per dwelling between 2.4 and 3.0. Auckland already had the highest figure after a period of weak building activity and with its population beginning to surge.

Yet the difference in rates at which housing was consented across cities, relative to actual new residents, is astounding (see figures overleaf). Auckland’s 4.31 new residents per dwelling is far higher than the ratio for the existing population. Meanwhile in Australia, all five cities have built faster than the ratio for their existing populations, meeting the needs of growth and then some.

This suggests (and nervousness at some Australian banks with regard to funding apartments bears this out) that Australia has overbuilt on the back of demand to park foreign money in newbuild properties there.

With that demand weakening, there is now an oversupply of housing, and some of it catering for a very specific segment of the market.

Adelaide is an exception probably worth looking at in more detail in future. It has fewer people per dwelling (an older population) but has built at the fastest rate relative to population growth. It has a housing mix more skewed toward stand-alone homes than Sydney and Melbourne, and greater stability in the number of dwellings consented and house price growth over the last 10 years.

So what?

Supply and demand’s axiomatic relationship sets the price of products and services. So in looking at what’s likely to happen to prices, what we’re really asking is: What has happened to things affecting demand and supply?

Here’s what we know. First, the demand side, or who is willing and able to buy houses:

• Auckland’s population continues to grow rapidly as net migration remains near record levels.

• The effect of foreign buyers being removed from the existing home market is baked into prices.

• Unemployment remains exceptionally low, and household incomes are rising.

• Interest rates are at record lows, and if anything, are likely to fall further making it possible to service more debt.

• The threat of a capital gains tax is gone indefinitely. This is music to the investor’s ears.

• That said, median house prices of $850,000 remain exceptionally high; saving for the deposit is a significant damper on demand.

And on the housing supply side:

• We haven’t built enough houses relative to our recent growth or our trans-Tasman neighbours.

• The Unitary Plan has stimulated a major boom in new dwellings being consented, so the gap is unlikely to be widening much now, but we do have a shortfall of at least 46,000 dwellings we’re a long way from eliminating.

This balance plus Auckland’s steady economic outlook mean a melt-down in the housing market here without a sharp rise in unemployment and/or interest rates is unlikely. While inside the realm of possibility, these eventualities are outside the realm of probability over the medium term.

Instead, prices are likely to bob around current levels, which is good news for macroprudential stability. Affordability is slowly improving (the best it’s been in five years), which is good news for first home buyers although prices remain high. But those who have bought for capital gains in the last three years will be least happy with the outlook.

*David Norman is chief economist at the Auckland Council. This article was first published here.

65 Comments

"With Auckland’s economic outlook, prices will likely remain flattish". Agreed, but only for two or three more years, when upward phase is due. This is a good evidence-based analysis. The next couple of years present a good opportunity to get a good deal while the market is flat, but sadly many will be put off by fear mongering and talk of catching falling knives.

Speaking of "little empirical evidence to support a view"...

Is the evidence-based analysis of supply and demand factors in this article not good enough for you?

Speaking of evidence, here's that link that you lacked the initiative or competence to find for yourself yesterday - https://croakingcassandra.files.wordpress.com/2017/11/credit.png?w=700

{kind=link}

Irish private debt approaching 400% GDP prior to crash. NZ not far over 150% now.

Due Diligence could you please support your Irish private debt numbers with a reference ?

Gladly - https://tradingeconomics.com/ireland/private-debt-to-gdp

Best case scenario 350%, depending on when you think the crash started.

What? Prices peaked in early 2007. At that point private debt was at 250%.

And why do you keep linking private debt. It very relevant to the overall economy, but less relevant to the housing market where prices are largely tied to household debt.

I'd agree that the levels of debt of property industry (shown in total private debt) made the risks to their wider economy greater. But household debt is a much better measure for property prices.

And government debt to GDP was around 21-23%.

Household debt to GDP went over 80% in 2007.

I keep linking private debt because, like you've just stated, it is very relevant to the overall economy, which is very relevant to the housing market. Even if you insist on taking it at an earlier date (250%), that is still significantly higher that what NZ is at now. Nowhere have I said that household debt is irrelevant. My point is merely that private debt is very relevant, and a differentiating factor between Ireland's back then and NZ's today. Ireland's reached 425% at one point, which I believe had an impact on its economy.

In your opinion, which of the two numbers has the higher importance and significance?

1) private debt to GDP or

2) household debt to GDP?

Depending on which metric is considered of higher importance and the more significant factor, then one might come to a totally different conclusion about the level of risk of house prices falling substantially.

I don't think either is more important. They are both relevant factors and I'm not going to disregard either. On the other hand, people hoping for an NZ recession and collapse in house prices choose to acknowledge one and disregard the other because they have an aversion to facts that point to NZ being different to pre-crash Ireland, or Sydney for that matter.

No, you are being disingenuous. You keep quoting 400% private debt even though those levels occurred almost a decade after the bubble burst. How is that even remotely relevant? Debt to GDP rose immediately AFTER the bubble burst as the economy was contracting, not because people were taking on more debt.

Households are holding almost identical levels of debt suggesting both markets are in similarly precarious positions. I'd agree that when NZ's housing bubble pops we won't suffer anything as severe as Ireland did (with peak to trough falls in real terms of 56%), nor public bailout of banks (unless its a global meltdown) resulting in government debt rising to 120% of GDP. But it doesn't mean there won't be a significant correction.

How is private debt (which includes household debt) even remotely relevant? Because when interest rates rise, high private debt leads to significant pressure on businesses. This debt stress flows through to many aspects of the economy, including incomes and confidence, which puts downwards pressure on house prices. That is why it is remotely relevant, which is not to say that household debt is irrelevant or even less relevant. Private debt to GDP was high in Ireland before and after the crash regardless of what date you choose to take it from, and much higher than what NZ private debt is now. New Zealand's economy, in this very important respect, is in much better shape than Ireland's was back then and as a result is more resilient to a collapse in house prices.

Once again you seem to be talking about something you know very little about. A significant portion of that private debt is held by the multitude of multinational corporations that domicile themselves in Ireland and load up those subsidiaries with debt for tax reasons.

The fact that you keep glossing over the most relevant measure (household debt) and the similarities between both countries discredits your entire argument just as much as your misquoting of facts and figures.

Actually he is basically correct about the debt level during the crash. The property crash in Ireland wasnt in 2007, the market was falling at that time but employment was holding up until about 2009 when it fell to bits and took a moon shot. The date for the 'crash' part of the correction is actually ill defined but is generally tightly associated with the plunge in employment in 2009 and at that time private debt/gdp was in fact about 350%. Your excessive focus on household debt is also mistaken, the commercial market is crucial to banking and did huge damage to their banking sector. A housing correction alone wouldnt normally snowball in to the mess they had, it got so bad in principal because unemployment was out of control and that is more to do with widespread economic problems and so wider measures of economic malaise are appropriate to use. Ireland entered technical recession some time towards the end of 2008 and 2009 was a very dark time for them.

Stop with the misinformation. Irelands private debt to GDP measure in 2007 was at around 250%.

https://tradingeconomics.com/ireland/private-debt-to-gdp

But realistically you want to look at household debt, as its far more relevant to the housing market.

NZ household debt to GDP: (currently at 94%).

https://tradingeconomics.com/new-zealand/households-debt-to-gdp

Ireland household debt to GDP: (in 2007 it was around 90%)

https://tradingeconomics.com/ireland/households-debt-to-gdp

A large part of the private debt was held by private companies simply domiciled in Ireland for tax purposes, where operations were largely carried out off shore but where the debt was held on the company accounts. It’s the same reason that their GDP numbers today are artificial.

I worked for Tyco a few years ago, I thought it was strange for an American corporate to have the corporate head office based in Ireland.

Thankyou Miguel . I have pasted a couple of articles for Due Diligence. Written by Irish economists ( they are different to ours of course http://www.finfacts.ie/biz10/AIBhousingreportoct06.pdfcourse ) in 2006/7. and http://finfacts.ie/biz10/biz10/WealthNationReportJuly07.pdf

Seems like the spruikers are getting more desperate and more dishonest with the facts by the day

David, thanks for the article.

So here's the thing. House prices doubled in Auckland over the period 2012 to 2016. Why ? Foreign money.

Now we have the FBB / OBB prices will slowly revert to the mean. Not a fast process unless there is a macro shock but what we are seeing is significant weakness at the top end of the market. We also have a building boom of places too expensive for most people to afford. We also have a likely global recession which will impact tourist and demand for dairy and logs.

So. Stable price outlook "bobbing around current levels"? No. Falling outlook yes.

And that's before we get into taxing empty homes.

Just like the previous article that said pretty much the same thing, this one also fails to mention where the money would come from. Young Kiwis on wages cannot put together $200k deposits (unless they're living with their parents, which would significantly increase the person/dwelling rate, thus lowering the "shortage" of dwellings).

And with a national average kiwisaver balance where it is and median levels so paltry, many are 10 years away from getting that sort of deposit together. Unless 15 median kiwisaver balances all cobbled it together to get the 200K deposit together. Bunk beds in your 20's, 4 beds in 3 rooms and three lucky punters get 3 beds... Draw straws for the single bed? Ah the joys of shared home ownership, please will someone clean the bathroom?

'The median value of KiwiSaver nest eggs grew to $13,000 at June 30 last year, up 62 percent or $5,000 from three years earlier, Stats NZ says

The growth reflects employee, employer and government contributions as well as any investment gains.

“KiwiSaver is still a relatively young superannuation scheme and median values should continue to rise as the scheme matures,” the government statistician says.

Unsurprisingly, those aged 15-24 had the smallest KiwiSaver accounts and are the only age group where men’s accounts are about the same size as women’s at about $3,000. In all other age groups, men’s accounts are larger than women’s.

Those aged 55-64 have the largest holdings, although men’s accounts were larger at about $30,000 compared with those of women at about $23,000.'

Yes. So it's flawed, and overly simplistic. Like the analysis of almost all economists in this country.

Prices will continue to fall (how much, who knows, I have predicted 5-10%), before flattening, because of the lack of affordability.

This lack of affordability means effective demand (as opposed to underlying demand) is low, and this will dampen prices.

Effective demand was bolstered from 2009 onwards by repeated cuts to the OCR, and money flowing in from overseas.

The money has dried up, and the OCR can't go much lower....

I'll take a stab and suggest the only real thing keeping house price stats stable at the moment is people buying/selling in the same market where prices are largely inconsequential (house swapping).

Glitzy

I agree with you on one point - a great article.

As for foreign money - 70% of NZ banks source of money is domestic. With NZ td rates currently 3% for 5 year terms and Australia currently well under 2%, I don’t see any issue with bank funding issues.

As for a future global shock, things are not looking flash but the past decade global downturn has meant even cheaper money.

What if house prices fall some? This is not an issue - just like the KiwiSaver growth fund, one is there for the long term so short term fluctuations are not important. Prices drop 5%; get up in the morning, no difference, same house. Falling house prices is just the bogey man scaremongering.

What about foreign money in the form of the marginal buyer? ... either:

- Off-shore domiciled and sourcing funds offshore - where are they now?

- Resident sourcing funds offshore - presumably a lot harder now given Chinese capital constraints.

With interest rates on term deposits so low, money will move to higher earning investments. Just look at the price action of the NZX lately, and the dividend paying power companies in particular. I'm already seeing a lot of people on finance Facebook groups start asking about alternative investments as they see no point in remaining in cash deposits. What happens to the banks when their domestic cash starts to dry up?

more singing from the same song sheet, affordability and low wage growth not even mentioned

A great article; well supported with sound data and rationale.

I trust that this - along with the other article today on improving housing affordability - gives FHB some confidence.

I accept that there are no certainties to the future but it would appear that interest rates look to be low for the foreseeable future (term deposit rates flat at 3% for 5yr) so FHB can have some assurance that if they can manage the mortgage now, then they have little to fear especially with wage rises also likely over that period.

No doubt some DGM will respond otherwise but will be based on unsubstantiated or unrealistic reasoning.

Thursdays property article will be provided by Dominic Stephens of Westpac who will help to explain why we're not really in a credit bubble. Friday, Ashley Church will explain why house prices will double by 2016. Who will we get for Saturday? Or do we get Mr Alexander back on rotation?

We really are being spoilt this week..... cash rate cut coming in August I think.

Will any of them talk about bank lending practices and credit growth?

The very first bullet point mentions demand, supply and interest rates. Absolutely nothing about the biggest driver as you've said.

Yeahhh....

Maybe Interest could seek out any economists who do not hold the mainstream position?

Mind you, that might be hard or impossible.

I've always thought Ryan Greenaway from Auckland Uni has interesting perspectives.

By " the mainstream" I think you mean *conflicted*.

Ship in Cameron Bagrie, he's not conflicted anymore.

And David. Auckland's prices aren't flat.

Factoring in inflation, they're haemorrhaging. Add -2% on to year on year falls.

" Perth prices have fallen 11% since the end of the mining boom."

Really?!

"Perth property values nudge 20 per cent decline since peak in 2014, CoreLogic data for June reveals"

https://tinyurl.com/y69czedh

Could Auckland become more expensive than Sydney for a median priced home?

Auckland's median dwelling price is above Sydney. https://www.realestate.com.au/australian-property-market/property-repor…

Sshh Cowpat! We don’t need our 2013/2014 arrivals to know that, they could decide to use their citizenship to leave for higher wages and better value houses.

Mining is picking up again in WA.

https://www.australianmining.com.au/news/wa-mining-salaries-now-higher-…

Very sound economic theory. Unfortunately markets don't co-operate with economic theory, because markets are people - irrational, subjective, lovable, dumb, genius, outrageous, inspired, and clueless.

There are a couple of oddly unsubstantiated claims / assumptions in this article:

1. In March 2019, the threat of a capital gains tax took Auckland prices down another (small) step. But with capital gains now off the table, we’ve seen a small resurgence in house prices in this city.

What data suggests either side of this claim is true? Even the REINZ HPI is down YoY in Auckland.

2. The effect of foreign buyers being removed from the existing home market is baked into prices.

On what basis is this claim made? None is provided. Seems on the surface to contradict with the feedback of agents and articles on this site that vendors are having to be conditioned to new, lower pricing expectations. How is it "baked in" if sales are not going back to normal levels?

Similarly, regarding this quote:

"The Auckland Unitary Plan, aided by tighter exchange controls in China and loan-to-value restrictions on investors in New Zealand, reduced land prices by about 6% in Auckland over the two years to 2018."

Might the exceptionally low sales numbers occurring in Auckland be related to the fact that supply and demand are not quite meeting, and many vendors are not appreciative of what has changed?

While we're applauding sound data might we have some to support these assumptions?

Good points.

Also, he doesn't mention that the Proposed Unitary Plan probably contributed to pushing values up 2014-2016

The Chief Economist of Auckland does not draw attention to the economic failings of Auckland planning.

There are a few other facts that seem to have been casually ignored.

~ tighter HEM limits* this is massive

~ plunging car sales

~ increased bankruptcy petitions

~ huge reduction in top end Auckland sales

~ apartment complexes in CBD being cancelled

~ tourism numbers from China down

~ log prices falling on lower demand

~ contractors lowering rates as domestic work dries up

~ tax changes (fuel surcharges, removing offset for property losses)

~ AML/KYC laws making parking/moving money more difficult for illegitimate funds

All is not well in the garden. But sometimes it takes a long time for a tree to die.

The trouble with data is you see what you want in it. It just proves you are right.

Auckland with 4.31 new residents per new dwelling over last ten years.

Therefore:

a New Zealand is special

b Auckland is more desirable than any other major city in Australasia

c Auckland Council is incompetent

d The RMA is a total failure

e The RMA is working well

The data appear to support ones assumptions, which in economics usually go unidentified.

While foreign investment usually benefits developing economies and creates local economic benefits in advanced economies, it generally does not benefit advanced economies on the whole except in very limited cases. On the contrary, foreign investment in advanced economies is more likely to lead to higher unemployment or rising debt.

https://carnegieendowment.org/chinafinancialmarkets/79261

Mr Norman makes no mention of the type of housing stock nor bedrooms per dwelling. Taken from yesterdays horse's mouth

"Since 2003, 67% of dwellings built in Australia have been in multi-unit developments. The NZ proportion is just 26%. Prices for apartments have historically shown greater volatility than prices for houses."

The article is superficially good, perhaps even useful to some. OTOH, it's just another spruiking of Make Auckland Great Again, and by an AC employee at that.

Cui bono?

Perhaps Mr Norman could comment on the economic drivers of Auckland's growth over the past two decades, and the implications of a prolonged slowdown in real estate, both in pricing and turnover. Which region would be most affected.

https://www.stats.govt.nz/information-releases/regional-gross-domestic-…. The table presents the factual evidence quite well.

Sorry to repeat myself folks but here goes:

Mr Norman starts well referring to demand as those "willing and able to pay"

Then he proceeds to undermine his good work by ignoring this criteria.

Demand (buyers) are LESS willing and able to buy at certain brackets of price, than they were in 2013 and 2016.

Measure of demand (real demand) is sales.

Population growth only shows you "need" for housing not effective demand.

So, to repeat, sales in 450-750k bracket in Auckland, first 6m of 2019, were 44% below that in first 6m of 2016. In that 3 year period, interest rates have fallen and we are constantly told that this factor and high immigration means (de facto and causatively) higher prices. Yet prices are falling.

In the 2016-19 period, Auckland sales of 800k-1.2m residential housing is down 25%.

Finally, one reader and contributor says that banks source 70% of their lending domestically, not abroad.

I am sorry but this misses the point by a country mile: foreign money was non-attributable in terms of source and 40% was supplied in cash form, not via banks, in purchases. This money was not produced nor earned in NZ. So, it artificially pumped up money supply and velocity which drove the boom 2013-16. The removal of that money is highly significant and can be seen in the disproportionate drop in purchases of houses above $1.4m in Auckland in the last 6m. This removal of liquidity will have negative feedback loop all down chain of supply in housing and wider economy and this point is entirely missed by 95% of commentators who are convinced that NZ wellbeing rests on exports to China of dairy and their tourists coming here. 70% of GDP rests on consumer demand. That takes a big hit when foreigners d not boost prices of sales by $100k a time. With normal delay this feeds back into the wider economy, about 9m later. GDP is already dropping and this will increase in pace, downwards.

Excellent post mikekirk29!

Translation: keep up the posts Mikekirk so that us gloomers can say we have an REA who agrees with us.

Again talking about supply. If supply is the only reason than house price in Auckland should never fall but move up, up and up only.

Forgeting that without Foreign Money and Money Launderers, how do local Kiwi buy a Million dollar or even $800000 house and even those who can afford, will they buy a pigeon hole unit for $800000 in far suburb of Auckland . Eariler when housing market was booming was possible as people were buying for fast money and not to stay but now to pay a bom to stay in pigeon hole - may not suit many even though can buy as the only motive of capital gain is no more for those pigeon hole.

Million dollar Plus House will be hard hit as that is one reason most houses with CV of 1.2 Million or 1.5 Million or 1.8Million (Except few that are worth) are hard hit and if vendor is not realistic will be unsold for few years to come.

To quote Jefferson:

"If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks and corporations that will grow up around them will deprive the people of all property until their children wake up homeless on the continent their Fathers conquered."

He was a smart man, and he knew that the ability to coin money and to allocate it was the real power of shaping the nation.

Banks 'coin' the money. Banks allocate most of it into property in NZ. That causes asset inflation. That's why house prices are high. The credit impulse in property has been steady at around 6% per year. That's why house prices are flat. It's about the price of money my friends and how much money is borrowed and against what. Not immigrants. Not shortages. Not land value. Quantity of money. We're more Japan than Ireland.

Yep, I completely agree. Price of property here is determined by how liberal banks are willing to lend. Any tightening of the lending will cause further price drop. Thats why the banks are fighting back and lobbying hard for the RBNZ drop the proposed new capital requirements.

Yeah and it's why spruikers including bank economists will get louder and more desperate

On the housing supply side:

- up until 2017 Auckland stifled house building by restricting land supply, the cost of land rose by massively in 5 years on the back of intense speculative gain.

- from 2017 onward Auckland doubled the amount of land supply available, the cost of land has fallen whilst the cost of building has increased - to create an apparent stability of prices. Speculative gains have ceased.

How much longer this balancing act can continue is a mystery, but it does not look like solid or well founded market stability.

"Melbourne and Sydney, meanwhile, saw house prices peak between June 2017 and March 2018. Since then, prices have fallen 15% and 10% respectively."

Shouldn't it be "10% and 15% respectively" ?

Next!

Please no more !

Bulls remain in denial...because they have to. Having lots of debt, declining asset value, and real possibility of recession based job losses will be the worst possible outcome when the banks finally come knocking. If there is a global even they will.

Lots of media beat up about holding prices, its all good take on a mountain of debt. I guess bailing out a boomer or investor dosent sound that great and a lot of young educated kiwis are just exporting themselves.

I have put some figures on FHB sales in Auckland, on LinkedIn this morning.

They do not support the theme that lower quartile prices and low interest rates are getting more sales in this bracket over last 12m, or in last 6m.

Unfortunately, this sort of analysis is not commonly seen, or attempted.

Buyer mentality has altered in real estate and asking prices are falling as a result.

Medians and averages are a rear view indicator of this. RE NZ prices and % in each bracket are a NOW indicator.

Great article David, unfortunately you're upsetting many on this site by daring to show that Auckland is different from OZ cities, they won't be happy, not at all

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.