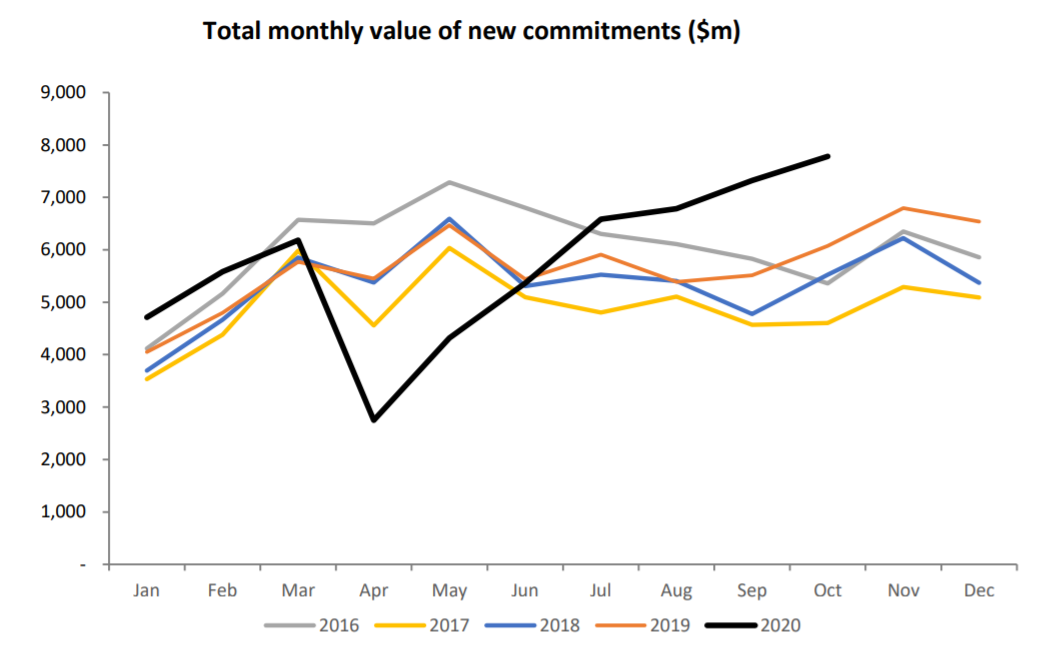

Mortgage lending hit a record high for a second consecutive month in October.

According to the latest Reserve Bank residential mortgage lending by borrower type figures the October lending figure of $7.8 billion was the most since the RBNZ started compiling this monthly data in 2013.

And it eclipsed the previous record of just over $7.3 billion set only in September 2020.

The latest month's figures confirm that investors are now very much on the march in the market again and are picking up share of the market at the expense of the first home buyers.

The $1.9 billion borrowed by investors last month was the highest amount by this grouping since July 2016. And July 2016 is significant - since that's when the RBNZ clapped tough minimum deposit requirements on the investors, slowing them down.

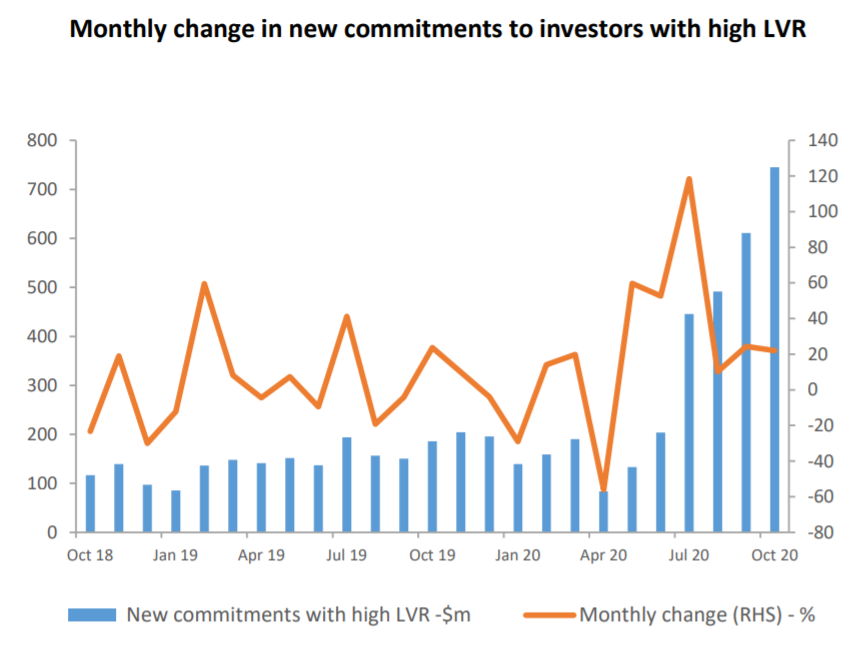

Also very significant is the fact that high loan to value ratio (LVR) loans to investors jumped again in October.

For investors, a high LVR loan is one where the amount borrowed is more than 70% of the value of the property.

In October the investors borrowed $745 million on high LVR loans, up sharply from $611 million in September. In June, the first near-full month after lockdown the investors borrowed just $204 million in high LVR loans.

The housing market has been on a tear since New Zealand emerged fully from lockdown in June, with prices rapidly increasing.

The RBNZ lifted LVR restrictions, which had been in place in some form since 2013, in May, with the intent that they be removed for at least 12 months.

However, the RBNZ announced earlier this month that it was going to consult with the banks on reintroduction of the LVRs from March 2021. This will be on the same terms as when the LVRs removed, requiring investors to come up with 30% deposits while there will be limits - 20% of banks' new lending - on LVRs over 80% of the value of the property for owner-occupiers, including FHBs.

The RBNZ has noted the rise of more leveraged borrowing from particularly investors, following the dropping of the 30% deposit rule.

Banks are already moving to accommodate the reintroduction of the LVR rules.

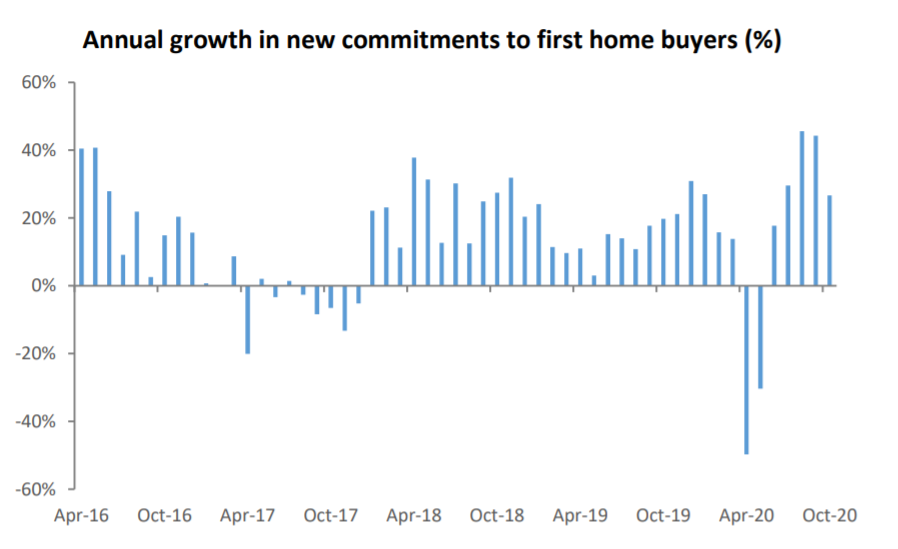

First home buyers have been very active in the market this year, gaining record share for this grouping in the monthly mortgage figures.

And while the FHBs are still borrowing large amounts each month, their overall share is now falling again in the face of the increased activity from investors.

In October the FHBS borrowed exactly the amount they had in September, at just under $1.4 billion.

However, this made up just 17.9% of the overall amount borrowed by all groups in the month, down from 19.1% in September (and it has been over 20%). In contrast the $1.9 billion borrowed by investors in October was 24.4% of the total, up from just 22.7% in September.

This is the detail supplied by the RBNZ:

- Total monthly new mortgage commitments were $7.8b in October – the highest month on record since the survey began in 2013.

- This is an increase of $0.5b (6.3%) from September 2020 and 28.1% from October 2019.

- New mortgage commitments to other owner occupiers were $4.4b in October, up from $4.2b in September while new commitments to investors increased from $1.7b to $1.9b.

- First home buyers accounted for 17.9% of new mortgage commitments in October, down from 19.1% in September while share of new commitments to investors rose from 22.7% to 24.4%.

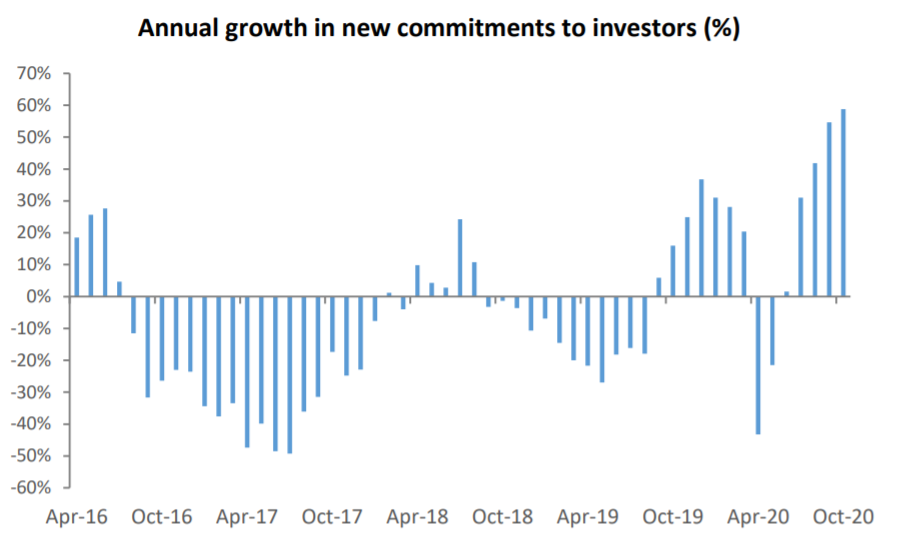

- The nationwide year-on-year growth in value of new mortgage commitments to first home buyers was 26.6%, while the annual growth in new commitments to investors was 58.8%.

- The year-on-year increase of 28.1% in new mortgage commitments was evenly split across Auckland and non-Auckland regions. The annual growth rate for new mortgage commitments in Auckland was 29.9% while areas outside of Auckland grew by 26.6%.

- Monthly new mortgage commitments with high loan-to-valuation ratio (LVR) to investors have increased since the restrictions were removed in May 2020. High LVR new mortgage commitments to investors saw a monthly increase of 22.0% in October.

58 Comments

What a sad state of affairs....

Is it ? This is what the Banks want us to do, borrow at cheaper and cheaper rates for buying houses, which can be rented out. Banks are not keen to provide unsecured loans to small businesses. As long as they want collateral in the form of houses, this will continue. Many Kiwis are scared to make investments in shares, etc. They are familiar with the house investment, see their mates get ahead with buying rental properties, so they also get in. Even FHBs want to upgrade soon. So churning gives more business and revenue to Banks. The Government/RBNZ can try as much as they want, but this is not going away soon. Imagine is this is the state amidst a pandemic which creates uncertainty all around, what would be the situation in a normal time. More the Merrier.

What happens when rates can't go any lower and we are facing the next economic crisis? We won't be able to borrow our way out of that one into house price heaven.

Think RBNZ would again ramp up the printing press until the crisis passes... of course depending on how much QE the government of the day did some of that would again flow into housing.

I thought if a country dumped big QE into their economy by printing money and distributing it they would debase their currency and international markets would devalue it accordingly but oddly enough the dollar has risen. Can anyone suggest why that may be?

Other countries are doing more of this on a larger scale. That is why.

Well, this is a surprise! who would have thought? Surely it must be coincidental with rising property prices.

House prices go up when the availability of credit increases. Who could have imagined?

"The nationwide year-on-year growth in value of new mortgage commitments to first home buyers was 26.6%, while the annual growth in new commitments to investors was 58.8%."

But it's a supply problem.

But it's a supply problem.

Not of mortgage funds lent into existence it's not. It's off the hook.

Fully agreed, just like JA uttering... it's only 'supply' issue. Worldwide, when the CB printing free money aka tweak the games.. they also experienced the same... so indeed they're also facing the same like NZ... supply issue. Who would have thought? - Most of these called expert economist hide the truth, that in order to increase the supply.. govt & rbnz need to stimulate the market to do so: by printing more money/QEs/FLPs into housing, permanent LVR removal (if just for gesture? re-introduce it at 5-10%), we need negative OCR soon, removal of bright-line test & ban rent freeze (more productive to allow of max increases of 4x/year), home is intrinsic value, peace of mind for the economy.

"The nationwide year-on-year growth in value of new mortgage commitments to first home buyers was 26.6%, while the annual growth in new commitments to investors was 58.8%."

But it's a supply problem.

Don't worry, in a months time these won't be high LVR mortgages through well earned capital gains.

Haha. "Well Earned"...I see what you did there.

nothing to see here, may as well wait until March before we look at putting some breaks on, as we need our xmas break, and let the summer house sale season pick up steam. You will however need to extend the axis on the graphs I suspect.

Huck yeah baby, get ready to feel that wealth affect!

For the next 30 years...

Huck yeah baby, get ready to feel that wealth affect!

Streets paved with gold. I want a NZD1000 bill with Jacinda Ardern on it and signed by Orr.

Solves the managed isolation capacity issue by putting out a sign for Kiwis wanting to return that says 'we are closed for [non-speculative] business'.

"First class problem" when you are sitting comfortably in your ivory tower.

She's a tough gig on $650K+.

At least the Chinese economy will be getting a boost from all this capital gain.

How exactly?

Less people are going to invest into productive business, more people need to buy products and services which might not be enough in New Zealand. Which country sells cheap products? China! Then NZ$ value keep falling, Chinese products wont be that cheap anymore. What do we get here? Inflation.

NZD is not falling. It's actually quite strong. As I have noted, it's on a par with the gold price relative to USD in terms of appreciation in 2020 since the 'crash' in March.

Ha ha.. yip! due to that current sovereign support of govt+rbnz, nothing can go wrong with that - we're on the stage of 3 to 4 of economic cancer IMHO - This is actually the best time to promo & encourage different prognosis from different professionals, if housing already 20% up, then 2021 should be the same, we're still far away in comparison to the most expensive housing on the planet. So more room to go up still. Strong patients, can still squeeze your hands hard when you asked.. but behind the scene you've read all the blood test result.

The Banks, especially JPMorgan simply believe they can do what they want without consequences. Over the last 15 years JPM has had to pay out over $38 billion in fines! Has anyone gone to prison. No! These fines simply go on the P&L under the heading Cost of Doing Business. One rule for them and another for the Smaller business owner. To quote Alice from The Vicar of Dibley.... " Naughty LaLa, don't do that again or I'll put you down the toilet and flush" A bit of a hair wash is all these greedy bankers get. https://www.cnbc.com/2020/11/24/jpmorgan-chase-pays-250-million-penalty…

This month will be Bigger and will be till March as Mr Orr has given window opportunity to so called investors to play as much befire LVR is introduced.

So as Mr Orr and PM JA NZ is have God Crisis - Mission Accomplished.

Mr Orr will be very happy for scr.. ing average Kiwi and FHB.

This month all 4 major banks have now come out saying they have imposed the 30% LVR restrictions again voluntarily. Which is a shocking state of affairs, the competitors in the market are now having to introduce their own legislation in absence of sensible legislation from the RBNZ.

bbobbles

Probably more-so in their self-interest rather than any commitment to cooling the housing market in the interests of wider NZ and its economy.

Put a 30% self-imposed LVR and then there is no argument for a premium on top of the standard rate for "low equity" loans, and just protecting their own butts as risk of some correction increases.

interesting point

Odd eh? so all those years they're being prudent? or self interest already at play all along (their commercial banking after all), initial LVR removal.. surely their greed self interest is at play loan to investors quickly, until oh another self interest or self-preservation started to nudge.. bip bip.. if we don't do this, 2023 we might have to join each other in bed of OBR (in all probability) - oh wait, this could be self-interest of pasturing, as they surely don't want the negative OCR eating their past profit savings. C'mon we thought we improve the IQ of OZ & NZ by migrating across the ditch, but in fact these geniuses kiwis have to be dictated not just by the OZ in banking terms but also in their daily groceries. Sweet..

Don't worry...all this borrowing is going to generate inflation...Honest!

To save the blood rushes resulting in coronary problems; taking out changing house prices and differing values of properties between each group and considering the number of actual mortgages:

- For FHB the number of mortgages for September was 3023 (11.8% of all mortgages) and October 2912 (11.6%).

- For investors the number of mortgages for September was 4419 (17.3% of all mortgages) and October 4271 (17.0%).

That is not a significant differences worthy of blood rushes and coronary problems. :)

Note that the the number of FHB in September was a record since data first available in August 2014 - about twice the number then - and is 111 down in the past month.

The number of investors is about the same as August 2014 and at 4400 well below the peak of 5-6,000 between Feb 2016 and March 2017 - and 148 down in the past month.

Trust that you are feeling better. :)

Thank you for those figures, hope it will go to govt & rbnz vein. The stimulus worked well, so hopefully the next 18-14months they'll steadfast with the current plan of: negative OCR for start by rbnz, extension/more value for flexi-wages subsidy by govt. - The LVR is clearly being self-imposed by our prudent banks, so it's useless to be introduced next year, let's hope the govt have a gut to remove this economic development unwanted lump; the bright-line test, then balanced by rbnz to allow more FLPs into housing - I bet you your stat number should get more positive there. - Honestly, we all going to feel better with more positive improvement in NZ housing cost it's a sure of economic growth sign.

Instead of stating a fixed price the price tag can be a revolving counter that clicks over a new price every few days. Top properties in top suburbs would click hundreds, middle suburbs tens and lse increases by single numbers... The longer you wait the more it costs

Previously if a couple could save $50k per year they could build up a nice deposit but with national median increasing $120k in one year they don’t stand a hope.

They just need to stop eating smashed avocado for crying out loud!

My advice to those junior doc, healthcare specialist, pharmacist, nurses, teachers, graduate engineers or cops? tidy up your CV, do zoom interview for Perth, Adelaide, MelB then heads here.. don't be shock with much better wages, grocery bill & housing. Kiwis adaptable to temperature quickly, but for some like me, albeit is tempting for $, I skip Brisbane & Sydney, I'm just chicken for that funnel spider, others include Australians... we can endure it. Even Uni Otago current VC with $625K, think NZ is not worth it - zoom.., next April to Perth.. who's next?

Perth looks rather solid now after a long time of softening after the mineral boom subsided as the chinese reduced their demand. I'm told by a friend who lives there the economy is improving, house prices finally starting to rise after many years of decline then flatlining. He also says it's in no small part to Lithium demand globally rising and at the southern tip of Western Australia, around 250 kilometres south of Perth, lies the Greenbushes lithium mine – the world's largest project to extract the increasingly critical mineral driving the clean energy transition.

Boom times ahead maybe in Perth...

Better still... they need to plant an avo tree and harvest the fruit. With no fse workers in nz pretty soon the price for smashed avo will be "flying"

Saving $50K a year is a lot for a couple as well!

A little stat not provided by REINZ: sales in NZ excluding Auckland, in 12m to October, FELL 2.3%

In Auckland they rose 18.6%

In July - October period, 12m series, Auckland sales rose from 21,892 to 25,975 (annualised rate)

In July-Oct 2019 there was no rise at all in the 12m rate in Auckland.

In 2020 it rose 3000 in that period, on a 12m rolling basis .

Sorry but this is a gross abuse of privilege by investors who can leverage. FHB cannot.

That the reserve Bank caused this is unquestionable.

Then they turn round and claim they rescued NZ economy.

Bull, The NZ economy is doing so well because it has NIL CV19.

Exactly, the “strength” of the NZ economy is primarily due to a robust health response rather than any RBNZ intervention.

Prior to 1971 and fall of gold standard, people used to value savings and earning money.

Now they just ramp up debt.

Who gets interest on all this debt?

The bond holders and banks.

Why cannot be be paid wages that mean houses can be bought without paying off debt for rest of your natural?

Not sort of question that gets asked or answered at elections.

A lot of smart people on Interest and a lot of unresolved anger. If at first you don't succeed try try try again. The property market is what it is, we can vent or rage but it won't change anything. I have bought properties at relative high prices and sold at relative low so I should be upset and angry... heck no. I work on making good deals out of bad and turning bad situations into good. Sometimes its time that makes that difference but not always. We almost never buy individual houses only multiples, they are there if you look and can be a better discount price.

Nice story bro

Unless, you're one of those privy... to do advance study, healthcare research for the betterment, treat others. Your only line of work available in major cities, your salary can only afford buying rental in remote places (which you don't have much control of, or is it bad when you decide the home investor is not for you?) - your age left before retirement surely not favourable when calculated against rapid expansion of prices when you want to apply for mortgage, no all along of your life you're being prudent, suddenly banks will only look at you, if you have partner, if you have less/no child, amazing NZ housing loan criteria eh? - so, like you've said.. we have to move on, world is not just NZ fyi. If NZ close this basic primary needs door for us, my advise to add to your suggestion? move on, OZ is open for highly skilled kiwis, mostly the one that return back to NZ is those without healthcare or wages subsidy, but luckily NZ govt will subsidy their NZ landlord via citizenship subsidy guarantee. So, if you one of a few at the top, imported to reduce waiting list etc? - you've been advised accordingly.

Government needs to firewall itself from a dangerously unstable financial system. We need a deposit guarantee scheme.

Kiwibank ... govt owned so govt guaranteed (probably)

That's the problem - same applies to the big four. Can you really imagine Ardern with her concerned face saying on national TV that Nana's life savings have gone. No - OBR wont happen. It'll be a bailout not a bail in! Labour have already proven they don't mind exploding the governments balance sheet.

Not sure why people worry about the banks, the worry should be about your net wealth if anything major happens and you find yourself out in the street. People appear to be still spending like there is no tomorrow and perhaps there isn't. Runaway house price increases are easily fixed, start raising interest rates, it's the only tool in the box that works.

What percentage Carlos. Wont work.... dollar up up up, exports, employment and economy crash.

and the damage seems cumulative. I really don't understand why the world sees NZ as a safe currency haven given what I see coming down the pike. All's well for now apparently but it's predicated on government debt going from 20->50% of gdp. That's unsustainable, and actually a national tragedy given that none of it will generate cash flow in the future.

Thank you for bringing the stats, it's not always the sexiest journalism, but so very important.

For the investors & FHB, please be quick some jealous advisors manage to nudge the govt & rbnz, hopefully it's just an empty gesture for any controlling measures. We don't need it. I hope Mr.Orr and team head to my advise, just show concern.. but before the Q1 2021 ended, ensure to print more money, ease the FLP towards housing productivity then ensure the 6-9mths of negative OCR, before PR gesture to public to re-introduce LVR at 10% - at the same time have that public PR discussion with govt to remove the bright line test.

I like it how you amalgamated the words "housing" and "productivity". Seems so natural.

I wonder are the powers that be banking, on hyper inflation, or at least quite high inflation, to take care of this debt and bring some balance to the force. Will it cause a rise in wages though? With out that it could be a risky strategy to pursue. I cant see any other way for the RBNZ and GOVT to get things in check.

But it doesn't appear to do that - look around the world. QE appears to be deflationary. So you just end up with more debt and no inflation to help you deal with that additional debt.

At the moment certainly, but once they roll out vaccines and things get back to normal say in 1-2 years? There is a lot more cash out there now, so theoretically at least, the $ around pre QE are worth less. I guess after the GFC and the QE we saw there it didn't cause anything but increased inequality.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.