Here's my edition of Top 10 links from around the Internet today.

We have a Monday-Wednesday-Friday schedule for Top 10. Bernard will be back with his version this Wednesday. We will have another guest posting on Friday.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz.

See all previous Top 10s here.

1. Europe's fiscal wormhole

Europe is in a tight spot economically.

The hunt is on to find a stimulus solution.

France wants to stimulate with more debt. Germany insists national debt limits remain.

The regions best brains are trying to square the circle.

At the same time, deflation looms. The ECB's Draghi has a plan, but it is constrained by previous rules and faces German opposition.

Up steps Guntram B. Wolff with a cunning plan.

With all of the rules pointing toward recession, how can Europe boost recovery?

A two-year €400 billion ($510 billion) public-investment program, financed with European Investment Bank bonds, would be the best way to overcome Europe’s current impasse.

Borrowing by the EIB has no implications in terms of European fiscal rules. It is recorded neither as new debt nor as a deficit for any of the member states, which means that new government spending could be funded without affecting national fiscal performance.

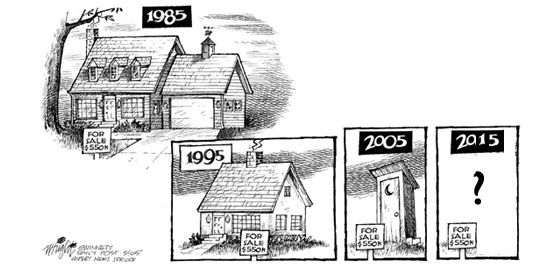

2. Distorted values

Last month the RBNZ published data that showed the 'value' of our houses was a remarkable $725 bln as at March 2014, a rise of more than $53 bln in a year. Heck, last week Statistics NZ reported that the total of our exports for the year to September was only $51 bln. I am sure when we are able to match September data, the gain of 'property' over 'exports' will be even greater.

It's a distortion because companies who export pay tax on their businesses, whereas those housing gains are all exempt from tax.

It's a distortion because those exports are companies 'revenues' and not their profits, whereas that housing $53 billion is all an untaxed gain.

To expand the RBNZ data, we took the Census counts of dwellings, updated it with [delayed] building consent data, and valued these by QV's average values. That gives a good look at just where the housing 'value' lies and exposes how distorting the Auckland market is. A third of the national population is in the Queen City, but more than 45% of the housing value is in this one city.

But the data also showed other interesting and somewhat unexpected insights. For example Hamilton has a bigger population than Tauranga, but its housing value is lower.

And another somewhat surprising insight comes by looking at the 'playground' regions. Coromandel and Whangarei Districts have their housing stock and values pumped up by holiday houses. The Census shows that 'unoccupied' houses represented 49% and 20% respectively of all those regions' houses. In Queenstown-Lakes it was 28%.

But 'holiday house' distortions are nothing like the madness that is going on in Auckland.

3. Long-term tendencies point downward

By the time you read this, the results of the ECB bank stress tests will be known. But Mohamed El-Erian, the former PIMCO head says this is now probably a side-show. He spoke about how Europe's core countries are failing to adequately confront their flagging economies.

Soon, banks will no longer be the biggest risk to the financial system and the economy. And five years from now, many credit institutions will be smaller than they are today, having discontinued some types of business, and will better support the real economy.

The US, the UK, Ireland, Iceland, Greece and other countries fell in love with the wrong growth model. They believed that - following the agrarian economy, industrialization and the service economy - the primacy of financial industries represented the next step of capitalism. Financial service providers that supported the rest of the economy turned into banks serving only their own interests.

Of course the euro zone could have done better. The high unemployment rate, particularly among the youth, is alarming. But the same applies for the US, UK or Japan -- there is too little investment overall, and reforms to labor and production markets are incomplete. With the exception of Germany, the highly developed economies slept through their opportunity to renew themselves.

Neither the Fed nor the ECB believe anymore that this model is sustainable on the long term. With their loose fiscal policy, they merely want to build a bridge until a system has been established in which banks play a serving role again.

And I'm afraid that the malaise and the weak growth will be here for a long time. Some politicians still don't realize how serious the situation is. They believe it's only a cyclical problem, just as there have always been periods of economic downturn and periods of boom. But the long-term tendency points downwards; the capacity to grow is declining continuously.

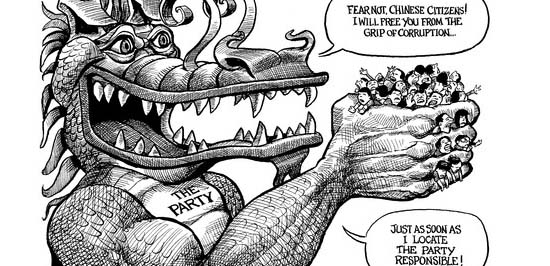

4. Graft on a grand scale

The scale of the transfer of bribes out of China is truly impressive. The AFR has a major review of the problem and Australia's part in it as a destination. There seems little doubt that New Zealand is also a destination, but that is just my opinion.

The AFR report however points out how difficult it will be to prosecute the Chinese bribe takers in Australia: they will no doubt get protection because the penalty for corruption in China is death. I suspect that will be another sore point between Australia and China as they try to negotiate an FTA (along with coal tariffs, the AIIB, and others).

The Chinese are calling it “Operation Fox Hunt” and the numbers involved are staggeringly large. The Washington-based Global Financial Integrity group has estimated that $US2.8 trillion flowed out of China illegally between 2005 and 2011.

The Central Commission for Discipline Inspection, China’s top corruption fighting body, estimates the figure could be as high as $US1.5 trillion for this year alone.

5. woops

Very low interest rates are unstitching some multi-lateral arrangements. The latest to be caught by them is the IMF, as the FT notes:

The SDR rate is what the IMF pays to its lending nations for the use of their funds. It then adds a margin to calculate the rate on its loans to Greece and other countries. The change will ensure lenders get a small positive return and fractionally raise costs to borrowers. The rate is calculated as a weighted average of the three-month risk-free rates in euros, yen, dollars and sterling.

After staying positive throughout the financial crisis, that basket has threatened to turn negative in recent weeks, as both the euro and yen rates have fallen below zero. They were affected by the European Central Bank’s move towards negative rates and continued easing by the Bank of Japan.

The most recent weekly calculation came in at 0.03 per cent. That reflected a euro rate of minus 0.02 per cent, a yen rate of minus 0.01 per cent, a dollar rate of plus 0.01 per cent and a sterling rate of 0.05 per cent. That rate will now be replaced by a 0.05 per cent floor from next week.

The possibility of negative rates caused several problems, according to a senior IMF official. There is no legal basis in its articles of association for paying a negative rate; it would have created a perverse situation where creditors were paying to lend money to the Fund; and it would have frozen up the SDR market as no country would have any reason to participate.

6. 'Speed is dangerous'

Here is a holiday Monday article that is worth taking the time to read - slowly. Mark Taylor wants us to slow down. I don't particularly buy his thesis but he raises matters that we should all contemplate. Those who feel they are being left behind will find his analysis helpful. Those who think they are keeping up need to understand the other view.

Here is a taster - it is here to try and get you to read his whole piece.

Though the importance of high-speed, high-volume trading is widely acknowledged, its political and social implications have not been adequately understood. The much-discussed wealth gap is, in fact, a speed gap.

In the past 50 years, two economies that operate at two different speeds have emerged. In one, wealth is created by selling labor or stuff; in the other, by trading signs that are signs of other signs. The virtual assets scale at a speed much greater than the real assets. A worker can produce only so many motorcycles, a teacher can teach only so many students, and a doctor can see only so many patients a day. In high-speed markets, by contrast, billions of dollars are won or lost in billionths of a second. In this new world, wealth begets wealth at an unprecedented rate. No matter how many new jobs are created in the real economy, the wealth gap created by the speed gap will never be closed. It will continue to widen at an ever-faster rate until there is a fundamental change in values.

The obsession with speed now borders on the absurd. In the world of high-speed trading, investors in Chicago, for example, can no longer trade on New York markets because of the additional nanoseconds required to transmit buy and sell orders over networks that can never be fast enough. Far from making place irrelevant, speed has made location more important than ever. Financial firms, following a practice known as "co-location," now build facilities for their servers located as close as possible to the servers of the markets on which they trade.

But speed has limits. As acceleration accelerates, individuals, societies, economies, and even the environment approach meltdown. We have been conned into worshiping speed by an economic system that creates endless desire where there is no need.

Many people lament the fact that young people do not read or write as much as they once did. But that is wrong—the issue is not how much they are reading and writing; indeed they are, arguably, reading and writing more than ever before. The problem is how they are reading and what they are writing. There is a growing body of evidence that people read and write differently online. Once again the crucial variable is speed. The claim that faster is always better is nowhere more questionable than when reading, writing, and thinking.

7. Energy everywhere

The world is awash in energy. Where ever you look, businesses and nations are planning to produce more. Today's news is all about the huge upsurge in fossil-fuel resources. But solar is also making huge efficiency gains.

However I was somewhat surprised to find the following graphic: there are enormous plans for more hydro, plans that could double world-wide output. Everyone want to dam rivers to store and generate energy. Never under-estimate human ingenuity or enterprise (or the occasional predisposition to be stupid).

The range of energy projects is breath-taking and hydro is no exception.

8. Just ask the Soviets

In the case of China and India, the core driver of why a more positive path is likely to continue is the simple process of urbanisation says Jim O'Neill who coined the term BRICs. Only just more than half of Chinese and a third of Indians live in cities. When people move from rural areas to cities, their economic output tends to rise sharply.

O'Neill is following a well-worn path of predicting the future from the recent past. But not everyone is buying the idea anymore. Neil Irwin surveys the changing thinking in his NY Times column.

For decades, economists have been building models to try to understand the mysteries of what drives growth. Is economic destiny shaped by culture? By government institutions? By patterns of industrialization?

But those debates have been inconclusive. Consider some of the economic success stories of the last generation — China, India, Mexico, Poland, South Korea and Turkey, to name a few. All have different cultures, government institutions and economic development strategies.

Years of work on growth theory suggest that there is no secret recipe for a developing nation to achieve prosperity. As it turns out, a simplistic reversion-to-the-mean approach explains economic growth about as well as some more complex approaches to predicting which countries’ economies are poised to boom or shrink.

This work also offers a reminder: If you just extrapolate from the recent past to predict the economic future, you are likely to be wrong. Analysts predicted that the Soviet economy would soon surpass the American economy in the 1960s, that Japan’s would do the same in the 1980s and that the United States had achieved a new era of perpetual speedy growth in the late 1990s. None of these have come to pass.

In other words, when it comes to predicting nations’ fates over the long haul, we know a lot less than we like to admit.

9. Banks unwilling to lend to SMEs; corporates do it instead

We have reported elsewhere that the ECB is contemplating buying corporate bonds. Why would they do that?

Well, actually there is a good reason, as FT Alphaville pointed out:

But we recently learned, via Nordea’s Aurelija Augulyte, of an odd peculiarity within the European financial system that could justify the rumored move, buried in a footnote of an ECB working paper that came out last April:

Improved funding conditions for large corporations can also benefit small and medium-sized enterprises indirectly, in particular through two forms of financing within the corporate sector itself: intra-sector loans and trade credits. These represented 40% of the unconsolidated debt of non-financial corporations in the euro area (which itself amounted to €13 trillion in 2011), a share similar to that of bank lending.

In other words, big companies in the euro area often act like banks to smaller companies. Since actual European banks seem either unable or unwilling to boost credit to small and medium enterprises because they are insufficiently capitalised, the ECB may be gambling that non-financial corporations can fill in the gap by borrowing ultra-cheaply in the capital markets and then lending the money onward for a modest return to the real economy. (For what it’s worth, Japanese conglomerates have a history of doing the same thing on a large scale, and it didn’t end well.)

Whether this will work is anyone’s guess, but it is certainly a creative approach to making sure that monetary stimulus is transmitted through a broken financial system.

10. Shallow money trench

"The music business is a cruel and shallow money trench, a long plastic hallway where thieves and pimps run free, and good men die like dogs. There's also a negative side." - Hunter S. Thompson

25 Comments

By trying to shore up their rich-world economies with unconventional policies like ultra-low

nominal interest rates; outright balance-sheet expansion; and aggressive, open-ended forward guidance, major central banks have dramatically widened international real interest-rate differentials and forced savers to seek out higher (and far riskier) returns for more than five years running. But that money did not just move further out on the risk spectrum from low-yielding cash equivalents to higher-yielding assets like US stocks, high-yield bonds, and MLPs. In the process of fighting naturally deflationary impulses and forcing investors to take more risk, the Federal Reserve has also forced an enormous amount of money to move out of the United States and into the emerging world. The risks have been clear to policymakers all along, but emerging markets are well outside of the Fed’s mandate. They are collateral damage, so to speak.

http://d21uq3hx4esec9.cloudfront.net/uploads/pdf/141025_TFTF2.pdf

So today due to the decades of mis-management of Greenspan, Bush and a generation or 2 of bankers we are left in an un-precidented mess. A mess so bad the certian outcome is 1930s style Great Depression mkII. The only desperate actions left are what you see now, treating the symptoms with powerful drugs with nasty side effects while the actual desease (bankers and peak oil) are un-addressed.

Who says its correct that interest rates are conventionally high?

If you look at say Keynesian economics lowering interest rates is totally standard economic response.

Yes its going to get worse.

regards

2: Distorted values. Fuelled also by Immigration (policies to simply boost numbers not target true skills shortages), International students (as govts no longer fully funding universities), uncontrolled foreign-based foreign rights to buy our property, an Auckland-centric economic policy (instead of allowing govt spending in regions thus stimulating nz economy wider), Provisional tax on small businesses penalising growth/profits on the productive enterprises, overtaxation of wage/salary earners who cannot cleverly swap profits for losses like corporations, - debt-based house equity is one of the few avenues for building savings/investment.

Many regions are flat or decreasing in property values. - However most regional home owners all get affected by the RBNZ trying to moderate Auckland house prices (which are not caused by low interest rates)

#7 is incorrect "huge upsurge in fossil-fuel resources" the resources have by and large all been discovered by the 1970s, (with most by the 1960s) so there is no increase of "in the ground oil", just the fantasy it can be recovered at a price we are prepared that we or more likely our grandchildren to pay. (that's 2 at the least, debt stretching out 50+ years plus climate change).

I find it strange that you seem to be a numbers person picking up even slight descrepancy's yet happliy post this rot.

regards

Not sure solar efficency, shale oil and natural gas from fracking was all known in the 1970's

Peak oil fears all hinge on extrapolating stagnant technolgy and extrapolating usage.

How many people were expecting us to be awash with cheap energy in 2014?

Sorry but I cant quite follow what you mean here.

Peak oil is a fact,on a finite planet the only Q is when.

Lets look at what has been used, roughly 1.2trillion barrels. Then consider the doubling time from the expotential function, even if its only 2% more per year thats a doubling of daily consumption from 85Mbpd (roughly) to 170mbpd in 35 years. If that were truely possible then the price today should be still in the <$40USD and not $80+

There would seem to be a lot of ppl saying peak oil, poo. Fracking makes peak oil a non-event, yet simple maths shows us that isnt the case it has to happen the only Q is when.

That means we have to move to something else or not consume it.

There are no other options. For the former, the trouble is the cost to the economy to do that even if its possible doesnt seem to make sense to me, ie the rich and well off 1% dont seem to care. Trouble is there is 70% of that rest who simply cannot afford to or are able to function in such a high cost environment. That measn the latter and that 1% might think they are immune to the problems of the 70%, but they are utterly wrong.

regards

I agree with everything except the assertion that the cost of moving to something else is too much of a burden on the economy. Technology doesn't just create new options for energy it also makes current technology cheaper.

Just look at how rapidly solar panels have come down in price, they will come down further still in the future as will fusion when it eventually gets off the ground. Solar already makes economic sense for households, soon we will be running our cars from the solar panels on our roof.

Fusion is still very much in it's infancy and extremely expensive but give it time and the costs will plumet and the ETA will be brought forward.

Unilever: China sales down of around (20)%

In China the impact of the sharp market slow-down has led to trade de-stocking across the distribution channels. This resulted in a decline in our underlying sales of around (20)%. http://www.unilever.com/images/ir_Q3-2014-Trading-Statement_tcm13-400605.pdf not over bought, more under sold, a failure in consumer demand, or a comment on changing suply chains/market channels?Also it seems that there is a noticable drop in coal/power use, unheard of for an economy supposedly growing at 7% per annum.

Something smells really rotten IMHO.

regards

Auction market in Sydney is cooling off

Watch the auction of the first 2 properties - watch the bidders carefully

http://media.smh.com.au/property/domain/epping-hot-surry-hills-not-5923200.html

As the man says - gotta have the right people there on the day

Those bidders are not going to be affected in any way by the level of interest rates. So Sydney property prices will keep going up regardless of the bubble or any future rate hike.

Wrong.

http://www.macrobusiness.com.au/2014/06/sydney-housings-spectacular-investor-blow-off/

Point being, it's credit fuelled + foreign investor fuelled...

The macrobusiness article is 5 months old and the data used for the graphics is probably 6 months out of date

Do you disagree that credit is being funneled in huge amounts into Sydney and Melbourne housing by investors?

I think Sydney is 9 to 1? So I find it hard to agree that its just going to go up and up.

It has also stumbled on a few occasions and that's why/when the FHB's grant was used, to pork the market back into life.

regards

Australia rates on hold til late 2015.

http://www.smh.com.au/business/markets/cba-pushes-out-rate-rise-timing-…

Aus about to use macroprudential controls in attempt to dampen property prices - Copying NZ?

Have a look at placard-waving number 5

Face looks familiar

Seen her in a couple of Barfoot's auctions on TV3

She's here, she's there, she's everywhere

It's her alright

"Soon, banks will no longer be the biggest risk to the financial system and the economy. And five years from now, many credit institutions will be smaller than they are today, having discontinued some types of business, and will better support the real economy."

I live in hope that this will eventually be the outcome here in NZ.

#4 It is all OK. Bill English implies there is no need to worry about overseas dirty money contaminating the Auckland housing market. No need for a register of overseas buyers particularly those who have no need for finance in the first place. It's all sweet as, maaaaate

And doesn't it just confirm the speculation that foreign capital (ill gotten, it seems) is behind recent house price appreciation rather than traditional credit expansion.

Of course the John Key Party will find it utterly convenient that there is no supporting data.

#4 I thought that whoever in the media described New Zealand Investor class visas "mushrooming" in the wake of Canada closing its off was entirely accurate, if only because mushrooms grow in the absence of sunlight.

#7. Energy everywhere - you 'aint seen nothing yet, Check this: http://www.lockheedmartin.com/us/products/compact-fusion.html

"Fossil" fuels will eventually go the way of whale oil and in the meantime lowering global demand and supply boosts from fracking/shale etc. means, Arabs should start booking Camel riding lessons about now.

Ergophobia

a) This is a solution apparantly looking for funding. Ask yourself if this was such a certainty and a killer product was isnt LM or the US Govn funding it? why do they need external funding?

"Professor Steven Cowley, director of the Culham Centre for Fusion Energy in Oxfordshire, says he is “nonplussed”. According to Cowley, Lockheed had said “all the usual things about how it’s going to save the world and how nice it would be if [the reactor] was small” but failed to produce any details upon which their success can be judged."

http://www.theguardian.com/environment/2014/oct/16/has-lockheed-martin-…

and,

"Lockheed is currently seeking partners in the CFR enterprise as development proceeds"

http://www.gizmag.com/lockheed-martin-compact-fusion-reactor/34277/

b) Even then ithere is the scale, time and cost to the world's economy to produce these "wonder" generators.

c) It has to be converted into a transport fuel.

Contained in a magnetic bottle....hundreds of thousands of them.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.