By Brendon Harre*

“We might make mistakes but we will make other things too”– Michael Joseph Savage

$170 a week for a converted sunroom (note the brick walls), in a flat with seven other people in Wellington. In Austria the average rent of a social house is $177 per week.

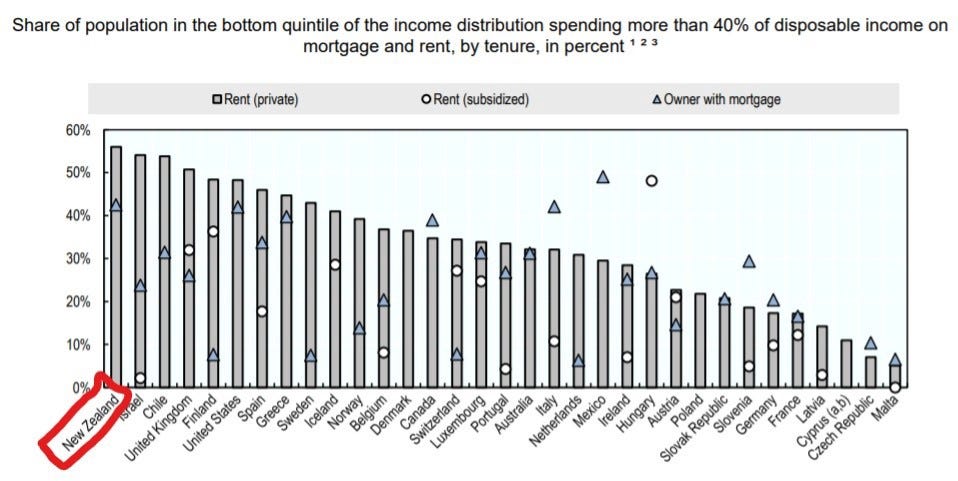

Renting in New Zealand is bad. The bottom 20 per cent of income earners spend a greater proportion of their income on rent than anywhere else in the OECD. For many decades New Zealand’s housing market has failed low-income earners due to rents inflating faster than wages.

For the bottom 20 per cent of households by income, housing costs as a proportion of income have increased from 29 per cent to 51 per cent since 1988.

Source OECD -Affordable Housing Database, Figure HC1.2.3.

Too much of New Zealand’s economy is rack-rent, where those with market power exploit those without. Effectively, wages are confiscated.

Rack-rent is described in Winston Churchill’s 1909 speech about land value taxes. Churchill spoke about a bridge over the River Thames that gave a poor neighbourhood access to work in London. The bridge was tolled, but in an act of civil kindness the toll was removed. However, the workers did not benefit because rents rose by the amount the toll fell.

Rack-renting is a problem for the Covid economic recovery because the stimulus is not evenly distributed across ‘the team of 5-million’. The biggest stimulus — $128 billion of nearly interest-free credit provided by the Reserve Bank — is giving the ‘haves’ a wealth-effect of lower mortgage interest payments and higher property values, while the ‘have-nots’ are still experiencing rents inflating faster than wages.

This raises the question: how much kindness does New Zealand give to the essential workers who did the hard yards during the Covid lockdowns? Not much is the answer if they are low-income workers — like cleaners or supermarket employees — living in rental accommodation.

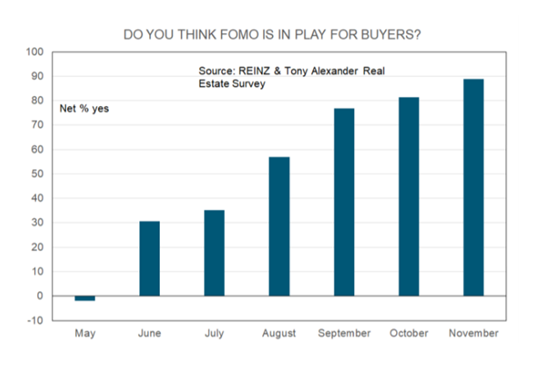

Landlords are not passing on their lower costs to tenants. Instead, property investors are going on a buying spree. Reserve Bank figures show the share of house buying by landlords with high loan-to-value ratio (LVR) borrowing doubled to 16% in the period between the removal of LVR rules in May and the end of October (H/T Bernard Hickey). House prices are rising as a result. First home buyers (FHB) with a fear of missing out (FOMO) are adding to the demand effect.

/p>

/p>

Source: REINZ & Tony Alexander Real Estate Survey — November 2020

As former Finance Minister Michael Cullen says in his paper titled Time for a Monetary Policy Rethink the ladder between the haves and have-nots is getting additional rungs at the top while the rungs at the bottom are being removed.

Political commentator Ben Thomas is correct to state the reason that housing “is so visceral is that it represents a fundamental break from the middle class egalitarian creation story of New Zealand (and elsewhere) — you can work hard, value education, and — even if you have a humble life — you can give your kids something better”.

What to do?

The government needs to define what its housing affordability goal is. Is it aiding the sons and daughters of the middle class into homeownership? Or is it ensuring the powerless can make gains without being exploited by the powerful?

In practical terms, is the goal returning the median house price to median income ratio back to three to four, so more first home buyers can afford a home? Or is the goal returning rent as a proportion of income back under 30 per cent for the bottom 20 per cent of households by income so that the high cost of rent does not cause those households to suffer poverty — something which is recorded far too frequently in New Zealand’s statistics. Both of these housing targets were in the affordable range up until the 1990s, and since then both have become steadily worse.

Former Prime Minister John Key seemed to have restoring the middle class home ownership dream in mind when he called the RMA a “self-imposed straitjacket” that needed reform in his 2002 maiden speech to Parliament and in his 2007 speech to the National Party Conference where he outlined a housing affordability plan.

The problem with fixing housing affordability for middle-income earners is the goal is defeated from the get-go.

For New Zealand to restore median house prices back to three to four would require house prices to roughly halve. In other words, to give the ‘future middle class’ the opportunity of home ownership requires much of the stored asset wealth of the ‘current middle class’ to be destroyed. No prime minister or finance minister in the modern era, at least since Helen Clark and Michael Cullen, has been willing to publicly announce that is their intent. This includes John Key and, of course, Jacinda Ardern. Yet they both campaigned on housing affordability prior to becoming prime minister.

I cannot find any evidence from around the world that restoring housing affordability for middle-income first home buyers in the way that it is talked about in New Zealand is possible. It might have occurred in Japan after their 1980s property bubble. But it wasn’t an explicit policy agenda as is demanded in New Zealand.

Current Labour Party Prime Minister Jacinda Ardern has long had a picture of the first Labour Party Prime Minister Michael Joseph Savage in her various Parliamentary offices.

Yet there is plenty of evidence that it is possible to restore housing affordability for low-income households if the government builds a good proportion of new housing stock (about a quarter or more) as affordable housing (affordable rentals and progressive home ownership houses) targeting a wide band of low-to-middle-income households in schemes that prevent speculative capital gains. New Zealand under Michael Joseph Savage did it in the 1930s and 40s. Austria has been doing it for nearly a century and Singapore has done it since WW2.

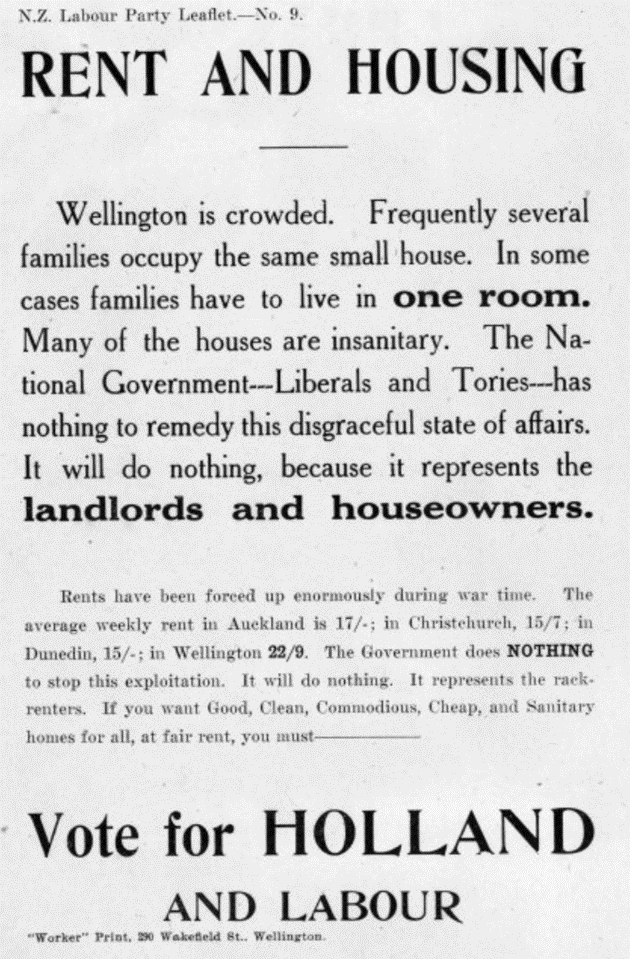

In the 1920s, after WW1, New Zealand experienced a housing crisis, especially once the Great Depression halted villa-suburb building. Rents were inflating and housing conditions were poor. The newly formed Labour Party campaigned to fix this housing situation.

Note the mention of rack-renters in the final paragraph: “The Government does nothing to stop this exploitation. It will do nothing. It represents the rack-renters. If you want Good, Clean, Commodious, Cheap, and Sanitary homes for all, at fair rent, you must — Vote… Labour

The Labour Party came into power in 1935. The next year it started a large, broad-based state house build programme that targeted not just the destitute but also low-income workers. By 1940, state land development programmes accounted for 45 per cent of all housing construction in New Zealand.

The first Labour government (1935 to 49) built 30,000 state houses over about a 10-year period once the construction stoppage of WW2 is accounted for. It took four years to ramp up — by 1939, 5000 state homes had been built. New Zealand’s population at the time was about a third of what it is now.

This historic policy agenda should be a lesson for the current government and the Reserve Bank. In 1936, the Reserve Bank provided credit with interest rates as low as now. This meant the government could fund infrastructure and its house building programme — this connected monetary policy with the real economy, thus aiding economic recovery.

Despite the government undertaking a large housing supply programme, targeting rental house affordability, there is no evidence this negatively affected the asset wealth of the 1930s middle class — something our current political leaders fear doing. And the 1930s monetary policy stimulus did not cause the inequality effects that New Zealand is currently experiencing.

This monetary/fiscal spending effect wasn’t a one-off or unique to a certain time and place in New Zealand’s history. The UK also successfully used housing construction and infrastructure provision (the expansion of the London Underground, for example) as a link between monetary stimulus and the real economy. It escaped a liquidity trap in the 1930s through a combination of cheap money combined with a house building boom.

This approach could be used now. The IMF issued an unusually blunt warning in November that the world was in a “global liquidity trap” where monetary policy was having limited effect. In this situation the advice from the IMF is further interest rate cuts will do little to stimulate growth and the only way forward is a coordinated global effort focusing on large government spending programmes rather than monetary stimulus.

The current Labour government would also do well to learn the lessons from the failure of KiwiBuild. The policy failed because the government committed too little capital and the goal was to aid middle-income earners into home-ownership rather than low-income earners into good quality yet affordable rental accommodation. Unfortunately, the numbers for KiwiBuild did not stack up.

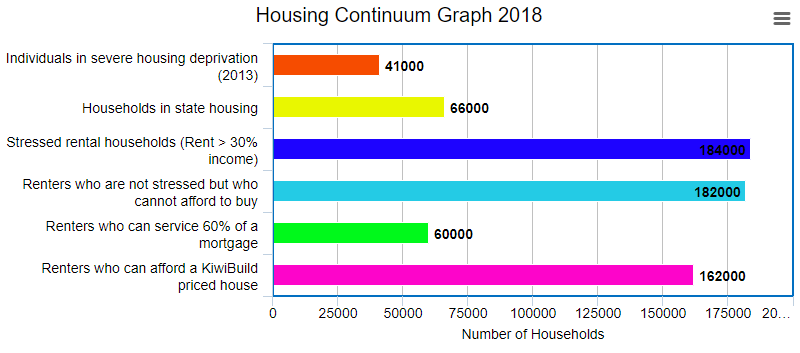

The Ministry of Housing and Urban Development’s (MHUD) 2019 assessment of first home buyer demand showed only 162,000 out of 588,000 rental households had the financial means to purchase a KiwiBuild priced home (see graph below). Of course, the number who would actually consider buying a KiwiBuild home would be much smaller due to various non-financial or personal reasons.

Source -MHUD Information on First Home Buyer Demand 5 July 2019. Note the house prices the KiwiBuild financial calculation is based on averages at $615,000 in Auckland and $425,000 in the rest of New Zealand. It also assumes a 15% deposit and 85% mortgage.

If it was properly configured, a government build programme could supply the rate of house building promised — 10,000 houses a year. New Zealand governments have built at that per capita rate in the past. Singapore and Austria do it now. The problem — specific to the proposed KiwiBuild pipeline, but not to government build programmes in general — was a lack of demand to buy even a small number of KiwiBuild homes. Since the start of the build programme in 2018 only 955 KiwiBuild houses have been successfully sold.

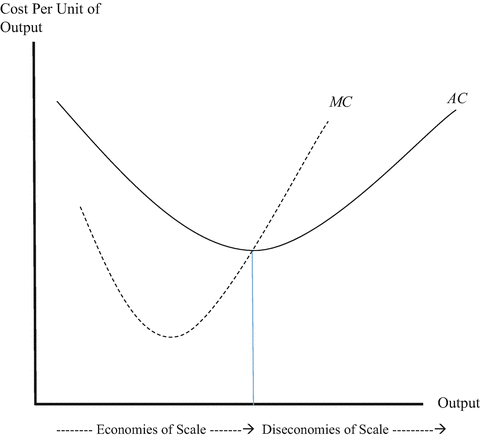

Lack of demand was fatal for the KiwiBuild scheme because its internal logic was reliant on building at scale. Creating more affordable housing types via investment in innovation, standardisation, specialisation, economies of scale, prefabrication, more and larger competitive construction firms, integrating housing with transport, using land more efficiently by building a range of housing types/sizes, improved land assembly and master planning — these all suffered because the lack of demand generated insufficient scale.

This meant per unit housing costs could not be reduced.

Overall, the problems KiwiBuild encountered means it is a failed experiment in restoring housing affordability for middle-income earners.

If the government had invested more capital in KiwiBuild they could have increased the build rate into the economies of scale part of the production system. But that would have meant significantly subsidising build-to-own KiwiBuild houses. This would have caused all sorts of problems that providing capital subsidies for social housing does not face because the rental housing sector is already subsidised.

Switching government housing support from being income based (the Accommodation Supplement etc.) to being capital grant based would be a significant shift; it would take time, but it is a viable option. New Zealand has run that sort of system before. Other countries like Austria have very well developed systems for issuing housing capital grants to their social housing sector — something that has architectural, economic, social and environmental advantages.

I have no doubt that improving housing supply by way of reforming the RMA and infrastructure financing can help maintain housing affordability. New Zealand from the 1950s to the 1990s had relatively affordable housing due to private sector developers being mostly free in how they built New Zealand towns and cities — mainly outwards (the Kiwi dream of a quarter-acre pavlova paradise as John Key described it in his 2007 speech). Other cities around the world — in the US, Germany, Japan and so on — are affordable because housing supply responds to demand.

I am less convinced housing supply can quickly restore housing affordability to middle-income first home buyers. No prime minister or finance minister will publicly support that course of action. Without their full support, interventions will always be half-hearted. Proposed housing accords cannot be undertaken. There can be no common cause.

With the prime minister’s hands effectively tied, action on housing inevitably degenerates into the various involved parties acting at cross-purposes to each other, blame-shifting and finger-pointing. We have already seen this with the finance minister and Reserve Bank Governor.

The better course for the prime minister would be to acknowledge political reality — housing affordability in New Zealand cannot be resolved by addressing middle-income needs first.

Politically, that might seem unpalatable. Being a centrist, the prime minister may have a vague contention that she should deliver housing affordability to middle class swing voters. Hopefully it is becoming clear to her that this is not possible — at least not in one electoral cycle, or even several.

This means housing affordability inequality should be addressed as the highest priority. The prime minister should state that the government’s housing goal is to get rent as a percentage of income below 30 per cent for the most vulnerable socio-economic groups, and that this target is what her government will aim to achieve first.

If housing inequality becomes the clearly articulated priority, it creates a common cause. A housing accord is possible. Actions from the various parties can be aligned and progress can be made without it being undermined by finger-pointing.

Over time, after a decade or two of government-led house building, the median house price relative to median income ratio may stabalise back to affordable levels. In the meantime, progress will be made by reducing housing inequality.

In the past, the Savage Labour government built state houses for the lower end of the housing continuum (see the below two videos). It was this house building effort that provided the foundation for the Kiwi housing dream of the 1950s through to the 1990s. New Zealand’s most successful housing policy agenda achieved its success by focusing on helping lower-income households first.

To re-establish the Kiwi home owning dream may require Jacinda Ardern to look at her photo of Savage and think: ‘what would Michael do?’

This is a repost of an article here. It is here with permission.

208 Comments

I really dont understand why the government is allowing the RBNZ to print money which is been used to overinflate the existing housing market and not instead using that money to instead build state houses with a design either to rent to own or just rent. In the 1960's when my grandparents moved from England to Sydney (Australia) they participated in the "rent to own" scheme for state housing in Sydney, at that time there were two options offered either rent to own or rent and the house goes back to the government at the end of the day. The scheme developed new Sydney suburbs, created employment and gave the bottom quartile - hope. We know that home ownership ensures people get a step up in life and can begin to build wealth, creating a base for the next generation and breaking the intergenerational poverty cycle. Isnt it time for Labour to stop talking about fixing poverty and actually start to do something about it. The government would also be well advised to look over the ditch to what Australia is doing at "closing the gap" with Aboriginal home ownership- a similar program to that in the 1960's is in place and by all accounts very successful at ensuing home ownership can be for everyone. http://www.dhw.wa.gov.au/housingoptions/homeownershipoptions/KeyStart/D….

"I really dont understand why the government is allowing the RBNZ to print money which is been used to overinflate the existing housing market .."

Because THE GOVERNMENT WANT HOUSE PRICES TO INCREASE.

Hope that helped.

..only 3 thumbs at 12.24 and this is the most correct comment of the day.

It may be the most correct but it's also the most obvious and it is not what is needed.

The Truth will Set YOU FREEeeee EEEE eeeeeeee :)

..tell us what's needed then eh fritz? You think anyone actually gives a rats a### what gets bleated about here?

Because if house prices fall we have a severe recession/depression on our hands and politically that is of course very bad. Kick the can for the next government seems to be the way to go.

Because if house prices fall we have a severe recession/depression ..

That's a tired old line. Capitalism is based on good businesses driving out bad. Wealth is like nature, it's always moving towards new life - think about that some before replying.

Not sure if a persons life would be long enough to!

I agree with you, but just saying that governments will do what they can to avoid a recession these days, thinking that is a good thing do so - but as you point out, in reality it can be bad (as you end up with zombie companies etc)

Nothing tired about that comment.

" Debt capitalism" is the modern form of capitalism.

It requires a continuing level of credit growth.

In nz most of that credit growth is in the household sector.

Maybe debt is the antithesis of weath... In nature , death and decay. ... Rather than a movement towards life.

Historically, the financial crises that spill over into economic downturns, are generally real estate related.

Debt is someone else’s paper asset

Except of course a massive government house building programme doesn't cause a severe recession/depression if it targets the bottom end of the housing continuum and if the houses are not immediately sold into the wider housing market. Housing building booms are very stimulatory to the economy. For Savage it helped escape the depression - it didn't cause one.

Ok lets build away then..

This statement doesn't hold together, prices can and should go down and its effect in the economy will have both positive and negative sides, while some people will end up with negative equity others will be able to afford a home and we will be able to alleviate many social and health issues.

How far into negative equity will the banks allow people to go? Banks will default if enough house holds go under. Banks that are under default pressure don't lend, then companies don't employ people, if companies don't employ people, more people default on rents and mortgages - and the vicious cycle repeats. I don't see how prices can fall without a severe recession or even depression - there's too much debt. There would have to be massive debt defaults and restructuring in a short amount of time - high unemployment, then hope like hell that companies can suddenly start new projects and employ people - but that is all based upon confidence in the future - and that is what bank lending is - a confidence that people will be able to remain true to their contract and pay the mortgage. If that confidence isn't there - you get stuck in a depression.

This is not true, as long as households can still afford paying their mortgages even if it is under negative equity banks should be fine. Probably the only way banks can stop people from going into negative equity is not lending into hyperinflated bubble prices in the first place, by doing so they are taking a big risk for very little interest.

A recession or depression is what is most likely to occur probably in 2021 caused by the debt load exacerbated by Covid 19 and the increasing divisiveness within and between countries. This may of itself reduce asset values, possibly significantly and the knock on effect of financial institutions will be devastating which may prevent a speedy recovery so a very uncertain future lies ahead and I do wonder if today's situation is similar to that pertaining at the time of the French revolution and if the fix will be similar?

Our Great government builds state houses and turns the occupants into tenants for life ... cementing poverty when generation after generation relies on handouts

Quite the opposite - my grandparents got a state house in the forties that they were later able to buy off the government. That opportunity was a springboard for three generations (and counting) of financial wellbeing. State housing can give people the social and financial stability they need to build generational security, if done right.

The Austrian social housing model has a provision where tenants can provide 5% equity and this gives them the right to buy after 10 years. In Austria they also have a government subsidised savings account which they can use to save for this equity contribution. NZ should allow this tenant equity/right to buy provision with an expanded social house build programme. KiwiSaver should be allowed to be used for the equity contribution.

Exactly. It shows a stunning lack of self-awareness for generations who benefited from affordable housing created through such efforts by the post-war generations and who have enjoyed wealth as a result to be lambasting such an approach. Although mass building of houses would obviously conflict with folks' feelings of entitlement to free money from their property(s).

(Unless - more unlikely - it's incredibly self-aware and they're aware they've received incredible amounts of wealth from state efforts then and more recently and simply don't want others to have the same.)

"That opportunity was a springboard for three generations (and counting) of financial wellbeing. State housing can give people the social and financial stability they need to build generational security, if done right."

Precisely... I don't know why you said "opposite". The Labour govt mostly does not sell SH and doing so dooms generations when they could enhance generations as you described. The Labour govt has the power to make a difference to poverty but instead mouth trite promises.

I thought you were objecting to State housing in general. Looks like we're actually on the same page.

Aweaome. What I dislike are SH ghettos. Cars dogs drugs and neglect. I am in favor of people being helped into a home and then they assume responsibility from there... that changes mindsets and is better for everyone. Another thing I hate is a family in a SH whose entire family all end up on bennies and with SH of their own. After all SH should have a limited time and not be for life. Agree?

The prime minister should state that the government’s housing goal is to get rent as a percentage of income below 30 per cent for the most vulnerable socio-economic groups, and that this target is what her government will aim to achieve first.

An excellent article supported by exactly the data we should be focusing on. Rents are at the core of our housing affordability problem. Address rents, specifically for the lower quartile of households incomes, and the crisis will abate.

I'd love to see Brendon do the same kind of consideration regarding rent controls, as a means to address the problem whilst ramping up of state house building. Rent controls would provide immediate relief which is so desperately needed. If we don't go down the #rentcontrolnow track - we end up with more subsidies and higher welfare benefits.

#rentcontrolnow

Kate are you going to take this further - petition, protest, FB group?

Yep, just tidying up a few bits and pieces at work and will then get onto the necessary research in order to firm up on a rent maxima formula proposition on a regional basis. Will then circulate the idea to targeted NGOs who have the logistical capacity to organise petitions and protests - and at the same time, I'll personally get onto local (LGNZ) and central government (Ministers and my MP).

In the period 1980-2000 the benchmark for property investing for rentals was a 6% gross rental yield before rates, insurance, interest and maintenance with a net yield of 3%. From published reports we have seen that property prices have increased 40% over the last 3 years while rents have increased by only 25% over the same period. Thus, there is serious compression on rents. Many of the examples you have given over the past week suggest gross rent yields are now down around 2%. For some of the dumps in Auckland now selling for $1 million, a gross rent yield of 6% would require $60,000 or $1,150 per week which is just not going to happen. Which tells you that investors are investing in Capital Gain. (rough and ready)

Kate, you seem smart and motivated - but rent controls on private landlords are not the solution. Someone gave Vienna as an example but it was totally different to your proposal (the state owns 58% of rentals for a start).

How many commenters here want to buy a residential property in the current market at current levels? I suspect some do want to buy, but at lower levels - so you are in denial. For those who want to buy their first place, maybe some form of government assistance or guarantee to the bank for the first 20% of the property value?

What about capitalisation of 10 years of Accommodation Supplement for NZ born FHB's

In my humble opinion, the single biggest enabler of wealth inequality is the lack of access to finance. Those who can access mortgages at competitive rates are far more likely to be able to get on the housing ladder today and assist their children in the future. This is where the state can play a role to make a difference and break the cycle.

Having said that, the buyer still has to step up to the commitment.

At the moment it seems that a bigger driver of wealth inequality has been the Reserve Bank's monetary policy devaluing wages and savings and transferring that value to asset holders. A straight wealth transfer.

This is where my idea about state funded Kiwisaver comes in. Breaking the cycle of wealth poverty for anyone who can't do it themselves.

By now anyone who joined Kiwisaver in 2010 - in a sensible fund - would have accumulated at least 40-50k each. (circa 100 per month per person investment). These families are stuck renting many to a house remember. Multiply that out and you get a useful amount of money.

It is the only idea I've heard of which would actually lift people out of poverty. _Not_ Income poverty, the myriad of benefits need to cover that. This is about increasing wealth and giving families a future and the possibility of owning their own home. Wealth is the key, but everyone talks about income.

The problem is that everyone involved is panicking and are stuck in ultra short term thinking. They aren't looking past the end of the week, just like the people they are trying to help.

More importantly, how many investors are going to want to build any new rentals knowing that it will be decades before they get to see a return on that investment? Building would literally dry up overnight. Which is exactly what happened overseas. Have we learnt nothing? You don't solve a housing shortage by creating an even bigger shortage. You solve a rental housing shortage by incentivising investors to build houses, or home owners to rent their homes out instead of selling them. Basically the opposite of current policies, which is why there is a housing shortage in the first place.

Yes KW.

We have a sovereign wealth fund that invests in and pays fee's to offshore hedge funds/PE when we are crying out for long-term housing investment here in NZ. Large scale housing initiatives are exactly what is required and which will provide long-dated annuity style rental income. They could be sold to pension funds with strict rental conditions. These are the sort of initiatives that provide decent quality long-term rental accom in Europe.

Market forces will prevent rents exceeding ability to pay.

If government hands out subsidies/benefits... they might as well own the house

KW.. so what % of investors build new houses in order to rent them out as opposed to buying existing stock. As I am sure you are aware it must be a very small number. You could of course fudge the figures by including apartments but let's face it, investors seldom build houses to rent out.

To Kooti, not sure what you mean by 'in denial' - denial about what? Do you mean to say that buy-to-let investors aren't active presently? I think the evidence suggests otherwise;

The $1.9 billion borrowed by investors last month was the highest amount by this grouping since July 2016. And July 2016 is significant - since that's when the RBNZ clapped tough minimum deposit requirements on the investors, slowing them down.

https://www.interest.co.nz/property/108125/latest-reserve-bank-monthly-…

Completely agree. Anyone entering the rental market today is nuts - but even a 2% return is better than the bank will give you. And without government backed deposit insurance - a fact you can combine with no tax on capital gains... creates the perfect irrational/rational storm.

1980's Donald Trump was purchasing rent controlled buildings cheap, forcing the tenants to vacate their lease (rodent infestations, power cuts, loud ongoing renovations, lawsuits, onerous stipulations) and converting the place to condos at a vast profit. Rinse and repeat, expanding scope as he went, he was able to amass his multi-billion dollar empire and by writing off his ongoing buys ended up paying no tax.

Whenever you see someone advocating rent controls, it is good to think of the Donald Trump's of this world who will profit from it.

Rent control can only be used if there is a big build programme for the bottom-end of the housing continuum. If there isn't enough new supply and prices/rents are fixed then the market will experience a shortage i.e. an increase in the homeless rate.

Brendon, there is plenty of new supply coming on the market, e.g.,

https://www.interest.co.nz/property/108245/no-sign-any-slowdown-residen…

The problem is that when listed for rent, it's unaffordable;

https://www.trademe.co.nz/a/property/residential/rent/wellington/lower-…

https://www.trademe.co.nz/a/property/residential/rent/wellington/lower-…

https://www.trademe.co.nz/a/property/residential/rent/wellington/lower-…

https://www.trademe.co.nz/a/property/residential/rent/wellington/lower-…

https://www.trademe.co.nz/a/property/residential/rent/wellington/lower-…

https://www.trademe.co.nz/a/property/residential/rent/wellington/lower-…

https://www.trademe.co.nz/a/property/residential/rent/wellington/lower-…

https://www.trademe.co.nz/a/property/residential/rent/wellington/lower-…

And these newly set rent maxima are driving up the expectations of existing rental accommodation.

I believe the government is building state housing at the fastest pace possible. Continuing to call on the government to go faster - gets us no where at the pace required during a housing crisis. Many existing rental properties in private ownership were bought 4-5 years ago when prices were extremely low compared to now. These landlords can well afford a level of rent that fits within that 30% of household income maxima. Those that bought recently, as per above, will either take a loss meantime (hoping the untaxed gains make up for it in future) or on-sell to the middle/upper income FHB market.

We need both if we are to get on top of this crisis.

Keep up the good work Kate!

/s

It just cracks me up that landlords/property investors assume that they can never make a loss on an investment.

But that is the whole concept of risk/reward - that sometimes you have to take a bath but NZ property investors haven't for decades and assume they never will.

Therefore any potential losses must be carried by someone else - either the tenant or the taxpayer. And up to now, the central banks and government have supported this false narrative - question becomes....for how much longer?

Yes, exactly - and it is indeed a false narrative.

The way I see it, is that your average housing investor has 'made' hundreds of thousands of dollars, untaxed the last 5-10 years. Some much more. I have friends who have made millions in property investments, yet they expect someone else to pay taxes to keep yields on property investments attractive enough to prevent prices from falling....its just completely out of touch with reality and how a free market should function that it almost seems corrupt.

Perhaps if the tenants can't pay enough in rent in the free market, they (the landlord) should be paying the difference out of their personal income or equity in the property to the bank to cover the mortgage. Then when we all realise the price level is too high, the equilibrium for the market (demand) will drop and with it prices. You can't have your cake and eat it too....unless you're a property investor...its a rort!

Those really dumb prty investors making millions sheesh

And your point (?)

I concur... they should not be making millions they are tooooo dumb

They can make millions if the want, but they need to be held accountable for the social cost. Like any 'business', the owner has a social responsibility. Time for the landlords who have made millions to stand up and look after the societies that have given them that wealth.

Should we vote green party... labour not implementing any envy taxes

Haha to believe that others are envious, would incorrectly assume a moral superiority in some sense (in this case wealth)....that would be the ego speaking.

To feel morally superior to others because one owns multiple properties (and therefore others are envious) pretty much sums up how detached our society is becoming.

Its odd how there is a high correlation between property investors/owners and being egotistical trolls - any psychologists read these comments and can provide insights?

You (sing or plu) get what you deserve right?

It's absolutely a problem of entitlement mentality and active resistance to any other approach (witness the hysterical shrieking when CGT was brought up). And this was money made off the back of affordable housing supply created through the efforts of the post-war generations and their governments. It's living off the backs of prior and following generations.

The big question is, how do we expect to keep transferring the wealth of younger Kiwis to older asset holders while expecting those younger Kiwis to maintain respect for law and our institutions. As places such as Austria experienced in the past, when we use inflation to steal the wealth of the young, there are moral consequences for society (moral decline). Why should a young person accept it's wrong to take the wealth of someone else if they've constantly suffered their own wealth being taken?

Yip but we don't record the 'inflation' because that would make it clear for everyone to see. It reminds of what I've read about the early 1930's. Just find it bizarre that those who are doing well from this fail to have any humility about it - instead think its their right to have even more. Doesn't ring true for me and as you say, its how societies will end up breaking down.

I agree, that this is the best Govt. can do, which is a telling indictment of their ability, as the top building company in the USA builds 55,000 per annum.

But Brendon is right, rent control at best is just triage and needs to be followed up with increasing affordable supply which is about removing restrictions that cause supply constraints.

40k houses built per year, zero net migration, zero students, massive number of apartments built (in Auckland anyway)

And empty motels available for use all over the country.

Seems like a problem that will fix itself pretty soon. And as long as the consents keep flowing it will stay fixed.

40k a year? Are you sure? I thought we were building 12 to 14k a year.

This published on Interest.co.nz yesterday.

"According to Statistics NZ, 37,981 new dwellings were consented in the 12 months to the end of October, up 2.8% compared to the previous 12 months."

I think this works out to 7.5 houses per 1000 residents. This is getting better but in the past ( the 1970s) NZ has built at 10 houses per 1000. Canterbury by 2016 was building at 10 per 1000 and that did stabalise the housing market.

But that is FHB paradigm thinking. What will bring rents down for the working poor? Because poverty cannot be addressed while they pay 50% of their income in rent.

The number of consents issued has been steadily rising since 2011. Assuming that translates into houses built then there has to be a large surplus.

I've been charting auckland trade me rental listings some june this year. Significant upward trend in listings since Sep/ October.

About 4500 then to 5300 now.

So I think supply will bring the rents down for the working poor.

Better data always welcome...

Seeing the same kind of data around Wellington area but see my post above - all the new build rents are unaffordable, and the existing rental properties are raising their rents in response to both new builds and new buys;

Purchased in 2004 for $140,000 - wants rent of $530/week;

https://www.trademe.co.nz/a/property/residential/rent/wellington/lower-…

Because same suburb, same house size purchased this year for $600,000+ - wants rent of $580/week;

https://www.trademe.co.nz/a/property/residential/rent/wellington/lower-…

Median personal income in the suburb is $34,600 - you'd need three adults working at that median income rate to make upwards of $500/week an affordable rent;'

https://www.calculate.co.nz/rent-affordability-calculator.php

5 years ago, the rent on those places would have been less than half what they are asking now.

Question is, will they actually get what they're asking? Some landlords are over-optimistic with their asking rent.

That said, Wellington does seem particularly tight at the moment.

Perhaps not but look at how Auckland has headed - multiple families in the single 3-bed dwelling as a means to make the rent.

Your argument misses the point completely. Its not about what the owner bought the property for 16 years ago, its about what its worth now. This is known as "return on capital". The owner has $600k now invested, not $140k. Because his choice is to get a return on renting out that $600k house or selling it and buying $600k of bank shares and getting a 7% dividend yield. The only reason long term property investors are still hanging in there for such rubbish yields is the capital gains. If you want to lower rents and reduce the capital gains, the only outcome will be investors selling up and moving to a different asset class.

The rent (to give your yield) is calculated on the value, but your return is based on your investment (ROI), which is both your yield plus capital gain minus costs.

So if you take the net rental return and net capital gains together, what has been the average ROI over the last ten/twenty years?

12k to 14k is Auckland, not nationwide.

Roger... exactly. the big ones are zero net migration and zero students. How can 300 000 fewer people requiring homes over the next five years not have a huge impact on homelessness, rents and property prices? It would simply have to and yet it seems immigration is almost a taboo topic, which is invariably left out of the discussion. That needs to change.

Excellent.

A bit more in news media about what real housing crisis is (unaffordable rents for the working poor in short) would be useful instead of total focus on FHB and deposits and sky rocketing house prices.

So NZ is worst in class for rent paid by bottom 20%. What an indictment.

And Jacinda has no clue what to do about it, or won't. Swing voters indeed . V acute.

Oh they will 'have a clue' - they just don't want to have to defend rent controls against what they likely perceive as a wave of criticism from the neoliberal crowd.

There's the truth of it

Most of the analysts in their govt agencies haven't moved on from a neoliberal world view. Seriously.

I know - I've worked with them.

Me too. :) double confirmation!

Oh they will 'have a clue' - they just don't want to have to defend rent controls against what they likely perceive as a wave of criticism from the neoliberal crowd

They are the 'neoliberal crowd.' Labour are absolutely no different from National in terms of economic dogma. The same thinking is pervasive across middle NZ.

You assume that is the fault of rents, and not the fact that incomes have not risen over time due to the record pace of immigration swamping the country with cheap, unskilled labour that permanently depresses wages. Its not that rents are too high, but that incomes are too low.

KW... 5 year rent freeze, unoccupied house tax and slash immigration for 5 years = problem solved.

Can't you just eat cake for a few years?

I've thought for awhile that central government should designate land for housing purposes under the RMA, which effectively removes it from any other use and avoids local government incompetence in providing enough land for housing. Central government would be able to purchase non-residential zoned land (i.e. farmland) at a farmland rate and thus avoiding the inflated 'zoned for residential rate', though it would probably need to pay a little more of a premium to get the landowner to sell (or utilise the Public Works Act).

The clear issue would be that such housing would generally be on the edge of cities and cause a whole range of problems for people this would be intending to assist - transportation to work etc. But if such housing was attactive to other people perhaps other housing would become cheaper?

Surely housing can be seen as a public work no different to three waters, schools etc?

EDIT: Of course this wouldn't be necessary if the value of land was nominal by there being an abundance of new and redevelopable land available. But it doesn't due to local government vested interest and hence the above solution.

This is part of the Austrian housing model. In Vienna - their most expansive land market - they have a city-owned housing land fund that provides an active land acquisition/master planning management mechanism. Vienna is pretty good at integrating this land with its U-Bahn rapid transit network. The new urban district Seestadt Aspern is a good example.

http://www.wohnfonds.wien.at/media/file/english/aspern_seestadt_2019_en…

There is more about the Austrian housing model - which must be one of the best social housing models in the world - in the following report. In recommendation no 8. Build Houses for the Full Housing Continuum.

https://medium.com/land-buildings-identity-and-values/if-not-now-when-f…

I was at a local government - infrastructure sector conference a couple of years ago. The Council CEO said that they were wanting to open up more land but said existing land wasn't yet expensive enough to make it worthwhile for developers. That's the problem right there. Any talk of solving the housing crisis by involving 'stakeholders' with vested interest isn't going to solve anything. The only people government should eb talking to is those that can't access affordable housing and then go from there.

(head in hands) 'not expensive enough..'

And the big subdivisions? Well they're often on land purchased by one developer who then doles sections out at a trickle over 10 or 20 years.

Exactly and private sector developers use covenants as well as the trickle tactic as a way of marketing the sub-division to the higher socio-economic end of the marketplace. So no affordable rentals, no multi-unit dwellings suitable for affordable rentals. The market is messed up and some sort of intervention is required...

The present system allows them to trickle out at the rate of how to extract the most out of the market without killing it. This is because the developers have a monopoly as they are the restriction in the market.

But if there is less restrictive land-use control, then the land is released to meet actual demand, so you don't get under developing or over developing. In this case, the buyer is the restriction, ie fewer buyers to supply, as the developers know there are other developers also after those same buyers. This is similar to how the car market operates, ie true free-market competition.

Re Covenants. Need less restrictive zoning, and let the market tell the developers what covenants they want or not.

Private covenants are a cancer and need to be banned. Or at the very least remove those that are 'in perpetuity' to a maximum of say ten years. There is going to be a massive problem for cities trying to intensify areas that have no subdivision covenants, in favour of a developer that took off years ago.

Covenants are just private zoning, and are preferable to zoning, and are essential for new developments, otherwise, if you are the first purchaser (someone has to be first) then your neighbours could do anything they wanted. Thus the amenity value of your property could be reduced to below its replacement cost. Who would develop, let alone build in a subdivision like that?

But I agree that they should have a review period, say every 20 years, which those that are covered by the covenants get to vote on to keep the same or change with say a 75% majority needed to take effect. This would give certainty to value but allow change over time to suit present needs.

Who would develop, let alone build in a subdivision like that?

Everyone that lives in an area of urban land subdivided in the 70s and earlier, I suspect.

And that's why they are complaining about developers densifying around them, ie they have no control of their neighborhood, or immediate neighbour blocking sun, etc. Sounded a good idea at the time, but the chickens have come home to roost, somethings literally.

So I think there is some justification of the owners in neighborhoods (historical especially) having concerns, but there is some hypocrisy too, ie fight to stop developers building next to you, but as soon as you are ready to go, then wanting full mini-land banker rentier payday. If the neighborhood had really meant that much to everyone, they could have individually put restrictive covenants on their own property, or collectively as a group to protect the area.

they have no control of their neighborhood

A neoliberal paradox - private property rights are sacrosanct, except when you want to dictate the rules beyond your rightful boundary.

To my mind, covenants are simply a means to maintain inflated land values through the staged release of land in a subdivision. They force expensive builds/designs in order to guarantee a higher median household income across the subdivision. And what I've found is that land values outside the subdivisions often rise at a much faster rate than the covenanted land, as people prefer older, 'organic' neighbourhoods.

Calgary in Canada provides some great example of this. I call it the 'Stepford Wives' effect.

You contradict yourself, 'covenants are simply a means to maintain inflated land values' vs 'land values outside the subdivisions often rise at a much faster rate than the covenanted land.'

And covenants were never designed as you suggest but were to maintain value, not maintain inflated values. There is a tendency that whoever builds first in a subdivision, sets the upper limit and any news builds will build to a lower value than that, so as not to overcapitalise, plus to also 'coat-tail' on the better value of their neighbour. The right covenants stop this and make sure everyone builds to the same value.

You can set covenants for any type of subdivision, whether it be a mobile home park to whatever. It sets the rules for a group of like-minded individuals to get together.

What constitutes value changes over time and good covenants allow for change.

It goes like this, Country rules, council zoning rules, covenants, your own house rules. Actually covenants used to be what zoning is today before it was handed over to elected public officials.

What would be best is to do away with zoning, allow land to be bought at rural value, and then let the developer set the zoning/covenants based in what the market is telling them they should build. That's what they do in places that have affordable housing.

Was it foreseeable by the powers that be? The local govts used to provide affordable but not any more, why not

And has the holding costs for that 20 or 30 years..

Sure, but that doesn't seem to put them off.

Here in Wellington we have Lincolnshire Farm (Russell Properties), Aotea & Kenepuru (both Carrus Group) and the proposed Plimmerton Farm (Plimmerton Developments Ltd). Huge areas tied up by a handful of players.

And the more they hold off, the more they make.

Also what you find with these groups is that they are either still part of the original farming family so was purchased originally at its farm price and was farmed and paid off on that income, or it has been purchased by companies that have cash surplus businesses and the land is a better cash deposit than money sitting in a bank earning very little interest. Any debt that they might have against the land will be as some tax right off against their cash businesses.

That's how monopoly landbanking works.

Exactly. What incentive would they have to flood the market and drive down land prices? What I don't understand is why they're allowed to do this time and time again.

Because Govt.s don't understand what they are doing, or if they do, either don't care or make money/votes for allowing this to happen.

It's classic monopoly rentier rort.

The govt owned Pamu aka Landcorp has millions of hectares it owns there must be some which is suitable for housing... don't cry foul about private individuals if the govt does similar

From Wikipedia page:

"Landcorp Farming Limited ("Landcorp") is a state-owned enterprise of the New Zealand government. Its brand name is Pāmu. Pāmu is the Māori word 'to farm' and reflects the deep connection New Zealanders have with the land, born from respect, and a genuine desire to protect and enhance the environments in which the company works. It's a proud provenance that stands behind every product bearing the Pāmu name.Its core business is pastoral farming including dairy, sheep, beef and deer, as well as a Foods business marketing milk and meat products globally under the Pamu brand and as a supplier to other food processors. Pāmu manages 117 properties carrying over 1 million stock units on 3366,3426 hectares of property under management."

Great article, and an important reminder that -- while middle-class FHBs are indeed screwed over by the current situation -- the genuine crisis is elsewhere, and too often ignored. Also a good summary of Kiwibuild failures, and the weirdness of targeting a social housing initiative at... people who can already afford to buy a house.

The politics involved in house prices to me has shown a dark underbelly of NZ society and culture. We are 'very nice' but we are also very selfish and greedy.

Prime Ministers and governments want to push prices down - see John Key and Jacinda Adern, from opposite sides of the house, a decade apart - but become pitifully weak in the face of the dark underbelly of NZ society and become the lap dogs to greedy asset owners. You may say I'm making this up, but how else do we explain the complete capitulation of two (internationally regarded) strong leaders over a nearly 15 year period?

Thinking that high house prices is going to be our savior, is like saying going to church will save me from dying. You have to face facts eventually regardless of how much like jesus you think you are, either christian or landlord.

We are 'very nice' but we are also very selfish and greedy.

I disagree. Looking out for one's own interests is not necessarily 'selfish or greedy.' The system is geared to make people behave as they do. However, there are unintended consequences for 'money tree' economics. People are genuinely unaware of this. When those consequences hit, the reality will sink in. People may wish there never was a property bubble.

“It is not from the benevolence of the butcher, the brewer, or the baker that we expect our dinner, but from their regard to their own self-interest. We address ourselves not to their humanity but to their self-love, and never talk to them of our own necessities, but of their advantages.”

“Civil government, so far as it is instituted for the security of property, is in reality instituted for the defense of the rich against the poor, or of those who have some property against those who have none at all.”

Written 250 years ago, but still relevant. I guess when we have enough serfs in society, as Smith says they also can act in self interest.

It is extremely selfish and greedy, when one knows that their actions have such a negative impact on others. Many of the people engaging in this behaviour are already quite well off, some incredibly so. They don't need to ride on the backs of others who have almost nothing, any further or harder than they already do, and yet they choose to. They could decide to be decent and stop at any time. The system might be geared this way, but these are people of means, who have far more freedom to choose than those below them.

We have long ignored the hypocrisy of considering ourselves a kind and generous people, while our culture of predation on others for the most basic of necessities, is normalized, encouraged and greatly rewarded. The number of tenants I have come across in this country, who have landlords that claim to follow Jesus - yet love jacking up their rents at every opportunity, while ignoring basic maintenance and making no attempt to understand their obligations under the tenancy act or deal decently with those under their power... Attending church and voting against the basic rights of others is what's important to them.

It's appalling. A mirror needs to be held up. We all need to have an honest look at the kind of society we really have here. There is no team of 5 million. There is a rising tide of frustration and anger that will break this delusion soon enough.

It is extremely selfish and greedy, when one knows that their actions have such a negative impact on others

This doesn't really make sense as an argument that self interest is not the same as greed. If I were to withdraw all my money from the bank and buy Bitcoin, this does actually have a 'negative impact' on the bank and its employees and shareholders. Does that mean my own self interest should be sacrificed for a bank worker or shareholder? I would agree with you to some extent if you were talking about slum landlords.

I.O.. totally agree but also think it is a lot more to do with protecting the banks.

And then you wonder why do we pay the executives of banks millions of dollars per year to keep a debt ponzi in order? Why don't we just allow FHB's to borrow at the risk free rate directly from the central bank and cut out the parasite that is supporting high debt levels and turning the country into debt slaves - pushing prices above where they need to be? It appears there is little competition between banks regardless, or if there is any, its simply for show.

If we want less debt and more people in homes, why not just go full communism on this - set a price point for houses and young people lend directly from the central bank at the risk free rate? We don't have free markets anyway, so why kid ourselves that a neoliberal capitalist approach is morally better than a communist approach?

Social housing sounds wonderful until you realise the magnitude of it. I'd appreciate any data on the percentage of a given population who receive social housing e.g. NZ vs Sweden vs Austria.

New Zealand from memory is around 5% for state houses and Austria is around 25% for social housing (but most of these are very different from NZ state houses - they received capital support when constructed - very low interest 30 year loans etc - but after that each housing project covers its costs by rent payments). I am not sure about Sweden's social housing numbers. You would think this would be really expensive for Austria - but it isn't because a system of capital grants payments is more efficient than income support payments when it comes to government housing support spending. For instance in 2017 the Accommodation Supplement was increased by $500m/year - yet it only provided temporary relief for tenants because over the last 3 years rents have risen so much the landlords have captured all the benefit. This is the problem with our 'rack-rent' housing market. There is a ratchet effect where all the benefits go to the landlords and none to the tenants.

Spot on data, yet again!

And increasing in A/S is like the government taking on the habit of smoking cigarettes - useless waste of taxation resources.

Beggars belief that we are handing over $500 million in welfare payments per year to property investors. Crazy. Property investment truly is NZ's biggest welfare scheme, all generosity told.

That was the increase only in 2017. The 2020 total figure is $2.4 billion:

The Accommodation Supplement (AS) is increased by $630 million to total $2.367 billion to support private renters and, to a lesser extent, home owners. The number of AS recipients is projected to reach 431,400 in 2020/21; an increase of almost 110,000 recipients over 2019/20.

file:///C:/Users/user/Downloads/Budget%202020.pdf

Sounds like half of NZ society is currently getting social housing - its just that landlords own it, and those paying taxes (not landlords...because they're making losses...how bizarre), pay for it.

This is exactly the point. We cannot expect the state to house one quarter of our entire population of households - most of which are working households. Income to rent at no more than 30% is the metric to focus on and the private sector has to be capable of meeting that metric, or exiting those businesses.

Going forward 1/4 of new housing could be social housing (about 9000 houses atm given we are building 38,000 houses a year) if New Zealand followed the Austrian model by developing a non-profit community housing sector. If they were given capital grants to build housing affordable to those on the minimum or living wage. Land bank fund used to ensure land is affordable and competition model of tendering with points for - economic, social, architectural and environment factors. Each housing project and each community housing provider being responsible for rent covering their costs. Tenants can provide equity - up to 5%, which they can use KiwiSaver to access - this gives them the right to buy after 10 years.

State housing and the Income Related Rent Subsidy could continue as it is - building about 2000 houses/year - providing a housing solution for the most vulnerable groups.

Or we could take out all the middlemen, which includes the 'non-profit ' groups, which as we know do make profits.

Govt. policy is making the problem, which they conveniently create a solution for, which strangely enough happens to create a costly quango for further the bureaucracy.

The amount of non-value-added costs (waste) in the system is about 1/3 of the cost of a dwelling.

A cost to us is revenue/income to these groups.

And we should not be needing to touch Kiwisaver, it was never originally meant to be used for this.

Dale there are other housing models as successful as your beloved Texas model that do not have the waste you complain about.

Also if FHB can utilise KiwiSaver for to buy a home outright then I cannot see why the same provision cannot be made for a rent-to-buy housing.

What other models give you a median multiple of 3x?

Kiwisaver was set up to be the retirement fund, with no matter what bad fortune you might have had with other investments etc., whether it was your own fault or just being on the wrong side of history, that when you get to retirement, you had enough, and didn't need further Govt. support, or at least less of it.

It was a huge red flag that the housing market was dysfunctional when JK allowed people to access their Kiwisaver.

The argument is not whether they should be allowed, but why they even needed to consider it in the first place.

Strangely you are still whittering on about the 3x median multiple when I have explained why that shouldn't be the priority target.

To me, for other models being as good as the Texas model as you said there are, would also include not having an increasing majority of the population needing to become wards of the state.

The Texas model includes massive subsidies for motorway building. What's the difference between subsidising the capital costs of roads versus social housing? Is one decent investment while the indecent waste in your mind?

Also the Austrian social housing model the subsidy is a one-off capital grant. After that the tenant pays the full cost of the rental. So your 'wards of the state' pejorative slur is off the mark.

Now that is a contribution to the greater good. This is what a Texas Motorway looks like, and what it does, not only for mobility in Texas, but for the whole country. https://www.thecorridor.org/

And yes it was a pejorative remark aimed at Govt. policies that cause its own taxpayers to become dependant on them for something as basic as a warm, dry, healthy affordable home.

Remembering that this is not a Govt. acting to protect the population from an external threat like Covid.

The Govt. wants to protect us from themselves, namely the failed housing policy.

If you think we are too far gone for the Texas model, then what is wrong with the Swiss model?

The point Dale was even the Texas model the government makes the major decisions about how urban spatial resources will be allocated - by building motorways in the Texas example. I think if the government is going to be involved (which it has to be - because no government would be a third world slum without fresh water, sewerage treatment, roads...) then it is reasonable that the system targets housing be a reasonable cost for the most vulnerable socio-economic groups.

Personally I think the Texas model has some merit - it genuinely does build a lot of affordable housing is the part I like. But for reasons I outline in the paper it is not attainable. I am promoting the Austrian model because it is modernised version of Micky Savages state housing model which we know works in NZ. If you want to promote the Swiss model feel free.

Yes of course all Govts. have some involvement in resource allocation, but Texas allows its people to have a more true free market involvement. And the Govts. the role is to set up the framework, like the roading plan, for which then they leave it up to the market to fill in the blanks as they see fit.

Maybe target the Texas system to allow a presumptive right to build on any land if it targets lower socio-economic group?

We both agree that things need to change, but I don't think we have any chance to build affordable housing by having Govt. getting actively involved. We just don't have the same evolved DNA as the Austrians to do it. It might work if we handed over control of it all to Austria.

Govt's role should be to set legislation that allows the 'invisible hand' of the market to work, but again, I would agree, that we probably don't have even the DNA to do the Texas system.

Have you read any of this piece from the Helen Clark Foundation: https://helenclark.foundation/wp-content/uploads/2020/02/somewhere-to-li...

and the piece on • Refinancing: ‘a progressive refinancing scheme could reduce household debt burdens for the primary home, to mitigate the risk of negative equity resulting from changes to taxation and mortgage lending.’

Basically, saying that the last in to buy in a housing boom are the worst affected when it falls. While small in number this cohort can have a big destabilizing effect that can start a negative ripple through the industry causing further and further collapses. What if we ring-fenced this debt, and while not creating a moral hazard by rewarding risky behaviour, at least not punish them for getting caught on the wrong side of Govt. policy that should have been done a lot earlier, but had to finally draw a line in the sand for the benefit of all now and into the future.

This would allow the Govt. to address the whole system, which would include the removing of restrictions to supply, not as they trying to do by giving the public system a benefit that they hold back from the private sector.

NZ certainly has made a mess of housing, with massive consequences throughout society. We both agree on that.

I suppose the Helen Clark foundation debt forgiveness idea could work, but I suspect it would be another intervention that our political leaders would feel would be not popular therefore not possible.

This is why I think our housing market is going to end in a disaster when everyone thinks they can't make a loss, but expect someone else to pay for their gain. It is stupidity of the highest order.

Utter nonsense Kate.

NZ has 60,000 social housing places for a pop of 5m, I think?

In Uk Housing associations have about 16% of housing stock, which should be: (30 million places for Uk)

So UK provision would be about 5 million.

NZ % is therefore 60000 divided by 1.8m housing units = 3.3%

UK is 16%

There you go

Yes and because we use the UK Town and Country Act as our base model, then that is what we will end up like. Also noting the UK has the smallest new house size if compared to EU countries, ie 73m2.

Great article.

There's no way bringing the overall median down to x3 or x4 is possible, desirable or achievable.

Rather, as I have said many times before, the government needs to build housing that is closer to that median. That would bring the overall median down a bit, but more importantly be targetted in providing house at x3 or x4 for low or lower-middle income kiwis. It's win win - the overall market isn't too affected and the people who simply can't afford to buy now have some hope.

Until the government realizes this, the issue won't be addressed.

Yes, it will require a massive uplift in the government's commitment to house building. But that's only what is required.

Best article in some time. Well done Brendon. I'm just curious as I'm not sure where I read it, but didn't someone, maybe on this site wonder out loud why this extra 28b that the reserve bank is creating, why is it not going directly to the Government to spend on what we need. Why are the banks getting it (to lend on housing) when the Government should and could spend it on state house building starting tomorrow.

Vested interests and their long-held ideology driven more by emotion and self-interest than reason?

Depends Fritz. I am unsure the median being so high is desirable either. If we can create a soft landing for owner-occupiers and then bring in aggressive tools such as DTIs and LVRs with carve-outs for adding new supply - perhaps lower LVRs for certain types of housing (terraced developments as opposed to standalone) in key growth areas like central Auckland - then maybe we can get housing back to sane levels. We might find people spend more and have a better quality of life if housing is much much cheaper - sounds ideal for coming out of a recession, no?

How this would work, I have no idea. In Chch the Govt picked a reasonably recent valuation for their payouts. Maybe we need to do something similar with owner-occupied housing and allow people 'insure' their equity held at a certain date on their family home - but it would require central bankers and govt to move at a speed they've never deemed necessary outside of wartime or pandemics or else people would find a way to game the system. Perhaps the best approach is to view the current situation as a national, natural disaster and work from there.

Yeah well said. This housing issue is a national disaster indeed.

I don't see how that would work GV as much as I understand your personal circumstances. Who would want to buy your house if you try to sell if the valuation of your house is 50% higher than the same one down the street? Or why would a tax payer say that they will pay the difference just for you? That would make you like the property investors who think they can't make a loss and expect the taxpayer to cover any potential downside (which is why we are in this situation (in my opinion)).

It really is a shit sandwich, but that happens when you have ignorant and self serving leadership for a decade or more.

That's the problem - *someone* will have to take a hit. Younger and more recent FHBs won't accept being wiped out financially by a problem they didn't create. Perhaps the investors can take one on the chin for the years they've had the taxpayers underwriting 30% of their losses while they milked tax free capital gains? I think there is a strong moral case to bail out owner-occupiers who have to sell at much lower prices into a reset market, but as you note I have a conflict of interest in that regard. No easy answers anywhere, we've left it too late for gradual change to get us out of this one.

Yeah its just a shame that we've allowed this to play out - and its painful to see how this potentially plays out over the coming years yet nearly everyone is still fixated on their own personal self interest and can't see the bigger picture (the narrative is 'I just need to get ahead', but the problem is is that we can't all get ahead of each other because of the interdependent way that society functions...you get ahead, but then someone does not, then you have to pay additional taxes to help house that person who has been left behind). Somethings is going to give eventually - you can almost feel the pressure building.

That's what bothers me. A structured climb-down is always better than an unstructured default. My argument would be that maybe we'd be better off with the 'real' economic activity that the free-cashflow of thousands of new home-buyers would generate through disposable income instead of throwing 40% of their future earnings at a mortgage and this would see us come out ahead in the long-run.

When you stop and think about it, it's not so different to how we approached the wage subsidy with Covid. Having thousands of businesses fail overnight was deemed to be not in our long term interests. We just spent the money to get it done. Does anyone really think the status quo for housing is in our long term interests? The solution requires the same audacity and boldness.

I personally think the horse has bolted - way back around 2013. I tried having these conversations with people way back then as I could see what was unfolding (after arriving back from seeing a property bubble explode in the US). The bed is made now and someone will need to take a loss - either the tax payer or the asset owners - either we keep paying too much in rents, subsidised by the tax payer, or the general price of the asset falls to represent the cash flows that it can generate in the free market (which we are already discounting near the risk free rate of zero!). We want to have our cake and eat it too, in some many respects, but that isn't reality.

It's maddening. Imagine structuring a pare-back of house prices using a wage-subsidy style equity intervention - and doing it to the point where the accommodation supplements weren't needed? Imagine spending that money on things like dental care or school lunches - maybe lifting benefits or rolling out rapid transit so we could build more, cheaper housing in places where people didn't have mega-commutes to get to work. It sounds a lot more like a New Zealand I'd want to live in than where we live now.

Yes but trying convincing the average kiwi that their house price will need to fall 40% and then you see why we can't have that. Short term self interest, vs a long term utilitarian view on the issue.

As I say above, nobody wants to take a loss, everyone wants to gain, but expects someone else to pay for that loss/gain. Yet we live in an interdependent society, so someone is going to have to take the hit. Question is who.....

GV.. the sad part is that if the shit hits the fan it will be FHBs who suffer the most. Most multi home owning landlords will be just fine because they have lots of equity but many of the generally less well off FHBs who get on the ladder just before any serious long term contraction will be stuffed.

100%. Current levels of indifference to the levels of risk the market expects FHBs to bear suggest that there is zero appetite for anything other than what we've got. It's going to be bad, but it probably doesn't need to be.

Imagine the anger that society will have toward parasitic investors that worked actively against any positive changes, should the worst happen.

Never thought I would contemplate the need for this but......

This piece from the Helen Clark Foundation: https://helenclark.foundation/wp-content/uploads/2020/02/somewhere-to-l… and the piece on • Refinancing: ‘a progressive refinancing scheme could reduce household debt burdens for the primary home, to mitigate the risk of negative equity resulting from changes to taxation and mortgage lending.’

Basically, just like you have highlighted KS, is that the last in to buy in a housing boom are the worst affected when it falls. While small in number this cohort can have a big destabilizing effect that can start a negative ripple through the industry causing further and further collapses. What if we ring-fenced this debt, and while not creating a moral hazard by rewarding risky behaviour, at least not punish them for getting caught on the wrong side of Govt. policy that should have been done a lot earlier, but had to finally draw a line in the sand for the benefit of all now and into the future.

This would allow the Govt. to address the whole system, which would include the removing of restrictions to supply, not as they trying to do by giving the public system a benefit that they hold back from the private sector.

Must have a read, but I imagine it assumes that changes to either taxation or lending will 'crash' house prices. Not sure I'd agree with that, and for the FHB anyway, being 'under water' isn't a problem as long as the bank doesn't see it as one, and as long as the FHB can continue to pay the existing mortgage. Might only need to re-finance (or force sell) in the event of a job loss. In which case, such a safety net whilst they wait to be re-employed might be useful to consider.

I think part of the reasoning is to take what is on paper a bad debt off the bank's books, so the banks are not compromised for normal lending. Although the last time the Govt. underwrote debt, eg South Canterbury Finance, they double-downed on risky behaviour to try and claw back previous losses, and of course, went down even harder.

I've attended seminars from people working at Kāinga Ora - there is a massive uplift in the government's commitment;

https://kaingaora.govt.nz/developments-and-programmes/what-were-buildin…

They are building at pace. But as more people currently finding rent unaffordable via the private sector, the wait list is growing faster than they can build.

The metric you suggest was achievable only 5 years ago - check out the price paid for any property five years ago. One of our sons bought the then very affordable rental he was living in for $260,000;

https://homes.co.nz/address/lower-hutt/stokes-valley/15-lord-street/DGp…

And his mortgage outgoings have since decreased (significantly).

Re: "I've attended seminars from people working at Kāinga Ora - there is a massive uplift in the government's commitment" -really? KiwiBuild is showing no massive uplift. The state house build program is showing an uplift -to about 2000/houses a year - maybe it will ramp up a bit further. Nothing else is expanding - not community housing sector - obviously not KB. The problem with state housing is it is funded by the Income Related Rent Subsidy scheme which basically pays 2/3 of the cost. This is really expansive on a per house basis - so limits expansion. The government needs to add something like the Austrian housing model into the mix.

I agree,and I disagree with Kate's earlier point about them not being able to scale up further.

If they got their shit together with prefabrication, they could easily scale up significantly.

There is a ramp-down of Kiwibuild - for all the reasons you outline above - and a ramp-up of State house building;

https://www.stuff.co.nz/national/politics/121511507/budget-2020-governm…

They're supposed to build 8000.

Oh Kate please refrain from 'building at pace'. That's Twyford gobblygook!

He must have got it from the policy folk at Kāinga Ora :-).

So with all this increase, can anyone point to when prices would come down, after all, they are already building enough volume to show the economy of scale?

The reality of course is prices have gone up. Under this present model, they can only come down if there is an oversupply, and someone else loses money. ie the developer/Govt. instead of the FHB/renter.

The economies of scale in my paper referred to the government programme focused on building housing suitable for low-end of the housing market. Which we have established elsewhere on this comment thread the private sector doesn't provide because developers drip-feed the market and use covenants to prevent low-cost build options - like multi-unit dwellings.

NZ is building pretty much the same way as we have for the last 30 years, using the same low productivity 'subblie' system, building companies who only build a few houses a year, with the same duopoly of building suppliers...