By Oyvinn Rimer*

The economic transmission mechanism does not fit classical economic models. Therefore, it is easy to default to a position of thinking it is too hard to analyse and conclude something must be badly wrong.

Since the Chinese share-market started its dramatic fall in June 2015, countless negative headlines have suggested that the Chinese dream is over, implying a global recession is imminent.

Undoubtedly, China faces some very significant challenges. These include high debt-levels, systematic over-investment in underperforming assets and slowing old economy sectors, such as real-estate investment and manufacturing. These will take time to address and there is likely to be multiple periods of market volatility prompted by fear around Chinese headlines and policy actions.

However, it is important to remember the policy agenda that was articulated at the Third Plenary Session in Beijing in October 2013. That agenda serves as a long-term anchor and provides a framework for thinking about China’s changing economic and social landscape.

The aim of these reforms is to transition towards a more sustainable economy with an increased focus on environmental, social and governance aspects. This is a big change in the political rhetoric and deviates from the traditional relentless push for ever-higher GDP growth.

There are obvious trade-offs between improved social and environmental policies and that of investment-led economic growth. The Chinese Government has started implementing many of the announced policies and is observing the impacts as they develop.

It is only natural that there are unintended consequences from policy implementation; especially given the centrally planned model that has ruled for decades. Any relaxation of controls require piecemeal execution to assess the effects of changes; and growth rates across the economy have started changing in response to policy-implementation and fundamental economic signals.

It is no surprise that it is the old economy that has taken the most direct hit as investments into these industries have been scaled back and increased environmental focus has challenged heavy industry to reduce emissions. This is negatively influencing Australian exports of raw materials and it is not obvious that there is a quick recovery for iron ore and coal demand on the horizon.

Although the manufacturing side of the economy is still the largest, there are encouraging signs of stability and growth across the consumer services side of the economy. Retail sales keep printing solid growth (+10.5 per cent Year on Year in August) and sentiment in the non-manufacturing (services) sector looks buoyant, with the latest PMI number printing 53.4 (a number above 50 suggests positive growth). This is positive because it represents the new economy and is a key focus-area for policy-makers.

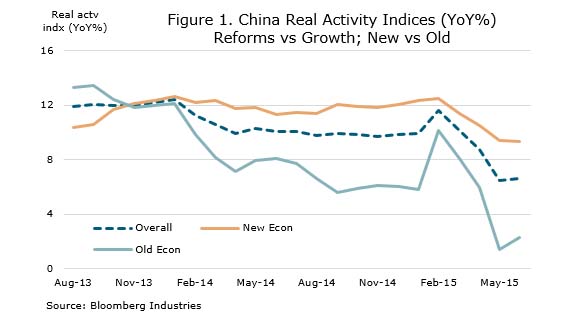

Figure 1 illustrates how the old economy has been under pressure for some time and has declined consistently since the reform agenda of 2013.

However, the new economy performance, which includes indicators such as generation of clean energy, vehicle exports, medicine consumption and production of communication devices and computers, is much stronger.

On average, the two sub-components suggest slower economic growth overall, but the stronger growth in the new economy is consistent with policy-objectives of rebalancing towards more productive sectors that are focused on services and consumption.

Consumption, coupled with improved conditions for the growing middle-class should be positive for New Zealand.

Unlike Australia, New Zealand’s main exports to China are agricultural goods and tourism. Both of which should benefit from better social safety-nets in China, which are likely to improve consumer confidence and increase spending on overseas travel and consumption of New Zealand-produced proteins.

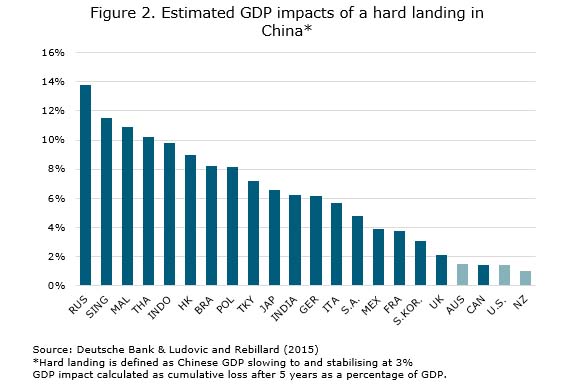

However, we live in an uncertain world. To aid our understanding of possible outcomes, it is important to consider the scenario of a hard landing in China (e.g. Chinese GDP growth falls to and stabilises at 3% p.a. instead of the expectation of 6%-7%). Although a hard landing is not a base-case forecast, the impacts could be significant both within China and the wider region.

Researchers estimate that the cumulative impact on New Zealand GDP from this scenario in China is only -0.9% of GDP. This is largely explained by New Zealand’s flexible exchange rate, which would depreciate sharply in response to a Chinese hard landing, therefore providing a buffer for the NZ economy. Food consumption is also expected to continue to grow despite headwinds across industrial sectors in China.

Figure 2 shows the estimated GDP impacts of a hard landing in China across a range of countries. New Zealand stacks up surprisingly well. Australia’s flexible exchange rate also works to absorb most of the impact of a slowing China. It is estimated that energy exporting countries and those with currencies pegged to the U.S. dollar experience the largest negative impacts.

In summary, it should be acknowledged that Chinese economic headlines and unconventional policy-responses provide market risks that are likely to influence investor sentiment.

As China transitions from investment-led growth towards services, there are likely to be unintended consequences that re-ignite market jitters.

However, over the longer-term, the transition to consumption from infrastructure and exporting is the key for New Zealand and should be positive, although it is fair to expect a bit of spilt milk between lip and cup during the transition.

*Oyvinn Rimer is a Director & Research Analyst at Harbour Asset Management. This column does not constitute advice to any person. www.harbourasset.co.nz/disclaimer/

10 Comments

Nice post - super important to think about the sectors NZ is exposed to when thinking about the outlook for China and where the risks reside.

Regarding the graph showing estimated impacts on GDP, I would love to know how they have estimated this. The impacts on the Anglo-Saxon nationals look relatively benign, which has to be based on the assumption of our "superior" monetary mechanism whereby the currency adjust to adverse economic conditions. However, look at the impacts on ASEAN nations, Japan, India, and key European nations. I would suggest that the impacts could me much larger than what we could imagine as the whole world suffers.

Completely agree. Australia will be lucky to avoid a recession even in the soft landing scenario let alone the hard landing.

There's many a slip 'twixt the cup and the lip"

more so, as of those things that seem certain are often only determined seemed by the view frame applied, as opposed to an appreciation of the human condition for example.

unconventional policy-responses

an example of stroke of a pen stuff, herewithin..

http://www.newsweek.com/chinese-communist-party-bans-golf-club-membersh…

The new rules announced earlier this month by the Communist Party, part of an ongoing anti-corruption drive by President Xi Jinping, are intended to be a “moral ethical code that members must abide by,” according to China’s Xinhua News Agency . Members are barred from "obtaining, holding or using membership cards for gyms, clubs, golf clubs, or various other types of consumer cards, or entering private clubs.” Chinese authorities banned the construction of new golf courses in 2004, but they have continued to be built in the decade since, the AFP reports .

life imitating art, golfs not very popular round here...

https://www.youtube.com/watch?v=uwAOc4g3K-g

China and the rest of the world have just come through a mind-pending credit binge which took global debt from $40 trillion in 1994 to $225 trillion at present. China was in the forefront of that binge, sporting a 56X gain in outstanding credit during the same two decade period (from $500 billion in 1995 to $28 trillion at present).

http://davidstockmanscontracorner.com/the-central-bankers-death-wish/

dreams and what others dream, here are others dreaming of middle kingdom and President 11 (those crazy Britts) safe as nuclear power stations...

https://www.youtube.com/watch?v=hlCMI-JEtHA

see 2:00 onward

and for RWC wonks, something Scottish from 17:10

and so, a great example of how home bias yields a flawed analysis:

http://brontecapital.blogspot.com.au/2015/09/job-interview-questions-si…

Take a moment to work your way thru the blog comments for in China descriptions of retail and SME web commerce & logistics.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.