This Top 5 comes from interest.co.nz's Gareth Vaughan.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing the occasional Top 5 yourself, contact gareth.vaughan@interest.co.nz.

The chaos in the global shipping industry, that is causing headaches for importers and exporters, is unlikely to abate anytime soon. https://t.co/Oownv1824y pic.twitter.com/W8V8fIC4qN

— Sharon Zollner (@sharon_zollner) June 30, 2021

1) The rise and rise of contactless payments at the expense of EFTPOS.

Last year I went to town with a five part series on retail payments. In part 4 I looked at the potential for COVID-19 to kill EFTPOS.

Remember that when COVID-19 hit, banks waived fees on contactless Visa and Mastercard debit card transactions for business customers. The limit on contactless payments was also increased to $200 from $80 to encourage consumers not to touch payments terminals. Banks earn money through customers using Visa and Mastercard credit and debit cards and are incentivised to grow this business. The EFTPOS system, which involves inserting cards into payments terminals and entering a pin number on a key pad, doesn't charge per-transaction fees to merchants.

Below is a snippet from last year's article.

An executive with high level experience in the payments sector who spoke to interest.co.nz on condition of anonymity, worries that all this could ultimately be the death of EFTPOS. Especially if the fee waiving goes on beyond the initial three to six months proposed by bank card issuers.

"Coronavirus is almost disastrous in the sense of the demise of EFTPOS," the executive says. "With more and more [payments] terminals being activated [for contactless payments] people will develop the habit...[And] the banks essentially don't see a future [in EFTPOS] because it doesn't drive any revenue for them."

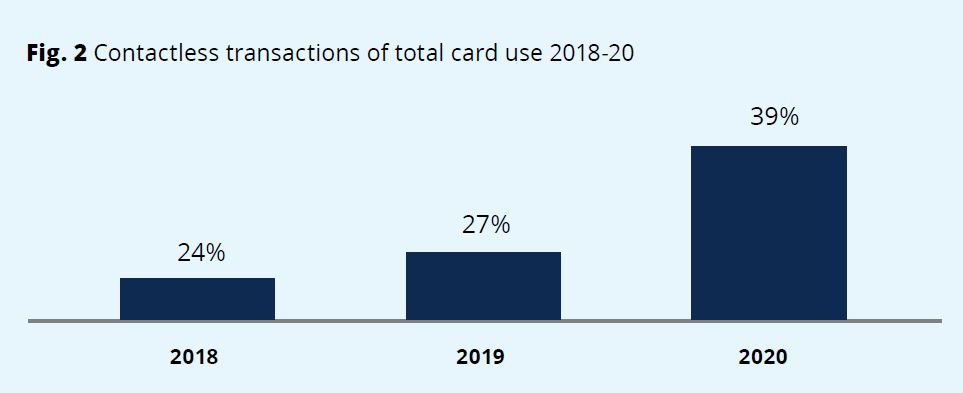

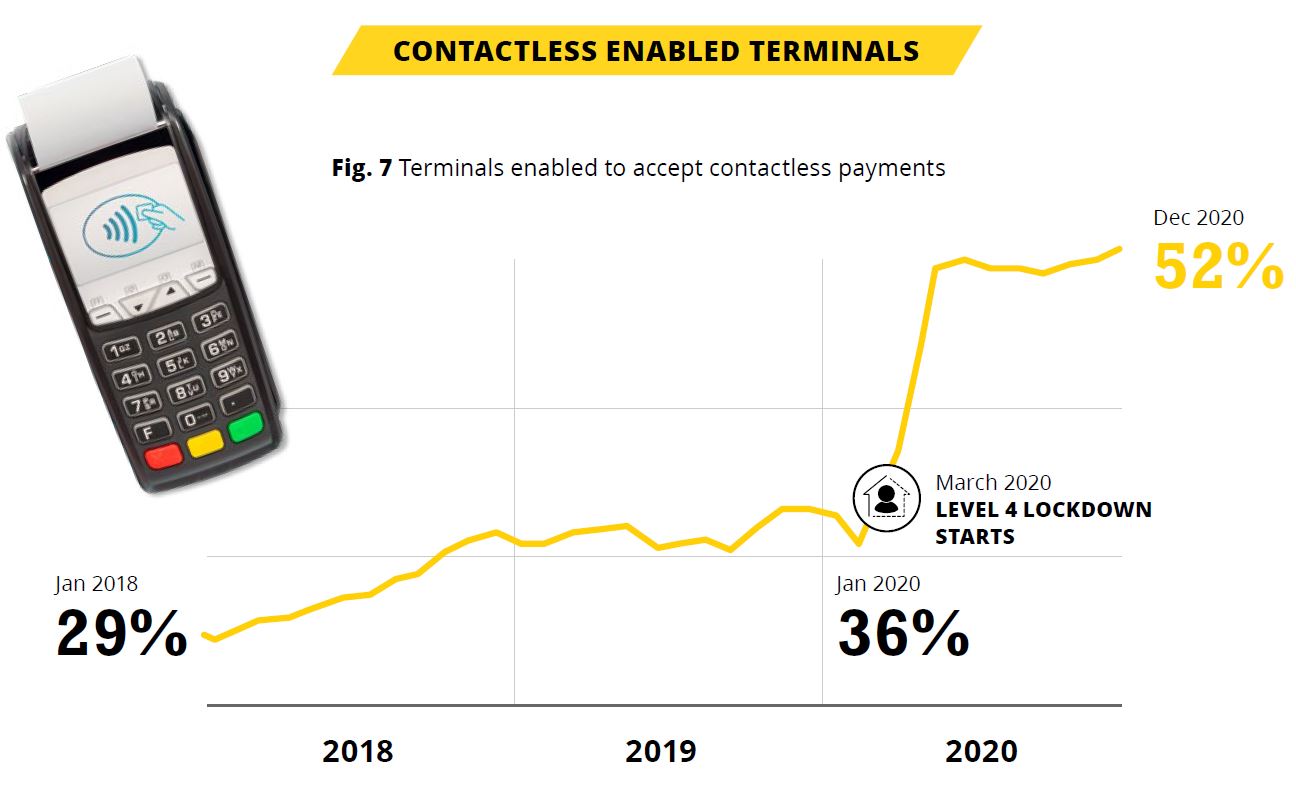

Now, Payments NZ's 2020 NZ payments statistics report (see charts below) shows a big increase in both contactless transactions and contactless enabled payments terminals.

There has been a 62% increase in contactless transactions since 2018, Payments NZ says. The Government has, however, moved to regulate merchant service fees.

2) IAG a potential takeover target?

The Australian Financial Review's Street Talk column raises the prospect of Insurance Australia Group (IAG) being a takeover target. Any move on IAG would be of massive significance here in New Zealand, remembering that IAG NZ is comfortably our biggest general insurer with about 52% market share. It operates the State, AMI, Lumley and NZ1 brands, as well as underwriting insurance for ASB, BNZ and Westpac.

The AFR cites John Lockton, head of investment strategy at Wilsons, who recently issued a report on IAG.

But with its share price still in a rut thanks to ongoing investor concerns, the business now looks like an attractive proposition - and not just to investors.

Lockton says IAG is priced low enough that it could fall into the gaze of the major offshore insurers as a possible acquisition target.

Overseas insurance businesses such as Japan’s Nippon Life and Dai-ichi Life have already shown interest in local companies.

Nippon acquired an 80 per cent stake in MLC Life Insurance from NAB in 2016, while in 2011 Dai-ichi Life acquired Tower Australia (now called TAL), before buying Suncorp’s life insurance business in 2018.

“Berkshire has just under [a significant holding] in IAG, but the register is otherwise open,” Lockton said.

“[It’s a] duopoly market [and it has] strong cash generation. Global players as we have seen with Life insurance don’t mind Australia.”

Any takeover of IAG along the lines suggested by Lockton would, of course, largely play out overseas. But with the Reserve Bank of New Zealand the prudential regulator and supervisor of insurers active in NZ, its approval would be required for a change of IAG NZ ownership.

3) A long trip to nowhere.

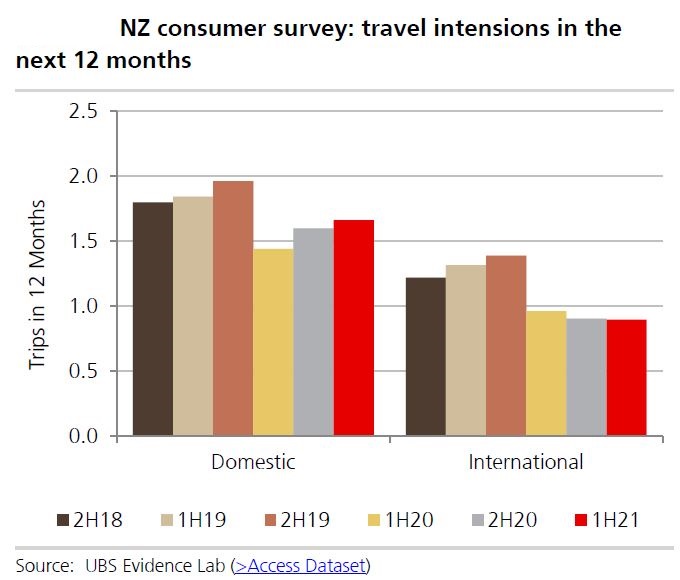

We all know how hard COVID-19 has hit Auckland International Airport with flight volumes plummeting. Now UBS analyst Marcus Curley has issued a report predicting a slow road back to something resembling pre-COVID life for the airport. The report's title is; A long trip to nowhere; downgrade to Sell.

Curley doesn't expect a return to unrestricted international travel before 2024, which he says is 12 months longer than share market expectations. Thus he has lowered the UBS rating on Auckland International Airport shares to "sell" from "neutral," until a more attractive entry share price emerges, or we're closer to unrestricted international travel.

Curley reckons international passenger numbers will return to pre COVID-19 levels in about 2025, reflecting a progressive re-opening of NZ borders in 2023 after the vaccination programme is completed in mid-2022, and airline seat capacity reaches 90% of pre COVID-19 levels in 2024.

…unrestricted travel unlikely before FY24 [full-year 2024] & structural drop in airline capacity…

We have pushed back the start of NZ border re-opening by 3 months to mid-2022 reflecting a slower-than-expected vaccine rollout. In additional, in line with industry feedback, we now expect a more cautious approach to NZ border re-opening, staged over 12 months starting with low-risk countries and vaccine passport requirements. Plus Tasman travel bubble experience and NZ consumer survey points to a gradual recovery in demand, especially by NZers. Once all borders are open in full-year 2024, reduced airline seat capacity sees international passenger volumes at 90% of pre COVID-19 levels. In particular, our analysis suggests Air NZ international seat capacity will be at 95% of pre COVID-19 levels in FY24 with retirement of B777-200s partly countered by new B787s.

…creating extended period of earnings downgrades and no valuation support

We lower our NPAT [net profit after tax] forecasts by 54%/17% in FY23E/FY24E [full-year 2023 estimate/full-year 2024 estimate] mainly reflecting a slower than expected recovery in international passengers. In addition, we have incorporated an extended period of retail rental abatements, deferral of aeronautical PSE4 [price setting event 4] reset until FY24, and a substantial reduction in capital expenditure from pushing back the new domestic terminal and second runway. Our revised FY23E/FY24E NPAT of $137m/$249m is well below market consensus of $235m/$285m.

Valuation: $6.65/share (was $7.30) in 12 months' time

Our 12-month forward DCF [discounted cash flow] is $6.70 (was $6.95) and SOTP [sum of the parts] is $6.60 (was $7.65). Our SOTP is based on FY24e to accommodate normal air travel, then discounted back. The 9% decline in our price target mainly reflects earnings downgrades.

Curley's sceptical about the government vaccination targets being met.

Based on vaccination rates in US and Europe, NZ’s vaccination target of 80% of people occurs by mid-calendar year 2022, being 6 months after the NZ government target. This doesn’t allow for potentially greater vaccine hesitancy in NZ given the country’s low COVID-19 death rate. Ongoing management of COVID-19 most likely sees international travel start with low-risk countries with vaccine passport requirements. Domestic and trans-Tasman travel experience points to a gradual build-up of route demand once quarantine-free begins. Our analysis suggests key airlines servicing AIA [Auckland International Airport] will restart in full-year 2024 with seat capacity at ~90% of pre COVID-19 levels based on announced fleet changes, including Air NZ at a maximum of 95% of pre COVID-19 levels. A partial exit of its B777-300 fleet, would see Air NZ seat capacity at 85% of pre COVID-19 levels.

At end June, NZ single dose vaccination rate was at 15%. This is slightly below NZ government plan mostly reflecting more limited vaccination stock deliveries. Moreover, NZ government plan assumes an average daily vaccination rate of 0.8% of population (38k or 8k per million) in second-half calendar year 2021. This is well above rates in the vast majority in other OECD countries, and substantially above NZ flu daily vaccination rate of 0.3%.

4) The great pandemic tipping boom.

Tipping is not really a thing in New Zealand, but anyone who has been to the US of A knows how big of a deal it is there. Writing for The Atlantic, Saahil Desai looks at what impact the pandemic has had on tipping, with the help of payments company Square.

What Americans actually tip, both now and before the pandemic, is an enduring mystery. The Department of Labor fastidiously tracks the smallest movements in wages, but no government agency even tries to monitor all the extra bills that get strewn on restaurant tables. To understand how the size and frequency of tips might have changed since the start of the pandemic, and whether they are changing back, I reached out to Square, the payment company that processes credit-card transactions for millions of small businesses. Square isn’t just how you use your credit card to pay for those heirloom tomatoes at the farmers’ market; a large number of American restaurants are also on the platform. That means all the tips that get tacked on to credit-card transactions using Square are also counted up and stored.

The company provided me with data going back months before the pandemic, on how often restaurant customers were giving tips, and how big those tips were. The numbers show that the Great Pandemic Tipping Boom was real, if perhaps a bit less great than I’d expected. In the innocent times before March 2020, the average tip when cards were swiped at sit-down restaurants never strayed outside a very narrow range of 19.9 to 20.1 percent—corresponding to the tipping norm that, coincidentally or not, is also incredibly easy to calculate. Then, on March 24, as stay-at-home orders began to pile up and Americans clapped and howled and clanged pots in appreciation of essential workers, the average tip did something weird: It started drifting upward. Within a few weeks, the average hit a peak of 21.0 percent. When the first pandemic wave receded, tips fell off a bit, to roughly 20.4 percent over the summer; they came up again, to 20.8 percent, during January’s massive spike in cases. Even now, as fully vaccinated Americans return to their normal lives, tips remain higher than where they were in 2019. In the past few months, the average appears to have settled at 20.6 or 20.7 percent, well above the pre-pandemic norm.

5) Poking fun at finance: "It's hard not to meme this stuff."

I stumbled across this Bloomberg TV interview with Kyla Scanlon, who is described as a financial content creator and influencer. It's interesting seeing a knowledgeable young person having some fun with the crazy financial world of 2021, albeit from a US perspective. You can see Scanlon's latest video below.

The Joy of Price Fluctuations with Inflationary Expectations pic.twitter.com/GXlKoTmnRh

— Kyla (@kylascan) July 1, 2021

8 Comments

"Curley doesn't expect a return to unrestricted international travel before 2024..."

I hope not, I've family abroad and don't want to be held a hostage for political reasons once the vaccine has been rolled out.

What would it achieve to keep borders closed, Covid-19 will become endemic in human populations. Why would the country live in denial until 2024? It's not likely to hurt any less then than it would in the near future.

What's the problem Squishy ? New Zealand does not stop you leaving.

On the way back in you do have to abide by some things about infection. Which are fair enough. Bit tricky, but you can travell.

So? Go see the whanau

With CF of MIQ, a planned overseas trip, outside of Australia and Pacific islands or any other bubble with odds and sods, of say a month is likely to extend how long? Pick a duration between 3 to 9 months

Yeah, well, it sounds like the Australians are starting to talk about managing Covid-19 with the tone if the public changing substantially and politicians responded:

https://www.smh.com.au/politics/federal/the-end-of-australia-s-zero-cov…

The government in the New Zealand likely enjoys more goodwill due to fewer lockdowns to date.

Sorry to say Squish but the pandemic has to be kept going till the next election.

The "Rally 'round the flag" effect won't last that long.

Also New Zealand might be found to violate "Right of Return", there's a test case against Australia going to the UNHCR. When the articles where written there wasn't actually any allowance given to countries to decline to repatriate their own citizens even in exceptional circumstances:

https://en.m.wikipedia.org/wiki/Right_of_return

Can't wait for Gov Coins to become a reality in this country. EFTPOS as we know it today may be the kind of infrastructure already in place to support the roll-out.

Cordell doesn't understand finance.

Love the cartoon !

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.