Welcome to our COVID-19 lock-down Top 5 weekend special. All our previous Top 5s are here.

The 2° Investing Initiative, a non-profit think tank, has had a crack at providing a stress-test template for financial supervisors to simulate potential losses on banks’ and insurers’ balance sheets under six different COVID-19 pandemic scenarios over the next 36 months. The paper draws on work done for climate change stress-test scenarios in partnership with the California Insurance Commissioner, the Bank of England, and the European Insurance and Occupational Pensions Authority.

The 2° Investing Initiative acknowledges its pandemic stress-test scenarios lack a number of key indicators including exchange rates, sovereign spreads and potential defaults, plus unemployment. Thus it's "an incomplete exercise."

However, to the extent that it does provide indicators, it represents the first attempt at developing a stress-test scenario specific to the type of pandemic currently under way in the form of COVID-19.

The paper should be read with an appreciation for the unchartered territory it seeks to enter. There are of course a range of studies on the potential financial effects of a pandemic in general. The past few weeks have also seen a range of reports, blogs, or op-eds define potential effects to different markets, whether it be credit, housing, or equity, to cite just a few examples. Here, a first attempt is made to represent, as close as seems currently realistic, an attempt at understanding what a COVID-19 stress test should or could look like.

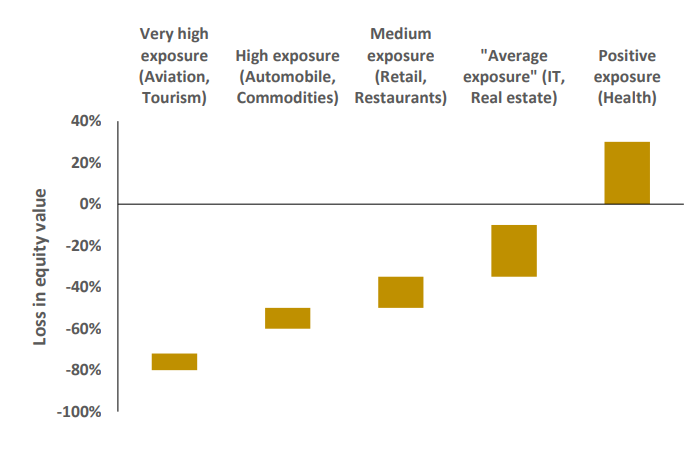

Among other things the paper assesses the health effects, the sentiment effect, policy responses, the impact of COVID-19 on GDP, inflation and oil prices, unemployment, stock market prices, corporate credit spreads/default, mortgage defaults and real estate prices.

The empirical evidence on the relationship between real estate prices and pandemics – limited as it is – suggests a very limited effect of pandemics and related health events on housing markets. The price elasticity of housing demand is relatively limited and given the incredible pressure on housing in many jurisdictions, this analysis suggests that ‘at best’ the pressures will lead to a reduction in price increases, but not a shock to housing prices.

The 2° Investing Initiative, which includes an "Armageddon scenario," says one of the critical questions is the extent to which past stress-test exercises can be used as an indicator for whether the banking or insurance sector is prepared for the crisis the paper's modelling outlines.

There are two points on that aspect. First, traditional stress-tests may reveal higher shocks than those identified in ‘sustainability scenario analysis’ or stress-test exercises like the scenario developed in this paper. However, unlike in traditional stress-tests, these shocks don’t tend to be cyclical, but secular. As a result, we see a more permanent value destruction in many cases than in stress-tests. Mortality creates a permanent loss to labour supply – even if in this scenario that loss currently appears contained – unlike in a crisis where job losses do impact long-run productivity, but in principle the unemployed can eventually find new jobs.

Second, traditional stress-tests assume defaults and losses at asset class level. As a result, they cannot identify micro-prudential sector- or risk-specific issues. For example, in the case of climate change, asset class losses are contained under most transition scenarios, but lead to losses exceeding stress-tests in certain sectors.

2) How panic-buying revealed the problem with the modern world.

Writing for The Atlantic, Helen Lewis looks at how just in time ordering came unstuck as panic about COVID-19 spiked in developed countries, and images of people stock piling toilet paper and empty supermarket shelves appeared all over both traditional media and social media.

Any student of economics will tell you that modern supply chains rely on just-in-time ordering. In the case of British supermarkets, production schedules are tailored precisely to demand, so that unused stock does not sit in warehouses or go to waste. In the current crisis, the country has not run out of essential goods such as toilet paper; the difficulty is getting them onto the shelves quickly enough.

Lewis argues the limits of modern society's drive for efficiency were revealed.

What happened at supermarkets is worth dwelling on, because it reveals a problem with one of the modern world’s most hallowed concepts: efficiency. As businesses and governments chase ever-tighter margins—ever-greater efficiency—they have created systems that are finely tuned, but also delicate. Many of us are individually guilty of indulging this tendency, encouraged by the trendsetters of Silicon Valley. “The tech sector’s overarching philosophy remains bent towards treating the human brain and body like a machine that can be tweaked and perfected until it is running at peak efficiency,” the journalist Lux Alptraum wrote for Quartz in 2017. This is, however, a fundamentally inhuman philosophy. People aren’t machines. We are inherently inefficient, with our elderly parents and sick children, our mental-health problems, our chronic diseases, and our need to sleep and eat. And, as the past few months have demonstrated, our susceptibility to novel viruses.

We have been trained to see efficiency as a desirable goal. We often don’t see, or don’t acknowledge, the risk of catastrophic meltdown. Think of efficiency as a high-performance engine. Under perfect conditions, it delivers maximum power and minimum waste. However, that very efficiency makes it less robust. Highly efficient systems have no slack, no redundancy, and therefore no resilience and no spare capacity. That’s a problem because perfect conditions rarely exist for long in the real world, and “rare” events happen more often than you’d think. (Climate change, for example, has turned “once in a century” challenges such as extreme heat waves and floods into more regular occurrences.)

#StayHomeNZ pic.twitter.com/T1EilIm9f2

— New Zealand Police (@nzpolice) March 25, 2020

Bloomberg's Francis Wilkinson compares President Donald Trump's handling of COVID-19 with President Lyndon Johnson's handling of the Vietnam War, and President George W. Bush’s handling of Hurricane Katrina. Trump does not come out of it well.

Johnson may have misjudged Vietnam, but at least he was acting, in part, on behalf of what he perceived to be the national interest. Trump’s response to Covid-19 runs strictly on personal pathology. The failure to obtain basic equipment, including masks and ventilators, is akin to sending soldiers off to war without rifles. His initial falsehoods about the imminent spread of the virus, like his consistent inconsistency, reflects Trump’s perception of his self-interest as well as his lifelong recourse to make-believe.

Trump lacks Johnson’s institutional knowledge or mastery of government. But Johnson’s weaknesses — ego, vanity, insecurity, selfishness — reappear in Trump at freakish levels.

At the time of writing the USA has more confirmed COVID-19 cases than any other country, meaning pressure will continue to mount on Trump.

In February, Trump said the number of cases would soon be “zero.” Bush may have failed to prepare; Trump actively thwarted preparation. Trump is a tactical liar, spreading falsehoods to get through the next five minutes, not the next five weeks or months or years. He is aided by a Republican Party that has routinely defended his incompetence and corruption and is now poised to contribute to the defining event of his presidency: unnecessary death on a mass scale.

And, like other world leaders, COVID-19 may define Trump's presidency. And not in a good way.

Casualties from the coronavirus failure will not persist for years. Scientists will devise a response, and public-health experts will make it stick. But Trump, who continues to encourage reckless behavior that will lead to additional loss of life, will make the death toll far higher than it should have been. The price of an unfit American president will be paid in thousands of American lives.

The chart says it all. https://t.co/Nt9pKrpZB2

— MarketWatch (@MarketWatch) March 27, 2020

3A) Writing in The Atlantic, Ed Yong points out that on the Global Health Security Index, a report card grading countries on their pandemic preparedness, the United States scores 83.5, the top mark.

Rich, strong, developed, America is supposed to be the readiest of nations. That illusion has been shattered. Despite months of advance warning as the virus spread in other countries, when America was finally tested by COVID-19, it failed.

His article, How the Pandemic will end, is an interesting if sobering read.

With little room to surge during a crisis, America’s health-care system operates on the assumption that unaffected states can help beleaguered ones in an emergency. That ethic works for localized disasters such as hurricanes or wildfires, but not for a pandemic that is now in all 50 states. Cooperation has given way to competition; some worried hospitals have bought out large quantities of supplies, in the way that panicked consumers have bought out toilet paper.

Partly, that’s because the White House is a ghost town of scientific expertise. A pandemic-preparedness office that was part of the National Security Council was dissolved in 2018. On January 28, Luciana Borio, who was part of that team, urged the government to “act now to prevent an American epidemic,” and specifically to work with the private sector to develop fast, easy diagnostic tests. But with the office shuttered, those warnings were published in The Wall Street Journal, rather than spoken into the president’s ear. Instead of springing into action, America sat idle.

Derek Thompson: America is acting like a failed state

Rudderless, blindsided, lethargic, and uncoordinated, America has mishandled the COVID-19 crisis to a substantially worse degree than what every health expert I’ve spoken with had feared. “Much worse,” said Ron Klain, who coordinated the U.S. response to the West African Ebola outbreak in 2014. “Beyond any expectations we had,” said Lauren Sauer, who works on disaster preparedness at Johns Hopkins Medicine. “As an American, I’m horrified,” said Seth Berkley, who heads Gavi, the Vaccine Alliance. “The U.S. may end up with the worst outbreak in the industrialized world.”

4) Fed balance sheet tops US$5 trillion for first time as it enters coronavirus war mode.

David Chaston is doing a sterling job with interest.co.nz's breakfast briefings during these crazy times. One of the most mind boggling aspects to me are David's regular updates on how much money the US Federal Reserve is splashing around on a daily basis. Here Reuters points out the Fed's balance sheet has now topped US$5 trillion for the first time.

The U.S. Federal Reserve’s balance sheet soared past $5 trillion in assets for the first time this week as it scooped up bonds and extended loans to banks, mutual funds and other central banks in its unprecedented effort to backstop the economy in the face of the global coronavirus pandemic.

The Fed’s total balance sheet size exploded by more than half a trillion dollars in a single week, roughly twice the pace of the next-largest weekly expansion in the financial crisis in October 2008. As of Wednesday, the Fed’s stash of assets totalled $5.3 trillion, according to data released on Thursday.

Where's the money going? Treasuries, mortgage-backed bonds, foreign currency swap lines to other central banks including the RBNZ, and new liquidity facilities aimed at stabilising money markets and supporting the banks that transact directly with the Fed.

Banks continued to line up for loans directly from the Fed at its so-called Discount Window, long stigmatized as the source of last resort for weak banks to get cash. The Fed is trying to ease that stigma and has encouraged banks to use the facility more liberally.

As of Wednesday, those borrowings were up to $50.8 billion from $28.2 billion the previous week.

This was, of course, bound to happen. And doubtless Queen's Bohemian Rhapsody will be but one of many famous songs adapted to a coronavirus theme.

64 Comments

It's not "where is the money going".

That's debt, conjured up by keystroke.

So it's " will it ever be repaid, how and by who(m)?

It will never be repaid in full. It will be paid continually however by future generations as it still continues to increase until we change our monetary system sadly enough.

My learning this week is that people living paycheck-to-paycheck are told they should have at least a month in savings while billion dollar corporations are so poorly managed they're on the brink of bankruptcy and asking for bailout loans with just a couple of weeks of reduced cashflow.

....and that those who were prepared, and can provide for themselves, will be 'asked' to pay the debts of both of those groups ( to answer powerwonkiwi's question above!)

I guess that’s the cost of living in a society like ours, not that we get to choose otherwise though.

So Morgan is on the record, no declines in house prices.

A house in St Clair, Dunedin RV $820k and would have gone for $100k to $150k over that in January is now for sale at $600k. I doubt it will sell for that at the moment and we are only at the very start of this and there are already fire sales.

It looks like Morgan is already wrong.

https://www.trademe.co.nz/property/residential-property-for-sale/auctio…

It only takes a couple of houses to sell below expectations and the market changes really fast..why buy now when this is the trend attitude.

Stanley? "Morgan Stanley forecast reveals Australian house prices could fall by up to 15 per cent.... which would mark the largest decline since the early 1980s."

Gareth Morgan, the self appointed knower of everything.

Gareth Vaughan on stress testing COVID-19 above #1.

I wouldn't worry too much about Gareth Morgan's expectation re the property market. He's as bigger advocate as any of us for a return to realistic, affordable prices that aren't supported by tax breaks and bailouts. But he's realistic enough to know that until we get a change in the structure of the economy ( that's what The Opportunities Party was all about really) we won't get what's badly needed.

Maybe, just maybe, this current chaos will give Gareth Morgan what he's always advocated for - more fairness in all things economic?

No body switches NZ to the ignore faster than GM.

Not many take his advice anyway, especially his professional whom he decided to show how to play the game.

Although we did all take notice of 'Happy Feet!' How time flies....

http://www.stuff.co.nz/national/5193679/From-Kiwisaver-to-penguin-saver

That before he poisons Stewart Island with toxin that remains in the ecosystem for years

Poisoned Stewart Island?

Seems to me that house has an RV of $620k not $820k or am I missing something? https://homes.co.nz/address/dunedin/saint-clair/18-hobson-street/LpPRX it also seems to have a very odd homes.co.nz listing generally.

I'm a risk management specialist, with some experience of working in a DHB, but working for another Government Department as well as experience of working commercially. I can say that no organisation has a tolerance for discussing, let alone preparing for a worst case scenario. This is often the case of how do you break the silence without becoming the person no one listens to? I can see Trump wanting to put some of the commentators Gareth cites above, against the wall and having them shot for treason.

I know of one organisation which prepared somewhat post the bird flu or CARS and bought up a whole bunch of pandemic supplies and then locked them up with no one able to access them unless the emergency plan was activated. Admirable, maybe? They forgot that virtually all of those supplies had a shelf life so the preparation needs to including cycling the supplies through to ensure it stays viable when needed. People who tried to suggest this to them at the time got slapped down.

'This is often the case of how do you break the silence without becoming the person no one listens to?'

Too bad art can't imitate life more and we could be this guy, https://tvtropes.org/pmwiki/pmwiki.php/Main/EinsteinSue

By 2025, New Zealand's housing "wealth" will have fallen by 35 percent. . The lost decade.

Yet the long hours, long commutes and large mortgages will remain.

This is about to be a very different country and it wasn't all beer and skittles before this all went crazy.

Maybe the lucky few will still have the longs hours and long commute. The really unlucky will just have the large mortgage....

The only way I can actually see any way out of this is if EVERYONE, and I mean the Fed, global central banking institutions and the IMF all collectively agree to write off a bunch of debt - like trillions of dollars of debt is just earmarked as noncollectable and disappeared in the name of expediency. Nations still need to function after this and build infrastructure, and a lot of those capital works are going to be deferred because they can't afford them. No infrastructure, fewer jobs in the central govt pipelines, and the ripple effect goes on. I would feel better about this if we didn't have someone with the intellect of a Terry's Chocolate Orange in the Whitehouse. Actually I would feel better if there was an actual Terry's Chocolate Orange serving in the Whitehouse.

I agree, there will be a lot locked out of buying there first home due to the sharemarket crash.

Property owners will be fine as interest rates are so good.

Opportunities will present!

TM2. Market investors are already severely marking down commercial property REITs. For your 'property will hold up' forecast to be fulfilled those investors either have to be calling it seriously wrong and we'll soon see a bounce or else directly held property is about to fall sharply in alignment with market investors bets. As a REIT holder I'd like to think you are calling it correctly but from long experience of multiple market upheavals and recessions I think there's plenty more rough water ahead.

Here's an article about Ostriches burying their heads in sand.

https://wonderopolis.org/wonder/do-ostriches-really-bury-their-heads-in…

Central bank actions have really just been wealth transferring anyway. From pensioners and savers to property owners. A change back the other way would actually just send money back whence it came.

One of the most mind boggling aspects to me are David's regular updates on how much money the US Federal Reserve is splashing around on a daily basis. Here Reuters points out the Fed's balance sheet has now topped US$5 trillion for the first time.

It is notable that an upward autonomous adjustment to the Fed's SOMA security holdings rose ~$977 billion because currency in circulation increased that much between 27/03/2008 and now.

Its interesting that reporting focuses on the 'impact' of Covid-19? From the facts that are readily available now, the impact is not due to the virus, its due to the media driven reaction/hysteria that is influencing governments to take unprecedented and unnecessary actions. #OpenNZforBusiness should be the governments priority not dwelling on underwhelming numbers of cases in New Zealand that don't equate to the predicted death rates by biased 'scientists' in the UK.

https://thefederalist.com/2020/03/26/the-scientist-whose-doomsday-pande…

I wish the experts would say "we just don't know"

You sound like something out of the Fifties.

Sorry, but 'lets keep the econmy going at all costs, I've bet my butt on it'- is a wee bit dated.

Perhaps do some homework.....

Ok, Well... death from despair will kill more Americans than Covid-19 this year. A 1% rise in unemployment causes (directly) 36,000 Americans to die. Do some home work and look it up. It should be easy for you to find it because it sounds like you are doing a significant amount of research/homework your self, right? or, do you just read the headlines. Also, another byte of information for you.... "On re-evaluation by the National Institute of health (Italy), only 12 percent of death certificates have shown a direct causality from coronavirus, while 88 per cent of patients who have died have at least one pre-morbidity - many had two or three,". Show me your home work please.

Do you know the saying about making a total arse of yourself when you assume? Perhaps if you'd done a little research yourself and found some info on PDK, which isn't exactly hidden, you'd know he has been known to give university lectures.

Lecture us please on what assumptions have been made?

If that's the case, then after the virus has passed and knocked out those with other medical issues, we should see reduced demand on our healthcare services??

You may be right be practical. I think the governments response is ok for now, but if it doesn’t work within say 6 weeks I think we will have to just accept the virus and the deaths (as you say predominantly to people who in a bad state to begin with). The people who are vulnerable can choose to self isolate if they desire.

The media hype is very strong, people under 65 honestly think this virus is a death wish when realistically their odds are very good. If you had a car crash and the doctor told you you could either go through years of not being able to leave the house or have a operation with a 1/1000 death rate which would you choose?

For NZ, the loss in equity value of real estate is tied too closely to tourism for the graph above to apply. Tourism is our number one export earner, and hits to that sector will bleed into property—both directly, via AirBNB yield (and therefore asset value) declines, and indirectly, via job losses in the tourism sector. Nearly 15% of our workforce is directly or indirectly employed in tourism, and there are 37,000 AirBNBs that depend directly on this sector for revenue. Depending on how long our borders are closed, and how well international (and domestic) tourism recovers, property's 'average exposure' may well prove to be aspirational.

One of our largish family businesses supplies components to the construction trade, a significant % to commercial developers, hotels, govt. infrastructure etc. This week we spoke with the principals in all our larger developments and every one confirmed the projects will continue despite the recession, that they had post covid re confirmed their finance arrangements etc. The consistent theme was that as the projects have multi year timeframes and are long term investments, they are looking through C19 and recession. Brave words perhaps and no doubt saying what we want to hear but the high level of commitment was consistent and we believe genuine. Of course if this ugly economic brute becomes catastrophic their commitment will wither but if Robertson continues to project a balanced sense of realism and fiscal reactiveness there is hope we can survive this.

But he isn't. That's the whole point. Realism says that by 2030, all bets were going to be sequentially 'off'.

This has likely brought that forward by a decade.

It's clearly hard for folk to argue for something detrimental to them and their perceived place in the world, but dispassionate appraisal tells us the present system is unsustainable. And it was brittle in a resilience sense, because the clever economists bled out all the capacitance (buffering, resilience) in the flow.

Some of us saw that problem decades ago, and live by (and advocate) a lesser-brittleness, more capacitive, lesser demanding, more resilient way of living. That includes not being vulnerable to shocks like this - which are statistically unavoidable.

Robertson having his eyes fixed on your distant horizon while under him the ship is sinking would be plain barmy.

I agree with most of what you say PDK. The big problem is that the vast majority of people have neither the resources, nor the systemic understanding to be able to change the world they live in or, more importantly, significantly change the way they live. They are literally at the mercy of the politicians. A portion of them are too self absorbed that if they had the resources, they wouldn't change to a positive model, and most are simply not educated enough.

The people we need to change are the politicians. They need to find a way to sell the appropriate platform to the people that puts them in the position to change policy. Expecting it to happen from the ground up will never get sustainable results.

Are you importing supplies, and if so have your air/shipping freight costs gone up?

Yes, importing. Freight costs are up, unsurprising given the reduce opportunity to backload. We are tracking one of the boxes we ordered from a chinese factory about 3 weeks ago. They promised delivery to NZ within approximately normal timeframes and so far it looks like they might achieve it. Our logistics people are giving us increasingly upbeat reports about chinese transport infrastructure freeing up. We are not holding our breath but over the years have found the chinese suppliers to be reliable so it wouldn't surprise us if they deliver again.

That's great to hear, except for the price increase.

Anyone know how many working visas were issued to people working in tourism here? (i.e. I'm assuming those people will leave NZ in the next few months?)

The Globe and Mail reported growing skepticism of the CCP’s claims to have controlled the epidemic, citing health officials who admitted thousands of asymptomatic patients were systematically excluded from the official counts to produce the “zero local infections” figure uncritically repeated by the World Health Organization and many American media outlets. Furthermore, the number of cremated remains returned to grieving families by the authorities this week is noticeably larger than the 3,200 deaths officially admitted by the CCP.

https://www.breitbart.com/national-security/2020/03/27/massive-protest-…

#4 Good to see this mentioned:

Where's the money going? Treasuries, mortgage-backed bonds, foreign currency swap lines to other central banks including the RBNZ , and new liquidity facilities aimed at stabilising money markets and supporting the banks that transact directly with the Fed.

It would be interesting to me if somewhere there was a breakdown of these foreign currency swap lines by currency. I think the Fed is keeping us (and much of the world) on life support. Without them, international trade would have ceased 'before lunchtime'.

I think the Fed is keeping us (and much of the world) on life support. Without them, international trade would have ceased 'before lunchtime'.

Not at all - the Fed has extended collateralised USD swap lines up to $206.051 billion as of close of business on 25/03/20 - Source section 2. Some international inter-bank eurodollar liabilities in the range of ~$50 trillion dwarf this miniscule intervention.

Moreover, the same counterparty global central banks possibly participating in this US gesture of benevolence have ~ $3.34 trillion UST+other securities (small) parked at the Fed which can be liquidated.

The outstanding amounts of FX swaps/forwards and currency swaps stood at $58 trillion at end-December 2016 (Graph 1, left-hand panel). For perspective, this figure approaches that of world GDP ($75 trillion), exceeds that of global portfolio stocks ($44 trillion) or international bank claims ($32 trillion), and is almost triple the value of global trade ($21 trillion).

The outstanding amount has quadrupled since the early 2000s but has grown unevenly (Graph 1, left-hand panel). After tripling in the five years to 2007, it fell back sharply during the GFC, even more than international bank credit. This most likely reflected a reduction in hedging needs, as both trade and asset prices collapsed. Section - The market: a bird's eye view

Thanks for the link! Comparison to the previous release tells the story. Will be interesting to watch that.

With respect to these words of yours: US gesture of benevolence...

Do you mean that sarcastically?

A mild rebuke to your claim:

Without them, international trade would have ceased 'before lunchtime'.

Thanks again - yeah, melodramatic, I agree :-)!

But, I do wonder then why they 'opened the window' to all the additional central banks (including us)? What function does it have (i.e., what's in it for us - what's in it for them)?

It's been open the whole time since GFC1 - you can peruse previous data releases from the page I linked.

These guys aren't even hiding their impotence. Fed announces dollar swaps that were already available this whole time. What, are we supposed to be impressed they cut the price on them by 25 bps?

Nope. The Fed just admitted to the global $ shortage. That's all it did.LinkNot only that, they also admit the $ swaps don't work (we already knew that)

"To increase the swap lines’ effectiveness in providing term liquidity, the foreign central banks with regular U.S. dollar liquidity operations have also agreed to begin offering U.S. dollars weekly..." Link

I wonder what he means by they don't work?

I guess the point is that 'over by lunchtime' (just an expression :-) - but meaning int'l trade will all but cease, letters of credit/dollar transacted trade having completely frozen up) is going to happen no matter what anyone, Fed included, does?

I'm just wondering whether my hunch that we'll find ourselves in the position of needing an economy (hard to say whether we'll call it that) largely reliant on self-sufficiency is pretty much on it or not?

International banks demand increasingly more pristine collateral (sovereign bonds, particularly T Bills ) to meet margin call claims on their counterparties, not more positions that can sustain further margin calls. Central banks need to stop competing for this increasingly rare resource as witnessed in current pricing structures. Central banks need to offer collateral not reserves to alleviate current stress points and then investigate how this situation developed - inevitably this must emanate from Treasury issuance - https://debtmanagement.treasury.govt.nz/

The tipping point for the world's entry into the Great Depression was when the Bank of England and the Federal Reserve admitted that their attempts to maintain the gold standard were failing. A similar tipping point, without the gold standard, could be imminent if the Fed is forced to admit that its actions are not producing desired outcomes.

After Putin and Trump exposed the American Democracy, now Corona is exposing American Efficiency.

Seems everyone here has forgotten who owns the Fed....

Good news in the making;

https://www.zerohedge.com/geopolitical/abbott-labs-unveils-portable-tes…

And another two rapid tests. Henry Schein, and Biomedomics. Amazing what the removal of too-stringent 'testing regulations' can do. Private sector creativity unleashed....

To be sure, both these tests are antigen-based and therefore less accurate. But, in terms of keeping things moving, and given that blood tests are both fast and easily administered, they could at the least show up the real state of infections, and that could serve to dial down the rhetoric of 'The End is Nigh'.....If actual infection rates are 10x the number breathlessly reported every day, then the death rates are 10 times less.....

Serological tests, in general, are well covered in this article from StatNews.

And Pepe Escobar, over at Asia Times, has a blistering indictment of the French collusion with their own Big Pharma to discredit the efficacy of hydroxychloroquine, while all the time sequestering stocks of it for the Elite, and preparing the ground for a more widespread (and vastly more profitable for their Big Pharma) general release in the future.

Raoult was part of a clinical trial that in which hydroxychloroquine and azithromycin healed 90% of Covid-19 cases if they were tested very early. (Early, massive testing is at the heart of the successful South Korean strategy.) Raoult is opposed to the total lockdown of sane individuals and possible carriers – which he considers “medieval,” in an anachronistic sense. He’s in favor of massive testing (which, besides South Korea, was successful in Singapore, Taiwan and Vietnam) and a fast treatment with hydroxychloroquine. Only contaminated individuals should be confined.

RTWT....

Not sure about collusion however, regarding hydroxychloroquine;

“If clinical data confirm the biological results, the novel coronavirus-associated disease will have become one of the simplest and cheapest to treat and prevent among infectious respiratory diseases,” a group of French researchers wrote in a paper published on February 15 in the International Journal of Antimicrobial Agents.

One of the three authors of that article was Didier Raoult, a prominent infectious-disease expert who ran a small clinical trial in France testing hydroxychloroquine in a few dozen COVID-19 patients. It’s one of many clinical studies around the world testing chloroquine or hydroxychloroquine.

Early reports of Raoult’s trial were positive, with Raoult saying chloroquine appeared to shorten the time that people with COVID-19 are infectious.

https://www.sciencedirect.com/science/article/pii/S0924857920300662?via…

https://www.en24.news/a/2020/03/hydroxychloroquine-would-be-effective-a…

Two friends, both self employed just got huge payment from this. Both over 65 one got 7k other 7.5k, both out in rate at 110 hour ,they will only work PT, they put in best weeks they have, both handyman...this just like EQC all over again.. winner's and losers

What's not in lockdown?

Supermarket prices, this last week its 5%, 10% more than 6 months ago, seems so.

https://i.stuff.co.nz/business/120661543/call-for-pricing-probe-as-prim…

Superannuation needs to be income tested and asset tested, included trusts after this.. everyone needs to scarfice after this.. everyone..

My old Cat 112 grader had a scarifier......would that help?

Super cut OK. Make it income tested is a bad idea - it isn't what was promised when they paid their taxes and it will keep accountants happy developing fiddles. Also unfair because some pensioners (eg myself) get a foreign pension and our NZ super is just a make up. Note make up - NZ super is generous by international standards so just cut it now or abandon CPI increases for a few years. Cut it now would be my choice - it is not as if us old timers are actually going anywhere or having parties.

I have been rereading a book published in 2006-Pandemonium, by Andrew Nikiforuk. The Epilogue is titled The next Pandemic. Here are a few short quotes from it; "If the next invader is a kin of the bird flu or H5N1, it will go global in weeks and soon be out of control". " A 2004 report by the CIA's National Intelligence Council predicts that a pandemic in the megacities of the developing world with poor health-care systems could spread with devastating e and derail globalisation".

"In response to a severe pandemic, governments will close borders and reluctantly impose quarantines on the sick. If voluntary quarantines fail, authorities will close schools and universities. They will forbid public gatherings and sporting events. People will fret in their homes and pray for the best" We were warned.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.