By Jenée Tibshraeny

Tens of billions of dollars are being pumped into the New Zealand economy, as like other central banks, the Reserve Bank (RBNZ) is “printing money” through its quantitative easing (QE) programme.

It’s buying New Zealand Government Bonds from banks and fund managers, freeing up cash for them to invest elsewhere. This bond buying is also lowering interest rates, giving businesses and households an incentive to borrow to invest to boost the economy.

Unlike other central banks, the RBNZ has never before lobbed what could be north of $60 billion into the economy.

The Government is by law required to leave the RBNZ to do its thing - use its tools to keep inflation and employment at target levels.

Yet Finance Minister Grant Robertson isn’t considering the flow-on effects of the seismic intervention the RBNZ is rightly or wrongly making in the economy.

He really needs to think about:

- What needs to be done to ensure that $60 billion gets to those who need it, as well as the most productive parts of the economy;

- How the cost of repaying the debt will be spread across society.

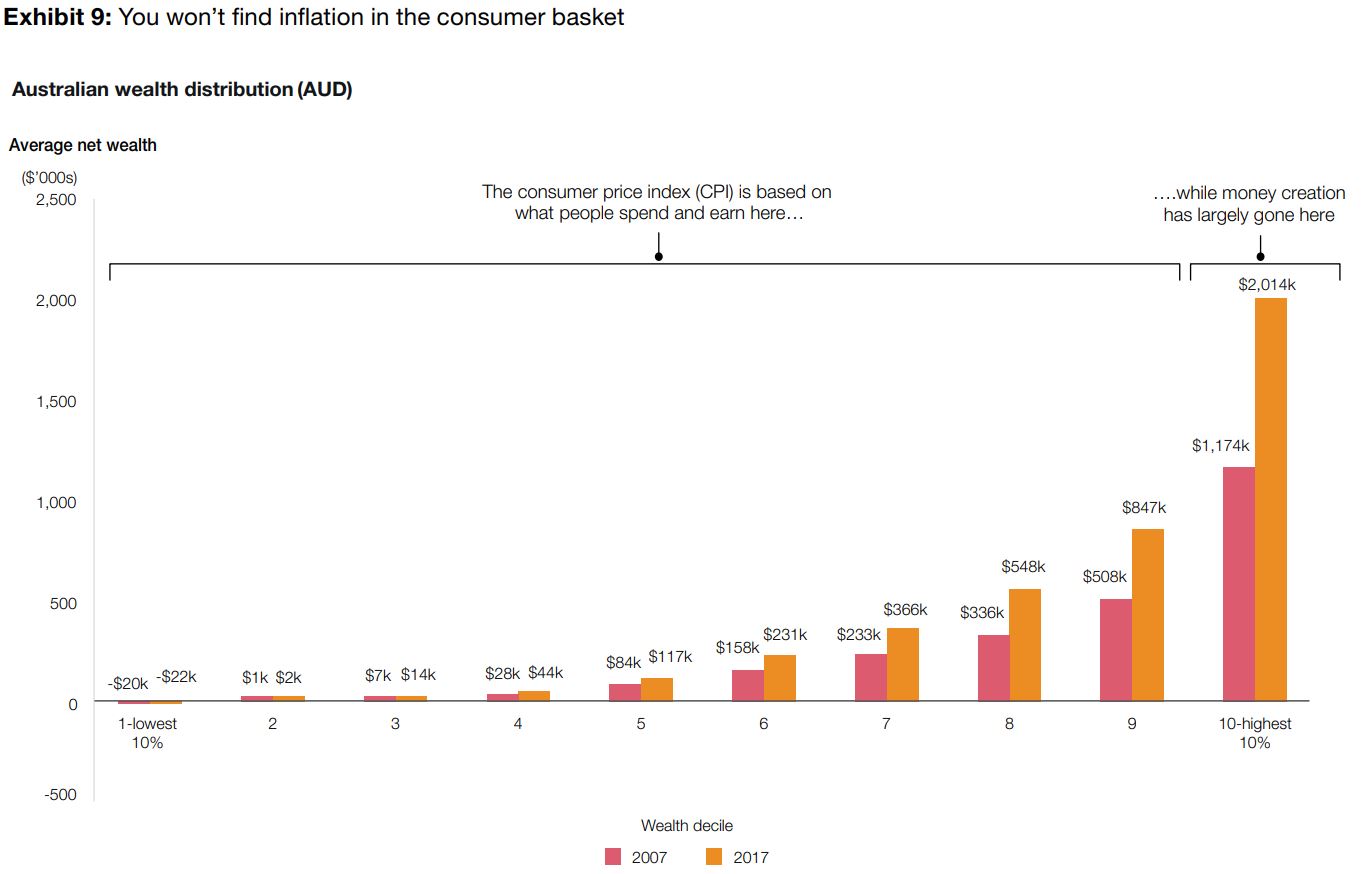

These issues are important because QE done after the 2008 Global Financial Crisis (GFC) contributed to asset prices - property and equities - ballooning, all the while inflation remained stubbornly low.

In other words, the cash didn’t flow through the entire economy. This graph put together by PwC in Australia illustrates how the money created went to the wealthy, asset-owning class.

While property prices are forecast to take a dip in the short-term, what’s to say that $60 billion won’t help pump them right up again in the medium to long-term?

There is an argument QE is already contributing to equity prices rebounding faster and much more than expected given the dire state of the global economy.

As fund managers have sold their government bonds to central banks, they’ve freed up cash to buy shares. What’s more, because share values have fallen, they’ve had to buy more to maintain the prescribed asset allocations of the funds they manage.

It’s still early days in the context of this crisis, and we’re undoubtedly in for much more share market volatility, but the point is, governments around the world can’t ignore the impacts of QE.

Robertson: Impacts of QE 'still to be told'

Talking to interest.co.nz, Robertson said his focus was on the direct response to the COVID-19 crisis.

In terms of the way the cash coming into the economy is being distributed, Robertson made a fair point: “A big part of the spending that’s happened in the last few months has gone straight into people's pockets via the wage subsidy scheme.”

He has previously said he isn’t keen on breaking away from the convention and enabling the RBNZ to buy bonds direct from Treasury with the aim of funding specific government policies, rather than with the aim of meeting its monetary policy mandate. An argument is that this could prevent the money from working its way into the economy via the banking system, which benefits those who own assets.

Robertson said the impacts of QE on asset prices were “still to be told”.

“I’m not yet seeing anything that indicates to me that that’s a major concern, but obviously we keep our eye on it.”

Put to him that it was too soon to see concerning levels of asset price inflation, Robertson said: “We’re very much aware of the potential for it and obviously after other crisis in the global economy we’ve seen those kinds of effects…

“For now, the financial system’s stable. Banks are lending in line with their policies and in line with the expectations the RBNZ has on them.”

Robertson also put the onus back on the RBNZ, saying it could employ loan-to-value ratio restrictions again, limiting bank lending against property, should the housing market overheat.

He wasn’t a fan of looking at the situation through an intergenerational lens, saying the Government’s response to COVID-19 would benefit all generations.

Looking at tax and the repayment of debt side of the equation, Robertson said the focus now should be on putting money in people’s pockets, not taking it out.

He said the Labour Party was still working on the tax policy it would take to the election. He couldn’t say whether the policy would be revenue neutral, but noted the prime minister had ruled out a capital gains tax under her leadership.

Both Robertson and National leader Todd Muller made the argument debt will naturally come down as the economy grows.

Muller said he wouldn’t increase taxes should his party be elected in September. However, he was open to tweaking the tax the system.

New crisis, same story

Clearly, with an election around the corner, politicians would rather keep the focus on how they’d spend, rather than how they'd repay.

As for looking at the way QE is done, and exploring whether the RBNZ could buy those bonds direct from Treasury, cutting out the banking system in the middle - it's complex and no one wants to risk “outside of the box” thinking looking like they want to turn New Zealand into a banana republic.

But most importantly, politicians don’t want to rock that boat in any way, shape or form to give people the impression their assets might be devalued.

This would of course be a particularly foolish thing to do at a time a pandemic is already shaking the ground on which the country’s $1.2 trillion housing stock is precariously built.

But a sensible discussion on changes that might be best made in the medium-term, needs to begin now.

You cannot throw a wad of cash a fifth of the size of the country’s annual GDP into the economy and hope it gets to where it needs to be, before the tab is tidily split according to how much different parts of society gobbled up.

105 Comments

Mohamed El-Erian, chief economic advisor at Allianz, says the stock market is in a "win-win" mindset as the Federal Reserve provides continued stimulus. He warns of distorted "zombie markets" and explains how some sectors will benefit while others will miss out during the economic recovery.

Beware not just of “zombie” companies but of “zombie markets” as asset prices become distorted and detached from fundamentals, warned Allianz chief economic advisor Mohamed El-Erian.

“I think we’ve got to be careful about zombie markets,” he said. “We’re not there yet, but we’re starting to get close.”

“Zombie” companies continue to operate by borrowing money, even though they are unable to pay off their debts. Record low-interest rates have contributed to a growing number of such firms over the past decade.

“They eat away at the dynamism of an economy, they misallocate resources and they eat away at productivity,” El-Erian said. “So you may be keeping them alive today, but it comes at a cost.”

El-Erian said “zombie markets” might occur when central banks like the Federal Reserve continue to prop up assets, destroying the market’s ability to allocate capital efficiently.

“Zombie markets are markets that are completely mispriced, they’re completely distorted,” El-Erian said. “Why? Because there is a policy view that you need to subsidize everything in markets for now.”

The Fed has taken extraordinary steps, including pledging to buy corporate debt and unlimited amounts of Treasurys, to keep the financial system running smoothly during the coronavirus recession. On Monday, the central bank said it would expand its purchases in the credit market to include individual corporate bonds.

The Fed’s aggressive actions have helped stocks recover from big losses earlier this year when the coronavirus pandemic started to spread across the U.S. The S&P 500 has surged nearly 40% since March 23, when the Fed first announced it would buy corporate bonds, even as parts of the economy came to a standstill and unemployment surged.

El-Erian said the Fed’s actions have created a “win-win” mentality in the stock market, as many traders expect the central bank will continue to buy assets including equities in order to prevent a financial crisis.

“The mentality of the market is if they’re willing to do high yield, they’re willing to do equities, because after all, the last thing the Fed wants is a financial crisis to make the economy worse,” he said. “The market feels very strongly that it basically is holding the Fed hostage.”

Thanks IO / That interview Came up on my YouTube homepage. What an eloquent speaker he is.... and makes a lot of sense too.

"The market feels very strongly that it basically is holding the Fed hostage"

Absolutely what is happening, The Fed and other central banks have lost control and the amounts they are printing is staggering, they will soon be buying all sorts of junk bonds and when they default that will be the start of the decline. It doesnt matter how cheap the interest is, if you arent making any money.

The Governments have not learned anything from the GFC and the rescue thereafter.

The Markets have learned a lot.

Your far to generous asking if they have thought about what affect this will have or how it will be repayed, your assuming they actually have a plan !

There is no thought of down the track its we have $20B extra to blow and we need to ensure we win the next election.

JPowell “We are not even thinking about thinking about the consequences of our actions”. Says it all really.

“A big part of the spending that’s happened in the last few months has gone straight into people's pockets via the wage subsidy scheme."

Yes. But it's not New Money! It's Replacement Money - no more, and in fact, less, than pre-existing Wages were. As has been repeated yet again in this article, all these artificial 'stimulus' projects don't get to where they are needed - they just pump up non-productive asset prices. And WHEN that fails, we will have expended huge sums of real money ( real, because it DOES have to be repaid) - and received - NOTHING in return.

Worse. We will have squandered the most important asset any country or individual has available to them - time.

"While property prices are forecast to take a dip in the short-term, what’s to say that $60 billion won’t help pump them right up again in the medium to long-term?"

Spot on Jenée, I'm not saying it's right but it will happen, despite the fact that I continuously get abused on this site for saying so.

(also the 2.65% retail interest rate will help "pump" values up)

You say it with such certainty yet we will in such an uncertain would. Would you like to change your 'will' with 'could'?

'right but it will happen'.

How do you predict the future with such confidence, I'm always impressed! Are you a sage or visionary?

Also note that the $60 billion will need to turn into wage increases and give the banks confidence to create even more debt for house prices to rise further. And if we have wage increases, there will need to be general inflation, and if we have inflation interest rates should rise to keep CPI within the 2% target bands. And if interest rates rise, how does it get easier to service the mortgage with even greater debt, to support even higher house prices?

Now imagine if House Prices were counted in the CPI. That would be a bit of a catch 22.

We need house prices to continually go up in order to drive the economy through lending growth, but how can house prices continue to go up if being measured in the CPI results in deviation out of that 2% target band ("inflation") and an increase in Interest Rates to combat? People borrow less as a result due to serviceability, economy contracts. Imagine that, house price inflation tracking general inflation?!??!?!!

Imagine an economy focused on productive enterprise instead of credit-bubbling up house prices for folk who received affordable houses from previous generations' efforts.

Imagine Burkean conservatives instead of pretend conservatives sucking on the welfare teat and draining wealth from surrounding generations.

I'm not sure if NZD is being sarcastic above - but its bizarre that as a society now we think that we have to create productivity via mortgage lending growth....

Yea that was a song by John Lennon

Is this sarcasm? I honestly can't tell.

Why do we need to drive the economy through mortgage lending growth? House prices should rise at the same rate as wages i.e. around 2%...but they haven't been recently, hence why we find ourselves up shit creek without a paddle.

But you've just identified how mad the current system is without realising it. Why else do you think house prices have gone insane since around 2000 when we start inflation targeting? But before that in real (inflation adjusted terms) house prices were flat?

I was pointing out how ridiculous the system is.

@indpendent , firstly inflation is dead , gone , we now have the reverse , which is worse , its called deflation .

Secondly asset prices are not a function of their face value / cost , rather there are a few other factors , like the cost f borrowing

For example if I buy a property for $500k and let it for $500/ week at 5% per annum borrowing costs I could break even with some skin ( equity ) in the game .

If I buy the same house at 2,5% interest , I am actually making money each week .

Then I go to the bank and plead hardship and get my mortgage 'interest only " on the investment property for 2 years ............ then I am really in the Pound -seats ...........its suddenly a cash cow

Easy-as !

Works fine while there are plenty of people with jobs and the ability to pay rent, I presume.

My fat finger reported you for that. Sorry.

Wanted to say it also relies on banks fronting up with more and more pretend money.

Yes we wouldn't have asset bubbles if we weren't attempting to maintain a 2% inflation target.

We would have had severe deflation post GFC, but instead we've pumped asset bubbles with lower and lower costs of borrowing.

How do you know we won't have inflation in 2 years, 5 years or 10 years time (many are predicting it), with the average FHB loading up with around $500,000 debt now to buy that average $700,000 home in NZ? What happens to interest rates under that scenario? (could be like the 70's and 80's again) Or are people fixing their home loans at 2.5% for 30 years, because you don't address that - you just consider what interest rates are now, not what they could be through the duration of the mortgage. 30 years is a long time. Any one would know who purchased a home in the 70's to find themselves with 15-20% mortgage rate 10 years later. Fine is the mortgage is small and wages rise at the same rate as inflation - but I'm hearing that we have stagflation ahead of us - price level rises (not house price, the general consumer price level), so does unemployment, but wages remain stagnant.

"inflation is dead"

Only the ridiculous definition of 'inflation' used by Central Banks.

I checked the composition of the CPI in NZ. According to this Stats NZ site, housing costs are included:

http://datainfoplus.stats.govt.nz/Item/nz.govt.stats/8b0860b8-cf63-4f12…

According to the above, the CPI has been reviewed frequently for over a century. For example, the 1948 Review has this on housing:

"The housing group incorporated the rentals of furnished properties, the cost of owner-occupied housing and rentals of unfurnished housing."

The 2017 review includes this comment on housing costs:

"Housing and household utilities remains the largest weighted group in the CPI. The updated weights show that $24.5 out of every $100 that households spent on goods and services covered by the CPI is on housing and household utilities, compared with $24.2 in 2014."

Do you have any info on where the CPI does not accurately reflect cost of living?

My understanding is it covers rent costs, the costs of housing maintenance and the costs of a newly construted dwelling - BUT THAT EXCLUDES THE LAND COMPONENT OF THE NEW BUILD! The majority of the price of the property market, buying an existing or a new home, is the price of land.

http://archive.stats.govt.nz/tools_and_services/newsletters/price-index…

So RBNZ keep dropping rates because the CPI says we've got minimal/no inflation - but at the same time house prices have gone insane because all of the new debt created at lower interest rates is flowing into the price of land that sits below the cost of the building. And each time they drop the OCR to generate inflation - it goes into the land value, but doesn't show up in the CPI. Its like a blind person tapping around looking for a door, not realising they're walking around outside near a cliff. Insanity.

If the land component was measured in CPI proportion to its weighting in the cost of a new build, the OCR probably would have been rising, not falling. We'd have far less debt and the price of the typical kiwi property might be half of what it is now. Everything would be in a much more balanced state, without the risk of a significant crash when we discover where the inflation was - it wasn't in wages or production, clearly.

It does not include the cost of buying existing housing stock or land (and so many houses in Auckland have CVs based on $750k-$1m land, $50k-$75k improvements). Only rents and the cost of building a house.. and i'm not sure if that cost of building includes the consents required, or just the materials and labour. Then you need to address the weightings in the CPI, and the hedonic adjustments.

Thanks IO and Pragmatist - I get it now. This gave me enough to find this link from 2016:

https://www.rnz.co.nz/news/national/311147/call-for-inflation-overhaul-…

eg. "Inflation is 0.4 percent, and Mr Eaqub calculates that if house price growth was included, inflation would have been 2.5 percent, or more, in each of the last three years. Council of Trade Unions director of policy Bill Rosenberg said households were under more pressure to make ends meet than the inflation figures suggested."

And look at this bizarre bit on the above page: "But Economics New Zealand managing director Donal Curtin isn't convinced the CPI needs to be overhauled. He said the Reserve Bank governor, Graeme Wheeler, understands the dilemma he's in when confronted with low inflation - which would suggest a rate cut - and an overheated housing market - where he would lean toward a rate hike. Unfortunately he can't use the same instrument for both things cos he needs to raise it on one side and lower it on the other. So that's not do-able."

Seems Mr Curtin believed the CPI can't be fixed because inflation (as measured by the CPI) is low. Hahaha!

Why do you think inflation is linked to interest rates? Roger Douglas raised interest rates to drive inflation down, and it worked. With US$550 trillion owing round the world, don't think the powers that be will allow any interest rate increases. We can bet the farm, literally, on that.

That is wrong.

Inflation is of course linked to interest rates because it limits the amount of debt (money supply) that can be created by the banks. If the rates are higher, they can't issue as much debt because people can't service the cost of it. Reducing the amount of issue debt, reduces prices, reduces inflation.

We've flooded our markets with money, but its flowed into capital asset prices, such as land that aren't measured in the CPI. We've got inflation...it just hasn't been measured. Have a look at the quantity of money supply (which in theory is the historical measurement of inflation) - its been growing, but inflation hasn't been because it isn't measured properly.

Read as it may not just be Fed but many reserve banks facing the same problem :

https://www.ccn.com/federal-reserve-trying-to-talk-out-prison-created/

NZ government by default has made many business make heaps of money (Instead of supporting made them richer) at the cost of tax payer. Suport is good but not free distribution to one and all. Result of improper planning and execution by current government.

100% agree with :

He really needs to think about:

1 : What needs to be done to ensure that $60 billion gets to those who need it, as well as the most productive parts of the economy;

2 :How the cost of repaying the debt will be spread across society.

Next support should be to industries that are afected / unable to operate because of border restriction and were doing fine before the lockdown.

Of course Jenee's assertion is correct .

If I had to get a slice of that $60, 000,000,000 .00 and it was cheap enough to borrow , I would almost certainly buy my very first residential property investment .

The stock market is again looking too risky for me and zero returns on cash means I have no alternative for passive investments

A few problems here. To optimize returns in a neo-serfdom society, you need as much as the housing stock as possible to be rental. With investment all flowing to becoming 'the landlord', the small investor would soon become irrelevant.

But this is all antithetical for a modern consumer society shaped by democratic and individual freedoms, which NZ likes to think it is. The neo-serfdom dream is quite bleak really and better illustrated by countries such as Cambodia.

This is why I've been asking the question for a while - 'how many people can try to get ahead of other people by becoming landlords before that system fails?' Looks like homeownership rates have fallen dramatically but not everyone can be a landlord, eventually you run out of serfs.

@independent , dont be silly now , there will always be people who will never qualify for a mortgage , and that number is never going to come down, its just going increase , its just the pace of increase that will vary from time-to-time .

As long as the sun rises in the east and sets in the west there will be tenants in New Zealand

My advice ............Get used to it?

For sure - but that is avoiding the question. How low do we want our homeownership rate to be? If you have teenagers now, are you happy that landlords are going out buying up all the houses that could be used as family homes for your children?

I thought Boatman's kids still lived at home with him? Maybe that's changed.

They are 19 , 23 and 25 , and yes they all moved back home during lockdown .

The youngest is a second-year apprentice with an SOE ( or almost SOE , Government largest shareholder )

The middle one, a quantity surveyor has saved 100k towards a home

The eldest is is in her final year at Medical school at Auckland Uni , but has missed a semester , so will not grad this year .

They are all intelligent enough to understand that Landlords are not to blame for house prices

Are they intelligent enough to realise that landlords' votes and advocacy have played a significant role?

Obviously doing the wrong degrees.

It sounds like a have a pretty solid whanau!

@independent ....here we go again , blaming landords !

Please explain to me how landlords are able to fix high prices at an auction ?

Logic suggests the landlords would want to pay as little as possible for an income generating property in order to maximize the yield

And , its a fallacy that landlords are buying up "all the houses "

The prices of secondhand houses are influenced by the costs of new builds and simply track the horrific costs of construction and land ............... this has nothing to do with landlords

Landlords are simply one cog in the gearbox , there are the Banks , the agents , the sellers , land prices , and costs of replacement ( building ) and borrowing costs ..........all influencing prices

Blaming landlords is just lazy thinking that fits a stereotype

I've always seen it as a supply/demand question. Aspiring landlords create demand, which pushes up the market clearing price for a house. Ergo, landlords increase house prices. Simplistic, but if all aspiring landlords dropped their aspirations there'd be more houses to go around. On the other side of the equation, FHB are desperate not to be tenants, because being a tenant sucks dirt. This desperation doesn't create demand, but increases their willingness to pay, which is another function of price.

Yes and for many landlords, instead of having to save a deposit, they just use equity in a previous property to buy more property. Gives the market pozni type characteristics - yet the FHB has to save their deposit. And it adds to demand. Instead of one home one family, you have one home and one family and one landlord attempting to purchase it. The effect of those marginal landlord buyers/pressures could have significant upward forces on the market. We will find out on the way down if many have been interest only and buying only for capital gain.

"Please explain to me how landlords are able to fix high prices at an auction ?"

Investors are a marginal bidder - marginal bidders push up prices, fact.

Without them in the room prices wouldn't be inflated.

And they use cross-collateralised equity.

That is considered madness in other countries.

@independent , dont be silly now , there will always be people who will never qualify for a mortgage

That is the point being made. That is the idea of neo-serfdom.

Yes think it has a limited life span.

Unless it goes hand-in-hand with Noblesse Oblige.

Isn't that what has been happening, in America towards the black population at least, but it would appear they've just realised how badly shafted they've been getting.

I'd have said it was happening towards the lower and middle classes in general. Why has everything suddenly become about race?

Its not entirely, but look the average wealth (assets) and wages of the black community across the US. They are generally speaking, living in a different class to the white citizens. Obviously there are numerous exceptions to that, but the statistics are quite clear.

Check out these charts and note the one on how the black community aren't catching up to the white community:

https://www.nytimes.com/interactive/2020/04/10/opinion/coronavirus-us-e…

Because it's relevant..Overall, incomes in black households are about 40% smaller than those in white households, and black men earn up to $1 million less than white men over their lifetimes.

This is why I've been asking the question for a while - 'how many people can try to get ahead of other people by becoming landlords before that system fails?' Looks like homeownership rates have fallen dramatically but not everyone can be a landlord, eventually you run out of serfs.

The idea of a nation's wealth being generated by rentier economics to its serfs is rampant across the Anglosphere, but particularly in NZ and Australia. And you're correct, if the rentier economic model is infallible, the whole thing will be swallowed by corporates.

Tens of billions of dollars are being pumped into the New Zealand economy, as like other central banks, the Reserve Bank (RBNZ) is “printing money” through its quantitative easing (QE) programme.

It’s buying New Zealand Government Bonds from banks and fund managers, freeing up cash for them to invest elsewhere.

That's blatantly not true.

The RBNZ exchanges reserves for the securities it purchases from authorised investors - these reserves remain on the RBNZ's balance sheet paying out OCR until the bonds are sold or expire. Private investors have merely swapped a fixed rate government asset for a floating rate one. In exactly the same manner they previously swapped their savings from deposits to the government in exchange for newly issued Crown debt. Which is where state deficit spending funding originates.

And, as you rightly say, the RBNZ LSAP programme primarily encourages banks to underwrite (invest in) new government debt to further exchange it for new floating rate debt at the RBNZ. But it certainly is not being invested elsewhere. The government is undertaking that task directly from investor's bank savings and crowding out the private sector in the process.

There is no crowding out as bond sales do not fund the government. It is the governments own spending that first creates the bank reserves. Commercial banks cannot create their own reserves. As Prof Bill Mitchell says "it is not to finance net government spending (outlays above tax revenue) given that the national government does not need to raise revenue in order to spend. Debt issuance is, in fact, a monetary operation to deal with the banks reserves that deficits add and allow central banks to maintain a target rate"

http://bilbo.economicoutlook.net/blog/?p=32883

Debt issuance is, in fact, a monetary operation to deal with the banks reserves that deficits add and allow central banks to maintain a target rate"

So the government issues this bank underwritten IOU (bond) costing significant syndication fees to put a floor under the OCR and the RBNZ turns around and buys them back from the market, almost immediately, to hopefully lower already low term interest rates and clearly signal an easing bias?

- Final order book at NZ$14.278b at the final level

PRICED - NEW ZEALAND GOVERNMENT NZ$7b MAY 2024 NOMINAL {NZ} ***

Issuer: Her Majesty the Queen in right of New Zealand

Issuer Rating: Moody's Aaa (Stbl) | S&P AA+ (Pos) | Fitch AA+ (Stbl)

Instrument: New Zealand Government Bonds ("NZGB")

Amount: NZ$7 billion

ISIN: NZGOVDT524C5

Launch: 15 June 2020

Pricing: 16 June 2020

Settle: 23 June 2020 (T+5)

Maturity: 15 May 2024

Coupon: 0.50% s.a

Margin: NZGB 5.5% April 2023 (mid) +9bps

(NZGB 5.5% April 2023 - FIS01 on Reuters, ICNG01 on Bberg)

Yield: 0.4275% s.a.

Price: 100.2796388105% plus 39 days accrued (0.0529891304%)

Denominations: NZ$1 million (Primary subscriptions)

Selling Restrictions: Offshore Selling Restrictions (refer IM)

Bookrunners: ANZ (B&D) | DB | JPM | WBC

Embargo: There will be no 15 May 2024 nominal bonds offered for tender prior to September 2020

Documentation: IM (25 March 2020)

https://debtmanagement.treasury.govt.nz/sites/default/files/information…

Product Disclosure Statement (25 March 2020) (where used in compliance with the Financial Markets Conduct

Act 2013, available on request. See section 6 of the IM)

Other: NZClear/Clearstream/Euroclear; NZ law; Not listed.

Bill Mitchell calls government bonds corporate welfare. "In this Part, I consider those justifications and conclude that the on-going practice of government’s issuing debt to the non-government sector is primarily an exercise in corporate welfare and should not be part of a progressive policy set".

http://bilbo.economicoutlook.net/blog/?p=45108

Edit:

Yeah I was still operating on the March 16th statement. Wasn’t up to date they’d adjusted those till now cheers

OK MMT teaches us the following.

QE is an asset swap. Bonds for cash. It doesn't make the private sector any richer wealth-wise. It makes them more liquid. Pros - it reduces interest rates a bit. Cons - it can cause asset price inflation. It is not that 60 billion of QE means 60 billion of extra spending in the real economy.

Fiscal stimulus - i.e. government deficit spending - well that is extra money going into the private sector. When the government spends more than it taxes the private sector ends up holding more wealth (as bonds or reserves) as bank accounts are credited. Deficit spending - unless you believe in Ricardian equivalence which never seems to empirically hold true - is extra spending in the real economy. Pros- it gets people employed and supports demand. Cons - no cons as long as you don't push beyond the productive capacity of the economy. But of course better to spend on the bottom end of town and on productive investment. So 60 billion of QE is not pumping new wealth into the private sector. 60 billion of fiscal stimulus - i.e. deficit spend - would.

Thanks cs, I like your "simple to understand" explanations !

So if QE does not provide more money to the market, why does it lead to asset price inflation in you opinion?

A high level of liquidity preferences, the low level even lack of economic growth to provide opportunity causes investors to seek refuge in what they consider to be safe liquid assets. The consequential rise in sovereign bond prices reduces term interest rates, which in turn increases the discounted present value of cash flows associated with all assets. This encourages investors to capitalise such an outcome in other asset classes. Speculation follows on quite quickly when bank offers of leveraged, collateralised borrowing allows a larger cohort of capital deficient participants entrance into the casino.

Given that interest rates are near zero, at some point the stimulus needs to result in wage increases, greater than the rate of inflation - otherwise how else do we pay for ever increasing debt, to cause house prices to rise? Its falling interest rates that has allowed it the last 30 years. But that would now appear to be gone. (i.e. mortgage rates are pretty much zero). Otherwise debt is rising faster than our rate to service it, even at near zero rates and eventually someone can't pay and it looks more like a ponzi than a market and the first to exit win.

cs, could you please translate Audaxes post into layman's terms?

Yvil - what he is saying (in normal speak) is driving interest rates to zero entices people to speculate on asset prices using leverage/mortgages/debt - such as property.

Correct, basically whats been happening since Alan Greenspans days at the Fed...and it won't flow through to higher wages either as we have seen, employers have the view that since interest rates are lower the cost of debt must be cheaper for employees who can go get a payday loan instead of a wage rise. Or quit their job and become landlords and make a living out of otherpeoples inability to get a mortgage...

Yes my personal view is that paradigm/system isn't sustainable long term.

but this time is different. Productivity has been decimated while the money supply is increasing. Also there's been a switch from monetary to fiscal policy. The next 10 years probably wont be like the last.

So big inflation you think?

Yes its why we've seen people at times making more money from the price of their house than wages. Its nuts and completely unsustainable.

Not in my view, its about confidence, you don't have any in the future you dont borrow regardless.

If you have no clue if you'll be able to eat next week speculation is not what people do.

If your confident in the economy and your job people borrow.

want personal economic confidence? join the army and guard covid isolation hotels in a barely used LAV armoured vehicle!

Just saying.

"While property prices are forecast to take a dip in the short-term, what’s to say that $60 billion won’t help pump them right up again in the medium to long-term?"

That already appears to have happened with the share market. The abundance of cash seems to be the driver, not the fundamentals.

In this crazy abnormal world nothing seems certain at the moment.

As to property, I am still "cashed-up, watching and waiting" - but I am also adding "hoping" to that. .

As to the share market; I had my eye on a couple of low risk, potentially less affected, companies. However given the market's recent performance it may be a missed opportunity for the best result.

The comment suggests that the property opportunity may likewise also be reasonably temporary.

When do you plan on entering back into property P8? 6 months time or foresee a longer lag?

ydb

I don't think that there is enough sound property data out at the moment to really determine where the market is at, and especially how significant the fall is likely to be. The current state of the share market - if it holds - suggests that QE and interest rates may have some significant influence on the extent of the fall and somewhat counter the full effects of unemployment and economic uncertainty.

I am tending to continue to listen to RBNZ and bank economists who are expecting around 10 to 15% fall and will be interested in any re-evaluations of these.

I am also keeping an eye on auction data as that is the most immediate available (that week) but is selective and small sample size; also on REINZ data but that is on settlement of sale so includes negotiated agreements commonly up to eight weeks previously, and also Core Logic Data (which also fuels the algorithm estimates) is over a three month period so notoriously slow in picking up changing trends.

If the downturn is protracted, then I will be looking at RBNZ mortgage data and any upturn in the "number of mortgages to investors" as a possible indicator of when investors (those with knowledge and experience of the market and prepared to put their money on it) feel that the market may be bottoming . https://www.rbnz.govt.nz/statistics/c31 - Excel sheet column E4

Keep in mind that I am looking at property for an investment and not a home; I think you ask as a potential FHB.

To FHB, my previous postings stand - if one has reasonable income security, then housing affordability is going to get better due to lower house prices and interest rates. Buying one's first house is not an overnight decision. From a definite decision to actively look to seriously buying and actually buying there is a period of a commitment to extra saving, researching the market by looking at properties, discussing and agreeing with your partner on the idea home on the basis of looking at those homes, and talking to lawyers, bank manager, family - and all that may take six months to a year.

So if I was a FHB, I would be starting to seriously consider things now (not buying) in anticipation of the likely fall in house prices and improved affordability.

If picking the bottom of the market is a major consideration, then I would be looking at "the bottoming of the market" rather than "the bottom of the market". A further 5% drop in the market is probably less than the difference between buying well and buying poorly.

Two factors more important in buying a FH compared to the state of the market are;

- firstly, currently how secure is my/our income and my/our ability to service the mortgage, and

- secondly, is the house what we want and does it currently suit us (keeping in mind that it is the first step on the property ladder).

Once you buy, remember it is a home - it is about financial security, security for you and your family, and its intrinsic value. Short term fluctuations in prices are irrelevant provided you can service the mortgage and are prudent (e.g. paying down the mortgage).

Personally I see some falls and subdued prices for some time. However, equally significant to the potential of a bubble burst is that - as following the GFC - the cheap and abundant money led to a decade of house price inflation and growing affordability issues.

Being prudent - such as paying down the mortgage - should better protect one in the event of an unexpected significant negative event such as a property bubble burst, a resurgence of Co-vid 19 and economic chaos, loss of income, illness, serious accident, marriage break down . . . . . Its like crossing the road - there is always the risk that the big red bus will get you, but you are prudent, chose the most appropriate time you feel is right and then you cross the road.

Thanks P8. I've actually got a home already and both of us have rock solid employment for the medium term. We bought nearly 2 years ago so we bought before the peak - new home in favourable area with large section. I ask because my sister and her husband are currently looking to buy their first home. They have very cheap, quality military housing currently and have a fair bit of Kiwisaver.

The problem is that everywhere they turn, people are telling them that they must buy immediately to avoid missing out as prices will continue to skyrocket. My personal advice to them was that they should wait as they have accommodation thats good and the world is experiencing economic downturn. Given that house price levels are predicted to drop, I tried to articulate that they take no risk by waiting 6 months. The risk is buying now then seeing 10-15% come off their equity. Thats my take anyway

ydb

Congratulations

Although you "bought at the peak" you both have rock solid employment, and seem happy with your home so you have no issue.

As mentioned home ownership is long term and short term fluctuations are irrelevant. As I have previously posted I purchased an investment property shortly prior to the GFC and the RV in 2009 was just over 10% less than purchase price; when I sold in 2016 there was very reasonable capital gain.

You will appreciate what I mean about financial security, security for you and your family, and intrinsic value of owning your own home.

As for your sister, only she and her husband can decide; there will always be conflicting advice and at the end of the day they need to critically evaluate the range of views themselves. There is certainly some advice I would listen to, and certainly other I would very quickly dismiss.

I wish you, and your sister and husband well in the current fallout from Co-vid.

Its hard to say if we did buy at peak. Recent bank valuation put it at over 100k more than we paid but I'd say thats about to change. Anyways, thanks P8 I value your balanced insight

REINZ data is not from settlement date. It is from when the sale goes unconditional - so much earlier than settlement. It's explained on this page: https://www.reinz.co.nz/reinz-hpi (Search for "unconditional date").

The rest of what you wrote seems pretty reasonable.

househunter

You are correct. Apologies!

Does it take into account private sales?

$60 ,000,000,000.00 ............thats about enough to get us drunk on liquidity......very drunk

No chance - even the Fed's QE $trillions is not helping the illiquid.

As Jay Powell’s QE regime is much larger, notice how, too, the private selling is likewise much larger. Two months in a row of numbers beyond compare. And, as I wrote above, history has shown this is only the beginning of behavioral changes that eventually wreak more havoc down the line.

Liquidity preferences. Logical and perfectly rational responses to what QE and bank reserves actually are. Not money.

Foreigners aren’t selling because they hate us, hate Donald Trump, or just hate the dollar. They’re selling because they’d love to be able to get their hands on some, but, despite Powell’s mythical flood, they can’t. At least they couldn’t through April when, curiously, the “flood” was at its highest. Link

{kind=link}

It's got to a point where it needs to be pumped forever, with wealth being accumulated by very few and growing civil unrest.

Renters Association protests outside NZ Property Investor Federation meetings?

It's got to a point where it needs to be pumped forever, with wealth being accumulated by very few and growing civil unrest

Short, succinct and focused. I completely agree with you. This is where the majority of people are unaware what's really going on.

"History!"

Well , on re-reading Robertsons comments , he is basically saying the wage subsidy scheme is our very -own version of helicopter money

Yep and when that runs out, say at xmas because they will need to keep it going given the amount of unemployment , and we still got borders mostly shut. What then, the money has been mostly spent on day to day living expenses, the economy is still in recession, the government has not come up with any real big think ideas to create large employment or stimulate the private sector to encourage hiring (as at moment they are reducing staff numbers daily)....I think a lot of people are thinking the WS will go on forever.

I have a feeling that when the wage subsidy stops, then everything stops.

Why would anyone have thought otherwise. I thought the fact it bolstered business cash flow at the same time was pretty good, better than straight helicopter.

There is another way. Incentivise the most productive:

1 Refund tax paid in prior years to the most productive businesses, eg by repaying GST paid last year, on a month by month basis to all businesses under a certain size. Do it now.

2 Consider refunding income tax paid last year, on a month by month basis to individuals and businesses under a certain income.

This is fair, proportional and targeted, as the most productive businesses will have paid the most tax.

Yep but that would require less Tax and Labour is not about that, they want more not less and to look like they are helping you out.

They would prefer to give to the employee and don't realise that if you lose the small business jobs go.

What Labour even dopier than National? Surely, not? Or is it that the bureaucratic machine must be fed and complexity is their blood sucking leech?

Please.... been hearing that QE is money pumped into economy for years. It is not. It is solely designed to keep interest rate down on gov debt. Other than that it did sod all for UK or USA in 2008-16

$60 Billion in increased liquidity is now available due to the Reserve Bank Governor trying to provide the only support he is able to provide under his mandate. He can't make Grant Robertson spend the extra money in the real economy, he can only allow the means for this to happen. Adrian Orr has done the right thing.

Grant Robertson is making a political calculation that there are more votes in being seen to be fiscally prudent and doing the bare minimum to limit the economic damage than there are in filling the economic hole left by Covid. The good ship New Zealand's crew is being told to fix a $50-60 Billion hole in the ship's hull with enough material to cover a quarter of the hole. It's not possible to fix the hole in the real economy with so few resources allocated.

The situation is not static. The multiplier effect will come into play. The hole will get bigger. People will lose their jobs, their companies and their assets. Spending will decease still further. More government money will be needed to stabilise the economy even at a lower level.

People who are moaning about how much the govt is spending now will be shocked to find out how much the govt will have to spend later to staunch the bleeding. Not acting to fill the $50-60 Billion hole now might be smart politically but it is bad economic management. Refusing to use 'helicopter money' when it might have been politically viable in the early days of the outbreak is in my (minority) opinion, sheer stupidity.

So the $60 Billion in increased liquidity will seep into investors hands over a lagged period of time while at same time the real economy is stalling. Prices for good income producing assets and property that will retain value will increase at the same time as people are losing their jobs and businesses. The govt of whatever stripe will have to react either by spending more to support the real economy than they would have had to if more had been done earlier or by enacting an austerity program for political reasons that will make a terrible recession inevitable.

Agreed. QE is a $60 billion asset swap for investors/banks. Their total assets have not increased; they do not have any new net worth to spend into the economy. QE without fiscal policy is completely useless. All private bond-sellers can do is bid up prices by swapping private assets back and forth. Fiscal policy, through government deficit spending, is the only way to inject new net financial assets into the economy. Also, we don't know how big the economic hole is, it could be $100 billion for all we know. The government needs to "go hard, go fast" with fiscal policy, and keep filling the hole (deficit spending) until we see evidence that the hole is full. Once the hole is full, then we should leave it alone, we don't want to pointlessly tax our way into a recession - the public "debt" doesn't need to be paid back, via QE it will be owed by the government to itself.

On planet Bakery an innovative Baker builds a machine that makes five pies a minute and is much cheaper to run than the three bakers he had before. He has lowered costs and increased productivity. He buys out all the local bakeries and automates them. Now the local district is flooded with pies and starving ex bakers. Since its planet bakery and there are no other jobs the economy collapses, there is social and political disorder and hardly anyone can afford the pies they used to make.

Before the end some of the laid off bakers started making artisanal pies that were nicer and far more expensive. But the Inovative Baker fought back using big data and machine learning creating custom pies for more discerning customers. Until they too could not afford the pies. The End.

Yet, that is how the modern world was made. A paradox.

https://www.telegraph.co.uk/business/2020/06/17/four-hundred-years-brit…

If the baker's profits aren't redistributed, then he goes out of business and the whole exercise is pointless.

Paywalled. But I can guess some of it. AEP is prone to hyperbole but usually excellent. The thing is that one must be exceedingly careful as to how "rich" is defined. Arguably the world has never been richer than it is now. After all there has never been more money available for pie making machines. But no one is building them.

This has happened before, including in GB at the height of the industrial revolution. Money flooded in but it was typically recycled out again because there were no more good investments in GB. Because, same as now workers could not retain a sufficient share of income to generate enough demand to warrant further investment. GB was rich but the wealth was so uneven that the economy as a whole was extremely weak.

The world may well be richer, but also the share of gdp going to capital has never been higher and to labour never been lower. This is the whole Piketty thesis.

So the most intelligent bloke of the lot is Tod Muller doing everything possible to avoid getting elected in September. And Winston throwing his chances of being a government partner under the bus as well. Very smart, both of them.

Helicopter Money is one thing we have not yet tried. Why not try that also and see how it works for us ?

I'll take it and spend it!

Bit of a joke isn’t it.... another poly with short term view and election on his mind!

Where's it going you may ask ?

While some may have gone to the wage subsidy , its as clear as a sunny day a lot is going into speculative activity on the NZX and the ASX and i guess some is going into property speculation .

However you look at it , its evident that its not going into any long-term sustainable development .

And its real easy to get your hands on cheap money to speculate , the Banks are awash with the stuff

"These issues are important because QE done after the 2008 Global Financial Crisis (GFC) contributed to asset prices - property and equities - ballooning, all the while inflation remained stubbornly low."

The problem is that there is not a comprehensive across the board capital gains or wealth tax. Asset bubbles would not blow up (also subject to bank leverage limitations) with a proper tax system. You get what you pay for.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.