At face value the large fall in many components of the ANZ business survey and especially the falls in business confidence and exporters' expectations provide Governor Wheeler with the evidence he is seeking to justify more OCR cuts, with the potential this will result in a lower exchange rate.

However, it is likely that a number of respondents to the survey are somewhat mischievously ticking negative boxes to increase the odds of OCR cuts and/or a lower exchange rate.

Since 2000 the ANZ survey has been used as a political football by a number of the respondents.

It generally greatly understated near-term economic growth prospects while Labour was in power between 1999 and 2008 and has generally overstated prospects after National took office in 2008. This has greatly undermined the usefulness of the survey as an economic indicator.

I believe it is highly likely some respondents are now ticking the negative boxes in the ANZ survey to supply the "evidence" Governor Wheeler is seeking to justify OCR cuts.

Most of the economists are largely interpreting the fall in the various components of the ANZ survey at face value. Quality analysis would highlight the past "political" bias in the survey and the risk some of the respondents are currently using it to influence OCR decisions and the exchange rate.

If I am right the outlook for economic growth and interest rates will turn out to be materially different from what the ANZ survey suggests and from what the shallow analysis by some of the bank economists suggests.

The ANZ survey has a history of political bias; making it a poor economic indicator

The fall in confidence has added to the chorus of calls for OCR cuts and may convince Governor Wheeler to deliver at least one more OCR cut. The economists are largely treating the fall in business confidence at face value. I am highly suspicious the ANZ survey has gone AWOL again, meaning it should be largely ignored as an indicator of the state of the economy.

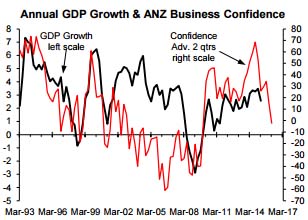

The chart above shows why the ANZ survey should be considered with considerable scepticism as an economic indicator. From 1993 to 1999 the business confidence survey was a useful barometer of nearterm prospects for annual GDP growth. Over this period the peak correlation was 0.73 with the survey leading GDP growth by two quarters. The red business confidence line has been advanced or shifted into the future by two quarters to reflect the past role as a leading indicator of GDP growth.

However, after Labour came to power in late-1999 and introduced some not so business-friendly legislation in 2000, the survey began to provide a much too negative indication of near-term GDP growth prospects. This is reflected by the massive gap opening up between the survey and GDP growth between 2001 and early-2008. Based on the survey, the economy should have headed into deep recession in 2006 but instead GDP growth improved to 3.5%. Not all business people are National supporters, but during Labour's terms in office between 1999 and 2008 a significant number of survey respondents were ticking the negative boxes as a form of political protest. Such behaviour is not uncommon with surveys that get lots of media coverage (i.e. the extensive media coverage the survey gets makes it more prone to be used and abused for "political" and other ends).

After National came to power in 2008 and implemented some business-friendly legislation, the survey improved much more than justified by the post-crisis rebound in economic growth in 2009/10 and it consistently provided an overly optimistic indication of near-term economic growth prospects from 2011 to 2014. Some of the respondents were ticking the positives boxes in the survey as a way of expressing political support for National. That is, until Governor Wheeler opened the door to business people ticking the negative boxes in the survey as a means to get lower interest rates and a lower exchange rate.

Some businesses have clearly answered the ANZ survey with an eye to which party is in power rather than based on what is happening with their business or what they expect to happen in the economy. It shouldn't therefore be unrealistic to suggest some respondents are now using the survey to try and manipulate OCR decisions. Or, more so, the governor has made it clear he is looking for signs of weaker economic growth to justify OCR cuts that are, potentially more than anything, aimed at getting the NZD down. In the context of the governor's longstanding campaign to talk the NZD down; it should be no surprise to find exporters providing him with "evidence" that a lower exchange rate is needed.

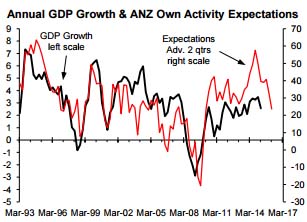

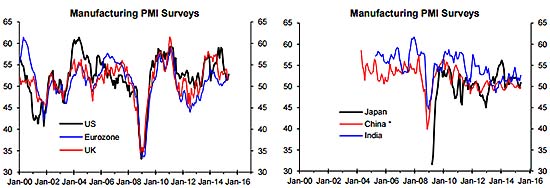

But with leading indicators of international trade for six major countries/blocks having muddled along recently rather than deteriorated significantly (two charts below) and the fall in the NZD TWI improving the international competitiveness of exporters (and local firms competing against imports) significantly, the fall in exporters' expectations is something of a puzzle. The fall in exporters' expectations also runs counter to feedback The Herald reported from some export industries about the boost they have received from the fall in the exchange rate (see the link below).

However, it makes perfect sense in the context of the invitation the governor has issued for evidence the fall in dairy product prices will have a significant negative impact on economic growth (i.e. some exporters are ticking the negative box even though the fall in dairy product prices is irrelevant to them because they hope it will help get the NZD down).

I'm not suggesting there is a grand conspiracy, but rather that some business people are acting rationally from a short-term perspective in trying to get down interest costs and the exchange rate.

In the early days of independence there was considerable scepticism at the Reserve Bank about business surveys for these reasons (i.e. the risk the business community would try and bias monetary policy decisions). I know this from my time at the Reserve Bank, including having for a brief period been a member of the Monetary Policy Committee before privatising myself.

My suggestion that the ANZ survey shouldn't be interpreted at face value is not new. In an April 2011 Raving, after there had been an excessive surge in business confidence that the bank economists largely interpreted at face value, including predicting many OCR hikes, I warned that a significant amount of the upside reflected political bias and should be overlooked.

Given the "political' behaviour of the ANZ survey since 2010, the first question the economists should ask in response to a significant change, like the fall since February 2014, is whether some of the change was due to factors other than what is happening in the economy (e.g. government policy changes or misguided RB experiments). But that would involve the bank economists being more than glorified journalists.

----------------------------------------------

*Rodney Dickens is the managing director and chief research officer of Strategic Risk Analysis Limited.

38 Comments

Thank you - someone had to say it.

every boss I had always ticked boxes other than what business was doing. Strangely enough they were also the ones who warned me off using such data sources in decision making.

What is the likely CPI June Quarter likely to come in as? 0%? Or .1%? Or minus .3 like the last on e in March.

What is the RBNZ inflation target? 1-3%. How many years now are they under shooting the target? 2 or 3 years now. What is the point of a target if you don't try and hit it?

So now we have a lobby group/movement jawboning the OCR back up?!

Exactly. It's laughable to suggest that Governor Wheeler bases his decisions on an ANZ survey.

No more so than a contrived domestic price consumption index which patently excludes a risk component associated with forfeiting as much to fund those whom cannot afford that which they covet today, but may in an uncertain future.

True, but those are the rules under which the Governor is required to follow over the "medium term".

However, the "medium term" is turning out to be a long period.

When will the inflation target be met next? 2018? Or never?

Rodney is obviously not involved in retail. It is diabolical and there is no end in sight to the pain. And the business I have an interest in is not in competition with the internet. Retailers will be looking to close down when their leases come up for renewal. We need interest rate and rent reductions to survive otherwise people will be laid off.

Lower interest rates is what is causing your problem, Gordon! Think about it. The banks etc are still making their same old margin on lending (or more!) - their profit, and yet those with savings have been treated to a fall in disposable income that has been transferred to the indebted. Those with debt would still have spent pretty much the same in your shop ( as most people can service their debts) but those with interest income ( more and more each day as our populous age) have less and less to spend in your shop. Lower interest rates has not gone into the shops ( people may have reduced their debt or, worse, taken on more!) but it has gone to the banks, and two asset markets - property and shares. And as rates fall, so will spending in your shop.....Counterintuitive, I know, but that's what's happened all over the World. Huge amounts of spending power has been taken out of the hands of the spenders.....

On that twisted economic logic, let's crank the OCR up to 5.0 and watch all the oldies spend up large.

One of the added problems to the RBNZ having run a very tight monetary policy for years is that this has been combined with a tight/capped Govt spending - ie "good" Govt spending such as Hospitals, schools, Universities etc - these have had a closely capped spending lid on.

In the middle of a global recession, you need loosening of govt spending and loosening of monetary policy. Yes, it has risks and mis allocated spending but Austerity is not a good option either.

Now that we have embraced lower interest rates - yes, we have trapped ourselves, like everyone else! But we have a choice, or the RBNZ does anyway; keep going further down what I believe is the wrong road - lower interest rates further - or cease that policy. Borrowers, by and large, borrow what they can afford to service and apply it ( How much do I have + how much can I borrow = What can I buy!). Let's say at 10% a mortgage of X is possible. How much will that same person borrow at 5%? Generally the answer is 2X ! The repayment; the debt servicing remains constant. The 'saving' does not flow to the wider economy. It goes into recapitalising the banks balance sheet ( that's why their margin remains constant or rises!). At 10% savers spend X of their disposable income, but at 5% they spend 1/2 X. Worse. As they probably need more that 1/2 X to live from, they start spending their capital down. So when rates do rise, they won't have much left to invest and spend at 10% when they do go up. It's all downhill with lower and lower interest rates....

What you believe you cannot prove though in fact the evidence points the other way. Conventionally a) lowering the OCR helps fight against a recession/downturn. b) raising in such circumstances has in recent history proved the very last thing to do, c) you provide a "model" that models how a single household may perform/act, in specific circumstances that may or may not apply, yet an economy is nothing like a household.

An economy may not be like a household, yet it is households! Lots of them , in fact. And many companies and businesses. It's easy to embrace the 'long term view' that a Country has a different set of rules because it will be here for a thousand years, and so economic imbalances can be spread out over time. But are they? How far into the future were, say,Czechoslovakia's economic issues spread in 1990? Not far, as the country 'disappeared' very soon after. Or West Germany etc etc. What is left of those countries is the people, the households and business. The problem with 'a country isn't a household' belief is that it relies very much on "in the bad times, spend and in the good times, save" philosophy. But that never happens, does it! Every country spends in the bad times, and spend in the good times. Rather, it's borrow in the bad times, and borrow even more in the good times. That....is why we are where we are today. And if the only answer anyone can think of is 'more debt' and 'cheaper' debt, then we aren't getting out of this lot anytime soon....if at all!

It does actually a) Dr Cullen ran surpluses paid down our debt in the good times, b) we have had to meet our obligation in the bad times by taking on debt. c) Indeed Dr Cullen tried to save in the good times for the problems caused by too many BBs later on trying to avoid a bad time.

In terms of interest rates being the problem, you seem to neglect to mention the tax cuts given as a reward for voting for National, where did that extra $s go? into housing it seems.

"That....is why we are where we are today." actually no we are were we are today due to too expensive energy. "borrow" sure lets go right wing dogma and set up the Govn finances with fundamentally too little income and refuse to raise taxes thus forcing borrowing.

"if at all!" indeed its a no. Oil will decline in output per day within a few years and then head to zero as it gets to all used up by 2050.

Think about it? How about you provide some evidence? So the "conventional" models, evidence and data all point to lowering the OCR as a conventional way to stimulate the economy but you dont want that. Savers v indebted, again you treat these as the only part of the economy, yet it is SMEs and workers beolwo 45 years of age that drive an economy and provide jobs. In terms of gone into property and shares, this is indeed a mis-alocation of money driven by greed nothing more. So your answer to that greed is kill the rest of the economy off as a side effect to curing ppls greed? This has not worked elsewhere so why would NZ be different?

And yet It's the savers that will be called upon, not the indebted, to bail out the actions of the many profligate workers and SMEs

Greek Banks Considering 30% Haircut On Deposits Over €8,000: FT. Read more

Time to force the proceeds of collateralised loans directly to the depositors in the event of default.

The Greek farce has been unfolding for 5 years. Anyone with a few smarts and some cash would be long gone. A 30% haircut of zero is zero.

I'm not the fastest gun in the gun cabinet, but I would have had my loose change out of there at least 2 years ago. Even blind Freddy could see this coming. After 3 years of spinning the wheels nothing changed. They were never going to change. And still don't want to.

Listen to this Duncan Garner interview about swimming pools at the 3 minute mark and you'll get the drift, then he gets into retirement at 51 on $80,000 for the rest of your life. You can see why they don't want to change

http://www.radiolive.co.nz/How-the-financial-crisis-in-Greece-affects-y…

Listen to this Duncan Garner interview about swimming pools at the 3 minute mark and you'll get the drift, then he gets into retirement at 51 on $80,000 for the rest of your life. You can see why they don't want to change

http://www.radiolive.co.nz/How-the-financial-crisis-in-Greece-affects-yo...

"The above appears to be little more than part an anti-Greek, smear campaign designed to foster moral outrage of the "hard working" Western middle classes in order to garner endorsement for the reforms the Troika seeks to impose on the Greek populace.

The true picture is rather different.

"Previous governments have tackled the problem. Pensions have been cut by an average of 27 percent between 2010-2014 and by 50 percent for the highest earners. The average retirement age was raised by two years in 2013 and Greece has said it is willing to curb early retirement benefits further.

On average Greek men now retire at 63 and women at 59, according to government data. In Germany, the average retirement age for those receiving an old age pension in 2014 was 64 years. But that figure goes down to 61.3 years once those taking early retirement on health grounds is taken into account, according to 2013 data. ($1 = 0.8874 euros) (Additional reporting by Alkis Konstantinidis, Paul Taylor, Holger Hansen, Leigh Thomas and Giselda Vagnoni; writing by Matthias Williams; editing by David Stamp)"

If you want to look at it that simply, OK. Oh and its the saved btw not the savers. There are two sides actually, the depositors and the investors/specualtors/parasites in the finance industry. The former I have some sympathy for, the latter, none.

Simple really the saved were the indebted at one stage yet they continued to consume, expand, waste and breed so how much sympathy do they deserve for a mess of their own making?

how much allocation has there been into residential property because of cheap credit. looking at the latest mortgage stats you would have to admit it has become the elephant in the room.

how much of it is negatively geared with people tipping in.

that is money taken away from consumer spending and used to pay debt.

we have now got to a situation where the lines between good and bad debt is muddled and all debt for assets (houses) is seen as good and SAFE debt.

meanwhile those that save or positively gear there assets are being punished for being conservative.

I think one of the biggest problems for retail are high housing costs, straight and simple. Given housing costs are such a significant proportion of household costs (usually), big increases obviously can significantly reduce disposable income - and the likes of retail, hospitality often suffer more than most.

Lowering interest rates is likely to pump up house prices even further so it could possibly cancel out or even outweigh any benefits offered by lowered rates. Most of these issues are never simple.

Especially rent. What I am seeing is empty shops on malls, walkways and corners that I would have considered prime sites, yet they stand empty for months.

Also is very hard in the Commercial landlording sector at the moment. Businesses often treat the landlord as the first one to not pay when things get tough and most commercial tenantsand landlords are heavily leveraged.

But you can't have flourishing retail without customers able to pay - that's the weakness of our current system. Where are the consumers supposed to get the funding from to keep the system afloat?

The shop is in a provincial capital where housing costs are much cheaper than Aucklands however it is reliant on farmers and oil/ gas workers spending. Neither are doing that and unemployment even amongst highly paid oil/gas workers is increasing. It's actually worse than the gfc era. We need lower costs just like the farmers.

Gordon:

Four years ago you were here, expressing concern about retail when Allan Bollard cut rates down to 2.5%, then when the Dairy boom appeared the last few years you went silent, then Wheeler increased rates 4 times to 3.5%, and still you were silent. Now Wheeler has started cutting rates while at the same time you acknowledge you are dependent on farming confidence and income. Now here you are again seeking further and faster cuts. So what is it you really need? Are all your farming customers those that are seriously in debt that further rate cuts will support them. Or is it better dairy prices. But hang about, the much weaker NZD is cushioning the drop in GDT prices

how about supporting the rest of the country over Auckland. for years we have seen business and government departments relocate how about trying to reverse that.

we are so Auckland focus now, Tauranga has the second biggest container port in the country but it is mostly serviced from Auckland, why has industry not moved to be nearby

have a look at growth of centres outside of the big four and it is more farmer focused than ever before.

tourism is filling some gaps with the lower dollar that will help.

lower interest rates wont make a lot of difference to consumer spending, it will go to either servicing debt or enable more debt to be carried

Retail has been terrible literally since 1/1/2009. We have not paid tax for years which is not great. I am propping it up with loans. This year is the worst period on record and it will get worse as farmers get deeper into the red. The reality is you need to protect yourself from landlords guarantees and there are 20 staff to consider. There is no rockstar economy in retail, there never was.

Sounds like it's well and truly time to cut your losses Gordon.

If people like Gordon cut their losses, then what happens to all his staff. That just removes all their families from the economic plus side. Unless the business was fundamentally flawed, which given the time he's been around I doubt that it's fundamentally flawed, then needing it to close would be the exact _recession_ process we need to be avoiding.

Businesses failing during a revaluation is one thing - or if they're not competitive because they won't stay on top of developments (in the computer sector they used to pay 150+k salaries and huge bonus - when IT went to the bitty boxes and desktop those salaries had to go because revenue wasn't there). But is Gordon's business model out of step? Are his products obsolete? or his wastage/leakage out of line with industry norms?

If none of those are the case, then what we are watching via the internet's far reaching vision, is recession in action. He loses customers, staff get released. no new hires. fewer jobs. reduction in customers. In the past double income families was the answer, or QE-like housing booms injecting money into the system, or "interest-free 3 - 7 year hire purchases" for box dumpers just to get sales.

If the customers don't have the funds, even if there is demand for the product, what can he do?

When I was an IT startup (and also when my friend opened his flower shop) we paid our people better than ourselves and supported them well. and we went into debt doing so. both of us lost our businesses, my friend lost his house. I don't know Gordon's debt recovery or stock turnover rate, but I'd love to hear alternatives: either for the business model (the TAB got in side businesses but it never really helped the bottom line) or to increase customer liquidity outside debt (which carries interest).

" or his wastage/leakage out of line with industry norms?"

I mention this one because from what I knew of Postie Plus I'm not in the slightest bit surprised they had to reorganise. One would have to wonder about what their accountants/CFO was seeing on the balance sheet ratios. (re: inventory movement and advertising effectiveness)

However it is flawed if its relying on a BAU / grow for ever model. Which is what I have been trying to point out for years. "If none of those are the case" isnt this the case? isnt this what is causing the OCR to be dropped?

"If the customers don't have the funds" When the non-tradeables are going up at 5% ish and ppl have no wage increases or say at 1% or something then there has to be something giving, that is retail.

"or "interest-free 3 - 7 year hire purchases" for box dumpers just to get sales" this has been the strategy for retail, this is the one point of advantage they have over Internet businesses access to the so called "interest free HP" The hd of my laptop just died so I had a look at a new laptop on say 1 year interest free except the setup fee is $50 and the yearly maintenance fee is another $50 so $100 plus in "costs" is 8% per annum so hardly "interest free". Anyway TM is my friend so lappy is now going again cheaply, not too bad for 7 years old, except its on its 3rd battery, 3rd PSU and now second HD, LOL.

Mike M you obviously are not self employed. I guarantee a rental of $215000.00 per annum. I cannot walk away.

Yes I am self employed. I've also employed people in the past but I know when it's time to walk away if I'm burning a large hole in my pocket.

But hang about, the much weaker NZD is cushioning the drop in GDT prices

Only cushioning it if the processors haven't locked in at say, 80c/USD. The falling dollar could also be costing us dearly depending on the currency hedging contracts in play.

Casual - rumour has it that Fonterra is relatively short-term hedged, so hopefully that's correct - those that unfortunately will also be positioned that way are importers who are typically 3-6mths hedged if that. This is a pretty substantial fall in the NZD, and NZ inflation is very susceptible to its moves - Wheeler will get what he wants, an early bottom in inflation and a move back towards more comfortable levels that will limit the extent of interest rates falls - we will get three more cuts I think (of which more than two are already priced in to fixed rates) then it will settle there for a while. That is, until the Fed moves, whether its the current expectation of Sep or early next year, but that will be the end of the really cheap fixed rates. Many will miss that however as they get complacent about a stable period of floating rates before the next eventual move higher, probably late next year but many months after the fixed rates are gone.

Sorry to hear it. Again shows how it's not simple because in your situation housing costs are unlikely to be fueled too much by lower interest rates

mike so you would take the risk with the landlord and get rid of 20 employees.

Out in the real world the one that is beyond the keyboard......the world in which people attach miking cups, fell tress, raise lambs, shear wool and other fibres, make widgets, host tourists etc........it is a world that is now completely dictated to buy those sitting at the keyboards.......and Rodney thinks we are ticking negative boxes for some other purpose like lowering interest rates!!

The whole of the productive economy, you know the one that is Agriculture and Business is swamped by State morons....the productive economy not only has its debt from taking on the risk of buying or building a business but it is selfishly lumbered with being responsible for all Government and housing debt......and Rodney wonders why there is pessimism!!! It's a ratio thing Rodney to many people grazing off the same paddock!!

If anyone visits this site they have read all the tripe from many commentators who post, who are responding to what I can often only call absolute drivel in most opinion pieces.......people who are not at the coal face do not have a clue and the worse thing is they pretend to know everything that is going on!! Too many NZ'ers have an anti agriculture sentiment...they seem to like biting the hand that feeds the nation.....but that is parasites for you!! The crap is not always directed at farmers it does get shared around, finger pointing at builders, forestry and most other business from time to time.

GDP doesn't measure how well business is performing so looking at increases is only something someone behind a keyboard would actually do....Increasing GDP does tell business how much the Government is screwing them over by because with every increase in GDP there is a bureaucracy creating the increase....

AS you are an ex RBNZ banker Rodney then please inform people as to how money comes into existence!!! Why not be really open and honest and tell people that all those mortgages and debts they have taken on are not backed by other people's money!! Now tell those people who have deposits sitting in the bank why the RBNZ won't allow those deposit holders to be given any type of security!?! Tell people that when they take out their mortgage that it is themselves who have created the security over the property.......the RBNZ's role is to take a cut......make a profit and pay that profit back to the Crown!!!

Business confidence is down for a reason....and I think it is a load of bollocks that you are portraying responders as trying to manipulate the OCR.....Disregarding the real agenda of the RBNZ and sticking to the commonly portrayed model of its existence....the fact is the RBNZ has made a complete stuff up and that is lightly worded on my behalf......the raised the OCR when they should have dropped it and the interest extorted is dead money so the SME business community moved into negative territory and has to now make up from that negative point....why you people don't learn some maths astounds me!!

Then there are the other stupid Government empowered leeches who have significantly increased costs across the board.....there is not a month that goes past that business is not shelling out money to some bureaucratic empire.......business is stuck in compliance from every direction and National have not improved this situation in fact they have in most situations made it worse.

National have completely screwed up by insisting on taking some of the left vote with them......they have done nothing for business other than entrap it with more legislative requirements which are highly dubious.....People in the SME's are under a huge amount of pressure.......an educated guess is that there will be some bad debt arise in farming and building in the not to near future!!!

Personally I have not felt this negative in 30 years of business......I don't see any light at the end of this tunnel for the NZ economy......so-called social good policies are going to destruct the whole of the productive sector.....bureaucrats writing reports and manipulating policy and legislation on the benefits of their existence is like prisoners telling the jail how the prison will be run!!

The big corporates are squeezing the SME's via the bureaucrats........they former pay stuff all taxes, and the latter are funded predominately by the efforts of the SME's.....if this BS continues then the framework of the NZ economy is completely destructed.....cos there is no one riding into town to the rescue!!

Better late than never and well done Rodney, yr on the right track. The ANZ (as earlier pointed out) has more incentive to cook the numbers due to its ending up with the Rural Bank accounts, but the trail of dirt in this managed "downturn", designed to crash the NZD, leads on...... Happy hunting.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.