By Stephen Toplis*

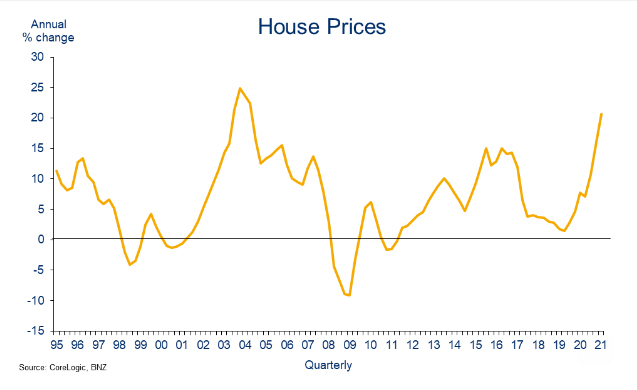

The RBNZ has every right to be worried about the potential for a house price correction. It is a moot point whether house prices, per se, can be sustained at current levels. But while levels might be maintainable, we are convinced that current house price inflation is not. Indeed, the longer inflation remains at current elevated levels the greater the chance that the housing market will be forced into a major correction.

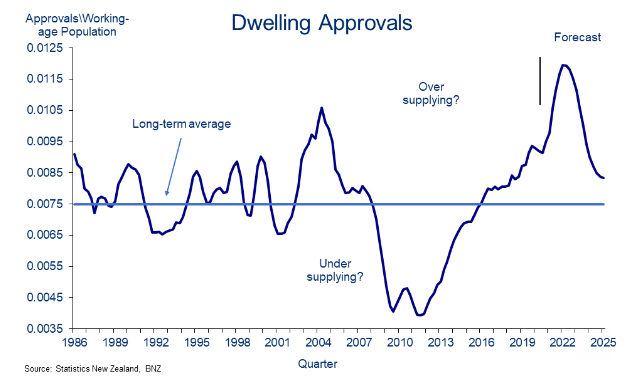

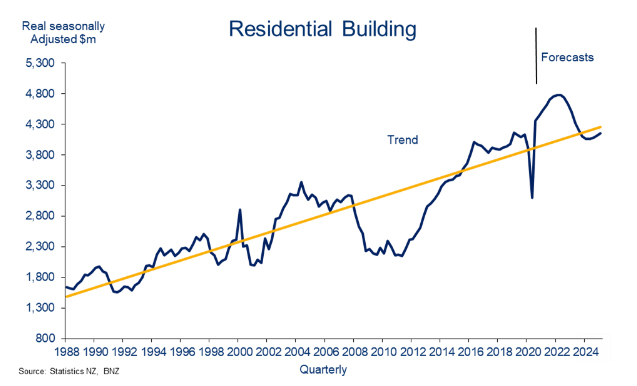

At the same time, we are increasingly concerned that the pace of house construction cannot be supported either. While we think there is further room for expansion in the residential building sector in the near term, we are very aware that an oversupply could start developing in some areas in the not too distant future.

The common themes for both house prices and construction are:

- Population growth has weakened considerably

- House prices are simply becoming beyond reach

- Both the Reserve Bank and Government are on a mission to remove overheating in the sector

- Interest rates are likely to start drifting higher.

Moreover, it is very hard to justify current housing valuations on the basis of current prospective rental returns.

There are multiple ways of analysing whether or not house prices are justifiable. Some much more complex than others. But before doing the analysis you have to ask does what has happened in the housing market really pass the sniff test?

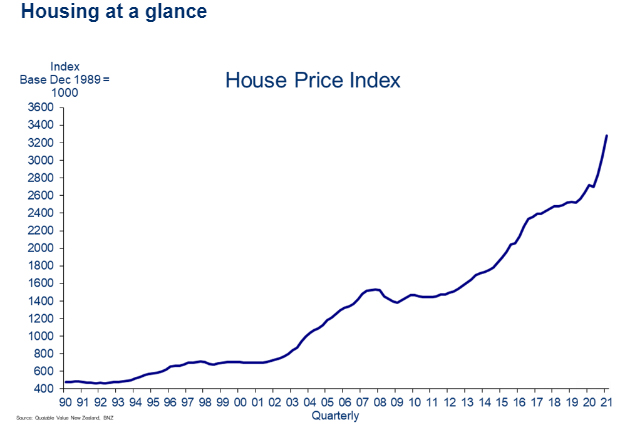

- Does it really make sense that the value of the housing stock has risen six fold since the beginning of 1990?

- That prices have doubled in the last eight years?

- And are up a third since the outbreak of COVID, especially when pre-COVID the view was that the combination of moderating immigration and rising supply would soften the housing market.

We are very sceptical that the price movement does pass the sniff test and we certainly do not believe the current momentum in house prices can be justified in any way, shape or form. And if the starting point is not exaggerated enough, we are now looking at growth in demand for housing fading at the same time that new supply is exploding.

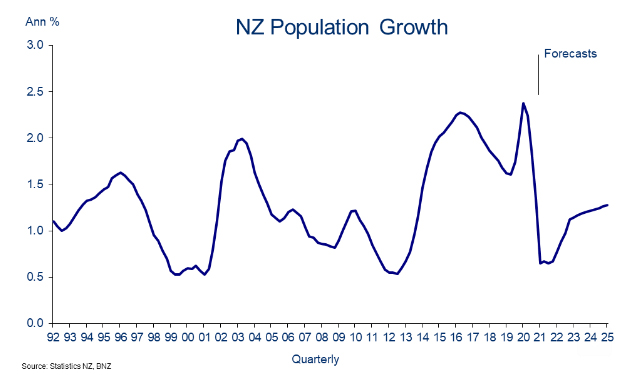

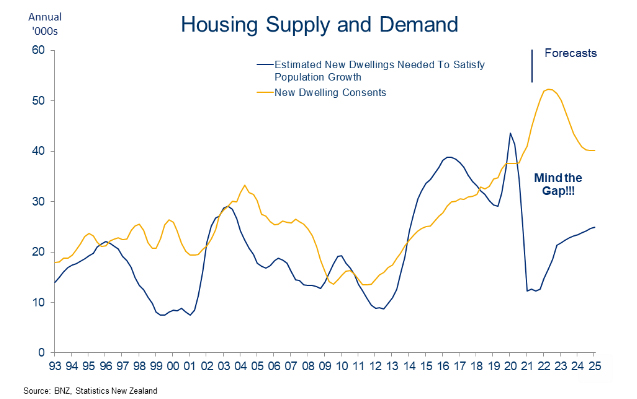

On the demand front, the migration-driven slump in population growth is a key factor. With annual net migration inflows falling to around 7,000, from a peak over 90,000, New Zealand’s annual population growth has fallen from 2.4% to just 0.7%. Roughly speaking, this means we only need to build around 12,000 houses a year to house our “new people” whereas the requirement was more like 44,000 houses a year as recently as 12 months ago.

We are projecting that net migration should start to pick up slowly next year. However, we caution that there is a very real risk net migration turns negative. Was this to be the case then demand would be even weaker than we are currently projecting.

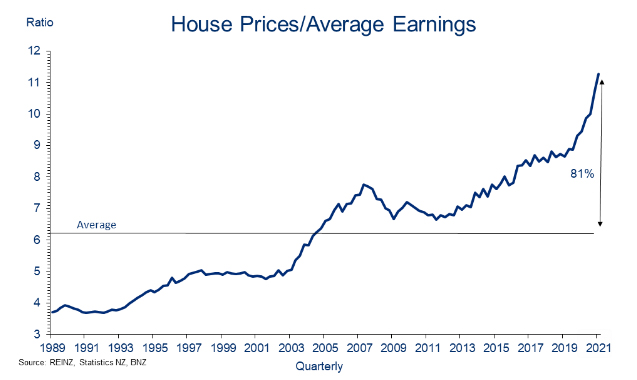

At the same time as physical demand growth is moderating, the possibility of purchasing a house has become an impossible dream for some. Sure, low interest rates have eased the repayment burden but the level of debt and deposit required is simply prohibitive for an increasing number of people. The price of an average house is over 11 times an individual’s average earnings. The average for this relationship is 6.2 times. Put another way, it now takes two people on the average income to afford the same house as one person could purchase back in 2003!

Investor demand must also be seriously adversely impacted by reduced returns on investment as landlords’ costs rise, tax deductions fall, compliance requirements increase, effective P/E ratios rise and now capital gains diminish as a result of lower likely house price gains and the imposition of a high capital gains tax on short-held property.

To cap things off, both owner occupiers and investors have been benefitting from a trend decline in interest rates. It is highly unlikely mortgage interest rates will fall much this year and there is now a very real chance rates start to rise within twelve months.

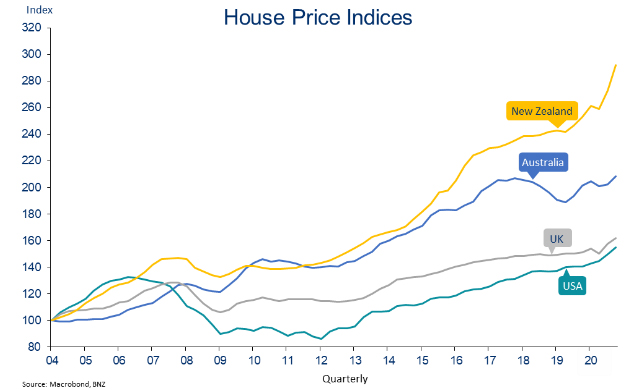

It is, nonetheless, true that the fall in interest rates does justify higher asset prices of all types, but we are wary that New Zealand house price levels have pushed much higher than our counterparts offshore.

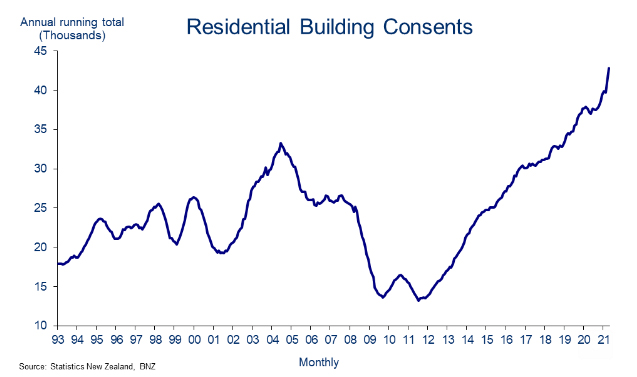

But, while demand comes under pressure, supply is going bonkers. In the year ended April 42,848 consents were issued for new dwelling units. On a per capita basis this is now surpassing the 2004 building boom. And, yet, there is no sign of this coming to an end anytime soon. Accordingly, we think we are entering a multi-year period when the marginal supply exceeds the marginal demand which, in turn, should put downward pressure on house prices. We reach the same conclusion whether we compare actual supply with the increase in population or just by looking at new dwelling approvals per head of working age population compared to average.

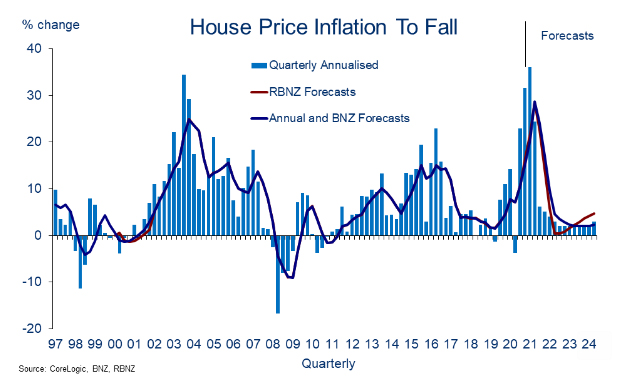

At this stage we are not forecasting a price correction, as such. As it turns out, the RBNZ’s latest house price forecasts are very similar to our own. Our view is a tad more inflationary but only at the margin. We are forecasting a 17.0% increase in house prices in the year ended December 2021 but the vast majority of this has already happened. Only modest growth is expected from here on in with annual inflation dropping to about 2.0% per annum over 2022 and 2023.

While we are not predicting a price slump, we certainly are not ruling one out. But let’s put this in perspective. Even if prices fell 20% it would only take them back to where they were a year ago. For new buyers this would be problematic but for prospective new entrants a boon. For the majority (everyone else) it shouldn’t really matter.

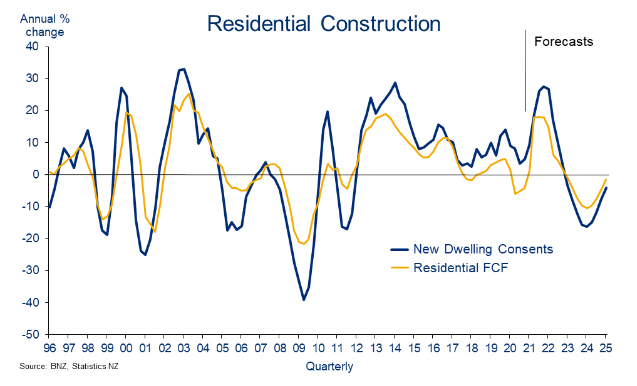

Eventually, the combination of weaker price growth, weaker demand growth and the current supply response is likely to result in a softening in residential construction too. We are forecasting a 17.8% increase in residential fixed capital formation across calendar 2021. This is the strongest pace of growth since 2003. Further modest expansion is expected across 2022 but we then expect a reasonable contraction in activity over the following two years.

While the expected decline might look dramatic, the level of activity we are forecasting after such a correction will still be in line with 2019, which was considered to be a strong year, and it simply takes the path of activity back to trend.

All the above might sound a bit dramatic to some but it really isn’t provided the rest of the economy hangs together over the period. And we think it is likely to, as strengthening global growth, massive infrastructure needs, post-COVID euphoria, improving tourism flows, ongoing fiscal stimulus and continued monetary policy support all underwrite the economy. Be that as it may, the likely course of the housing market over the next few years will be a harsh reminder to some that economic and financial cycles are not a one way bet.

Stephen Toplis is the Head of Research in the Institutional Banking division at BNZ. He is based in Wellington.

105 Comments

Yes it seems crazy that house prices keep rising but they do. At some point however, you just have to admit your predictions and all your basis for falls are just wrong and move on like I did. You can throw house price falls out the window when the materials to build them are going through the roof. Fact is prices are set in concrete to keep rising for at least the next 12 months. Its going to take something on a global scale thats even bigger than a Pandemic to kill the market. Houses in NZ may be rot boxes but the driveway is paved in Gold.

I agree that many of us have felt a correction was on the cards for the past 5 years and we have been wrong....so far. There is a good description of the Irish property market bubble on Wikipedia. Warning were made for around 7 years before the market crashed between 35 and 50%. What goes up must come down in the end. The only thing that could keep demand rising would be increased immigration but this looks to be off the cards for a while.

We got through COVID with only a small rise in unemployment, which I think is nearly reversed now (going by the stats, anyway)? Unemployment is what really sets off a recession and prolongs it.

If you consider that a lot of low-productivity tourism jobs are gone, with those people going often into training for trades or construction, then the labour market over the next 18-24 months is probably going to help underpin growth.

Pretty sure unemployment is a lagging rather than leading indicator

Never said it was leading, just that it is correlated with worse recessions.

Definitely what's held up with skyhooks must come down

Waikatohome: you can't compare apples with oranges; Ireland has always been a land of emigration, while NZ is and always has been a land of immigration. Immigration means more demand for housing and the recent tsunami of immigration ( largely encouraged by National) has meant the sudden arrivals couldn't be accommodated by existing house numbers. The supply of new housing was always going to play catchup. While there's a housing undersupply prices were always going to increase. While every man and his dog are predicting reduced immigration from now on, they are still predicting some thousands of immigrants, and this doesn't allow for the numerous immigration scams which will surely resume unabated once the borders are reopened.

Yes, immigration has played a part, but in jurisdictions where immigration has been consistent as high as NZ over time, the price did not go up because supply was allowed to keep up with demand. Plus over the course of NZ immigration, when immigration has been as relatively high, prices remained affordable.

NZ has artificial restrictions to supply, namely our land-use policies.

Street wise: NZ population fell in 1999 and 2000. I take your point that the countries are not directly comparable but we can still learn lessons from other countries mistakes. I visited Ireland just as the market was turning and no one believed that prices could fall. They thought they had seen the end of boom and bust.

The Irish market failure was built on absurdities, it was 20% of employment, twice as bad as NZ, it was an absolutely staggering 25% of GDP, 4x worse than NZ. All of that normalising caused unemployment to hit an eye watering 14%. Because of these extreme differences Ireland cant be used as a template for NZ other than to say the direction we are heading in cant persist indefinitely.

Just fools and those with vested interest blinding their objectivity cannot see this coming. Ireland was just one example and those of us that have gone through a housing crash can see how evident all signs are, no matter how much politicians and central banks try, once the people starts to believe prices must fall (which is happening just now) the only way is down.

The price of new houses may keep increasing, due to material costs. But new houses make up only a tiny part of the total market.

Not correct, the price of new houses affects the whole market. There is no such thing as a "second hand house" if new builds rise in value so does the whole market.

Not the only possible outcome.

Anther outcome is that house prices slump, the cost of new builds remains elevated due to input costs and so new builds decline, until such time as reduced demand results in reduced input costs for materials and labour.

Lanthanide: Assuming there is a house price slump next month, and accepting that our existing domestic economy is now largely based on the residential construction/realestate industry, what will happen to all those thousands of tradie apprentices that have been encouraged by the Government and all to sign up over the past few years? The boss will say "sorry son but there's no more work in the pipeline. I'm going to have to let you go", and the tradie apprentice replies "what will I do? My girlfriend and me, we were planning to get married later this year and now we will both be unemployed because she has also just been laid off....she was a customer service person in a timber supplier. This is crushing".

Lanthanide, give us a considered answer to this scenario.

Lanthanide: Assuming there is a house price slump next month, and accepting that our existing domestic economy is now largely based on the residential construction/realestate industry, what will happen to all those thousands of tradie apprentices that have been encouraged by the Government and all to sign up over the past few years? The boss will say "sorry son but there's no more work in the pipeline. I'm going to have to let you go", and the tradie apprentice replies "what will I do? My girlfriend and me, we were planning to get married later this year and now we will both be unemployed because she has also just been laid off....she was a customer service person in a timber supplier. This is crushing".

Lanthanide, give us a considered answer to this scenario.

Lanthanide: Assuming there is a house price slump next month, and accepting that our existing domestic economy is now largely based on the residential construction/realestate industry, what will happen to all those thousands of tradie apprentices that have been encouraged by the Government and all to sign up over the past few years? The boss will say "sorry son but there's no more work in the pipeline. I'm going to have to let you go", and the tradie apprentice replies "what will I do? My girlfriend and me, we were planning to get married later this year and now we will both be unemployed because she has also just been laid off....she was a customer service person in a timber supplier. This is crushing".

Lanthanide, give us a considered answer to this scenario.

Lanthanide: Assuming there is a house price slump next month, and accepting that our existing domestic economy is now largely based on the residential construction/realestate industry, what will happen to all those thousands of tradie apprentices that have been encouraged by the Government and all to sign up over the past few years? The boss will say "sorry son but there's no more work in the pipeline. I'm going to have to let you go", and the tradie apprentice replies "what will I do? My girlfriend and me, we were planning to get married later this year and now we will both be unemployed because she has also just been laid off....she was a customer service person in a timber supplier. This is crushing".

Lanthanide, give us a considered answer to this scenario.

Lanthanide: Assuming there is a house price slump next month, and accepting that our existing domestic economy is now largely based on the residential construction/realestate industry, what will happen to all those thousands of tradie apprentices that have been encouraged by the Government and all to sign up over the past few years? The boss will say "sorry son but there's no more work in the pipeline. I'm going to have to let you go", and the tradie apprentice replies "what will I do? My girlfriend and me, we were planning to get married later this year and now we will both be unemployed because she has also just been laid off....she was a customer service person in a timber supplier. This is crushing".

Lanthanide, give us a considered answer to this scenario.

Lanthanide: Assuming there is a house price slump next month, and accepting that our existing domestic economy is now largely based on the residential construction/realestate industry, what will happen to all those thousands of tradie apprentices that have been encouraged by the Government and all to sign up over the past few years? The boss will say "sorry son but there's no more work in the pipeline. I'm going to have to let you go", and the tradie apprentice replies "what will I do? My girlfriend and me, we were planning to get married later this year and now we will both be unemployed because she has also just been laid off....she was a customer service person in a timber supplier. This is crushing".

Lanthanide, give us a considered answer to this scenario.

Lanthanide: Assuming there is a house price slump next month, and accepting that our existing domestic economy is now largely based on the residential construction/realestate industry, what will happen to all those thousands of tradie apprentices that have been encouraged by the Government and all to sign up over the past few years? The boss will say "sorry son but there's no more work in the pipeline. I'm going to have to let you go", and the tradie apprentice replies "what will I do? My girlfriend and me, we were planning to get married later this year and now we will both be unemployed because she has also just been laid off....she was a customer service person in a timber supplier. This is crushing".

Lanthanide, give us a considered answer to this scenario.

Lanthanide: Assuming there is a house price slump next month, and accepting that our existing domestic economy is now largely based on the residential construction/realestate industry, what will happen to all those thousands of tradie apprentices that have been encouraged by the Government and all to sign up over the past few years? The boss will say "sorry son but there's no more work in the pipeline. I'm going to have to let you go", and the tradie apprentice replies "what will I do? My girlfriend and me, we were planning to get married later this year and now we will both be unemployed because she has also just been laid off....she was a customer service person in a timber supplier. This is crushing".

Lanthanide, give us a considered answer to this scenario.

Apology, I didn't intend seven copies of my post. Don't know what happened here. I think there was no immediate response when I pressed the 'save' button so I pressed it a few more times not realizing that it was in fact working and there was just an uncustomary delay.

"Its going to take something on a global scale thats even bigger than a Pandemic to kill the market."

That would be the inevitable GFC style crisis that comes when all the bad credit issued in recent years comes calling at the same time rates start their rise again. The solution around the world has been "print money, make more debt, keep the party going." Like giving a credit card to an over eager teenager, this isn't going to end well.

Totally agree dla06c but the really big question is when ? Yes another GFC is inevitable but how long can you afford to wait for it ? Even then when prices do finally crash you find that your job has also gone so your even worse off than before the GFC. 5 years ? 10 years ? to long to wait I'm afraid, house prices could have doubled again before it happens and you would be back to where you are right now with even a huge 50% crash.

Sounds like FHBs are better off by leaving the country Carlos and buying somewhere else that hasn’t lost the plot as much as NZ has...

As much as NZ. That’s a very important distinction IO. The entire world is struggling, but NZ particularly so in terms of living costs and wages.

Is this Jacinda defination of prosperity - problem is that she has to witness first hand to believe like she saw that open home near her house to realize the seriousness of the situation :

https://i.stuff.co.nz/life-style/homed/real-estate/125303303/lack-of-ac…

What "bad credit issued in recent years" are you referring to? (to clarify:I mean in the NZ markets)

Your model might not be the same as others'. The recent house price increases make sense directionally in terms of what's happened to migration (strong early/pre Covid), and interest rates (continual declines and now extra low). No need to throw the models out, they are doing alright.

HP forecasts for COVID were wrong because the underlying forecasts for employment and migration were wrong.

Yes the construction cost will keep rising, but that doesn't mean house price wont come down. Housing in New Zealand is not considered as consumption goods but as investments and assets. It's not wise to use cost and price theory to apply to this situation. The housing price going up or going down depends on the market and affordability. Supply and demand determines the market, interest rate determines the affordability. That's why through covid last year, the price went up 20% because of 75 basepoints slashed and removed LVR. As interest rates going up and demands coming down, housing price will be stabilized and eventually come down. That's what economists are talking about.

"Its going to take something on a global scale that's even bigger than a Pandemic to kill the market".

Nope, all it takes is just a rise in interest rates, that's it. If interest rates rise significantly for whatever reason, the whole NZ housing Ponzi will collapse under its own weight like a house of cards.

Well I guess it's just as simple as keeping interest rates low forever then.

My issue with a forecast of "oversupply" is that we don't know what levels of pent-up demand exist from years of undersupply. Regression to trend on pricing might take years of relentless supply bias now and deleveraging is never easy.

The forecast doesn't hinge on oversupply. The market is in equilibrium (i.e. prices have already adjusted with the current 'undersupply'), just people are living more crowded (moving on from flatting or living with parents later). With prices having adjusted already, even by meeting some pent-up demand, there should still be a moderation in prices.

That’s precisely what Squishy is saying... the demand will remain strong as people are already in crowded living arrangements... key is at what price point will this ‘equilibrium’ move to allow younger generation to move into their own home.

Wow, the low rate of construction during the last National government, at the same time immigration went nuts and they sold off state houses, is really really stark.

A lot of stuff changes quickly during policy slowly worked out much earlier. The immigration that shaped these decisions was likely mid brain drain.

GFC? Not something you noticed?

Sure did notice in 2012-2013 lots of media stories about builders moving to Australia because there was no work here.

Pity we didn't have a government in power who could do anything to jolt the construction industry into life, like a kiwibuild policy to keep the industry busy for the huge immigration surge the government was also presiding over.

National weren't dealt a great hand, but they played what they had poorly. They had the latitude to say they were investing in assets for the future, but instead they chose tax cuts and neo-austerity, so they could trumpet returning to surplus as if it was an amazing and worthwhile achievement in its own right, ignoring that the purpose of an economy is to allow people to live good lives. They knew that Labour could only promise to spend more money than them, and so did everything in their power to make spending money an electoral bogeyman so they could retain power, regardless of the long term costs and damage they did to the lives of a large segment of the population in this country.

Remember this was the same party that actively supported hysteria around P contamination of housing because it let them kick people out of state houses and reinforce their perception of being "tough on crime". They weren't interested in seeing all NZers get ahead, despite what their election slogans said.

Good comment

"Both the Reserve Bank and Government are on a mission to remove overheating in the sector"

Agree with the article but to say that RBNZ is on a mission is over statement. Can say that it was on a mission to support ponzi but to control ....smoke created by Mr Orr.......

When on mission adopted LEAST REGRET policy and when no intent WAIT AND WATCH policy.

So are they on a mission now to control or were they on a mission earlier to promote housing ponzi ????

Sustainable or not but for now the party is in full swing and Mr Orr is definitely on a Mission but that mission is to finish FHB by his inaction.

https://thespinoff.co.nz/business/05-06-2021/a-bizarre-afternoon-at-a-c…

The only mission the Reserve Bank is on, is one to force indigenous culture down our throats. To quote the RBNZ, sorry Te Putea Matua, "The future is Maori"

Just how are any of us, Maori included, supposed to be able to afford a house Mr Orr?

I think anyone predicting anything spectacular from here for the next 2 - 3 years will be disappointed. Prices will hold mostly flat, before slowly starting to rise again. But at a slower pace than previous previous cycles.

Larger interest rate movements in either direction could be what upsets this prediction though.

With regards to immigration, when tourism returns the government will start letting in more people again. With our unemployment so low they will have no choice , but again the settings will be at a lower pace than in the past.

A housing over supply like in Ireland is very unlikely in nz. Would possibly only happen if there was a lot of construction compacity combined with another large price boom.

Characteristic of any ponzi is such, that it has to keep moving up, Up, UP...and the moment it loses it's momentum, it falls.

Their is no place for price to stabilize in ponzi. It is either up or down - no flattening.

Also is true that RBNZ and government has no choice now but to allow the ponzi to grow as otherwise will lead to disaster. So chill come what may as promised by Jacinda Government and supported by Mr Orr, personally will keep the fire alive as long as they are in power unless economy fundamentals takes over and economy is not just supply as many try to hide behind to justify inaction on housing ponzi.

Hmm, I think the word ponzi could have been used at least 3 more times. Maybe in a follow up comment???

Need to correct you here on your use of the word Ponzi. A Ponzi scheme is an investment fraud that pays existing investors with funds collected from new investors without there ever being an underlying asset. A housing market can never be a Ponzi as it matches buyers and sellers with assets that actually exist. An overly inflated residential property market is an "investment bubble" not a Ponzi. I used the word Ponzi four times...whoops now five.

You don't need housing oversupply for a correction to happen. You just need inflated prices and some sort of trigger. There was no oversupply in the US but after the GFC prices fell up to 50%. We have one of the most expensive housing markets in the world now, relative to incomes, so basically we're sitting on a bubble waiting for a trigger to pop it. It will come out of the blow, they always do.

I invest in property and I hope it cools down. The fewer people competing with me for run down blocks of units to renovate the better and the government can go focus it's attention and blame elsewhere.

a

Good writeup. But any prediction is untrustworthy including your own.

I advocate a population policy to keep NZ sustainable. And rich.

Two very wise sentences.

100%. We need to have a carrying capacity established but we also need to retain skilled NZers by ensuring NZ is a desirable place to work and live.

What will a population policy require.... that’s right, a prediction

"We are forecasting a 17.0% increase in house prices in the year ended December 2021 but the vast majority of this has already happened. Only modest growth is expected from here on in with annual inflation dropping to about 2.0% per annum over 2022 and 2023." BNZ 's forecasts would have the Corelogic HPI at 3588 end 2021 , and 3602 end 2023, alternatively the REINZ median house price at $871000 end 2021 and $906000 end 2023. All the other stuff is plainly fluff.

Saw a tweet by Bernard Hickey, that sums up the shit hole that government and RBNZ are in, created by them and now are really screwed. They can hide behind lies and manipulated data thereby digging themselves deeper in the shit hole and we as a nation will have to bear the shithole and the people created will fly off .....after making heaps.

https://mobile.twitter.com/bernardchickey/status/1400590992357560324

Housing ponzi is like a black hole that sucks everything in and destroys anything that comes near to it - people’s values, infrastructure projects, new business ventures, hope of prosperity for anyone under 30...

True but unfortunately politicians and Orr do not see long term and they are happy as long ponzi continues during their term.

Need a leader with vision.

It's not the RBNZ mandate to ensure the ethical glue that keeps society cohesive remains intact.

No one is going to vote for a party that promises a recession, and no party promising house prices will go down will get enough votes to have a meaningful say in government. At least not with our current voting demographics.

Maybe not vote for but they may vote for one promising to get out of a depression

It's all very sad and clearly the government has shifted from wanting to do something meaningful when it was first elected 4 years ago to now simply limiting further damage.

Their house building achievements are mediocre at best- what happened to the major Unitec project they announced with much fanfare 4 years ago?

I drove through Glen Innes the other day and there's a fair bit of nice new housing up towards Glendowie, but this is the product of a programme that has been going for 10 years not 3. In that respect, the delivery is poor.

They won't engage in ideas such as a major leasehold or shared equity housing programme - the only thing that would provide meaningful opportunity for home ownership for low to middle income earners. I know several people or organizations who have been lobbying for this, all they get is arrogant and poorly substantiated dismissal from the office of Megan Woods.

So as far as I can see we are screwed.

A correction will come one day but as Topliss says it won't pull prices back far enough to make a meaningful difference.

An expectation that your property will increase every year in value seems ingrained now in the minds of home owners. How long can it keep going for? Rents and wages are not keeping up with the house price growth and how can this continue? Certainly the decrease in interest rates helped to reduce loan payments meaning higher prices were possible for buyers. Net migration is down, a discontinuation of interest deductibility will certainly have an impact. I can't see how the price increases can continue steadily for the next 3 years even.

Given the housing shambles, I expect more and more young people on middle incomes will migrate to Australia.

Good for them, I say.

The only problem with that is we will develop a crisis in education and healthcare staffing. But that is not their fault or problem.

But shops selling brown slacks will be rushed off their feet.

I agree. Moving to Australia is the best solution for a lot of people. It's much easier to save there than it is here.

Young people shouldn't have any loyalty to NZ because NZ doesn't care about them.

That house price index is damn near vertical now....whats next?

If that chart doesn't give people concern, then nothing ever will.

In its own right, 2008 was a peak that could have been a bubble that need deflating, yet we've tripled down on that now! i.e. a second peak in 2017-2019 that was going to deflate until emergency intervention by the RBNZ, and now we've got what looks like a third bubble built on top of that now....its absolutely crazy.

For better for worse, "justified" or not, the market is always right. Wishful thinking is not. And there is an abundance of wishful thinking in this column.

Wishful in which direction?

Take your pick.

So every market where the bubble has burst (any there are many examples!), was the market pricing right before the crash, or right after the crash - often when values are half of what they were previously? In other words, the market pricing was 50% wrong...so are you sure it is always 'right' because a 50% margin is a pretty loose concept of the market being right!

Or can we agree that at times, participants in markets become irrational (and act with animal spirits).

Then what is worse, acting irrationally in the market, or posting wishful comments?

Why is there no mention of the estimated 40,000 empty houses in Auckland? Of course, there can be perfectly good reasons for any particular house not being occupied; it could be a holiday home or waiting to be demolished, but there can be little doubt that a substantial number permanently empty.

In some countries there is a name for this phenomenon-in the UK it's buy-to-leave,in the US, warehousing. Vancouver has imposed a tax on these properties for some years and Toronto is i believe, doing something similar. Why can't we do it? Let's say that 10,000 of these could be identified as permanently empty, so an annual levy of $10,000 would raise $100m with all of that,less collection costs, going to build more houses. Is there a flaw in that and if so, what?

The flaw is that councils now see empty houses as a source of revenue, so never want to bring in penalties high enough to stop it, but find that balance where they can charge the maximum without causing too many people to sell to avoid it. And after collection costs, there is not much money left to build houses with. Also, it still allows those rich enough to escape having to sell at all. ie avoid the 'crime' of having an empty house, so is morally unjust.

Especially since the right law to prevent this type of speculation would allow 1,000's more affordable housing to be built without any council interference.

Waste of time trying to tax an empty house, anyone with half a brain would "rent it out" to a relative for $10 a week.

If empty houses are caught by monitoring water and electricity use and whether there's an internet connection present, then you'll need to do more than sign a rental agreement.

"However, we caution that there is a very real risk net migration turns negative." this is the comment that stood out for me..if you were under 35 and with a decent skill/education behind you and wanted to start a family - go to Australia, forget NZ -- Boomers have and continue to spend your current

income - future income/savings, and have no qualms or any intention to slow down doing it.

Yep. Trans Tasman migration is normally negative (we usually to migrate to Aussie on net). Surely the latest housing debacle (which is worse here than aus) will see more people go there. Trans tasman migration played a role in the post 1974 housing market moderation (when real house prices fell 30-40%)

Except it’s the opposite. It’s money from Aussie, HK and London returning Kiwis in their 30s with young kids who are buying up many properties.

"Ponzi" is spelled with a capital 'P' as it's a proper noun - thank you.

Strong Towns - Shopping Malls are killing the cities - The Shopping Malls are dying

A counterpoint to Alison Brook

The water infrastructure bill indicates we are repeating all the same mistakes American cities make as highlighted by the Conservative "Strong Towns" movement.

Watch a couple of theses short videos and then go back and read Alison Brook's article and what she says about planning

https://www.youtube.com/watch?v=y_SXXTBypIg

And a crack at Christchurch

How Christchurch, New Zealand became a lesson in how NOT to rebuild after a disaster

https://www.strongtowns.org/journal/2021/3/2/christchurch-rebuild

Repeat from November 2020

This is out of control, Robertson and Treasury and RBNZ have got themselves into a tangled mess that is beyond their control. Nothing they can do about it. Anything they do from here on in will make matters worse

https://twitter.com/two_otherguys/status/1326279643670851585

This is great piece by Andrea Vance, exposing yet more double standards of a government making a name for itself in double standards. Trying to get through to Ministers is a nightmare, and when you get info so much of it is redacted that it's hardly worth the while.

https://i.stuff.co.nz/national/politics/opinion/125352433/this-governme…

Our "caring and kind" Jacinda has said that they will never allow house prices to fall so there we have it. No matter how crazy the situation may seem it will never be allowed to correct itself. I cant see the openly property rental sympathetic National party being any better. Even if prices increase no further, a large proportion of young aspiring first home buyers will never be able to save enough for their own home with stupidly high rental cost and the low wage low productivity economy. There are a lot of older people in that boat to and an increasing number of middle aged people headed that way also. Their only hope is to get out of NZ and the sooner the better.

Chris, anyone who thinks Labour are fundamentally different from National on housing and many other things need to rethink. The differences where they exist are subtle and usually quite immaterial.

I will never, ever vote for either of them again.

It's quite liberating coming to that position.

I agree. Makes you wonder whether either of them really ever run the country and other forces are making all the decisions. Just puppets in in the big public charade called democracy.

Actually prices are high but affordability is the best it’s been for a long time.

If you buy the house you’re renting you’ll pay less than your rent. It’s the deposit that’s the hurdle.

So its not really affordable then...?

Guys it is not going to fall because Govt. backed it.

The life of many will be full of misery in NZ it would be good if you are FHB or renter move to Aus.

Guys it is not going to fall because Govt. backed it.

I see. You think Jacinda Ardern and her generals can control asset markets. While I agree that there are some things they can control to support house prices, I do not believe they are as powerful as you believe. History shows that other more illustrious leaders have not prevented bubbles from falling. Why do you think Ardern's fairy dust is more potent? People should not believe this kind of nonsense.

Exactly, she is just simply saying what she believes is politically popular in the short term (and to keep RBNZ puppets happy)....despite the fact that a poll indicated that 3/4's of NZ'er actually want house prices to fall...

So go figure...

Let the price fall by 10% to 15%, all the current restrictions will be out of window in no time.

no LVR, negative interest, interests tax on rental revenue, foreign investment, bright line, permanent IO loan & flood open immigration gates.

There is 35% increase in last one year what substantial action is taken by now? Nada..

And you are saying govt action is not controlling asset market I know people waiting before Covid for price fall & now they are praying to go back to pre covid price..

Guys it is not going to fall because Govt. backed it.

I see. You think Jacinda Ardern and her generals can control asset markets. While I agree that there are some things they can control to support house prices, I do not believe they are as powerful as you believe. History shows that other more illustrious leaders have not prevented bubbles from falling. Why do you think Ardern's fairy dust is more potent? People should not believe this kind of nonsense.

If houses flatline for the next 3 years, they are essentially dropping in price when you factor in inflation.The government seem to want them to flatline, so not to rise as much.

No CGT, no change in land planning, no change in OCR, no window guidance on credit issuance, but house prices must correct. Lol ok.

All of those things are changing though...?

The current house prices is the market's vote on the best investment class in the country- textbook economics seldom reflect reality and economists are seldom the richest folks in the investing world.

If you were to follow Stephen's opinion in 2014 and stayed out of the equity markets, you would had been relatively much poorer.

https://www.interest.co.nz/opinion/71368/next-few-years-may-well-test-p…

Never the less, we need DGM economists to give some hope to their DGM followers.

That said, the market is betting he's wrong again on his current housing opinion.

Be quick, there's still room for property up-valuation.

I'm confused, are the DGMs the people who want to destroy the country via unsustainable gains in house prices, risking the financial stability of the country and the moral fabric of an equitable/prosperous/cooperative society, or is it the people who want prices to fall in order to prevent those bad things from happening?

So are you buying now? If so, what and where,

Our system is a boom and bust system. This happens when supply and demand cycles are allowed to get out of sync. with each other (Govt. policy) and the more they do, then their oscillations can increase and become countercyclical.

The greatest distance between cycles is when you get a slowing of one and an increase in speed in the other.

What I am seeing at the moment is a slowing in demand, which at the same time there is an increase in supply. This supply cannot be turned off immediately to match demand as it takes so long for our supply to come to market that much of it was started over 12 months ago and is committed to coming to market even if the demand for it has slowed.

Whereas in jurisdictions where supply is allowed to meet demand in almost developer real-time, then volume can match whatever is happening both on the way up and on the way down, and this allows the prices to remain a very stable low median income multiple, eg 3x median income.

I am seeing a trend at the moment with how newer houses are being priced in my area which are houses in small towns. The late 2020 GV tends to be around 600k, the homes estimated value tends to be mid 700's, and the asking price tends to be high 800's to 900k. These seem to stay on the market for about a month and either sell at a deadline sale / tender, or they may sell shortly afterwards. Older homes aren't selling as easily, mainly because many need so much money spending on them.

It is amazing how many older people I am now seeing starring at listings outside the different real estate agents these days. Never used to be much of a thing, but they are probably looking for their source of retirement income now banks aren't paying much on their savings i TDs.

"you have to ask, does what has happened in the housing market really pass the sniff test?"

So now the BNZ's chief economist has added a new tool to measure the housing market, that tool being "THE SNIFF TEST" WTF ???

None of their models seem to work very well so why not.

Not alot passes the 'sniff test' in the comments section that's for sure...

1) Its not house prices, its mainly real LAND prices that have risen.

2) None of the analysis above considers the existing shortfall in supply. We are nowhere near closing that gap yet.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.