By Bernard Hickey

Someone has to say this loudly in public and it may as well be me.

Bank profitability in New Zealand is too high and we have to do something about it. It's time regulators and customers hammered their banks into producing fairer returns that help the economy grow healthier. That means lower mortgage rates and higher term deposit rates.

Don't take my word for it that the banks are too profitable.

The Reserve Bank Governor Alan Bollard said as much recently in a very under-reported speech to the New Zealand Shareholder's Association in Tauranga.

"It seems unlikely that the rates of return in banking enjoyed over the past decade can be sustained in the future,"

Bollard said in a 10 page speech packed full of detail showing how high bank profitability was and trying to explain why it was so high. After tax return on equity for the banks averaged around 18% from 2002 to 2007. See the full speech here.

This made them the second most profitable set of banks of a sample of 22 OECD countries conducted by the Reserve Bank. They were even more profitable than their parents in Australia, who third most profitable behind the Slovak Republic and New Zealand.

The last two weeks of profit reports from ANZ, ASB and Westpac underline just how profitable these banks are again, despite the weak growth in the economy and virtually no lending growth.

Banks have boosted their profits by quietly allowing their net interest profit margins to rise and they have seen their bad loan costs fall as the economy recovers. See more here from Gareth Vaughan on growing bank profitability and the need to haggle.

The latest bank leverage and return-on-capital data, by individual bank, is here »

Many may ask, how did the banks increase their net interest margins at the same time that mortgage rates were unchanged? Partly it has happened because banks pumped the effects of higher funding costs from the Lehman Bros crisis into their margins in 2008 and 2009 and haven't taken them back out as those wholesale market funding costs have fallen through late 2010 and early 2011. Floating mortgages are also more profitable for the banks and there has been a big shift to floating from fixed over the last year.

Close to 60% of all mortgages are now floating because they are nominally cheaper for borrowers, but more profitable for banks.

Back on July 1, 2005, the margin (what the bank pays to borrow versus what it charges to customers) on a floating home loan rate was 1.87% with the average bank floating rate at 8.90% versus the 90-day bank bill rate of 7.03%.

As of last Friday it was up almost 100 basis points to 2.85% with the average bank floating rate at 5.73% versus the 2.88% 90-day bank bill rate.

On July 1, 2005, when fixed mortgages were still all the rage, the average margin between the two-year swap rate and two-year fixed-term home loan rate was just 0.92% with the two-year swap rate 6.68% and the average bank two-year fixed rate 7.60%. As of last Friday it had more than trebled to 3.07% with the average two-year fixed rate at 6.41% versus the 3.34% swap rate.

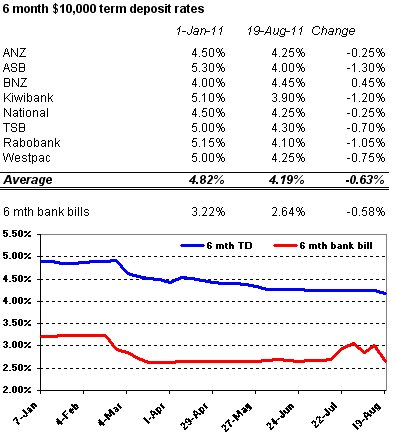

Also, term deposit rates have slowly fallen through the year as competition between the banks for such deposits has eased back.

The average bank one year term deposit rate has fallen 71 basis points this year. See more here on falling term deposit rates here from Gareth Vaughan.

All this meant the banks' net interest margins are rising. ASB reported this week its net interest margin rose 40 basis points to 2.08% this year.

Reserve Bank figures show the banks' combined net interest margin has risen to 2.23% by June from 1.87% in September 2009. New Zealand households need lower mortgage rates. The Reserve Bank can't cut the Official Cash Rate without fueling inflation.

It needs the banks to do that work by cutting mortgage rates. Savers need higher term deposit rates to help lift national savings.

It's time the banks played their part.

55 Comments

Good call BH, but as a Kiwibank customer with a variable mortgage, I'm not sure what I can do to help force rates lower. NZ needs more people to switch, and keep switching to the bank with the lowest rates...perhaps we need a government endorsed campaign like we are seeing in the electricity industry.

It costs too much to change mortgages so it has to be a big difference in rates before you'd do it. You can't just switch like you do for power.

It's actually much easier to switch than you'd think. Threatening to switch is really, really easy.

I did it via a Roost mortgage broker and managed to get ASB to cut my floating mortgage rate to 5.39% from 5.75%.

Try it.

You might get lucky.

cheers

Bernard

Good try Bernard but the banks farm the country...so you can forget about any real help from govt or the RBNZ on that score...best concentrate on getting the public to stay away from the banks...

I think the banks are being allowed to make extraordinary profits to restore their books, give them some fat before the storm hits

Interesting piece and of course profit is usually related to risk for stakeholders including retail creditors. In the US and Europe retail bank deposits are covered by government guarantee. In NZ and Australia they are not. Here living will legislation for banks is scheduled for early 2012 when creditors will take a haircut if a bank falters but a run on the bank is avoided along with taxpayer guarantees. Recent funding changes have also affected depositor risk. NZ banks can source covered bonds backed by ring fencing up to 10% of their assets. Any foreign currency denominated bonds carry exchange risk. When the Bank of Ireland faltered in 2010 headlines screamed its loan to deposit ratio was 160%! Its just one rough indicator but some of the big banks here seem to be around or above that %. Perhaps the credit rating agencies re-evaluation of NZ subsidiaries after downgrading their Aussie parents will shed more light on how high profits have been earned.

Three things:

1) "It's m' bad debt provsions guvnor', honest." Remember that one? Yeah right!

2) Banks are there to work for their shareholders. RBNZ is, supposedly, there to work for it's main stakeholder, NZ. It's just that the banks are better at their work than RBNZ is at theirs, simple.

3) What regulatory ratios would ameliorate the problem? (C'mon, they should be on the tip of your tongue.) Why haven't they been implemented given NZ would have benefitted in other ways, eg. better control of non-tradeables inflation, with less overvaluation influence on NZD and improvement in national savings rate? Who benefitted because said regulation was not implemented? (Sure as hell wasn't RBNZ's main stakeholder, was it.)

Cheers, Les.

PS - over to you Wolly.

Zigzactly right Les , banks have a duty to create a profit for their shareholders . One only has to tootle over to the ASX to purchase a slice of the action .

..... it's called the Capitalist System , Bernard . I'm disappointed that you disapprove of it . For a moment back there , I thought you'd joined us on the path of thrift & innovation , to walk on the Light Side .... But alas , back to the " friends of NZ Labour " you go .

In terms of competition maybe more of this kind of thing might help:

It was on Campbell Live last Friday night.

Hard to believe eh.

Cheers, Les.

Gummy,

I'm all for capitalism where we get competition and we don't have governments bailing out 'Too Big To Fail' institutions. This creates a moral hazard and a type of taxpayer-driven subsidy.

Consumers can do their bit.

The RBNZ could do some interesting things that could increase the potency of its monetary policy power without further damaging exporters. Forcing banks to match their funding with their lending (in NZ dollar terms) would reduce our foreign borrowing and increase term deposit rates.

It would allow the RBNZ to keep the OCR lower for longer.

What's not to love.

Unless you're a bank shareholder.

cheers

Bernard

Bernard vs Gummy 0:2 and still no sign of improvement. Bernard can you not feel it ? It is right up there. He's juggling you.

Yes indeedy , Walter . The Gummy one is beavering through : " Lessons from the Art of Juggling " by Michael Gelb & Tony Buzan . .. Marvellous wee tome .

.. although I doubt that I'll be juggling Bernard anytime soon ... no offence big guy , but the hernia belt doesn't exist which could take that strain ...

Gummy, I’m sure you read the book “The two P’s - Propaganda & Politics” by Nathan Silverstein many times.

First that I've ever heard of it . Thanks for the tip , will try to get a copy ..... I'm altogether too soft on the namby pamby scum sucking socialists . Hope that the book will toughen me up a bit .

...... cheers !

There it is Roger, one particular ratio that should be tip of tongue:

"The RBNZ could do some interesting things that could increase the potency of its monetary policy power without further damaging exporters. Forcing banks to match their funding with their lending (in NZ dollar terms) would reduce our foreign borrowing and increase term deposit rates."

And it could be varyied beyond 1:1 if we really want to get serious about rebalancing the economy, wouldn't you say Rog?

"The world has once again cottoned on to the fact that the enormous overhang of debt it discovered back in 2008 has not been dealt with, but has instead been passed from households to banks to governments and, hence, back to households again... the upshot of those negative interest rates is to help erode away.....debt. It is appalling news for savers, of course. But this “financial repression”, in which a captive financial system accepts sub-par returns, was precisely what helped shrink ... war debt after 1945. ."

From the automaticearth

The Domino Effect of Europe Bank Woes

by John Carney - CNBC.comThere’s also the problem with hedge funds trying to hedge exposure to European banks. The short-selling ban on European banks makes hedging exposure more difficult. One response by some hedge funds will be to short U.S. banks as a proxy.

Ilargi: I'm sure you can agree that that is funny, no matter how tragic it is.

The tragedy that's unfolding is shed in an even clearer light when we expand the stats series to include the longer term, in this case 5 years.

In the past 5 years (dating back to August 25 2006, a date I took from Google Finance), these are the loss numbers for financials, as taken at noon, August 19 2011:

- Bank of America : - 86.68%

- Citigroup: -94.33%

- Morgan Stanley: -70.72%

- Keycorp: -83.46%

- Fifth Third Bancorp: -76.06%

- Barclays: - 76.85%

- RBS: -96.83%

- Société Générale: -83.57%

- BNP Paribas: 60.64%

- Crédit Agricole: -81.39%

- UBS: -75.27%

- Credit Suisse: -52.92%

- Deutsche Bank: -65.26%

The numbers are made even more poignant when we look at losses at the Dow and the S&P in the same time period.

- Dow Jones: -3.97%

- S&P 500: -12.81%

If this happens to house prices here then the banks are finished, have look at it sale price in 1989

http://www.redfin.com/CA/Vallejo/363-Catalina-Way-94589/home/2265725

NZ - land of the long white rip off

Check a little further .. over the past 5 years the 4 banks have moved aggressively into the wealth management sector and now have influential "control" of 80% of the "funds management industry" through their investment platforms, financial advisory networks, insurance subsidiaries, and have that much power over the $1.4 trillion AU compulsory superannuation megalith.

To pick one bank at random , the ANZ , the 2009/10 annual report shows 411 692 shareholders . From 1 to 1000 shares , there are 211 496 shareholders . And from the 1001 to 5000 shares range , a further 163 252 folk . The first group holds a combined 87 million ordinary ANZ shares , and the latter group controls 364 million shares .

....... wow , there's fourth tenths of a million holders of ANZ ordinary shares . Gosh , alot of people stand to benefit if the bank makes a decent profit .

Speaking of which , in the last 5 years the ANZ has paid the following dividends : 126 cents ( 2009/10 ) , 102 , 136 , 136 again , and 125 cents in the 2005/06 year .

On the current price of $A 19.50 , the ANZ is paying a historic 6.46 % yield . Wow ! That's better than money in the bank .

... crikey , those 411 692 people who own ANZ stock have reason to feel very pleased with their investment .

Unless their entry to the stock was between Nov. 04 and Sept 08, or Aug 09 and now ( when the stock price was above the current $19.50). In which case their dividend has to be viewed in the light of an unrealised capital loss; especially so for those unlucky enough to pick Oct. 07 ( $31.47) as their jump in point! That's a paper loss of 38% ...so far. Or the fact that ANZ is still offering Aussies 6.25% for term deposits at the mom. with no capital risk :)

ANZ earnt $A 2.24 / share of profit in the 2006/07 year . Buying their stock at $ 31.47 in October 2007 gives an earning yield of only 7.1 % ( inverse of the PE ratio ) , and a dividend yield of just 4.3 % .

..... that was alot to pay for an Aussie bank . And so I didn't . Did you , St Nick ?

[ .. anyone fortuitous enough to buy ANZ stock at just $A 12.06 per share on January 19 , 2009 ... would be sitting on a hefty 62 % capital gain today ..... plus dividends ... Gummy can " cherry pick " too ! .. ]

The answer is simple, stop using the banks and contributing to their profits.

Don't have a mortgage and they can't make money from you. Don't have any deposits and they can't lend that money out 63X over to other suckers to get mortgages.

That is the choice you have.

If you have a mortgage and go into negative equity, you only have yourself to blame for participating in the fraudulent scheme.

And lets be clear on this, the system is fraudulent. Once that is drawn to your attention, then you become a criminal by participating.

I have said to you before Iain that your commentary on the money supply is excellent, although long winded. I have no doubt about the fraudulent nature of it all.

The big disappointment was to learn that you are in the thick of it yourself. You choose to participate fully by having a mortgage, it sounds like for some considerable time also.

As I say, by participating then you are guilty. How can your brand of politics be trusted?

So I am left in a situation where I wonder what exactly you stand for.

For me, now that I know I will take steps to slowly wean myself off. I don't have a mortgage or pay rates, I make/catch/grow my own food where possible. My money in the bank is limited, my bank transactions only what is absolutely necessary.

I negotiated hard on the rent Iain. Landlords return on capital, assuming he is freehold, would be about 2%. The rates woud be about 25% of my rent, so I while perhaps I do pay them it actually comes out of his income more than mine.

Very poor form , Iain , to accuse St Nick of deception . He is one of the good guys around here . Play the ball , not the man !

...... and for what it's worth , just to burst your latest conspiracy theory , the majority of those companies you list are in control of hundreds of millions ( $A ) of superannuation monies ........ and they invest it where , where do you think , hmmmm ?

Good stuff thanks BH. The banks seem to be keeping their dividend policy at the same levle so I do not know about retaining profits for losses to come

Not wanting to deceive the astute types who frequent this forum , are we Iain ?... Nor to deceive ole Gummy as well ?

..... but that is not Bunnings Warehouse you have quoted and maligned , above . A small matter , Iain , but it is in fact a separate listed entity called Bunnings Warehouse Property Trust . They own the majority of the sites that the warehouses are on . They lease them to Bunnings Warehouse , who are themselves a division of the Wesfarmers Group , from Perth , WA .

There's a trillion bucks Iain , an ice cool trillion with a capital " T" , accumulated in the compulsory superannuation funds across Australia .

... is it a coincidence that the companies responsible for investing this money frequently turn up on the majority ownership lists of larger companies listed on the ASX & the NZX , ..

... or is Gummy trying to trick the good folks at interest.co.nz again ?

Which bank granted you a mortgage , Iain ? ..... I want to dip into their annual report to see if they have a dedicated Parksy Page for you , with a nice photo of you in the truck .... and a caption , oooooh , I don't know ...

... something like :---

" Loyal client Iain Parker , of New Zealand , merrily driving us to greater profits in 2011 and beyond " .

Drive " merrily " do you , Iain ? Remember Bill Murray to the Groundhog , " don't drive angry , OK ! "

"What is physically possible is always fiscally possible, but not the other way around."

Hence debt....and hence I have to Q it ever being repaid.....the assumption is of course its underwritten...what happens when ppl figure out it isnt?

regards

Ok, so tomorrow I will call into my local Westpac branch and ask for a reduction on my floating mortgage. Wonder what the response will be?

Why do the people of NZ allow foreigners to bid up the price of their land? How many other countries have such a policy and could it be the banks that stand to gain the most? Just a thought...

Well these are all publicly traded companies (except Kiwibank) so if they're on to such a winner then just buy some shares. You can use the dividends to offset your mortgage.

Well said , that man ! ... Exactly . . Wotcha gotta say to that , Bank Hater .... .... ooops , . .... ... apologies for my Froodian slip , .......... wotcha say to that , Bernard Hickey !

Gummy

Love your froodian slips.

But reluctant to be branded a bank hater. It's nice our banks seem better than the ones in America, Britain and Europe.

But we're right to push back against government guaranteed profitability near 20% ROE.

cheers

Bernard

oohooh me I'll be the Bank Hater ....yesireebob...shoot a banker and relieve some of your tension.....Baby eating bastidos to a man .....

Im actually quite surprised a few have not been shot, hung or otherwise delt with....

Hmmm I wonder how long it will be before our first casualty results....

regards

795 561 : Holy shit , Batman .. that is the number of shareholders in the CBA , the Commonwealth Bank of Australia ... imagine if they all wanted a printed copy of the 241 page 2011 annual report ....... sheeeesh !

... 587 741 of those folk own between 1 and 1000 shares in the CBA . A total 196 677 335 ordinary shares , or 12.62 % of the grand total 1558.7 million shares .

So an average " small investor " has 335 CBA shares , $A 15 259 worth ( ASX : CBA , Friday close $A 45.96 ) . And they collected $A 3.20 in dividends ( 6.96 % yield on current share price ) , per share , or an average $A 1072 per small investor .

... the NZ proportion of CBA's $A 6835 million net profit was a mere 7 % , just $A 470 million ,( ASB ) .

Cowabunga ! .. there's a heaping big number of folk gaining a well deserved profit from this splendid firm .

GBH: This post contains actual verifiable facts. Facts are not welcome here. In future please stick to rumour, speculation, opinion (half baked, never well done), accusation, conspiration, allegation and maybe perspiration. But not facts. Upsets the big guy.

Well deserved eh.

So you buy are stolen Porcshe with a market value of $100K for $10K, does that make it a well deserved purchase?

Thumbs downs scarfie. Go deliver your copies of the Commie Daily News.

If you were familiar with my posts I don't think you would make such an amateur allegation.

I would be interested in what you think the bank lending out $9 or ever $1 deposited is if not fraud.

Most people have no idea it is happening and I doubt they would consent if they knew. Even more so if they understood the implications.

You however have no excuse.

Granted, and for the most part I don't propose solutions because they will never happen because of this.

They won't care until they don't have slops, a distinct possibility:)

Scarfie old bean..it's not just 9 for one..the 9 moves to become deposits in other banks and each one creates 9 more..all part of parky's nightmare scarfie and it explains the gargantuan splurging madness the RBNZ failed so fabulously to control in the bubble....

You are living in a total F%$#$@ mess scarfie...it's called an economy...look who's in charge!

I know, I was being conservative.

You might have seem my posts comparing M0 to M3, which is 63:1. Gee and people think gold will be no good.

Love that headline scarfie..."the hunt for Gadaffi's gold"...pretty soon it'll be..."the hunt for american gold".....the last straws have been loaded in the Camel....hear that cracking sound!

Hehe yes, I cringe when I watch the news. Be interesting to see how things pan out, and whether stratfor.com are right. Going off the news last night you would think Libya is done and dusted.

And were you referring to those gold coated tungsten bars America has?

It's been fun Iain . Goodnight .

The banks make high profits because they can. I know, not funny. The issue is why is it they can make that much profit. I'm quite sure on this forum we have a pretty good idea by now.

"That means lower mortgage rates".. Seriously?! Only on mortgages less then 60% ltv yeh. Make that 50%.

There are many who know why they can make that much profit, but there are a lot more who don't want to admit that they've overpaid for their high priced shelter.

Maybe they're saving for rainy day, what with all the excrement hitting that thing that spins on the ceiling & all the last few years.

Has anyone delved into their financial statements to see if cash has been increasing?

Maybe if NZ banks didn't have their interest rates dictated to them by the OCR there might be some competition between banks?

They can set what they like actually.....and do....or is there a method that stops a bank setting a rate lower than the OCR?

Competition is sadly lacking....yes.........

regards

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.