Today's Top 5 is a guest post from Council of Trade Unions' policy director and economist, Andrea Black.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz.

And if you're interested in contributing the occasional Top 10 yourself, contact gareth.vaughan@interest.co.nz.

As a blend of my old world as a tax specialist and new world as Policy Director and Economist for the New Zealand CTU – today I am looking at tax from the perspective of people in paid employment.

The tax system prides itself on neutrality. For the geeks amongst you that is what the mantra of broad base low rate is all about. Every dollar is taxed in the same way.

This is indeed is the starting point in any tax policy analysis, but it is just the starting point.

Often, however, when compliance costs or levels or types of enforcement are factored in, there are situations where working people in the PAYE tax system end up paying full whack on any income they earn but others don’t.

And this is much broader than the obvious - capital gains on residential property or the PIE tax discount for high income earners only[1].

1. 20% tax gap between self-employed and employed.

In 2018 Ana Cabral and Norman Gemmell of Victoria University concluded that the self-employed under report their taxable income by 20%. That will be from a combination of: income splitting using trusts; cash jobs; personal expenses claimed as business and simply not returning income earned. Most of which are not ‘legal’ but rely on enforcement and audits to stop.

For completely reasonable resource allocation decisions, Inland Revenue does not audit everyone. However, the effect is that there are favourable tax conditions – as MBIE called them[2] – that apply to the self-employed that do not apply to those who have PAYE deducted from every pay.

There is also another reason for this tax gap that became clear with the current MBIE consultation. Exploitation of vulnerable people[3]. Unscrupulous employers putting staff on contract which can have the effect of a pay cut if the cash they now receive is gross of tax when they previously received net.

All with the effect that they are now unwittingly responsible for their own tax and ACC.

It could even be worse if they are registered for GST. Their ‘employer’ can now claim back 3/23rds of what they pay to the contractor. With the contractor now also liable for GST.

Pleasingly the government is reviewing the employee/contractor boundary for employment law. But they will need to make sure equivalent amendments are made to the tax acts to ensure the definitions are consistent.

2. Untaxed transfers from companies to their shareholders.

One of the key tenets of the CTU and union movement’s approach to tax is that it should be progressive. All coming from the approach that the more a person has in income the more they should proportionately contribute to society at large.

And for those solely in the PAYE system that is absolutely the case. A person earning $12,000 pays tax at 10.5% on their last dollar while a working person earning $80,000 pays an equivalent 33%.

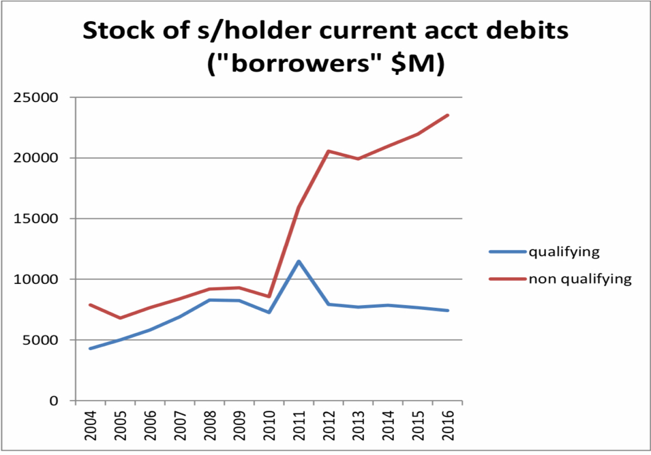

However, when looking at income from closely held companies[4], it all becomes less clear that income is taxed progressively. The Tax Working Group showed that loans from closely held companies’, aka shareholder current account debits, to their shareholders exploded from pretty much the time the company tax rate was reduced to 28%.[5]

So fringe benefit tax does not come into play on an interest-free loan, shareholders should be paying non-deductible – to them – interest to the company.

And because of this need to pay interest, which is not deductible to the shareholder, I have had it put to me that only an idiot would take income from a company this way.

A fair point. Except that in 2016 over $26 billion had been taken from companies by their shareholders as loans.

So, either there are a lot of stupid people getting income from their companies like this or they aren’t paying the interest, or the 5% tax saving is worth the interest payment.

Either way many high-income shareholders are getting income from companies and only paying – at best – the company tax rate of 28% while anyone else earning $70,000 from their job is paying 33%.

And this shouldn’t be happening.

But a combination of ‘not auditing everyone’ for compliance and administration cost reasons and weak dividend rules means that it is.

3. Phoenix companies.

Changing gear slightly.

While employers deduct tax from employees on a pay day, or receive GST when they make a sale – they don’t have to pay it to the government until a month or so after. This is a combination of reducing compliance costs for them and a bit of a compensatory cash flow benefit.

All good. They hold on to other people’s money for a while but in return they act as a tax collector. A reasonable trade-off.

However, the obligation to pay tax to IRD is with the business or company who makes the sale or does the employment. Even though as we see from 2) small businesses intertwine business and the personal finances of their owners.

What that means is thanks to limited liability, if the company has no money and doesn’t pay on the tax, Inland Revenue is on the back foot with collecting. And this equally applies to employees who miss out on wages when the company, that owes them, is liquidated and any health and safety liabilities the company may have incurred.

And this becomes even more egregious when the same owners restart their business with a new company – phoenixing. Effectively stealing from their employees with lost student loan and KiwiSaver contributions as well as all of us through not paying the tax they collected from others.

The Tax Working Group recommended directors with an economic ownership in a company become liable for any GST and PAYE that is due when a company fails. This should be introduced stat and equally apply to lost wages and health and safety liabilities.

Because otherwise the status quo is saying that being able to start a new business is far more important than any obligations to society at large from any past businesses.

4. FBT exemption for charities.

Back to tax. Number 4 is a bit more niche but evocative of my general point.

Business generally pay fringe benefit tax on any fringe benefits they give to their staff. Charities, however, are largely exempt. They are exempt because there were substantial submissions from charities that any fringe benefits – think Plunket nurses’ cars – are incidental and so the compliance costs of dealing with FBT outweighed any revenue or risk of substituting wages for benefits.

All fair enough. Until charities started giving credit cards and vouchers to their staff instead of pay. And because it was quite widespread – the law changed to make FBT payable on such benefits.

But the general exemption remained. And so when the recent reporting on the Neurological Foundation and the bespoke benefit package – which included personal travel - of the Chief Executive came out, I was unsurprised.

Again, an ostensibly reasonable way to minimise compliance costs has enabled high income people to pay less tax. A loophole that is unlikely to be closed down because it is so rare – unlike when the general masses use the same rort – it is promptly stood on.

5. Right from the Start tax administration.

Inland Revenue has relatively recently adopted an approach to tax administration called Right from the Start. The vibe is that rather than going back and getting involved in messy audits when people get things wrong – they’ll put their energies into helping people get things right in the first place.

And such an approach is intuitively appealing.

However, it recently played out when it became clear a large number of people had underpaid tax on their PIE income[6] and had so for many years. IRD made a business decision not to go back and pursue that tax. Because administration costs.

Legally IRD can go back 4 years to collect back tax. And from the perspective of a working person whose tax is always right because PAYE is deducted – four years can be considered a complete gift.

So to not go back at all on income from capital, and focus on going forward has hallmarks of phoenix companies. Except here it is just the tax base – and therefore users of public services – who miss out on the revenue.

And again, it sends the message that the people who always do the right thing are not the comparator when these policy choices are made.

So, to all the people who have in the past asked me ‘what does paying their fair share’ actually mean for tax? It means this. It is not all about Google and Facebook.

It means giving greater weight to fairness in policy decisions, and how the person who has PAYE deducted is treated, over compliance cost or administrative costs. Or in Living Standard Framework speak, it means putting as much emphasis on human and social capital as we have historically done for physical and financial capital.

Because ultimately our tax system is based on voluntary compliance and tax being collected in the background. All of which is put at risk when there is a two-tier tax system with different outcomes for those who pay their tax quietly and diligently each pay day and those who don’t.

[2] Anya’s story

[3] https://www.mbie.govt.nz/dmsdocument/7376-better-protections-for-contractors-consultation-summary Sue’s story.

[4] These are ones where the shareholders and directors are the same people. It is a structure commonly used by small business.

[5] A current account is the common way for companies to account for transactions between them and their shareholders. Transfers from the company to the shareholder are debits or assets to the company while transfers from the shareholder to the company are credits or liabilities for the company.

The distinction between qualifying and non-qualifying companies is not relevant for this discussion.

[6] PIE stands for Portfolio Investment Entity. An explanation can be found here: https://www.ird.govt.nz/roles/portfolio-investment-entities

23 Comments

Great article and nice career move, Andrea. All the best in the new job.

My company made 300k cash profit last tax year, but because of some asset revaluations I in fact made an actual loss and am looking forward to a big tax refund as well as full WFF entitlement, which is great because I need to pay for my latest Tesla.

And what asset revaluations are you legally deducting from income then?

Outside the Herd Scheme (which as many times works against you as for you), name an asset revaluation, anyone, that is deductible for income tax purposes? Noting this article in pretty much talking SMEs.

An downward valuation of a bond investment would be deductible under the financial arrangement rules.

That's not a revaluation reserve, but okay. Also, though, upwards movements are taxable. In fact a bond is one of the most viciously taxed of all investments ... all interest and increases in value are taxable. Decreases in values represent not theory, but a real loss.

But this is irrelevant to the article which is about business deductions against business income.

Change will eventually be enforced by those who pay their taxes quietly on those who are abusing the current system, once they have the numbers to vote in a government that looks after them.

I'm picking it will take 20 years to see off the baby boomer generation.

Never seen so much envy ridden uniformed rubbish in an article (written by academics, what a surprise) or in comments.

Accountancy firms are not in the business of claiming private, etc, deductions for their clients. A lot of clients might 'think' they're getting away with all and sundry, and flap that around in the pub, but once their accountant has been through all the ledger accounts, that stuff is taken out, and a GST reconciliation is sent with how much to pay back (or recommending a voluntary disclosure).

Then lets look at income splitting via a trust. Trustee income is taxable at 33% the top personal rate. So if all income was left in the trust with all adult beneficiaries then then the 'business' income would be taxed much higher than if the individual had earned it (if allocated as beneficiary income, then at the same rate as a wage worker). Okay, distribute to the kids: nope - minor beneficiary tax rule, taxable at 33%. There may perhaps be a slight advantage allocating to an individual over 18 in the first few years they're working, but then it's on current account and once the individual turns 21 - with trusts facing increasing transparency to beneficiaries - they can demand payment thank you (or you've now not so cleverly created a relationship property claim) ...

Debit shareholder current accounts are a disaster: if the company doesn't pay FBT on the interest foregone, then it has to charge the shareholder interest at FBT(market) rates: taxable income to the company; not deductible to the shareholder. Debit current accounts are normally the result of bad times for business when there is not enough income to allocate salaries to cover drawings. Worse, under liquidation debit current accounts are taxable under the financial arrangements rules (an unmitigated disaster).

[Yes, the authors also make this point but then assume there is widespread abuse: these debit balances are a reasonably new thing, the numbers have surprised me, so I would question that assumption; again, the accountants will clean this up (that's their job). Also the debit current account has to be declared on the IR10 - otherwise the client is not protected by 4 year statute bar - so given the tax return is telling IRD here's a debit current account, it would take a particular sort of idiot to 'evade' tax by not then charging the interest on it or company paying FBT.]

Etc.

Perhaps some points re phoenix companies are warranted, but not surprisingly most working via those end up broke at some stage. They're wide boys and a very small minority I bet. And I wouldn't want their seat-of-the-pants lives.

Here's an interesting thing though: if IRD moves everybody to AIM as is their want, to take out accountants and agents, then yes, there will be wide scale avoidance and evasion. The Department will need an auditor for every ten taxpayers.

Totally agree Mark. There is no way (PAYE) employees of accounting firms, who do the recoding for client accounts leave non deductible items in expenses. People that skite at the pub about what their accountants deduct are deluded. Accountants are not going to risk their tax agency for a client's dodgy tax write off. And it is a concern that IRD want to move away from intermediaries fixing up client accounts and GST. There will be definitely more errors if small businesses file their own returns.

You have to pay the full whack of taxes via PAYE, especially if you are not a high income earner, because others are envious of you. It is, without doubt, an envy tax imposed on people who choose or maybe are unable to buy investment property where any capital gain is not taxed. So yeah, there you have it.

Andrea, can you help with some comment about Just Transition.

We understand it came from the trades union movement.

Thanks in advance.

Hi Henry. Here are the CTU’s contact details. https://www.union.org.nz/contact/

Cheers Andrea

FBT should go. Problem (apart from complexity) is that the business pays the tax, not the individual. The value should be imputed into the wages/salary, much like farm accommodation to an employee. It also impacts WFF as the value of the fbt is not included any any welfare testing.

(never mind that the farmer owner pays no tax on this big flash house he gets, while poor older farm worker does...buts that's a TOP issue)!

Wrong on one point Rastus: the value of the taxable benefit (FBT) to the employee is caught within family joint income for WFF purposes: have a look at form IR215 on IRD site.

Come on Andrea

"The tax system prides itself on neutrality. For the geeks amongst you that is what the mantra of broad base low rate is all about. Every dollar is taxed in the same way.

This is indeed is the starting point in any tax policy analysis, but it is just the starting point."

This is simply NOT the case. More than 40 years ago Mirrlees and Diamond (both Nobel prize winners in economics, Mirrlees for this work) showed that it is not the case that all income should be taxed at the same rate. This is not good for efficiency reasons, and it is not good when equity considerations are taken into account. Most economic theory suggest that capital income should be taxed at lower rates than labour income. Almost all OECD countries actually tax capital income at lower rates than labour income. New zealand is an exception - except when it comes to owner-occupied housing, for the income from owner-occupied housing is taxed at lower rates than labour income in New Zealand.

"Broad based, low rate" is a New Zealand slogan that is used to defend a unique NZ approach to taxation. It is not heard overseas, where tax rates tend to be more in line with standard economic theory. As far as I can see, one of its main purposes is to ensure very high paid New Zealanders have some of the lowest marginal tax rates in the world - great if you are one of them, perhaps not so good if you are not. A mantra perfect for well paid tax bureaucrats and tax accountants.

According to the OECD cross country comparisons, New Zealand has some of the lowest taxes on labour income in the OECD and the highest taxes on capital income. Most other countries, countries such as Norway, Sweden, Denmark and Finland which are known for high incomes and low inequality, try and tax capital incomes at lower rates than labour incomes to ensure that firms have good incentives to invest in capital equipment and pay high wages. The international evidence is fairly clear that when countries raise taxes on capital incomes some of the burden falls on wage earners through low incomes.

I know "broad base low rate" is a popular slogan in NZ, but please don't perpetuate the myth that it is orthodox tax policy or the normal approach to tax policy in most other countries.

It is the starting point - in NZ - of every piece of tax policy analysis I have been part of - or around - for the last 20 years. And it was the approach before I turned up too. By all means disagree but that wasn’t the point of my article. My point is that the system isn’t neutral in practice and to me that is a problem if you want to keep ordinary people dutifully paying their taxes.

I would argue that with no tax on capital gains on residential property and the high income PIE discount - capital is already taxed less. But again that wasn’t the point of my article.

You are right, of course, Andrea, that the "all income should be taxed equally" principle it is the starting point of most discussion in NZ about tax policy. The Tax Working Group didn't seem to even query it. But that does not mean it is the right place to start. "Broad base low rate" is a principle that is simply inconsistent with standard tax theory and overseas practice. Is this a case where New Zealand has got the best idea, where most tax experts (outside New Zealand) are wrong, and where most countries have the basic tax strategy wrong? Well that is a possibility, but it strikes me as a little unlikely. When everyone is sailing one direction and you choose to sail in another, you should be very careful that you have chosen the right direction, and make sure your system is delivering what you want it to deliver. New Zealand has a tax system that provides incentives for high labour participation and low capital accumulation, without being particularly redistributive. New Zealand has an economy that has high labour participation, little capital and a lot of inequality. It is not clear that tax choices are the main reason for these outcomes, but when you choose policies so different from other countries and orthodox (international) tax principles it seems reasonable to question the starting assumptions.

You certainly raise legitimate concerns where firms choose loopholes to try and reduce their tax burden. But there are really interesting alternative ways to address this problem which New Zealand doesn't even seem to contemplate because it is so fixated on the "equal tax for equal income" principle. In the Scandinavian countries, for instance, the tax rate on capital income is set at the lowest marginal tax rate - this rather removes the incentive to search for ways to reclassify business income to reduce tax rates, although it does provide incentive to classify labour income as business income. Of course high income earners in these countries pay much higher tax rates to ensure that the tax system achieves its redistributive aims without reducing the incentive to invest in productive firms. The celebrated Hall-Rabushka flat tax also solves many of these incentive problems while attempting to achieve redistributive goals. When you rule out such innovations because they don't tax all income at the same rate (or at the same time) you end up only contemplating a very small range of solutions to problems. Experience across a wide range of endeavors suggests that ruling out successful or interesting ideas simply because it is 'not the way we do things around here' is a recipe for isolated backwardness.

It is true Scandinavian countries have lower company tax rate for widely held companies. Closely held companies - the point of my article - tend to have the same tax as individuals. Those countries also have payroll taxes on business, capital gains taxes, property taxes and much higher VAT/GST.

They collect - as a proportion of GDP - much higher levels of tax than we do in NZ.

I agree that the Scandinavian approach to tax has a lot to commend it. But I think we need to look at it as a whole and not just focus on the tax rate for widely held businesses.

You are preaching to the converted there, Andrea - I have now made the point for years that the NZ tax system is fundamentally different to most tax systems in the OECD, largely because of the way social security is funded in NZ, partly because we have chosen to tax retirement savings differently from most other countries, and partly because we have chosen to tax high income earners at low marginal tax rates. Unfortunately the first issue - the biggest single difference between the NZ tax system and tax systems overseas - didn't warrant more than a single paragraph of discussion in the recent Tax Working Group report, even though it is the primary mechanism that countries overseas manage to drive a wedge between labour income and capital income tax rates. It would have been nice if the group had either discussed this or reported their discussion to the rest of us. The third issue was bizarrely ruled out by the Government so it didn't get discussed - it seems to be an article of faith in NZ that top marginal rates on our highest income earners (such as the Prime Minister, senior bureaucrats, and tax accountants) ought to be lower than the rates in the UK, Australia, the USA, Canada, France or Germany. Unfortunately it means there will need to be yet another group or analysis some time in the future, one that actually takes tax theory and overseas experience seriously. In any case, the growing amount of international evidence about what works and what does not work will justify a re-examination of New Zealand's tax structure at some point - there have been some very nice papers about the incidence of capital income taxes on wage earners, for instance. I look forward to your perspective on some of this work as it seems directly relevant to New Zealand workers.

looks like you have touched a nerve,provoking a blustery defence of the saintly role that accountants serve as gatekeepers of morality.I would think 20% is a starting point and would indicate a newbie who is testing what he can get away with.

I would have been unemployable if I had had to work for someone else throughout my working life. I am temperamentally unsuited to working in other people's businesses or in a civil servant type role; I consider working for others as undignified, really a form of slavery no matter how much you are paid. Working for others is tolerable when you first join the workforce, but by their late 20s a person worth their salt should be be self-employed if they want to exercise their talents to the full.

Anyway I've paid more tax as a business owner than I would have as a mere employee. A business owner who tries to avoid paying their share of tax shouldn't be in business and will ultimately fail. I've provided others with employment. My relatives have been mostly self-employed.

Business ownership can come with a lot of extra worry and responsibility and at times I have been envious of those who are content to be employees. But in our society the business person deserves their success and businesses are the main source of employment.

So police, nurses, surgeons, firefighters, teachers and any number of other essential careers that don't lend themselves to self employment, are not worth their salt? Nice one, imagine that society

Streetwise never said that.

Don't put words someone didn't say into their mouths just so you can run out your pet grievance. That's dishonest, like the bias of this article is false and dishonest.

Without SME's set up by the self employed, there are no jobs. And there is no tax to pay the police, etc.

Incidentally I've paid far more tax as a businessman than I suspect I ever would have on PAYE working for someone else. (And I'm still paying lots of tax).

Typical lefty "it's all their fault" misdirection. Based on the desire to stir up envy, hatred and blame so they can seize power by whatever means.

https://www.asiatimes.com/2020/02/opinion/did-they-miss-the-french-revo…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.