Reserve Bank Governor Adrian Orr has announced that a Funding for Lending Programme (FLP) to give banks cheap lending based on the Official Cash Rate (currently 0.25%) will start next month.

The RBNZ estimates the likely size of the FLP could be about $28 billion based on take up.

In the RBNZ's latest Monetary Policy Review the OCR was again kept unchanged and so was the size of the Large Scale Asset Purchase (QE) programme - at $100 billion.

The RBNZ is still keeping its options open on the possibility of taking the OCR negative next year. However, the latest Monetary Policy Statement from the bank gave no update on the projected level of the OCR beyond March next year. The RBNZ has indicated it would keep the OCR at 0.25% at least till March.

The announcement on Wednesday gave few specific details on the detail of the FLP. The RBNZ said it would be implemented "in early December". Details of operations, including terms and conditions, would be made available "in coming weeks".

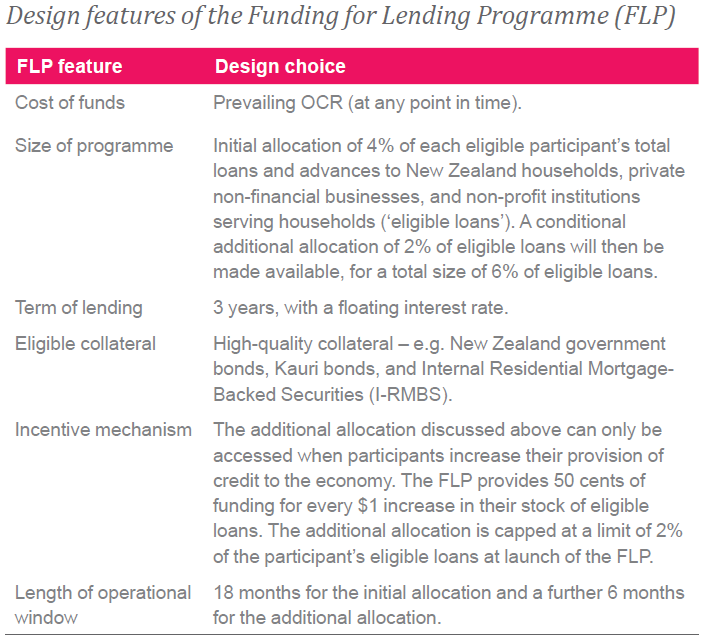

Kiwibank chief economist Jarrod Kerr explained the so-far available details of the scheme like this:

The initial funding allocation of 4% of total bank loans and advances, domestically, will be followed by an additional (and conditional) 2%, for a total available funding pool of 6% per bank. The funding will be available for 3 years on a floating rate (so to capture any cut into negative territory). The FLP will be effectively open for 24 months (18 months on the initial allocation plus 6 months for the additional 2% allocation).

Some economists had suggested it would be a good idea if the FLP was 'targeted' specifically for business lending. But there's no indication from what the RBNZ has said in its announcement that it will be targeted.

There's been concern that some of the money from the FLP would further fuel the hot housing market. The RBNZ separately on Wednesday announced plans to bring back limits on high loan to value ratio (LVR) lending.

The RBNZ said the "key success metric" of the FLP will be whether it results in declines in funding costs, and encourages recent declines in these costs to be passed through to lower household and business borrowing costs.

"We could see a scenario where FLP funds are only drawn down in small amounts, but its availability encourages a broad decline in interest rates. We would consider this scenario successful, even though actual use of the FLP would seem minimal."

ASB chief economist Nick Tuffley said the impending FLP "looks like it will be designed to be large, incentivise lending, and be free of restrictions such as sector-specific targets that might otherwise constrain its effectiveness".

"Those criteria should give it a good chance of being effective, though the devil will be in the final details.

"Given the recent resilience of the domestic economy, we assess that the FLP scheme will now prove to be enough future stimulus, and that the RBNZ will keep the OCR at 0.25%. Whether OCR cuts do indeed occur will depend on the effectiveness of the FLP scheme in driving down NZ interest rates and on whether the recovery is not derailed by events."

Westpac chief economist Dominick Stephens said it seemed that the decision to add additional monetary stimulus was a judgement call on the part of the Monetary Policy Committee.

"The RBNZ’s economic analysis, prepared by staff, clearly indicates that less monetary stimulus is needed relative to what the RBNZ thought in August. The RBNZ’s GDP forecast has been revised up substantially, it is now forecasting a peak unemployment rate of 6.4% (previously 8.1%), it is forecasting house price inflation of 9.6% this year (previously -7%)."

This table was provided by the RBNZ on the FLP:

This was the full statement from the Governor and the RBNZ's Monetary Policy Committee:

Tēnā koutou katoa, welcome all.

The Monetary Policy Committee agreed to provide additional monetary stimulus to the economy in order to meet its consumer price inflation and employment remit. The Committee agreed that the additional stimulus would be provided through a Funding for Lending Programme (FLP), commencing in December. The FLP will reduce banks’ funding costs and lower interest rates.

The Committee will also continue with the Large Scale Asset Purchase (LSAP) Programme up to $100 billion, and retain the Official Cash Rate (OCR) at 0.25 percent in accordance with the guidance issued on 16 March.

Progress has been made on the Bank’s operational ability to deploy an FLP and a negative OCR. The Committee agreed that these instruments can be mutually supportive in bolstering economic activity if necessary.

Economic activity since the August Monetary Policy Statement, both international and domestic, has proved more resilient than earlier assumed. In New Zealand this trend was evident across a range of indicators, including employment, household spending, GDP, and asset prices. These outcomes reflect the effectiveness of the health and economic policy responses to the initial shock.

However, the COVID-19 shock to the economy is very large and persistent, and inflation and employment will remain below the remit targets for a prolonged period. These outcomes are despite the current significant fiscal and monetary stimulus.

The outlook for global economic activity remains dependent on the containment of the virus. While recent news on vaccine developments is positive, there remains a long and uncertain lag before any widespread vaccine deployment may be achieved. Meanwhile international border restrictions will continue to curtail international trade and migration, with variable impacts across industries and regions. International prices for New Zealand’s exports have remained resilient, although export returns continue to be partly offset by the New Zealand dollar exchange rate.

Domestically, fiscal stimulus remains significant even with the Wage Subsidy scheme having now run its course. Government spending on business assistance and household income support continues, and government investment will rise.

However, we expect an ongoing increase in unemployment as the economy adjusts. Consumer price inflation is also projected to remain at the lower-end of the remit target range for a period, and inflation expectations remain subdued.

The Committee agreed that monetary policy will need to remain stimulatory for a long time to meet the consumer price inflation and employment remit, and that it must remain prepared to provide additional support if necessary.

Summary Record of Meeting

The Monetary Policy Committee discussed international economic and financial market developments. The Committee noted that following a severe contraction, economic activity has subsequently improved. However, these outcomes diverged across countries, depending largely on the degree of social restrictions imposed as a COVID-19 containment measure.

Members noted that economic activity had been surprisingly resilient in some economies, including China. They also noted that the impact on New Zealand of the global economic weakness had been more muted than expected, with commodity and asset prices remaining firm. However, members remained concerned about the downside risks from the persistent spread of the virus in Europe and the United States in particular, which would constrain demand for global exports.

Members discussed domestic economic developments since the August Statement. Overall, economic outcomes had been more resilient than earlier assumed. This trend was evident across a range of information, including the labour market, household spending, GDP, asset prices, and goods trade. These outcomes partly reflected the effectiveness of policy responses to the shock.

However, members noted that the severe economic effects of the pandemic were persisting and have significant implications for the Committee in meeting its remit. Both headline and underlying inflation were below 2 percent, inflation expectations were subdued, and employment was assessed to be below its maximum sustainable level.

The Committee discussed the implications of the pandemic and associated steps to contain it for the New Zealand economy. The implications of closed international borders meant service export industries, such as tourism, would operate well below capacity for a prolonged period. Meanwhile, economic activity in other sectors appeared resilient, with labour shortages re-emerging in some cases.

The Committee agreed that the assessed maximum sustainable level of employment may continue to be lower than otherwise while the economy adjusted to the virus shock. Some members noted that resources could take a considerable period to be redeployed, which could result in isolated cost pressures. Others emphasised that underutilised labour from some sectors would put downward pressure on wages and inflation.

Members agreed that there was substantial uncertainty around how the economy would adjust. The Committee agreed that it remained appropriate for fiscal policy to play the primary role in bolstering economic outcomes, given the nature of the economic shock, with monetary policy in an important support role.

Members discussed the outlook for inflation and employment. Staff presented a baseline scenario, conditioned on a number of assumptions, including that there were no further substantial community outbreaks of COVID-19 in New Zealand, and that the international border would be fully open by 2022.

In this scenario, the labour market was projected to weaken further in the near term. It was projected to recover over subsequent years, in particular after the border was assumed to be fully reopened. Inflation was projected to fluctuate around the bottom of the Committee’s 1 to 3 percent target range until late in the projection period.

Most Committee members agreed that risks to the baseline scenario were less skewed to the downside than they had appeared earlier in the year. Economic outcomes could be stronger than assumed if household or business spending accelerated, for instance due to an earlier partial border reopening, or a higher propensity to consume out of household wealth. The latter could be supported by higher housing and financial asset prices, or improving sentiment about the global health outlook and its management. Members agreed that recent news around vaccine development was promising, but that there were still challenges to overcome before widespread availability could be achieved.

Members agreed, however, that it was still the case that unpredictable events could push inflation and employment significantly lower than in the baseline scenario. They discussed events such as ongoing virus outbreaks, delays in borders reopening, and continued reluctance to invest by businesses due to general uncertainty.

The Committee discussed the effects of its recent monetary policy actions. Members noted that wholesale interest rates had eased following the August Statement. This reflected the expansion and front-loading of the Large Scale Asset Purchase (LSAP) programme, and expectations from market participants that the OCR could be reduced below zero next year. Bank term deposit rates had also fallen substantially in recent months. In particular, these falls had followed the Committee’s guidance to Bank staff issued in September to prepare a Funding for Lending Programme (FLP) to be ready to deploy before the end of the year.

However, members noted that bank lending rates were largely unchanged since August despite the reduction in funding costs. They discussed the importance of banks passing on funding cost reductions to their lending rates in order for monetary policy to transmit effectively. Members noted that the Reserve Bank had announced a further 12-month delay to the start date of increased capital requirements for banks following the capital review, to July 2022, which would assist them in maintaining lending growth.

The Committee agreed that a prolonged economic downturn would make it difficult to achieve its inflation and employment objectives. Some members noted that while the decline in inflation expectations this year was not surprising given the scale of the shock, it would be concerning if expectations fell further or remained low for a prolonged period. The Committee agreed that it was important to anchor inflation expectations around the mid-point of the target range over the medium term.

Members agreed that, under current circumstances, the appropriate stance to achieve its remit objectives would be to provide further monetary stimulus. They also agreed that providing sufficient monetary stimulus would also promote financial stability, through improved employment and household income prospects. The Committee agreed that, given the current inflation and employment conditions, and the ongoing significant uncertainty with regard to the outlook, there was less regret associated with the risk of temporarily overshooting their policy remit.

The Committee noted that other prudential policy settings could be adjusted to reduce risks to the financial system if required. Members noted that the Reserve Bank will consult on the possible reintroduction of limits on high loan-to-value ratio lending, in order to slow the build-up of riskier lending on bank balance sheets.

The Committee reaffirmed that an FLP, a lower or negative OCR, purchases of foreign assets, and interest rate swaps remain under consideration.

The Committee noted that staff were prepared to implement an FLP from early December. The FLP was expected to work primarily by lowering system-wide funding costs, benefiting all financial institutions, not just those that drew on FLP funds. Lower funding costs would enable financial institutions to lower borrowing costs for firms and households.

Members noted that the effectiveness of an FLP would depend on financial institutions passing on declines in their funding costs to borrowers, and agreed to monitor pass-through to lending rates closely. Members agreed with the staff assessment that an FLP would be an effective way to provide additional monetary stimulus, and that it was the best tool to deploy at this time given the Committee’s principles for alternative monetary policy instruments. They also noted that evaluations of similar programmes deployed overseas had shown that they were effective.

Members discussed the design of the FLP. They endorsed staff advice that the programme should be of sufficient size to allow financial institutions to reduce interest rates with confidence that a low cost, stable funding source was available.

Members noted that the FLP was likely to be drawn down gradually given banks’ current funding needs, and that the success of the programme would be measured by the fall in household and business borrowing rates, rather than the level of drawdown.

The Committee agreed that including an incentive to expand lending would help to ensure adequate supply of credit to support the economic recovery, but that targeting the incentives to specific sectors would reduce the programme’s effectiveness. The Committee noted that overseas initiatives to target sectors of the economy had been designed to overcome specific issues in those countries. The Committee agreed targeting credit to specific sectors was the role of the banking sector or government initiatives.

Members noted that the banking system is on track to be operationally ready for negative interest rates by year end. The Committee agreed that it was prepared to lower the OCR to provide additional stimulus if required.

The Committee noted staff advice that bond purchases under the LSAP programme had been effective at keeping yields low, and endorsed their recommendation to continue adjusting purchases as market conditions dictate. On Wednesday 11 November, the Committee reached a consensus to:

- hold the OCR at 0.25 percent, in accordance with the guidance issued on 16 March;

- maintain the existing LSAP programme of a maximum of $100b by June 2022; and

- direct the Bank to implement an FLP in early December 2020.

46 Comments

"Good afternoon class"

"Good afternoon Mr W."

'Please be seated and you'll find in front of you a release by The Committee of the Reserve Bank of New Zealand on its next set of stimulating initiatives.

Now. In 100 words or less, can you tell me what's going to happen.

Oh, and Alice. Please refrain from derogatory comments made out the Governor. You'll note I marked you down on last week's essay from an A+ to an A as a result.

Ok, class. Start now....."

No wonder came out earlier with views on LVR as knows that this action will add fuel to fire unless do targeted FLP but than whom will the bank lend as only business in NZ is Housing Business.

maybe i have missed it, but i don't see any interest rate mentioned, if it is at OCR 0.25% then that will not make a huge difference to anyone, the banks add on their standard 2% points, so the lending will be at 2.25%

You can already get mortgage money at 2.4% and some at under 2%

Edit: ok i see it is at prevailing OCR, so has some small potential to adjust down if RBNZ goes ZIRP

RCD: Bank margins are more in the 1% - 1.5% range. The bulk of their funds are from retail deposits (mum/dad/nana/pop) which cost them more than 0.25% (although watch this space). So RBNZ has been asking banks to lower mortgage rates but banks were replying that retail depositors won't accept much lower rates from here. Remember banks make money on the difference they pay depositors and charge borrowers. So what's the RBNZ's reply to banks saying that they can't lower deposit rates due to the risk it all flies out the door? FLP. RBNZ said "sweet well what if we just give you the money at OCR, that way you can lower your deposit rates (and therefore lending rates) without worry if the money leaves. RBNZ directly funding NZ mortgages since ages ago (Dec 2020).

"That's a very good start, Taimaiakka.

But it's always good to give an essay a title. Something bold and eye-catching to grab the readers attention.

What are you going to call it?

"When you're in a hole keep digging, Sir?."

Excellent. Carry on....

Another title..... don’t trip over the can....

What a joke.

Thats because the inmates/children are in charge

If Mr Orr is worried about housing ponzi and he still wants to bring more cheap or free money that will boost his favouraite passion - housing ponzi than why the delay of introducing LVR, as can reintoriduce at the same time unless FLP is to add wings to rising house market

Let's give everyone a million dollars. We'll all be millionaires and life will be good.

That is not the intention here. The great unwashed will not be given 'free money.' However, the intermediaries will be up for the million dollar-type bonuses depending on how much of the money they can shovel to the punters.

Lets give everyone with a million dollars an additional million dollars, then everyone will be even richer.

"the success of the programme would be measured by the fall in household and business borrowing rates"

Doesn't matter what the business borrowing rates are if the commercial banks are too yellow bellied to lend to any businesses. What a terrible time to not currently own a house.

Nail, head, Underhill. Policy effectiveness and outcomes science 101 does NOT rest with measuring the outputs of the policy intervention [whether borrowing rates decline or more borrowing ensues] but assesses the ultimate policy outcome [the economic effects and impact of the intervention].

This thinking is not just RB. Widespread in public sector. Serious outcomes science in Govt is rare/patchy (NZ was a world leader decades ago, with NZ officials amongst leading OECD initiatives), hollowed out by a generation raised on NPM targets (New Public Management). And post-NPM, many agencies (mis)label targets as 'outcomes' - and wonder why we keep falling on actual outcomes, in education, health, economy, etc

"Lower funding costs would enable financial institutions to lower borrowing costs for firms and households." RBNZ MPC statement.

So rather than targeting solely businesses, it seems that mortgages will also be included in the programme.

Downward pressure on mortgage rates, continually fueling of the housing market???? Surprising - there is need for LVRs to be implemented urgently.

… Orr just not implement the FLP ?

Every RBNZ output makes me more triggered.

That is the desired response.

OMG. Because more private debt is what the economy needs right now?!? How wrong-headed can you get!

See the Bloomberg.com article about the Japanification of NZ, with the RBNZ now owning 37% of treasuries. Gov. Orr does not seem to grasp the consequences for the economy and for the currency. NZ does not have a reserve currency. Once international investors realise what is going on with our Reserve Bank, the NZ dollar will drop like a stone.

Correct. Orr must be dismissed immediately, before he does more serious damage to the economy. I watched his press interview today, and I could not believe his eye-watering pigheadedness and his refusal to confront reality and the negative effects that the misguided RBNZ policies will have to the long term health of the NZ economy and financial system.

Perhaps that is the intention?

I guess the F in FLP really mens Free. The only investments in town are property and shares neither justify any stimulus. The FLP is targeted to reduce funding costs but this will not produce inflation neither will reducing interest rates when the funds go into property and the share market.

all he has to do is lift interest rates, they created this asset bubble by going on and on about going negative, now we have 1.1 million dollar houses in Waipukurau that someone bought for 340k 4 years ago. LMAO.

When humpty falls off the wall there is no putting him back together again that's all the central banks and all the Governments, couldn't put him together again.

And the pre-auction bid made by our son this morning after being spooked by the LVR announcement missed by... 12%.

Sold to an offshore buyer; sight unseen.

Well, done Adrian. Well done.

I tell my children never to forget, 'the bad news is good times never last forever, the good news is the bad times don't last forever either. Just remember they all end'.

The property bubble doesn't end. Not in this county.

I hear alot about offshore buyers - yet this government banned foreigners from purchasing residential properties, didn't they? Which means these offshore buyers are either NZ citizens or Australians, is that right?

Is it possible to transfer funds to kiwi residents to make a purchase and manage it? How about multiple purchases and put it under a company? Something's going on...

"Which means these offshore buyers are either NZ citizens or Australians, is that right?"

one million nz passport holders (kiwis) are offshore plus Australians plus Singaporeans. Recent study shows hundreds of thousands are planning to come back over the next few years and they will all need somewhere to live.

Why do this? No reason at all.

* won't stimulate anything.

* only intermediaries will benefit.

Better task is.

* stabilise house prices. The current outrageous situation is poisonous - mmm - to just about all New Zealanders.

'The Committee agreed that it remained appropriate for fiscal policy to play the primary role in bolstering economic outcomes, given the nature of the economic shock, with monetary policy in an important support role.'

What is the fiscal policy that is bolstering economic outcomes?

On the 1st November $NZ vs $US = .66

Today $NZ vs $US = .69

All I see is pressure from the govt to rein in monetary policy and cut off residential housing activity which is the only part of the economy with activity of note while the govt does absolutely nothing on the fiscal policy front.

Now the squeeze is coming onto exporters. Mr Kerr's article saying don't worry about the exporters they will have hedged already I thought was grasping at straws. Perhaps the importers have hedged their currency bets already as well?

Death to the economy by a thousand cuts. Death to the economy by waiting around to see what happens. Too slow, too lumbering, too much woolly thinking. It is starting to appear that the decisive Covid-19 govt action was a one off.

Assets will be repriced in US dollar terms as a result of increased United States Liquidity. You can either have higher $NZ dollar asset prices or a higher $NZ dollar. It looks like the govt is choosing a higher $NZ and the stagnation of the economy over rising asset prices.

Just so long as govt realizes that that is the choice they are making.

If the economy needs stimulus why not giving publicly funded zero interest loans to productive activity? Instead we delegate our responsibility into the banks which will lend according to their own interests making a profit out of it and put no restrictions to loans into speculative assets.

It is clear, they just want to further inflate the housing Ponzi. Orr is not even trying to hide it any more.

In the latest MPS the RBNZ says the declines in interest rates through 2020 "are likely to have contributed to recent increases in house prices, in part by making mortgages more affordable to service"

So the RBNZ implements a Funding for Lending Programme with the explicit purpose of lowering retail interest rates even more.

Let me consider my words carefully… IT IS STUPID !!!

Has Orr completely lost his mind?

Is this even needed anymore? Things didn't pan out how they thought they would - property rising yet again rather than falling as predicted. Yet they want to throw more petrol at it. M-Orr-ons.

Orr - 'Don't hate the player, hate the game'

cocaine junkies reformed to property junkies

Q. Why did the Reserve Bank Governor cross the road?

A. He's lost his copy of the RBNZ mandate, and increasingly found himself taking actions that might destabilise the NZ Banking system, so he went looking to find it.

If only these clowns remembered they also have a mandate to be human f**king beings.

I always thought Banking was about being "Honest".... someone you could trust.....?

Now it is ORR...not.

Muppets!

You mean to say we're not borrowing enough already?

20 years of "stimulus" and this is as far as we've gotten?

Unfortunately the biggest muppets are we, the people, buying into this bullshit.

The only mandate the RBNZ should have is the regulation of "money" supply and financial stability. If the banks and the property "market" are too big to fail, the RBNZ has already failed.

That's what I stated long time ago. People in this country are lacking simple dignity . If noone buys at stupid prices , no bubbles

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.