The Reserve Bank used dubious assertions about wage inflation and the impact of global factors on the NZ economy to justify the aggressive 0.5% OCR cut last Wednesday. This Raving focuses on two areas where the RB's assertions were well off the mark to the extent they look like porkies.

This should ring warning bells with two areas businesses and investors should be taking actions already to protect themselves against the RB's misguided pro-growth experiment that has strong parallels with the misguided pro-growth experiment last decade.

The RB's analysis of wage inflation is well below the standard the RB should deliver

In the August Monetary Policy Statement the RB wrote: "Nominal wage inflation has been subdued since the global financial crisis (GFC), despite a steady economic recovery, a tighter labour market, and employment currently estimated to be near its maximum sustainable level."

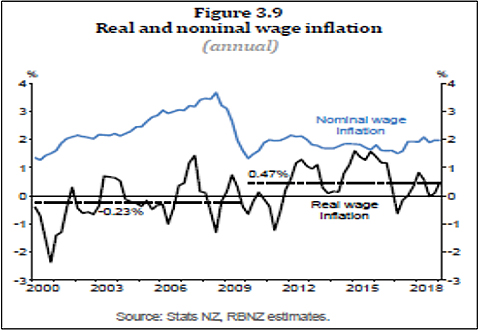

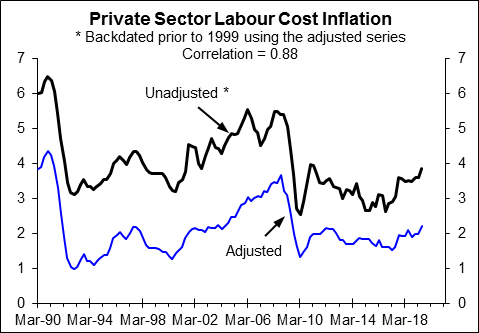

The chart below was used in the MPS to justify the claim that wage inflation has remained subdued at just under 2% over the last year. It was also used to show inflation-adjusted wage inflation that has performed better (black line). However, the RB was remiss in not highlighting that this measure of wage inflation by design hugely understated actual pay increases received by employees and paid by employers. This measure is designed to show what is happening to the pay of people who do the same job without any training or other factors that have a large impact on actual wage inflation. The second chart below shows the RB's preferred measure (blue line) and the unadjusted or actual measure of wage inflation that hit 3.8% last quarter (black line).

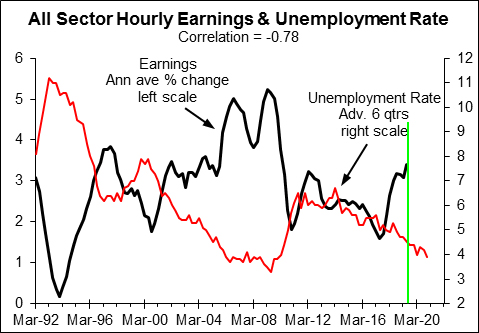

Even more enlightening, all sector average hourly earnings increased 4.3% over the last year and private sector average earnings were up 4.6%. The chart below shows the unemployment rate is still a useful leading indicator for the annual average percent change in all sector average hourly earnings. The peak correlation is a healthy -0.78 with the unemployment rate advanced or shifted into the future by six quarters. This chart makes a lie of the RB's claim that wage inflation has been subdued despite a tighter labour market.

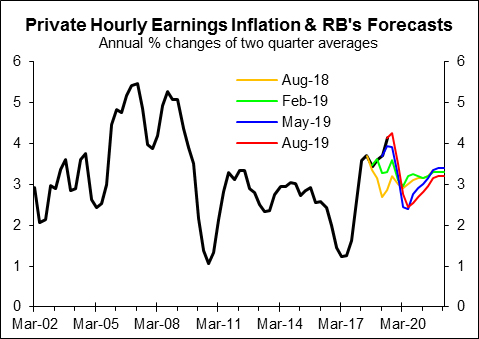

The RB's huge misrepresentation about how wage inflation has responded to the tighter labour market shouldn't be a surprise in light of the RB's terrible track record at predicting wage inflation (see the coloured lines in the next chart). A year ago the RB predicted an imminent, sharp fall in hourly earnings inflation (gold line). Despite getting it consistently wrong the RB has taken to predicting an even larger fall over the next year (the red line shows the most recent forecasts). The RB's wage inflation forecasts run counter to the improvement in economic growth it is predicting that will with a lag mean an even tighter labour market and with the range of government policies aimed at boosting wage inflation will mean the RB's forecasts end up looking like political propaganda. It reminds me of Peter Mahon's "orchestrated litany of lies".

The RB's claim about the impact of global growth on the NZ economy is misleading

Concern about global prospects has been a factor in the OCR cuts this year and the impact of global factors on the NZ economy has been a feature in the last two Monetary Policy Statements. Below is another quote from the August MPS:

"Weaker global conditions often lead to lower prices for our exports and imports, and reduced tourism spending in New Zealand. Currently, slower growth in global demand is suppressing the outlook for import and export prices, despite idiosyncratic factors supporting prices for some of the export products. Low export prices reduce domestic incomes and spending."

It doesn't take much analysis to bring into question the RB's views on the relevance of global factors to domestic spending and, by association, the case for the 0.5% OCR cut. As an aside, the latest cuts have a strong parallel with the OCR cuts delivered in 2003 that contributed to an overly tight labour market and were followed by 13 OCR hikes.

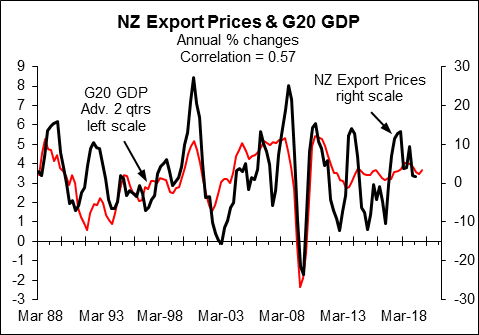

The next chart shows that there is some basis for suggesting that global economic growth, proxied by GDP growth for the G20 countries, has an impact on NZ export price inflation. The peak correlation at a relatively low 0.57 (like a 57% mark in an exam) is with G20 GDP growth advanced or leading by two quarters; which gives some credence to the idea that global growth does impact on NZ export prices although the link isn't close.

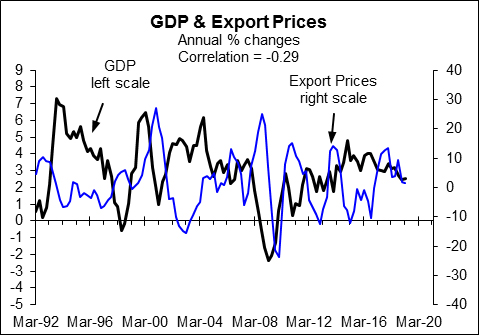

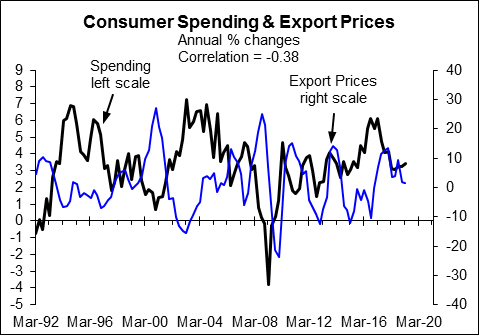

However, there is no basis to suggest a significant link between export prices and NZ spending. The next chart shows a negative not positive correlation between NZ export price inflation and GDP growth while the second right chart shows a negative correlation between export price inflation and NZ consumer spending growth; it is a similar story if export price inflation is assumed to filter through to spending with a lag. Other factors have swamped the impact of export prices on spending as will remain the case. Despite this, the RB continues to put too much weight on the relevance of export prices; contributing to bad OCR decisions.

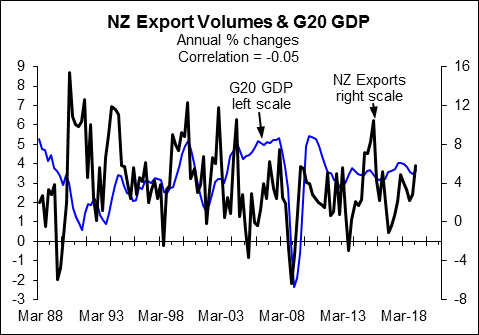

Similarly, there is no clear link between NZ export volume growth and G20 GDP growth (next chart). Other factors including weather generally swamp the impact of global growth on NZ export volume growth other than in situations like the 2008/09 financial crisis when the negative impact was quick but quite short-lived. Again, the RB's claims don't stack up to even basic analysis, which should ring warning bells for businesses and investors.

This article is re-posted here with permission. The original is here. Rodney Dickens also says: " In light of the importance of this issue that is covered in detail in the latest Economic Roadmap report I am offering the latest report to business and other major borrowers on a complimentary basis."

12 Comments

Hmmmmmm..

The [so-called] Ph.D. standard exposed?

Negative Interest Rates are coming. They would rather pull the wool over our eyes than risk making us all poop ourselves, which probably is going to happen anyway.

Who knows, perhaps, maybe the tax cuts proposed by National were more than an election bribe? After all there are other ways of getting money into the economy for stimulus, other than encouraging the private sector, to borrow and spend up gaily.

National tax cuts were a realignment to bring the tax take back in line adjusted for inflation. Fiscal creep means we pay more tax if it is not adjusted. I do like Bridges claim that tax brackets will be adjusted for inflation so the tax take stays relative sounds sensible

As long as nobody is controlling the banks' ability to lend overwhelmingly for the purchases of non-productive financial assets we're doomed to ride this roller coaster for ever.

This is a Warning Siren from Reserve bank that Be Aware

I said it last week and will say it again .............. the RBNZ is treating us like mushroom , keeping us in the dark and feeding us with manure .

They should come straight out and tell us their fears about DEFLATION pressures

Imagine if this hit the headlines???

https://www.zerohedge.com/news/2019-08-11/david-rosenberg-these-are-tru…

Well worth the read shawking, if you don't have the time, here is the critical take away in the last few lines.

"Investment recommendation: cash, gold, silver, long Treasuries – and limit your equity exposure to noncyclical sectors with strong balance sheets and reliable dividend/cash flow streams (even in the Great Recession, Walmart still made you money).

Most important – be as liquid as possible for the next several months."

Negative interest rates will change the landscape in a way that none of us are able to presently predict.

It will become obvious at that point, that our fiat currency will have become worthless.

Interest rate cut was to attempt to rescue house sales and to devalue currency. Of course, RBNZ cannot SAY that.

Jyske, Denmark's third largest bank, is offering a mortgage rate of -0.5 per cent for 10 years, which means borrowers' debts are reduced by more than the amount they pay back.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.