As New Zealand prepares for the potential of negative interest rates in 2021, the IMF issued an unusually blunt warning in November that the world was in a “global liquidity trap” where monetary policy was having limited effect.

Chief economist Gita Gopinath pointed out that low inflation and low growth has persisted despite 97% of the advanced economies having policy interest rates below 1% and one-fifth of the world with negative rates. In this situation further interest rate cuts will do little to stimulate growth and the only way forward is a coordinated global effort to focus on large government spending programmes rather than monetary stimulus.

Persistently low growth

There were already signs prior to the pandemic that the prevailing economic policy was not working. In October last year the former governor of the Bank of England Mervyn King argued that the world’s advanced countries had failed to address the structural problems which had led to the global financial crisis. As a result they had been stuck in a low growth trap ever since then. Too much borrowing plus too little spending and investing meant the standard economic models were no longer effective.

Indebted demand

In a recent paper economists Atif Mian (Princeton University), Ludwig Straub (Harvard University), and Amir Sufi (University of Chicago) proposed a theory of “indebted demand” to describe the situation the global economy finds itself in.

Looking at data from a group of advanced countries1 including New Zealand, they conclude that since the 1980s, economic growth, investment to GDP ratios, business productivity and inflation has all declined. Meanwhile the average real interest rate in these economies has dropped from 6% to less than zero. The COVID-crisis is likely to accelerate these trends.

Mian, Straub and Sufi argue that since the Global Financial Crisis the top 1% have been saving at an increasing rate resulting in a huge accumulation of income and wealth. At the same time there has been an explosion in borrowing from the bottom 90%. This imbalance has led to a permanent transfer of wealth in the form of debt service payments from borrowers to savers, depressing demand even further.

Low interest rates had worked for a while in propping up demand, but once interest rates hit their lower bound it is impossible to encourage the bottom 90% to consume more. Once interest rates moves close to or below zero, the economy finds itself in a debt-driven liquidity trap which is hard to escape from.

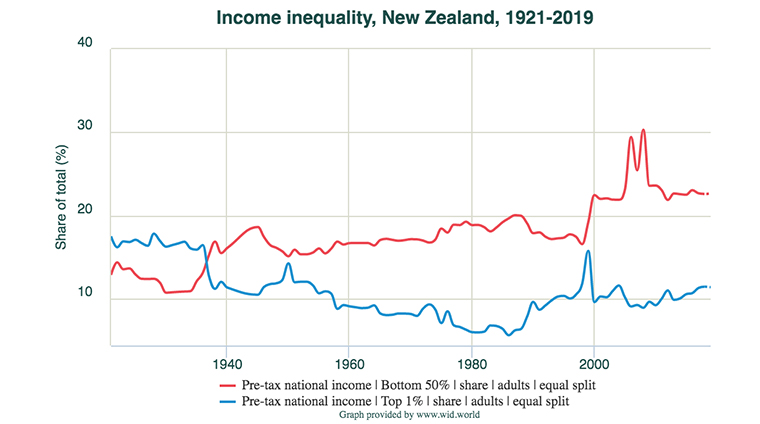

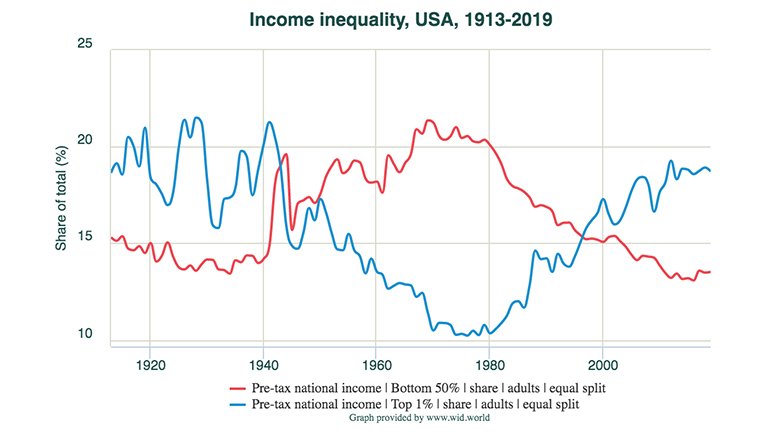

Debt and income share in New Zealand

While the top 1% of income earners in New Zealand have gained a larger percentage of the total income pie over the last decade, at 11% income share we are still a long way from the levels of inequality in the USA where the top 1% account for almost 20% of the income share:

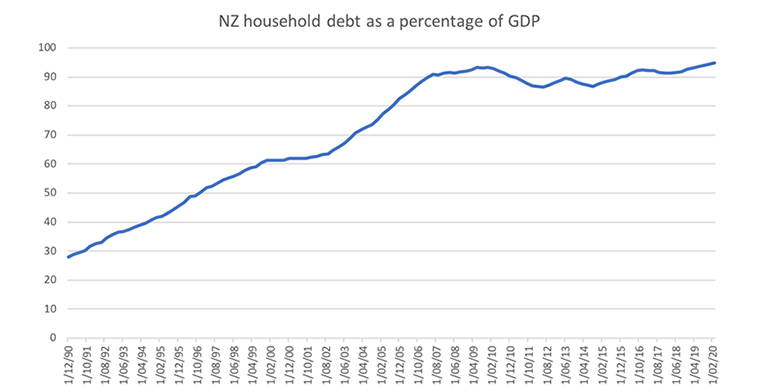

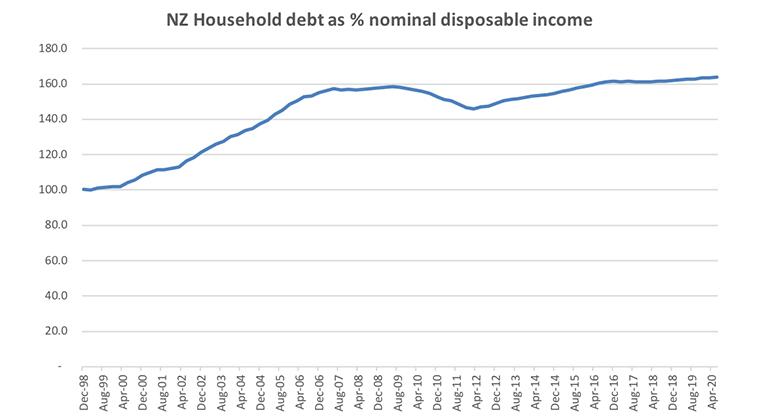

However New Zealand does have some of the highest levels of household debt in the world (currently 14th of the OECD countries), even before the pandemic struck. Most of this is mortgage debt due to the high cost of housing.

Data source: Bank of International Settlements

Data Source: RBNZ

Household borrowing declined slightly post 2008, but since then it has resumed its march upwards.

The 2020 pandemic and recession has only exacerbated the situation by disproportionately hitting low-income workers who tend to have less savings and more debt. All of this points to deflationary pressures which impact the debt-burdened the most.

The solutions to the liquidity-trap are tricky when there is a need to stimulate growth without sending households deeper into debt. The UK escaped a liquidity trap in the 1930s through a combination of cheap money combined with a house building boom. Mian, Straub and Sufi conclude the only solution is to redistribute funds away from the top 1% through things like wealth taxes, raising top marginal income tax rates and inheritance taxes.

Whatever the answer, the continued imbalance of debt, saving and investment are clearly not sustainable in the long run and more radical approaches will be required to avoid a level of inequality that will ultimately affect everyone.

1. The countries in the sample examined by “Indebted Demand” authors were Australia, Canada, Finland, France, Germany, Italy, Japan, New Zealand, Norway, Portugal, Spain, Sweden, United States and United Kingdom.

*Alison Brook is from the Knowledge Exchange Hub at the Massey University campus at Albany, Auckland. She is on the GDPLive team. This article is a post from the GDPLive blog, and is here with permission. The New Zealand GDPLive resource can also be accessed here.

31 Comments

75 years since Bretton Woods and that is the typical length of any monetary system. Might be time for a war and restructuring of the global financial system - probably in Chinas favour.

75 years of levering (at exponentially-increasing rates) off a one-off energy bonanza.

And we picked the low-hanging fruit (best EROEI) first.

We are on the way down, leaving more maintenance-requiring balls in the air that were ever built. The divergence has been expressed in flat-lining 'productivity', increasing debt-to-GDP ratios and increased forward bets held (in the face of never less remaining underwrite).

Numbers of economists who understand the problem? Soddy, Keen, Daly, Georgescu-Roegen, and I've run out..........

Number of economists who get it in NZ? One. And (I stand to be challenged :) not at Massey.

The way I see it, we shouldn't be complaining about debt down here in NZ. Debt, migration and selling local assets to foreign buyers funds our first-world lifestyle without having the wages and industries to show for all of that.

I doubt this country has what it takes to put in the careful planning and hard work to actually build productive industries?

We at least had decent living standards until about a decade ago and we couldn't help ourselves but scrape the bottom of the migrant barrel to turn a quick buck, and in the process destroyed the only good thing going for us.

We have phenomenal living standards by almost any stretch of the imagination, but I agree not like it was a generation ago. I've travelled through some pretty crap places and NZ offers: clean drinking water, sewerage systems that work, universal vaccination which is free (whether you accept is another matter), free primary-secondary education, a socialised health care system that will fix a broken leg, stent your coronary artery and subsidise your asthma inhaler. Not working? No problem, you'll get a pittance but you won't starve. Anyone starved to death or died of cholera in Aotearoa? Kiwis need to get used to living in a caravan park if they don't have some skills to fall back on, and make smarter decisions. Christ, if you want to hang with Bruce the local bikey and have 4 kids whilst puffing on your pipe, you don't deserve anymore.

We just need a good recession, the best wealth redistributor there is, better than any gubmint policy anyway.

Ie only solution is for bottom 90% to be given more of the pie, so they can spend it.

Which for 45 years, most OECD governments have been doing nothing to bring about, in fact quite the opposite.

Debt is not a substitute for wages in the end analysis.

The opportunity was there with helicopter money. Those in charge chose to deliberately head to the wealth effect from more housing debt.

That obviously means you are wrong.

As am I and many others commenting on this site.

As a non asset owner and older age I'm at a loss to know where to go from here. Jiin the crowd due to fomo? To late I fear. Believe it will inevitably correct? If I'm wrong I'm screwed if I'm right I'm screwed.

You could learn a bit of wood or metal working and go into the gallows making business? Or perhaps rope making is easier. Although easier again to just use cheap chinese stuff, what is that saying about on hoist their own petard?

Much like Marie Antoinette didn't create the conditions sparking all the those wood and metal work craftsmen crying "vive la révolution". She just happened to be in power when the music stopped, holding her head high with the righteous hubris of power, authority, and past successes, never thinking there was need to fix the core problem itself...

"only solution is for bottom 90% to be given more of the pie, so they can spend it."

Which would DECIMATE resource bases

Its environment OR the economy in the end

Yes. The only question is: At what level of resource-consumption do you want to live?

Then you set the time period - say seven generations hence they should have the same resource options we do now.

Then you can work out your optimum population.

Note I didn't quote a banker or an economist, to reach that conclusion.

If there is an infinite amount of money that can be created from a few taps of a keyboard, then there is an infinite amount of debt we can take on - you just need appropriate policy to create hunger and willingness for the masses to take it on.

I agree there is no limit on the debt in the system, its just numbers in a computer these days and is no longer backed by anything physical like gold so its physically limitless. The limit is what the punters want to take on, which essentially then effects their lifestyle and quality of life, this is the limit. if the wealth continues to flow to the rich then there is obviously a breaking point. The rich cannot see the problem, therefore the only outcome is war in an attempt to restore balance.

Thanks Alison, great article highlighting much of the global macroeconomic driving forces that will shape out future.

Unreal only 2 comments, everyone busy writing on the property articles while missing what is really going on...

People seem to be completely missing the macro picture we find ourselves in. This only happens once every 75-100 years...usually it results in war and debt restructuring (and a new reserve currency).

Howe Strauss were right on the money back in 97. https://en.wikipedia.org/wiki/Strauss%E2%80%93Howe_generational_theory

Property brings it down to a rational, personal level, so I get that.

40% of your income for the next 30 years, minimum. Assuming you can maintain your earnings and maintain your job - to keep a roof over your head for your family. Probably 40% of your partner's wages as well.

Throw in 12% of your wages for a while to clear a student loan.

Once you account for tax, food and housing for your family unit, there's not enough left over - so stimulus has to flow from debt. And that's before you think about your retirement, and who is paying for that (hint: you are, you probably just don't know it yet).

your mortgage declines, your income goes up. Repayments don't stay at 40% of your income. My first house took $2k/month IIRC, approx 9% on 250k loan. My net was 4 k. I lived on about 4-500 and paid EVERYTHING else on principal. Then got a 2nd job to pay even more. If I had the same mortgage 20 yrs later, it would be around a 1/5th of net. Smashing the principal early is the key. I used to spend hours playing with financial calculators, realizing the $4 beer in Ponsonby was actually costing me double due to interest on my mortgage vs paying extra principal down. This was th trigger to stop drinking, eating out and generally being a consumer. I'll take all the hate people want to dish out, but if you want to get ahead -you have to sacrifice. Constantly I hear whiners about housing costs who still spend like they are freehold lawyers. FFS

For context, I'm at $2.2K/month on a $500K loan at sub 4% bare minimum on a modest 3 bedroom home 20km+ out of the CBD. I think the key here is that people are waiting longer to buy homes, so are closer to their incomes tapping out so are servicing bigger debts on what is probably approaching their max earnings, and have less time before things like families etc become a question of now or never. And young people seem to be saving more and spending less than previous generations, but the reality is many are coming off wages which might have been comfortable once, but haven't moved much in a decade or more. It won't take much of a % rise in interest rates to put many on the back foot.

As for the $4 beers, where can I sign up? :)

OK boomer, so where is this inflation thats going to drive incomes up in relation to debt? WE have inflation only for assets and it has driven price to income to such insane ratios no ones going to make a dent in the principal by skipping a few meals.

Born in 1966 ? born in 1967 and basically did the same. The focus was to pay the mortgage off in 15 years and you really need to smash it early on as $50 now was saving you $50 later on on interest rates at the time. Its a totally different mindset that has unfortunately all but disappeared in the current generation.

Peak Debt... indeed

now where have i heard that before

https://ourfiniteworld.com/2020/11/09/energy-is-the-economy-shrinkage-i…

Excellent article, thanks. “A global liquidity trap where monetary policy was having limited effect" and "the standard economic models no longer effective". Yet the "solution" was not to let new facts get in the way of models. Sacrosanct, they be. After all, slamming rates down and QE up "should" have worked. If this was 2008.

But with rates already artificially low, even lower rates no longer work that way. Massive more debt piled up, yet progressively less went into productive assets that actually grow the economy. Instead, S&P500 and housing booms, in a recession, a clue, maybe?

For years, Govts and c/banks have been like the pilot of a plane in a vertical climb, but the air's now so thin even us plebeians have started to notice the engines hardly give any thrust anymore. Yet the high priests' answer is to keep wishing away the thin air and near-empty gas tank, keep it pointed up and the throttle wide open, just like their incantations (sorry, models) say. What could possibly go wrong...

Personally, currently unsure and questioning what a post-Covid (widespread use of vaccine, few cases of Covid, open borders) economy is going to look like.

How harsh and for how long will actions be addressing debt and other issues such as housing affordability?

If fact, a little unsure what will those actions are likely to be and their implications regarding cash and assets?

It seems that for the next six months at least we are going to have continuing policies of low interest rates and QE and FLP that will maintain current upside on asset prices.

However, personally I think likely it can't continue being the same old, same old as for the past decade which has only been more intense this year due to Covid.

I don't feel that the actions of the past decade are sustainable but the uncertainty makes it difficult to plan for the longer term.

Will cash rather than assets become the better option? For instance, should one be looking to sell that investment property within the next year as house prices flatten long term or have a slight correction?

That's going to be the interesting thing. I assume more people have a heightened awareness of the current housing crisis and struggling global economy than in more normal times, so what will happen when it appears the music is about to slow or stop? Increased market volatility? Will there be a rush for the exits to capitalise on gains in the housing market?

However long the 'tough times' last (when or if we eventually do have really tough times as a result of Covids fallout) it will most likely be followed by a large property boom as we emerge from it.

Thanks Alison for the good read as usual.

Of particular interest is this "Mian, Straub and Sufi conclude the only solution is to redistribute funds away from the top 1% through things like wealth taxes, raising top marginal income tax rates and inheritance taxes."

Shame we don't have at least a small % inheritance tax (estate duty) anymore imo.

If we did it would also help to include the potential loopholes like family trusts or offshore wealth.

Don't forsee any risk of the New Zealand Government implementing these policies and neither do financial markets or retail banks wouldn't be offering such low fixed rate mortgages.

We are far away from that peak Alison, good time ahead still. Right now, what we see just worry some parents because their $ prudency in the past, is differ to the new norm of today. So, that's about it really - we must keep this good momentum up for the party to keep on going. The next 6 years, if JA still at the helm, the guarantee of no CGT is a definite relief.. What I'm still unsure is this, last time she said no CGT as long as she's the PM in the previous govt. that in bed with NZFirst, to satisfy the partner. Now, she's rightfully exercise a new statement as a majority party leader that form the govt. - So, to all - Be quick you all got about until mid next year/2021 to buy/leverage more - the more of participants? the more likelihood of govt. sovereign bail out in case things go custard - take bull by the horn, strike the iron while it hot, 'No Regerts!'

Surely the fact we are effectively at zero interest rates confirms we have reached peak debt

I don't think so but its getting close and the boom in the property market is possibly the last gasp before your average Joe goes underwater. The bigger problem is the worlds increasing population and reducing resources on a finite planet that nobody wants to address. Essentially all our serious problems are caused by to many people. What would be interesting is if the best and brightest individuals in the world crunched the numbers and came up with the maximum number of people on this planet for sustainable quality life going forward. You don't need to be genius to know we have already got to many on the planet right now. If we don't begin to control it then it will self limit through starvation and disease which will be really really ugly.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.