This is a re-post of an article originally published on pundit.co.nz. It is here with permission.

For much of the time, an economy is in a boringly benign phase. New Zealand seems to be in one at the moment. This is not the way the commentariat present it. To grab your attention they magnify small changes arising from noise and measurement error to matters of significance. They do the same for political opinion polls, headlining as significant changes from the last time which are within sampling error rather than trying to see whether there are evolving trends. The challenge is to see the evolution.

I confess I have been looking for what economic historians call a ‘climacteric’, the time when perhaps, at first imperceptibly, the economy changes its direction. It is easy enough with a long data series to see after the event that it has happened, Even so, there are still scholarly disagreements about when and why the British and French economies went through one in the nineteenth century.

So when I look at economic forecasts I am usually looking at whether the apparently benign events have significant change going on underneath. Thus it is with the Treasury forecasts released at the budget. I focus on their numbers because they are in the public domain, reasonably detailed, and done by a forecasting team which has more than just pride in getting the predictions right; wrong ones can screw up the fiscal and borrowing stances. (Similarly, the RBNZ’s ones can screw up the monetary stance.) In any case, they tend to be in the middle of all the other macroeconomic forecasts.

I am going to compare the Treasury assessment of the economy before the Covid Crisis – almost all the data are in – and after – which are the Treasury forecasts. But first to deal with the Covid V.

When the covid lockdown struck, most informed economists – including me – assumed that it was a cyclical shock and used business cycle theory and our experience of past cycles to analyse it. In fact, the shock has proved much more temporary; it was more like the closedown over Christmas. Hence its the description as a V – up and down over a very short period (rather than for virus). Brian Fallow suggests the V also stands for ‘vindication’ (of the government response) and ‘vulnerable’ (to further external shocks). (I would add ‘vaccination’ because if we don’t do better with the rollout, we may get another nasty shock.)

The V means that there is a sense that after a year the economy is back on the pre-covid track (although the data is a bit mucked up). Admittedly there some sectors which continue to struggle, notably tourism. (My impression is that education services provided to overseas students was struggling before the external lockdown; I shall come back to that when trends are clearer.) Admittedly too, there are changes to border flows – importantly of workers – which require more consideration, but that maybe as much due to policy changes.

Perhaps this latter factor contributes to the Treasury assessment of a slightly slower population growth. From March 2013 to March 2020 the increase was annually 1.6 percent but it is expected to be only 1.2 percent p.a. from March 2002 to March 2025 (as far out as Treasury forecasts). Significant? I’ll spare you an hysterical rant.

Real GDP grows at much the same rate, so GDP per capita grows slightly faster. Because employment grows slower, the Treasury thinks that productivity will grow increases a little faster too. To be frank, the changes are so small that a forecaster would not die in the ditch to argue that the differences are significant.

Where they might be more concerned is the change in the level of nominal interest rates. Treasury reports the 90-day bank bill rate at about 2.5 percent p.a. in the period before the covid shock and forecasts 0.4 percent p.a. in the period after. As you would expect, longer term interest rates are more sluggish; the 10-year bond rate is 3.4 percent p.a. and 2.6 percent p.a. respectively. (Consumer inflation is roughly the same at 1.8 percent p.a. So the bond rate is expected to be marginally above the likely rate of inflation.)

What is going on? Lower interest rates may presage a climacteric in which the economy – the world economy – is going through some fundamental change. We need to be cautious here (as I said there is still debate about what was going on in the nineteenth century). Let’s go through some orthodox economics.

Low interest rates ought to stimulate business investment. fact, the Treasury thinks that business (non-residential) investment is growing faster than GDP after the covid recovery, although they are not predicting a boom. But the rise is driven by publicly-funded infrastructural investment rather than commercial business investment. The best explanation I can think of is that the low interest rates are an international phenomenon and that business is not investing, despite the low interest rates. So in richer economies, at least, business does not see profitable opportunities for its investments. One reason might be slower population growth; another is that there are insufficient new technologies and opportunities coming on-stream. Perhaps there is greater uncertainty which would discourage investment although is the world economy that much more uncertain today than before covid? It is all a bit of a puzzle.

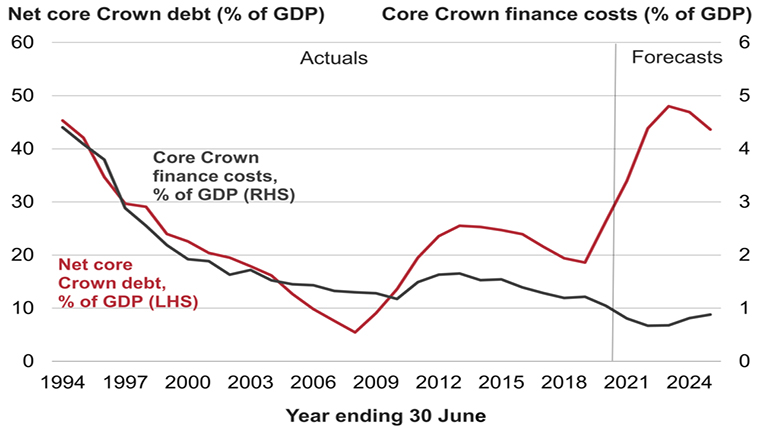

One curiosity – or should I say benefit? – is that while government debt may be rising throughout the world, our burden of debt servicing is not. Treasury reports that the New Zealand debt-to-GDP ratio was 18.6 percent in June 2019 and expects it to be 43.6 percent in June 2025. (Groans and hysteria from the commentariat). But the same graph forecasts Core Crown finance costs falling from 1.2 percent of GDP in 2019 to 0.9 percent in 2025. (Silence from the commentariat.) That difference is about $800m a year. Not a bad dividend; I leave you to spend the money or, if you are that way inclined, cut taxes by that amount. (My preference would be to invest it because the borrowing is still a burden on the future; however I favour soft investments such as on the environment, climate change, education and training and children.)

Of course, the forecasts may be wrong. Many of the risks are listed in Treasury’s Budget Economic and Fiscal Update 2021.It may be that real interest rates rise into more positive territory and the dividend disappears. But if they remain low, the economy is in a new ball game. Treasury no doubt appreciates the possibility but has not made up its mind. You may join them.

Brian Easton, an independent scholar, is an economist, social statistician, public policy analyst and historian. He was the Listener economic columnist from 1978 to 2014. This is a re-post of an article originally published on pundit.co.nz. It is here with permission.

12 Comments

Nice piece

Insightful piece - thanks Brian.

Do you think the chain of causality between low interest rates and business investment is over-egged and maybe even broken? Perhaps a *change* (reduction) in interest rate might make a marginal business case more favourable - but there are a lot of interacting variables here. Empirical studies also conclude that interest rates follow business confidence rather than drive it. Monetary policy appears pretty limp and lifeless? https://www.sciencedirect.com/science/article/pii/S0921800916307510

The last 500 years of capitalism suggest that periods of growth happen when capitalists find a 'fix' - something that unlocks resources or allows for an increase in productivity (the rate at which resources can be capitalised). Enclosure in the UK in the 19th century, industrialisation, colonisation, increased access to low cost labour and raw materials in the developing world in the 20th century, asset price bubbles in the 21st century (enabling increased consumption) etc. Perhaps we will see an end to the current 'benign' economy when capitalism finds it's next fix - or maybe we've run out of fixes that can be achieved without wars, ecological disaster, or unpalatable human misery?

I agree - economists need to seriously consider whether lower interests are a stimulus outside the theory books, and indeed whether they are more important as cause or effect. I still haven’t seen a convincing explanation from a mainstream economist of why Japan and the EU have so thoroughly failed to see growth *or* inflation from their low-interest-rate regimes, decades old now; or of why we should expect any better now we’ve joined the party.

Yes, agreed; "In fact, the shock has proved much more temporary; it was more like the closedown over Christmas".

However, there has been significant advantages and negative consequences for different groups within society.

My guess would be businesses have benefitted from demographic and societal trends that allowed them to forestall investment, by which I mean a bottoming out in the old age dependency ratio (2008 was the nadir in New Zealand) and female participation in the workforce (has flattened out at around 48% of the workforce, dropped slightly during the pandemic but will likely normalise this year.)

We're at a very interesting time because both those trends are turning now across high income countries. That probably means we'll start to see a normalisation of inflation over the next decade, possibly sooner if we get a deleveraging event in the next few years.

OADR: https://bit.ly/3x2lwbj

Female labour participation: https://bit.ly/3ptJTfG

This kind of article needs editor critiquing.

"So when I look at economic forecasts I am usually" - sorry, but economic forecasts are exponential, and ' usually' is linear.

"Real GDP grows at much the same rate" - my car has accelerated since I started my journey, so it will continue to accelerate at this rate of change.

"The best explanation I can think of is that the low interest rates are an international phenomenon and that business is not investing, despite the low interest rates. So in richer economies, at least, business does not see profitable opportunities for its investments. One reason might be slower population growth; another is that there are insufficient new technologies and opportunities coming on-stream. Perhaps there is greater uncertainty which would discourage investment although is the world economy that much more uncertain today than before covid? It is all a bit of a puzzle."

Only to an economist, Brian. The Limits to Growth is what is happening, you need to understand energy, entropy, and the exponential function. Try reading Clugston's Blip: https://www.amazon.com/Blip-Humanitys-self-terminating-experiment-indus… before writing anything else, eh? People take you as some kind of expert - read that book and see it their belief is warranted?

Some of us KNOW what is going on.

""Some of us KNOW what is going on."" - Wow. Sounds like a Trump supporter about to occupy a govt building.

Well you clearly did not know basic mathematical and physics concepts powerdownkiwi and managed to garner a few chuckles. So opinion pieces about opinion pieces about economics has you placed well. Unless the whole comment is a piece of obscure satire on the state of economic opinions...

paciica,

On what basis do you accuse pdk of not knowing basic maths and physics concepts? I rather think the boot is firmly on the other foot. there is no work without energy-there never has been. If you don't understand that, you understand nothing. I will quote very briefly from a recent report from the Geological Survey of Finland--The Mining of Minerals and the Limits to Growth. "Like all industrail activities, without energy mining does not happen".Our current economy has been built on the back of fossil fuels-primarily oil and its derivatives. The EROI(any idea what that means?) of all fossil fuels and minerals is declining. Go and look this stuff up.

pdk refers to a book Blip which I have in front of me. The book's subtitle pretty much tells the story- humanity's 300 year self-terminating experiment with industrialism. It proposes a year for this-2050. Now this is where there is some disagreement between pdk and me. I simply think that is overly pessimistic for a number of reasons I won't bore you with.

I actually agree wholeheartedly that economic growth can and will not be decoupled from energy and resource use, and that growth in developed countries needs to stop (we’ve got enough stuff). But the messaging is a bit harsh mate!

“Treasury reports that the New Zealand debt-to-GDP ratio was 18.6 percent in June 2019 and expects it to be 43.6 percent in June 2025. (Groans and hysteria from the commentariat). But the same graph forecasts Core Crown finance costs falling from 1.2 percent of GDP in 2019 to 0.9 percent in 2025. (Silence from the commentariat.) That difference is about $800m a year. Not a bad dividend”.

The Crown’s borrowing cost (currently low, as Brian points out) is not a reason in itself to borrow more. The Government is running the largest fiscal deficit of any NZ government in the last 50 years at a time when Brian says the economy is in a “boringly benign phase”. Sure the borrowing is cheap but it all goes on the Crown balance sheet. Not only does it have to be paid back in the future, but it restricts the ability of future governments to borrow within prudent limits. If there was something in the budget to spur productivity then perhaps there would be a good story to explain the need, but the budget was largely about redistribution. “But it’s cheap” just doesn’t cut it as an explanation for borrowing in the current situation.

You're right - it doesn't cut it because current low interest rates are not set by the market, rather by the printing presses of central banks.

This can't go on forever, so by Stein's Law has to stop sooner or later.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.