By Jenée Tibshraeny

See video montage of politicians' responses over the past six months to the question: How are you considering the effects of the Reserve Bank's monetary policy in your policy-making? Finance Minister Grant Robertson admitted, as early as June, he wasn't factoring this into his Covid-19 response.

Skyrocketing house prices are turning the Reserve Bank (RBNZ) into a political football.

In the past few weeks, we’ve had Finance Minister Grant Robertson signal he put pressure on the RBNZ to reimpose loan-to-value ratio (LVR) restrictions on bank lending against housing.

Thereafter, the RBNZ announced it would consult on reinstating the rules in March - two months before it previously said it would look at the matter.

On the same day the RBNZ indirectly committed to sprinkling water on the raging housing market, it added fuel to the fire by confirming it would launch its $28 billion Funding for Lending Programme (aimed at lowering interest rates) in December.

Then we had National come out saying Robertson should make the RBNZ require retail banks that draw down on this low-cost funding to on-lend it to productive parts of the economy, not housing.

While scrutiny and public debate over the immense amount of power the RBNZ is exercising are important, the situation begs the question - how is the Government responding to the side-effects of the RBNZ’s actions - namely ballooning house prices?

There’s an argument the RBNZ should take a breather and stop going all out to lower interest rates. There’s also an argument money could be injected directly into the economy rather than via the banking system, as the RBNZ seeks to meet its inflation and employment targets.

But given the RBNZ has been clear from the start of this crisis it’s front-loading its response and using conventional “unconventional monetary policy” like quantitative easing, the onus has been on the Government to respond to the well-known impacts of this.

It admits it hasn’t, and now we are seeing the consequences of that.

The problem: Inequality

The stimulus isn't being evenly distributed. The haves are getting more, and the have nots are missing out - all the while being most at-risk of losing their jobs.

Lower interest rates are giving residential property owners both relief and capital gains.

Someone with a $500,000 mortgage, who switched from paying the average two-year mortgage rate at the beginning of the year to the average two-year rate now, would save about $54 a week in interest payments.

Someone who owns a median-priced home would have seen the value of their property increase by $85,000 between February and October, to $725,000. That’s a 13% increase in seven months… in the midst of a pandemic.

However, it’s the renters who are disproportionately affected by the crisis. These are typically young people and low-income earners. Their rent costs aren’t falling and they aren’t accumulating wealth, as they don’t own assets.

Those who lose their jobs and go on Jobseeker Support will only get $25 more each week than they would’ve before Covid-19.

Coming back to those rock-bottom interest rates, it’s fair to note lower debt servicing costs also benefit those trying to get into the property market.

But first-home buyers are stretching themselves. The portion of mortgage lending to first-home buyers with debt more than five times their annual income rose to 43% in September, from 36% a year earlier.

A major upside: Lower-than-expected unemployment

It isn’t all so bad of course.

The RBNZ has provided ample liquidity to avoid a Global Financial Crisis-style credit crunch.

Robertson made the right call fixating on keeping people employed. The wage subsidy, tax relief and loan facilities made available to businesses have been instrumental.

Making trades training free was also clever. The uptake has been good so far. Let’s hope these people can help stem labour shortages to get infrastructure projects off the ground.

Putting yourself in Robertson’s shoes

It is also to some extent understandable - politically and economically - Robertson has focused on providing stability to give households and businesses the necessary confidence to spend and invest.

It wasn’t long ago that economists were forecasting big spikes in unemployment and house price falls.

The RBNZ, in its May Financial Stability Report, said: “After nearly two decades of house price growth generally exceeding the growth rate of incomes, the current economic downturn could bring a significant correction.”

It said the introduction of LVR restrictions in 2013 meant household balance sheets could absorb a greater decline in house prices without going into negative equity. But still, a 20% drop would put 7.5% of mortgage debt at risk of negative equity.

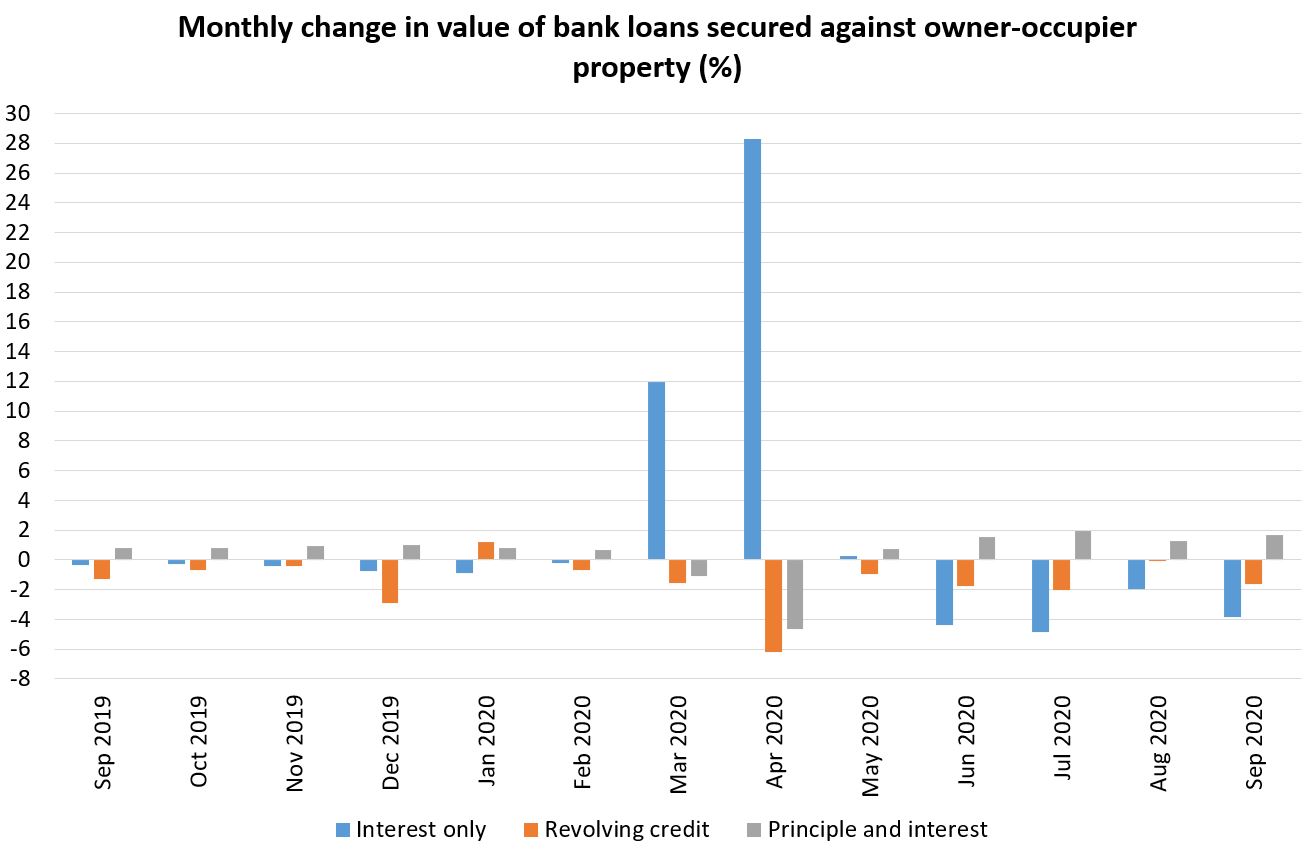

What’s more, in March and April there were worrying-looking spikes in the value of owner-occupier mortgages that went interest only.

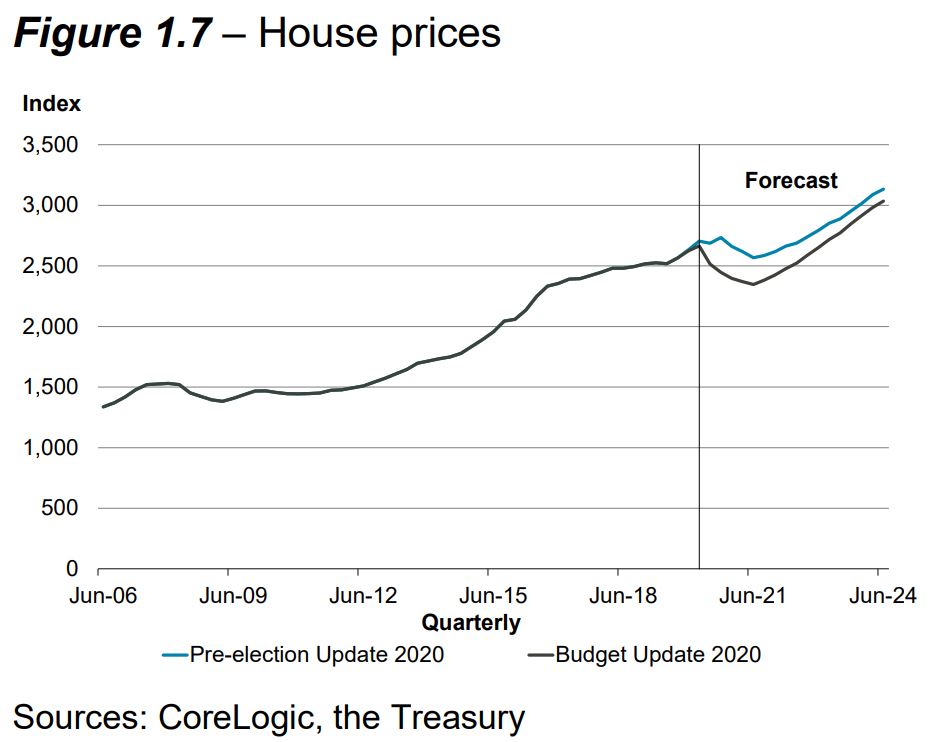

Come the release of Treasury’s September 16 Pre-Election Fiscal and Economic Update, it turned out all the key economic metrics were looking better than expected in the short-term, with the crisis to weigh on the country more heavily longer-term. The bright spot was house prices, which Treasury forecast would keep climbing.

We weren’t at that point, and still aren’t, out of the Covid-19 woods. Confidence is key.

But with Labour no longer needing to feel compelled to gobble every centrist vote in the country to secure a landslide election victory, it’s time it wakes up to the reality the RBNZ’s intervention in the economy is seismic, blunt and exacerbating long-standing inequalities.

I’ve been harping on about it since June - Robertson needs to consider the distributional impacts of monetary policy.

How?

- Ramp up housing supply

We’ve heard it all before - land supply, infrastructure financing, consenting, etc. There's lots to be done.

There is hope in that the number of building consents issued is up and a new National Policy Statement for Urban Development is in place.

Former Urban Development Minister Phil Twyford has given the housing agency Kāinga Ora a number of powers to streamline large-scale developments. It now needs to initiate, or find projects, to go through the new process.

The Government is also committing to underwriting housing developments at-risk of falling through, as banks become risk-averse.

While this sounds dicey, it might be a good thing, as bank lending for residential property development fell 12% year-on-year in September, while banking lending for existing houses was up 7%.

Repealing and replacing the Resource Management Act is vital, but will take years to have an effect.

- Reform the tax system to make it fairer and incentivise investment in productive assets

Taxing income earned from assets more, and income earned from wages/salaries less, makes sense.

Designing the right package is above my pay grade, but the likes of Westpac chief economist Dominick Stephens make a valid point that addressing housing affordability from the supply-side alone isn't enough.

This is of course where Robertson will hit a political wall, as Labour campaigned ahead of the election on not introducing new taxes beyond a new tax bracket for income over $180,000.

A deviation from this will upset some people and give the Opposition ammunition for Africa.

But the counterfactual is Labour spending the next three years being berated by both the Greens and National, which now sees political capital in voicing concern over house price inflation.

- Work through the recommendations in the 2019 government-commissioned Welfare Expert Advisory Group report

A childless-adult cannot have a half-decent existence living on Jobseeker Support of $250 a week.

The Welfare Expert Advisory Group called for this rate to be increased to $315. It suggested some types of benefits be increased by as much as 47%.

The gross cost to government of implementing all its recommendations was $5.2 billion a year.

To put that in context, the Government spent $13.7 billion on welfare, excluding the wage subsidy and NZ Superannuation ($15.5 billion) in the 2020 financial year. This is expected to jump to $17.2 billion in 2021.

The RBNZ has committed to printing up to $128 billion through its quantitative easing and Funding for Lending Programme. Long-story-short, this money will be trickled through the banking system to lower interest rates.

It’s hard to argue with the 70 non-government organisations that have signed an open letter urging the government to increase benefits before Christmas.

What’s more, those with less are most likely to spend what’s given to them, which is stimulatory.

It’s great businesses can borrow for cheaper, but there’s no point doing so if they don’t have customers.

Conclusion

So, let this debate over monetary policy continue. But let’s not accept politicians deflecting to the “independent” RBNZ when it comes to housing.

This state-sanctioned concentration of risk in one asset class - residential property - needs to stop.

It’s unsustainable, imprudent and risks eroding the fabric of our society.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

147 Comments

There’s an argument the RBNZ should take a breather and stop going all out to lower interest rates.

"There's very little stimulation coming from the RBA," Mr McKibbin said.

"What they're doing is maintaining liquidity to prevent a loss of confidence and to prevent a financial crisis. So the Reserve Bank's role is to create a stable environment for fiscal policy to step in."

"Keeping illiquid firms alive is a good idea. Keeping insolvent firms alive is a very bad idea for productivity," he said.

The comments follow a speech from Reserve Bank governor Phil Lowe on Monday in which he defended the need for QE to fight the gravitational pull of low interest rates,

Mr McKibbin described the Reserve Bank's $200 billion term funding facility as an important innovation. He said it would allow the banks to borrow funds at 10 basis points and invest in state government bonds at 60 basis points – a trade that keeps liquidity in the system.

"That doesn't stimulate lending enough to jump-start an economy that is contracting between 2 and 6 per cent this year.

"The bank really just has to wait. We have many issues in Australia but also shocks coming from overseas [such as] the re-emergence of the virus and the uncertainty of the election outcome in the US.

"There's a lot of potential external shocks that the bank can't do anything about but it can prevent a financial crisis in Australia."Link

[my bold]

Is this fellow competent or just spinning a line of nonsense for our consumption?

We did not get a capital gains tax because Jacinda just was not capable of fronting it. Almost every OECD country has one and for good reason, which is why the Tax Working Group recommended one. But a wealth tax would result in capital flight to Australia.

Labour picked one hell of an election to adopt a conservative approach towards new taxes and spending.

NZ National may have lost the election but seem to have walked away with the ideological victory of forcing team Jacinda into wasting yet another term on phoney fiscal prudence.

Meanwhile in Aussie, NSW government's land tax proposal has received bipartisan support and attracted praise from their central bank's governor.

Meanwhile in Aussie, NSW government's land tax proposal has received bipartisan support and attracted praise from their central bank's governor.

Not a great example. The Australian States are bloated and duplicate everything (education qualifications for example) with great inefficiency - all funded by stamp duty, pokie taxes and GST. The NSW state is the largest employer in NSW. Stamp duty stops people moving for work and simply pays for a bloated and unnecessary bureaucracy. Australians look admiringly to NZ on this issue. It's not going away, just that you have the option to pay through time or upfront.

I agree with you that the Aussie's have a major drag on productivity because of their bloated state sector. These state governments have no interest in economic diversification outside of mining and real estate because royalties and stamp duties make up large portions of their state budgets.

All that aside, there is some merit in the decision to move away from collecting stamp duties on property transactions towards a land-based taxation.

I think whatever the New Zealand solution is, in terms of tax for property, it needs to scale - if you want to hold more property, then you should be taxed at a higher rate. Multiples, even. We have to break the idea of investing for capital gains to get people thinking about pathways for financial independence that don't involve making shelter such a major expense.

I'm sympathetic to this, NZ has the most investor friendly property market by some margin and it does create distortions. I would go for capital gains ahead of land tax, the latter will be passed onto tenants.

It depends, do you want to tax at realisation or create an additional holding costs? I know the CGT lock-in effect has been academically disproven, but I'm not sure how that will pan out when we have such massive supply and inherent affordability issues to begin with. Logic suggests that cheap credit will mean vendors can price in extra margin lost to a CGT and buyers won't have any choice but to borrow extra to pay for it. We have to be really careful about how we proceed with this one.

Land tax can't be passed onto tenants, landlords already extract the maximum amount of rent they can.

Wrong. Land Tax ( and any other costs) can and will be passed on.Once all landlords are on the same page rent rises will happen.

They will have to fight against the increased supply as marginal vacant houses enter the market, and current land banks are released for development due to higher carrying costs. Sub-division is also encouraged, further increasing supply.

Over time, landlord costs will equalise somewhat as land prices fall and new entrants have lower finance costs. Existing landlords will have to suck up that loss, but that is the way of the world.

Haha.. dream on. When you're involved in the industry you'll understand, until then you're just guessing and tilting at windmills. Any marginal tax is merely a minute cost easily covered by Cap gains and added to sale prices or rent.

I do own a rental incidentally, but I'm under no illusions that I'm any kind of price setter in the market - we all simply take what the market offers us. There is no rule that being a housing investor is a 1-way bet, and significant government intervention can easily have an impact by reducing property prices, reducing achievable rents, or increasing costs.

I fully agree that over time things will equalise so that property investing remains profitable, but every now than then this will occur by existing holders taking a bath under price matches yield again.

Do note that you are against the economic consensus in claiming that a land value tax will lead to higher property prices. This is not a logical position.

That's the same economic consensus that predicted house prices falling?? haha.. yeah that was a gem of a prediction by so called experts wasn't it?

Why would landlords not already increase rents, if they are able to? Of course, the market is not perfectly efficient, but in general all sellers of a good or service will try to sell it for as much as they can.

Take an example case (which would be replicated en masse across the population):

Tenant Bill earns $900pw. He pays $450 rent for an apartment in Auckland. If his landlord, Jane, increases rent to $500 he will move to Christchurch. Jane will not increase rent to $500 because she hasn't got any potential tenants who will rent at $500 (they will all prefer to move to Christchurch instead at that price/wage ratio).

A land tax is added at 0.5% of the land value per annum. Jane increases rent to $500 to try to pass on the cost. Bill moves to Christchurch, and Jane has no tenant.

Is Bill living under a bridge in Christchurch? If Auckland rents go up due to land tax, then so will Christchurch rents. Christchurch (and the rest of NZ) landlords will pay land tax too, so moving cities won't avoid rent increases.

Christchurch rents are cheaper, though. If you can't afford to buy all your necessities in one city but you can in another, you'll move to the other.

The fundamental problem is that there's no reason for landlords as a collective to extract as much rent as possible from their tenants, so adding on taxes doesn't change that.

Landlords charge what the market will bear - nothing to do with costs. I bought a rental property over 30 years ago and I charge a similar rent for a similar house as a new landlord who paid roughly eight times for purchasing a similar house. If market rents were to double, I would charge double and if market rents were to halve I would charge half. Despite it not being in my self interest, I believe landlords should be charged a land tax, not charged to homeowners. Society should favour homeowners over property investors.

If a land tax makes rental property a less attractive overall investment, capital will just move elsewhere.

Why own a rental if you could do better elsewhere.

That is ok. You can move your capital elsewhere. The house will still be there for a homeowner to buy

At the micro level, it suits a segment of buyers to be able to pay over time than upfront (you can still do both) - particularly those who move frequently. It is being done because people simply aren't moving and tax revenue is falling - the Laffer Curve, not for any altruistic purpose.

At a macro level it's a good example of a lazy tax that encourages wastefulness.

Oh, Auckland has much higher Council taxes than Sydney - so there is a form of Land Tax happening already.

Given the billion dollar hole in AC's budget and non-rate revenue to drop off for at least another year, we could expect council rates to go up significantly.

Hopefully for those businesses and workers not trying to escape NZ altogether, other regions could prove more lucrative for relocating. Wellington city is already reportedly losing investments to Napier and Whanganui. Taranaki councils seem to be creatively stepping up its game in attracting more economic activity to its main centre.

http://business.scoop.co.nz/2020/11/20/npdc-slashing-fees-helps-buildin…

Living in NP the unfortunate side effect is you have to kiss a builder or any other tradies Bksd to do any minor works, even if you are prepared to wait. No we don't need a large boost to residential housing in NP. There are still many unsold sections.

State housing aka Kiwi build for FHBs. An ad in a local magazine in the last month, some brief extracts. 3 bedrooms ranging in price from 380 < 450k, not too bad but pre-tax income under 120k for last 12 months or !80k for dual income. Haven't crunchd any numbers but if you are earning as a single $120k you have a well paid job and ratio house cost to income just over 3 on the lower priced house. Two people on 60k each a year still not too bad until one loses a job. So compared with Akl not too bad but of course those well paid jobs stated to slip when the Jacinda and Shaw decided to can any more oil/gas exploration here, ouside of existing permits. A shutdown of an oil/gas project already in the construction stage in the last month.

Well, your council chose to hedge it's entire debt for 10 years at much higher market rates. Not only that, it did so under an accounting standard that required the losses to be taken in p&l AND under CSA so it has to borrow $2.1bn to post to it's banks.

So yeah, rates are going to rise.

Mate, the past 10-15years not just OZ look admiringly to NZ in multiple variety of issues, including money laundering, pushing more illegal drugs, deport more crims, cheap labour & student for residential pathway.. you name it. Trust me, any prudent measures by A compare to B will result the natural component of A movement to B - High pressure to Low pressure. It's relative view where you look at it from. Balance in the end? .. is the key.

To my understanding the TWG recommended a comprehensive capital gains tax regime that would capture a wide range of capital gains (including cruelly taxing capital gains in Kiwisaver). This never made any sense to me. We have a serious problem with residential “investment” property gains - not with other capital gains. I would have thought that a capital gains tax exclusively on residential “investment” property would be the way to go.

As time goes by, the partisan approach taken with the TWG will be the biggest black mark against Ardern's name. Such a major missed opportunity at a crucial juncture.

The first part of this is good - very good,

But then we fall back on the 'housing supply' 'land supply' 'consenting more' - which all constitute 'growth', and 'growth' is the all of our problems; overpopulation, over-pollution, over-degrading. That is what has to be reduced, then reversed. It will do that to us anyway; better we do it in a controlled fashion.

Equity can be had at any consumption level, but in an increasing population/decreasing resource scenario, the fair share is ever-diminishing. Hard to see everyone knuckling under that.

Fully agree with the last sentence; couldn't have put it better. We need to rejig banking for the low-then-no growth era. It may well be that the interest-chargers become obsolete (despite trying to monopolise transactions vis cashlessness) and it may be that debt-issuance has to be linked to proven real underwrite.

Agree largely PDK. This sentence stood out for me; "Taxing income earned from assets more, and income earned from wages/salaries less, makes sense." Taxing income is correct. Much of the past rhetoric has been taxing 'value' as in capital gains. But a capital gain is in itself not 'income' unless and until some move is made to realise it by either selling (which establishes an actual value, or borrowing against as a security). Many of the contributors in this forum do not seem to understand or accept this basic fact.

If the pollies are unwilling to increase taxation I cant see them nationalising the banks (until forced by events) and the problems of a successful autarky remain.....especially when all current plans are predicated upon the importation of resources and demand.

Can kicking has become an international sport and NZ is attempting to qualify for the world cup.

We believe to regulate this random world, to at least assert order rather than chaos, there's a lever level for each regulatory means. We do it for tobacco, alcohol, traffic control land/air etc.. now, you all need to be aware.. those words of growth, more, supply which lead to the words 'over' of everything? - are all back to the root: Credit $ supplied by Banks - Control measure should start from here. Majority Banks on the planet are always projecting/advocating growth.. is it not? how many bank is it advocating reduction? who knows, if we now have reverse mortgage? there could be a bank in the future that makes their profit? by actually give credit $ for reversal activity? - I wouldn't count on it, even Blood or Sperm Bank are asking for more growth/donors.

Brilliant critique. best thing on interest in a long time.

Government oblivious to monetary impact on inequality of income and of wealth.

"Independence" of central banks disguises their total lack of accountability to electorate plus the fact that large swathe of economic policy has been self-ring fenced off by politicians. Stalemate. Who benefits, as Jenee so well points out, utterly at variance with supposed ethics of Labour Party. NZ Labour Party is out of its depth I am afraid, on this.

I would go so far as to say that labour are not out of their depth and instead are a calculated progression of the John Key / Bill English Govt with a smiling face. This continued house price growth from untargeted QE at this stage can not be anything but intentional, the data is clear, house prices are rapidly growing, yet the QE is ongoing. Labour do not represent the workforce any longer but instead that 5 percent swing voter who voted for them for the first time.

Ardern is a phoney.

No she's not. She is doing what she was elected to do, lead the country with a degree of personality and charisma. she is like most politicians, not an expert in any subject but heavily reliant on expert advice. She like most politicians will not be able to take the time to canvass contrary opinions and views, canvass other expert opinions or research topics in great detail. That is why they hire staffers, and personality politics and personal agendas will play a big game here. Contrary views in any organisation are usually stifled before they get to the leadership, these are the 'filters' that lie below the highest levels. So JA is presenting the best view she can based on the advice she has received. On the other hand John Key could have been expected to have an understanding of matters finance and economy so he had no excuse!

So basically you are saying she is not a phoney - she is just clueless , therefore it is OK.

Only in so much as you and I are.

She is a phoney because her main policy platform since being elected is 'transformation', addressing inequality and poverty. She has done little to address those things, and is showing little will to do so.

As she is not following her rhetoric with actions, that is a phoney in my book, at least.

History may well judge Ardern to be nothing more than a charlatan focused on political survival

"Zip it sweetie" may well turn out to be a very accurate retort

Haha.. yeah. Paula Bennett should have stayed on, she might have taken up the torch from Winston in time for her quick retorts

At that point she will have become John Key 2.0

We need a Roger Douglas to squeeze the zit that is once again the central funding and protection of a favoured industry (property).

Both Nat & Lab provide their unpopular tool to RBNZ (eg. No DTI & Employment, apart from inflationary mandate), we all now rest hope on the shield of RBNZ independence.. they only have a short term window to make a significant/transformational changes.. I really do hope they're steadfast on their current course of negative OCR & more printing money, it's clearly beating the crap out from Covid19 economic dire predictions, this good momentum need to be maintain and amplified. NZ economy is the envy of the world now, let's keep moving 2021 is coming, more QE+FLP+negative interest soon!

Depressing, there are no quick wins really are there.

Why don't we just offer to write a cheque to young Kiwis to give up on their dreams in New Zealand, leave for another country and not darken our doorways again? Rather than building 100,000 houses we'll just get rid of about 240,000 kiwis (2.4 people per dwelling on average.) We could offer them maybe $10 or 20k each and for very little money we've solved that problem for years.

Maybe we could offer the boomers 10K each to top themselves?

Even if they haggled it up to 20k, the young would be on a winner.

:)

Didn't we have a referendum on this?

I've got a spare 15K if your estate wants to pick it up - would be money well spent.

It was called covid19....oh the irony

It's no use paying young Kiwis to leave if we then let in 50 or 70,000 less educated and less skilled migrants every year.

You're right of course. And why would we when the UK, Aus, USA, Canada, Europe are all willing to pay our young kiwis to leave anyway in the form of higher wages and more affordable housing? Something frankly insane has happened in our property market this year. Auckland is now more expensive than both Sydney and Melbourne

Average high earner in healthcare profession are clearly have much better opportunity in Perth, Adelaide, Melbourne, Brisbane, Sydney. For their income vs disposable towards housing cost and grocery bills - I only put Brisbane & Sydney in the last order merely due to that funnel web spider hiii..

I would argue , only about 10% of kiwis (at least in those working environments I've been involved , which is 5 different companies) can be considered as higher skilled and educated compared to the average person from "50 or 70,000 less educated and less skilled migrants every year" group. All others just think immigrants are so stupid and believe in all bul1$hit the other 90% bring to the table. The thing that they jump around the office trying to sound sweet and nice to the bosses (majority of whom are also clueless in most of the cases), fingerpointing to one another does not make them more skillful and educated. They just sound sweeter just because of lack of accent, and naturally being better in English. Anyway this is the often reason for promotion for many of them. Most of them argue that communication is huge part of success , however if they would be focusing on improving their skills and education we would all have much lower prices an higher quality in all areas of our life (not only in housing) as the frugality leads to higher productivity with paying less. Please don't even argue , i've been contemplating this for years . Want to be promoted or higher salary, don't waste time upskilling, just try sound sweet ..That's it

this is actually the reason why NZ will never attract best talents in IT, science etc. Just because NZ has different values, which is lower mortgage rates and what bank to choose discussed in the kitchen area with your boss . By the way , best talents normally very good with math, Pretty sure if you ask the best talen what would be 2 +2 , they will answer 4, whereas NZ monetary policies say it is 4.2 or 4.5

Life's a popularity contest.

Just play the game and suck up.

Less aggravation than sticking your next out.

Very good article Jenée. There are two points you failed to mention:

Firstly, the money being borrowed - that will have to be paid back largely by the young - those most likely to be missing out on house price growth and most likely to lose their jobs or suffer from low wage growth. It's a double/triple whammy for young people as a result which will see inequality (particularly generational) explode if nothing is done about it. This will be damaging for our society as long as it continues.

Secondly the governments programs ensuring employment continues to create perverse productivity incentives, which cause the ongoing zombie company issue. There are a lot of companies that should have gone under and their staff redeployed to more productive industries. This is a difficult but necessary part of pushing our economy higher up the value chain - i.e. increasing productivity. In many ways I think GR got this wrong, he should have provided a small cushion for particularly affected industries (e.g. tourism), not a mattress for everyone. His actions might look good short term, but the longer they continue the worse the issue. Smiths City (for instance) was about to go under, from memory, but government intervention has thrown them a massive lifeline. And remember - the money thrown at that is borrowed, so still has to be paid back, mostly by the young (see above).

The only saving grace for our future would be if the government were to expedite RMA and apprenticeship reforms, bring state housing projects forward, and fast-track large-scale housing and infrastructure projects. This would ensure the broader economy, particularly the productive sector, shares some of the gains from skyrocketing house prices.

A measly 7k increase in annual building consents issued in the 3 years to June 2020 hasn't been cutting it.

Increasing supply is no good if investors snap it all up. Home ownership is essential for our superannuation scheme. We're headed for future elder poverty like we've never seen if house prices don't come down.

Could not agree more. If an investor buys up all the houses built, then we have achieved nothing. Stop subsidising landlords with huge tax breaks would be a good start.

Rents are also primed further with accommodation supplements. Where supply is short these do nothing but raise the rents tenants can pay thus driving house prices higher based on yields.

Indeed. It's supply and demand.

We can have adequate supply of housing for the purpose of housing. But no amount of supply will ever be sufficient when the demand is actually for the government funded and risk-protected investment that is property in NZ.

Yes as long as there is seemingly unlimited demand( after all some investors have hundreds of properties), increasing supply won't achieve much because it won't keep up. And developers are not stupid enough to flood the market - they ration supply.

I get rather sick of this conversation, because as I have said many times the only way the issue will.be properly addressed is by the government building housing en masse for first home buyers. Get the scale and then sell at no profit. Then you will see 3 bedroom townhouses available for FHBs in Auckland at circa 500-550k.

But no one wants to know. Because there's only binary thinking - government builds state housing, private sector builds market priced housing. The huge chunk in the middle is neglected.

Prices not coming down for many reasons.

Need another solution.

I always dispute that we have supply side issues in housing driving up prices. You can see this from the last 6-8 months, we have added thousands of houses, with immigration flat to negative and prices still skyrocketed. This is at a time when heaps of AirBnBs have also come to the market as well as housing freed up from no students.

Really I think it's an efficiency issue, we aren't housing people efficiently and we most likely have a whole lot of vacant houses that are going up in value. Which to me is batty, they still have rates/insurance/maintenance to pay, so have overhead costs that aren't being recovered while they sit empty. It's not just here, China has something like 80 million empty apartments, huge ghost cities full of housing that is somehow maintaining it's prices. There are near enough whole streets of empty housing in central London, still maintaining or gaining in value.

The real reason why house prices are going crazy is the same thing that's being played out for the past decade or so - loose monetary policy and a lack of government action to stop the financialisation of housing. The availability of credit seems to be the only reliable indicator of price rises.

Your final sentence nails it.

Actually the effect of having net migration of 50-60k pa is still being played out despite it being minimal for the last 6 months.. If we tried having net migration of negative 50-60k pa for a few years, I can assure you house prices will come down.

It's hard to imagine that the effect of adding a lot more supply with lower demand would not be instantaneous - people have to live somewhere. I cannot imagine there is a lag to the supply/demand/price equation for housing, if indeed that is what is happening.

You see - I don't think we will see prices drop at all, in fact I am picking huge growth. We have financialised land/house prices and integrated them into our financial systems. And the central banks of the world have been printing money at such a rate that the money has to flow everywhere it can - but the economic system is only set up so that the money can flow into assets and land prices, instead of wages and inflation. The central banks are determined to do whatever it takes to keep the system going and can influence them simply with a few keystrokes and some policy changes. In such an environment, it's not hard to see why supply is no longer an issue.

Happy to be wrong about it, but the signs are telling me that I aren't. 15% price growth during a pandemic and simultaneous drop in world economic activity of move than 5%? That cannot be blamed on "pent up demand" or "increased demand" when over the same period we have experienced a severe drop off in demand.

All true (though incomplete) but how does one deflate a credit bubble without creating the problems it is designed to avoid?.. and meanwhile the RBNZ has its work cut out ensuring the currency remains competitive and the banks solvent...and all with the backdrop that the output mortgaged from the future will not exist.

Mr Orr must be a masochist

Rewards those who can think for themselves and not follow the Mike Kirk herd of sheep.

V reasoned

What ru on about with this “sheep” reference?

"who can think for themselves" = people who agree with me,

"herd of sheep" = people who don't agree with me

I've really been enjoying seeing monetary policy getting some heat from the media recently.

The audience here has been ranting about it for quite some time but it seems that even normies are starting to see the issue according to my unscientific reckons/observations at a family gathering last weekend.

Jenee – thanks for your work putting these issues into the spotlight. It is incredulous that our country is so passive on this sanctioned inequality.

How do you build wealth in New Zealand? Everyone here knows the answer. There is only one game in town: buy another house, pile on more debt, create another tenant.

Imagine if we built wealth by doing work; creating something of value, and were paid in kind for that value. Imagine!

Jacinda Ardern simply must begin using her political capital to do what is right for the country.

I want to see:

a stated median house price to income ratio target/strategy

a stated population target/strategy

I offer the following broad changes:

Further increase LVR for investors

DTI ratios for mortgages

Transition our monetary intervention from bank driven to helicopter money/tourism vouchers etc

Miniscule raise of OCR to indicate that the bottom has been reached

Land tax, no exemptions (eg 0.5% per annum, deductible from any other income tax being collected on the land use)

Ministry of Works-style direct government activity in infrastructure sector

If your Land Tax was aimed at housing investment (i.e. non owner occupied) it might have merit but what about other land holdings? (lifestyle blocks for eg). Besides, if a Land Tax was initiated wouldn't that outgoing just be added to the eventual sale price?

"Besides, if a Land Tax was initiated wouldn't that outgoing just be added to the eventual sale price?"

Yes. So as a buyer you are now getting less value for money. This is a price disincentive and will actually act to reduce prices long term rather than increase.

Kind of the opposite to first home grants; that on the surface seem to make houses easier to buy... but over time act to increase prices.

Buyers have been getting less value for money and lower rental yields for some time now but it hasn't stopped the inexorable rise in prices. I think any Land tax would just be viewed as another inflationary addon and either countered for at sale time or be adjusted for in rent rises.

Why would a buyer pay more for an asset that now has an extra liability? It's a heroic assumption that the seller would be able to add on the extra annual cost onto his sale price - more likely people will be keener to sell to reduce their outgoings, and buyers would be prepared to pay less.

That's a completely groundless assumption. The housing market is driven by lack of supply and easy credit, any tax won't have any more than a transient and temporary effect, there are plenty of buyers and a lack of sellers.

Westpac estimate a 1% land tax would lead to a 9.5% fall in house prices. I do note that they also predict a 4.8% increase in rents which supports what you have said further up the thread - perhaps we have a score draw.

https://www.interest.co.nz/sites/default/files/embedded_images/Tax%20an…

"The amount of revenue generated will be affected by any change in land values arising from the imposition of the tax. The 2009 estimate assumed that land values would fall by 16.7% in response to the imposition of the [1% land value] tax; a greater fall in land values would lead to a lower amount of tax revenue"

https://taxworkinggroup.govt.nz/sites/default/files/2018-09/twg-bg-3964…

Further evidence of higher property taxes being associated with lower house prices:

https://www.greaterauckland.org.nz/2015/05/18/do-property-taxes-affect-…

“ How do you build wealth in New Zealand? Everyone here knows the answer. There is only one game in town: buy another house, pile on more debt, create another tenant.”

So rather than waiting for a government to take action how about personal ownership of the problem..... Stop going out and buying up houses.

That's the whole issue isn't it? To those who have the funds there is no problem. You're asking people who can, to stop provisioning for themselves in later years - pretty big ask. Most people I know aspire to retire in comfort so knowing they have 20 odd years of expenses to fund post retirement, housing is the easiest and probably least risky way of doing it. Certainly Banks seem to agree.

Hook, won't be a comfortable retirement if there are a lot of young homeless and poor, they will simply remove it off the people they perceive who have created the problem,one way or another. It will turn a few good people into criminals. But the real criminals have already acted their part.

Happy investing.

The satirical side of me thinks we should pour some fuel onto this fire by further investment, anybody else?

Given the FHBs are only about 25% of the market it would seem the current model is working well for investors, and there is nothing on the horizon to suggest that will change. I'm not sure what you're alluding to re: criminality but inferring criminality (even morally) to people who are attempting to improve their own situation is unwarranted imv. Expecting the private investment sector to reverse course and become an altruistic or socially charitable entity is futile and probably ultimately delusional.

Yes that is the whole issue. If there is only one game in town, you are a loser if you don't play. And if you do play, you stretch yourself into debt servitude making everyone ahead of you in the game richer and leaving those behind you in the game poorer.

That's the thing though Ip.. investors don't really factor debt into the equation as it's just a figure on a spreadsheet if it's serviceable by rental income and they view the portfolio as just a retirement fund to be realised piecemeal at a later date.

Basically, yeah. To make money in NZ, buy property. Then the government transfers wealth from others to you.

"Imagine if we built wealth by doing work;"

That would mean rewarding people for that work. Yes nah, just import some more slave labour for farms, orchards, construction etc.

Don't you work on a farm redcows? What's your take home wage and are you provided with accomodation as part of your package?

It's a well known fact nobody gets rich by working for a living so what makes you think it will change now?

We need more articles like this. The disparity between what Jacinda claims to care about, and the reality of her actions, or rather inaction, needs to be consistently displayed to the public if we are going to see any real change in our course. I found this piece particularly good as well:

The cruel violence of ‘kindness’ and ‘unity’

https://www.newsroom.co.nz/the-cruel-violence-of-kindness-and-unity

"...celebrated globally as the most compassionate and empathic leader in the world. However, one can’t resist the feeling that her voice and smile are being used more and more as weapons against our most vulnerable and resilient, capable of disguising the cruel rejection of tangible and evidenced-based steps for change as fair and even necessary for the greater good."

"But it’s time to acknowledge that these messages can no longer be seen as just ‘politics as usual’. There comes a point where the blatant exploitation of our most vulnerable and resilient for votes becomes emotional and psychological violence that is added on top of the state-sanctioned violence of poverty and marginalisation. At this point, not only are our most vulnerable and resilient routinely targeted, manipulated, used, and disposed of by these supposedly “kind” politicians who they trusted to take care of them. They are then made to suffer in silence when these popular (and seemingly untouchable) politicians proudly and publicly deny them the means to live their lives with dignity."

Let's shut the RBNZ and have this conversation about monetary policy in the parliament the same as any other policies. We cannot have a non democratic institution ruling the lives of all citizens in the country. This way Labour will not have any excuses to whether they can or cannot do anything about this.

Thanks for all the work you do Jenee.

Jenée

Question

As interest.co.nz's political/economics reporter based at Parliament can you sense whether views and opinions published by commercial and independent media ever get any traction in the Parliament

What you write about has been written and commented about here at interest.co.nz, either directly or indirectly, over the 10 years I've been a visitor here. The only thing that is new is the current dilemmas are simply a variation on what has been going since 2008 GFC. The magnitude of the social and financial impacts are a product of ignoring problems which have now coalesced and collided

The wisdom of the crowd is blowing in the wind

Simple!,

when there is elephant in the room everyone ignores it ,

when this elephant grows everyone ignores it,

when this elephant grows more and poos everyone ignores it and swipe his $hit under the carpet,

no one washes the elephant an he smells and everyone tries to swipe him under the carpet too ,

when carpet can't cover everything -- guess what is done ??? Bring bigger carpet !!!

Our eldest son and his partner have just moved into their first home in Auckland. My son tells me, "it's amazing, we come home from work and know that no one can kick us out, or that the rent will just keep going up". They bought a house and gained a home that provides them with security, dignity and pride. Labour needs to stop being aspirational and start doing something. Aspiration requires action.

Congrats! It is terrifying how much people have to commit out of future cashflows for that basic level of security and stability. It's time for a long hard think about whether this is really the kind of New Zealand we want to be. Our mortgage is less than what our rent would have been by now by a long shot and we would have been sold out from under us had we not bought it. It will get cheaper when we refix in the not too distant. We were DINKYs and both working professionals - and it took an exhausting amount of time and energy to save and sort everything out, when in days gone by, it would have taken a fraction as long. For the people who can't make it work, life must be miserable. It shouldn't be like that.

they are just renting this house from the bank now for a fixed rate , for ,almost in every case , the rest of their best part of their life, if they can't pay that new rent for some reason - they will be kicked out the same way.

They have been sitting on the side-lines for the last four years, paying off their students loans and saving hard. $100k they saved. How much longer do you think they needed to wait?

I don't know , I am not saying they must wait , I am just saying , they did not change their status , this is just very weird form of "ownership" when you have to pay for the rest of your life and kicked out if you can't. In addition to new fixed rent they MUST feed insurance company regularly ,council with rates (not fixed ) for their life , but yes , now they can proudly say I "own" the house , we apparently just view ownership from the different angle.

Andreas_od they did change their status. It's called happiness.

believe it or not , I am not buying exactly for this reason (I actually can afford now to buy ) - because what I can buy (the quality and the financial burden for the rest of my life) will NOT make me happy. I see happiness differently. But happy for your kids if they are happy

andreas, you may well waste your time now. I have long given up trying to explain to young and often naive people that when you participate in multiple offers or auctions, then you can’t blame the sales people really. but nobody wants to “give way” in thids country, same issue you see on the road too...

Don't get too wound up about it Mountie - some people think a crash is due any second, but the problem is they've been saying it since 2008. Not sure how they expect people to put up with being turfed out of rentals or potentially putting off families for 12 years, but that seems to be what some people here think everyone should do. Maybe an easy attitude to have if you're older or much younger, but for some of us the clock is ticking and has been for some time already.

The irony is that they're not wrong about things being ridiculously out of hand. But practically speaking it's completely unrealistic for people to wait around for it fix itself. This overdue correction has been coming now for almost two old-school economic cycles, we're so far into the unknown that we're into stopped clock territory.

agree , without regular corrections, you'll have to review the definition of "ownership" at some point. You know how in other parts of the world the state of things where one entity was owning everything and all people were just renting from them was called ?? By the way in those COMMUNIties the renters paid $0 per month

For a laugh I thought I'd work out what the opposite of security, dignity and pride would be, to help me articulate my place in the world as a renter.

I think this is my best shot: Insecurity, subordination and shame.

Well done, Jenée - very nicely written.

Some economists, including central bank economists, have been working on this problem for some time, in the context of the way that tax polices and interest rate policies lead to large intergenerational transfers via their effects on the housing market. Indeed, the RBNZ hosted a conference at the end of 2018 that had several technical papers on these issues. Unfortunately, this work is not yet central to the main frameworks central bankers use, however. I suspect that will change in the next couple of years. It is not just young people that are being disadvantaged by very low interest rates and a tax system that favours people who save by accumulating bank deposits are also disadvantaged. But there are limits to what one central bank can do: if NZ were to raise interest rates when other countries do not the consequences for the export sector would not be pretty.

New Zealand has a tax system that is now radically different from the tax systems in place in most OECD, and one that accentuates the effects of low interest rates. So it could be the case that the effects of low interest rates are more pronounced in NZ than other places. The departure from OECD norms started with Muldoon and was continued by Douglas and Cullen. The problem has been building for decades now. There has been no political appetite to look at how the tax system disadvantages young people, and these days there is scarcely any recognition of how different the NZ tax system is from other countries (largely the absence of social security taxes). In fact it appears many older tax experts are proud of the differences and downplay the potential effects on house prices wherever possible - the Tax Working Group was certainly guilty of this.

Keep up the good work - and think before you borrow $800,000 for an Auckland shack! There are good reasons why gravity is very weak in housing markets, but eventually gravity wins. (The problem is your kids can age before prices become sensible.)

Although I am just a layman your reasoning makes sense to me - however ...

If I understand you correctly the underlying difference between NZ and "typical" OECD tax system is very low relative Social Security tax take in NZ , much of the rest flows from there .

Australia has Social Security tax take much closer to OECD average as well as CGT - their tax system seems to be much more in line with a "typical" OECD one ( am I missing something major ? ) - but they have a housing problem not dissimilar to that of NZ .

Perhaps the tax system is not the main factor in play after all ?

It's understanding how the tax issues work together with the other factors in the market. If your rental is going to turn a capital gain that comes out as more than the un-refunded portion of your interest-driven losses, then you keep buying more as long as they keep making gains. If you keep adding people faster than houses, it keeps going up. So people keep buying.

I certainly agree that tax is not the only thing important in housing markets. Supply restrictions, the quality of the transport system (and hence the premium people will pay to live on land close to desirable amenities), the speed of population growth, and so forth all can matter a lot.

NZ's tax system is different in at least three ways from typical OECD countries

(a) There is only a very small social security tax/ mandatory retirement saving schemes - the ACC scheme, but no contributory saving scheme. We differ from Australia (and almost all other OECD countries) in this dimension, which is one of the reasons why taxes on labour income are low and taxes on capital income are high.

(b) No CGT. This is relatively small, but we differ from Australia and most other countries here.

(c) The taxation of retirement savings accounts. Both Australia and NZ tax discretionary retirement income accounts on a Tax-Tax-Exempt (TTE) basis (money placed in a retirement income account is taxed when it is earned and so after-tax money is placed into the account; earnings are taxed; the money is not taxed on withdrawal) whereas most countries tax them an Exempt-Exempt-Tax (money placed in a retirement income account is tax exempt when it is earned earnings are not taxed when they are earned; the money is taxed on withdrawal). Money taxed on a TTE basis is effectively taxed at higher rates than owner-occupied housing, whereas money taxed on an EET basis is taxed on a similar basis to owner-occupied housing. Thus countries with a TTE system provide greater incentives to spend more on owner-occupied housing than other countries. The Australian situation is complex as the retirement saving system is compulsory, not discretionary, and the earnings on the account are taxed at somewhat lower rates (15%) than normal savings; moreover the Australian old age pension is means tested against the amount you have saved in the compulsory scheme, which for many people reduces the incentive to contribute additional saving. This means investment in owner-occupied housing is still tax favoured relative to investments in standard (non-compulsory) savings schemes. In many other countries in the world this is not true.

NZ's system means there is a large need for private retirement saving, because the replacement rate is low for middle and high income people; it means taxes on capital income such as corporate earnings, interest or dividends are high; and it means investments in owner-occupied housing and to a lesser extent rental housing are tax advantaged relative to other classes of investment, with the tax advantage higher when inflation is higher. This is a combination which countries do not find particularly sensible, and so most countries do not do this.

It is also fair to observe that these tax advantages for housing haven't changed for the last few years, although the extent of the advantage depends on the level of interest rates. The recent spike in house prices would appear driven by extremely low interest rates, and the prospect of low interest rates in the next few years - these depend on central bank choices. However, the tax system provides incentives that accentuate these advantages, and this is true to some extent in Australia as well as NZ. Unfortunately it is very difficult to untangle how much tax is a contributing factor as it is difficult to uncover how much people respond to the tax incentives - but it seems difficult to believe it is not a contributing factor. While I haven't looked for a couple of years, I think it remains true that residential housing wealth is a higher fraction of total wealth in NZ than in other countries, which is consistent with its tax advantaged status (although this does not prove that tax is a major cause of house prices).

It is worth noting that even if supply restrictions were a smaller issue (as they are in some NZ cities relative to others) there is still a tax incentive to pay more for land convenient located to nice amenities, which you can expect to be capitalised into the price of land. The extent that this is true would be smaller if NZ had taxed retirement savings on an EET basis.

AC

Very informative piece AC - well done.

You need an important no. 4 Jenee - amend the legislation governing the RBNZ, to change its mandate.

As an expat, got involved in a discussion with NZers y'day on why a burger at the White Lady food truck in the Auckland CBD has to cost $16. Sounds very fickle but you can get to much reality through these discussions.

because they have a mortgage to pay

It cost $16 because that's what the idiots will pay. Hope you didn't buy one. Saw the same thing in a small town near where I live - $8.50 for a basic hamburger. I was in Auckland CBD last year and was gobsmacked at the prices being charged. The term "ya get what ya pay for" has been completely ignored by both the consumer and the vendor.

No. I don't live in NZ at present and I wouldn't pay that price. Even $8.50 is not necessarily cheap for NYC or Singapore.

My partner ran a cafe/burger bar - production cost for a basic burger (buns, patty, lettuce, grated carrot, onion rings, beetroot and labour) was $1.75. Fast food is a money printer

The fact that it is a money printer that requires very limited expertise but very few Akld fast food joints (with the exception of franchises) are owned/run by NZ born people. Seems like a perfect business for many of our less skilled and/or less qualified, lower socio-economic families, especially when many of them reside in areas that are conducive to these types of business. Says a lot really.

Why do you think companies like Restaurant Brands are making money hand over fist in a so called downturn? The lower SE families are too busy buying MacDonalds, KFC and BK when they could furnish healthier meals for their families at a lower overall cost - reason?: it's easy, quick and they're addicted. It's always been the way and it'll continue to be the way.

These are the same families that walk out of Pak N Save with 10 packets of potato crisps and no vegetables in their grocery shop claiming that the price of produce is soooooo expensive.

Packet of chips -> $2 for 150 grams / $13.30 per KG

Loose Washed Potatoes -> $2.99 per KG.

Hear hear... always cracks me up the excuses expounded for poor food choices.. it only takes desire for change, planning ahead and a little work

If the RBA was a parent, then when its kids are on a trampoline it surrounds the trampoline with soft pillows to gentry catch and protect its kids if they bounce off the sides. This is very different to how the RBNZ acts. It decides to surround the trampoline with 1000% more springy trampolines so instead of cushioning the kids they are catapulted into the sky. The problem is those kids will have to come back down and who knows where they will land and in what state they will be when the do. The RBA's kids will be in a much better condition and will just brush themselves off and carry on. The RBNZ and Jacinda have massive egos that are going to destroy NZ for over a generation and nobody but Jenee seems capable of holding them to account.

If only there were another 100 Jenee's in our totally biased media.

And yes Ardern has an absolutely enormous ego.

Would be hard not to when you've been revered as having almost saintly powers.

I sometimes wonder, did they put something in the water of the 50%+ who voted for her who literally fail to acknowledge the bare faced facts of their failure?? The same voters who blatantly refuse to hear a bad word said about her lordship.

That is the cancel culture we live in now. Pretty hard to overcome facts in the face of total indoctrination only encouraged further by our socialist school system.

One of the biggest consequences of money printing and QE is the destruction of money as a store of value. Arguably, sound money is a prerequisite for society and economic growth and development. The U.S. is now trying to bully Vietnam to revalue their currency (the currency is pegged). Should the Anglosphere really be telling countries like Vietnam what to do?

Renters did not suffer under the 1st Labour government. Savage when faced with a 1 in 100 year economic depression used monetary policy to build 30,000 state houses at a time when NZ had 1/3 of the population it does now.

And at a time when:

- There was no RMA.

- No District Plans, Plannerz and other We Know Best overheads.

- It was perfectly possible to build one's own house (refer Norm Kirk...).

- Councils supplied 3 waters (barely), roads drains and bridges. Period. No 'social/cultural/environmental' Wellbeings....

- Many of the houses then built are still standing proud, despite the lack of all of the above 'helpers'.

Very well put. Now councils make developers supply everything, whilst charging them development contributions at the same time. $25k or so per section. Plus another $13k or so for a water connection, reserve contributions and on and on. And then they complain that developers are not building affordable houses.

Brendon and Waymad miss the salient point: Global population at that point was jusy ofer 2 billion.

NZ population 1.5 million.

Resources (including fossil energy) still available for consumption? Most of them.

And the difference is?

So many people, so many heads in the sand. Overpopulation/overconsumption/increasing competition equals more rules, more commandeering, more Enclosures, more Grapes of Wrath/Mein Kampf scenarios.

You cannot go back, without addressing population and consumption. Period.

There may have been no Resource Management Act. There were Town and Country Planning Acts which explicitly protected farm land against greenfield development, there was central government assistance for infrastructure, there was an active state house build, there was trade training, there was State Advances Corp assistance, there was capitalising on family benefits, there wasn't the current system of corporate welfare for landlords.

The Reserve Bank supposedly has inflation and employment targets. In reality it has only one target, to maintain the integrity of our banking system. It interprets this role as maintaining the profitability of the banks, hence it doles out money at virtually nil cost and permits the banks to onlend it where their margins are greatest. If this is to the detriment of first home buyers then they simply become collateral damage'

Basically, transfer wealth from the young workers and savers and old pensioners dependent on savings to prop up the banks and investors that overreached.

Great article, but can we please stop reinforcing the 'housing supply' myth? This myth is being pushed by developers who want de-regulation so that they can make more money more quickly. House prices in NZ are driven primarily by rental yields - and the market is *never* going to deliver affordable rental / shared ownership housing without intervention. The Govt needs to find a way of reducing rental yields - landlord licensing with high standards would be an obvious start (and would not break political promises).

The Govt actually assists rentals by Social Welfare to accomodate them in dire need, also Motels..etc.

Yep - monetary policy lowers interests rates and pushes landlords to invest and then govt pays rents that reinforce - it’s a race to the max yield

Nonsense.

Sadly, it's true. It's been a rort (but piggy-backed on a bigger).

And this lot won't buck the system.

+1 Jenee - spot on.

Also

"As shown below, real house prices increased almost three-fold between 2000 and 2018."

https://en.wikipedia.org/wiki/New_Zealand_property_bubble

Great article Jenee.

Suggest when you mention 'supply', you could also discuss ways to influence 'demand'

They are two sides of the same thing.

Bravo Jenee, what a great article.

You are a top journalist and your voice need to be heard.

Increase the supply of money, seems without consequences in the short term. But in the long term it will pop up regardless. Avoid real painful medication? for betterment? or opt for continue denial? or opt for gradual medication? - in absence of meaningful move by either left or right govt, then come RBNZ - We the five million team, really should support/encourage RBNZ to tripling the current QE & FLP moves, quickly to put neg OCR now.

Even before Queen-maker Winnie put Adhern into office I said she was the emperors new clothes! Still is, always will be!

Good article, but once again no mention of the demand side of things i.e. the mass immigration policy we've been following for 10 years prior to covid and will no doubt revert to asap.

All the talk is about "Building more houses". Not one mention of "Lessening people coming into the country because we can't house them".

The media is seriously guilty there;

It isn't a housing crisis, it's a population crisis.

And the plan is to import more volumes post-COVID to keep the ponzi going.

Remember JA only knew Supply side of the equation, yours advocating Demand, as you can see Covid eventuality is 'expected' for reversal.. now here comes the distortion, anyone expected RBNZ moves? building more houses or not, lessening people or not, it can be shown recently right? that if we don't like the equation natural outcome to become then we add, introduce, tweak the variables to satisfy the equation. In other illustration, is we're all in a life boat, about to sink as more people jump to it, then make no more people jump to it (phuih), but the boat still sinking in order to save the senior, we decided to throw out the younger ones, the boat start to float a bit.. more to be thrown out, some swam out, decided the boat is too toxic, may be it's better to meet quick end with the shark rather than be shackle enslave until die to serve the old de-facto side. NZ is always need to import peoples for the purpose of exploiting them for sure.

Remember, a majority of this government were born in the Neoliberal era. Mum and Dad failed as parents at teaching these Mellinials about there are always consequences and accountabilitys and responsibility for your actions ect ... they also dont like to be told what to do or been told no. But cosplay and social interaction and consensus decision making within the chosen friend group is cool. A failed State is a com'n.

Of course, hoarding of property, strangulation of land and building supplies and rampant migration settings don't have any consequences at all, right? Nope, definitely the millenials at fault. Maybe they don't like being told what to do by generations who have failed at every single at everything other than enriching themselves at the expense of the society they benefited from hugely in their own youth? If the state fails, it's because it was plundered long before millenials had anything to do with it.

And thats why #HistoryMatters. The 'M's' are supposedly the most highly educated generation of all, but have failed or have chosen to ignore to learn from, and have chosen to 'make-up' a new world they've reconfigured together to be better and easier than dealing with the realities that face us all. Eg; MMT, Social inventions like adding another letter to represent a new 'group' to the alphabet people that ignores science, history and evidence and facts.

More mining for disposable cars, circumspect analysis of what Green Wash'n Capitalism really is. All of this adds to the ebbs & flows of capital and where it ends up. And when you spook the market with false ideology, we get recessions and possible depressions?

We're doomed!

The solution is pretty straightforward: heavily tax all forms of speculative housing. For example, we could introduce an increasing asset tax rate on housing, like 2% p.a. on the value of the second house, 5% p.a. on the third, 10% on the 4th etc.

This will go a long way towards fixing the problem and it will also provide enough funds for delivering more support to the real productive part of the economy and to the average hard-working Kiwi.

Excellent article, thanks.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.