Here's my edition of Top 10 links from around the Internet today.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz.

See all previous Top 10s here.

1. It's the stories.

Behavioural economists - of which Robert Shiller is one - suspect market movements and 'drives' are more about the way we respond to the swirling narratives about economic prospects than the core data. They are on to something because, as we see even in our comment stream on this website, many start with 'conclusions' which they defend, looking for 'data' to support those positions. It appears whole markets may be motivated by such thinking.

Stories get momentum, and drive thinking and sentiment, quickly powering 'market forces'. It often seems backward to me, but it is what it is.

Shiller penned a useful analysis recently in the NY Times, here, although to be fair his points are different to my take-aways. But if he is right, it upends what most think drives markets. And trending narratives on social media are becoming even more important to how markets move. But, actually, it may just be a return of some deep human drives.

Most economists generally do not refer to such popular stories or assess their emotional appeal. The same is true for most historians, but the Yale historian Ramsay MacMullen is something of an exception. In his remarkable 2003 book, “Feelings in History: Ancient and Modern” , he wrote: “History is feeling. It is feelings that make us do what we do; and feelings can in fact be read. But the reading of them requires writers and readers to join their minds in ways that have long been out of fashion among students of history.”

Professor MacMullen tries to convey to the reader the feelings people had long ago when they were inspired or dejected. He says he believes this will help us understand history at a deeper level. One emotional story loaded with moral value leads to another, in his retelling.

2. Assets and debt.

We have a pre-occupation with the amount of debt in society. (And I think that is a good thing.) Typically we assess debt levels at the national level as a function of GDP. But debt is a 'stock' whereas GDP is a 'flow'. That relationship is a crude but useful way to assess sustainability of the debt levels - the ability of an economy to service the debt. Useful perhaps at a very senior level, but there are many much better ways to assess serviceability.

But if we must talk about the sustainability of debt levels, we should start by assessing them against the underlying assets that support this debt.

Here is the big picture for New Zealand households:

| Assets | Debt | ||||

| NZ$ bln | 2015 | 2014 | 2015 | 2014 | |

| $ | $ | $ | $ | ||

| Households | 1,105.4 | 964.0 | 160.3 | 150.8 | |

| - houses | 862.3 | 745.0 | 130.2 | 121.8 | |

| - bank accounts | 151.8 | 136.6 | |||

| - KiwiSaver and Funds | 91.3 | 82.4 | |||

| - consumer debt | 15.3 | 14.7 | |||

| - student loans | 14.8 | 14.3 | |||

Elsewhere I have noted that you can see that total 2015 household debt of $160.3 bln is almost 'covered' by total household bank accounts of $151.8 bln. Of course, they are not held by the same households (they never are) but the overall 'system' has far more in 'assets' than 'debt' - even if you exclude all the residential real estate.

3. Unemployment and wages.

Plenty of observers are sceptical of the December unemployment data and its sudden improvement in the jobless rate. Most eyebrows have been raised by the slightly lower participation rate (down to 68.4% from 69.4% for the same quarter a year ago). But lost are two facts: 68.4% is above normal for the past decade and far above any time earlier than that. It is the last few quarters that have been abnormal. And every other Western country would give its eye-teeth for a participation rate of 68.4%. It is very high by OECD standards.

Last year, the Aussie stats agency earned a black-eye for errors in their household labour force survey. But I doubt we are facing the same credibility issue here.

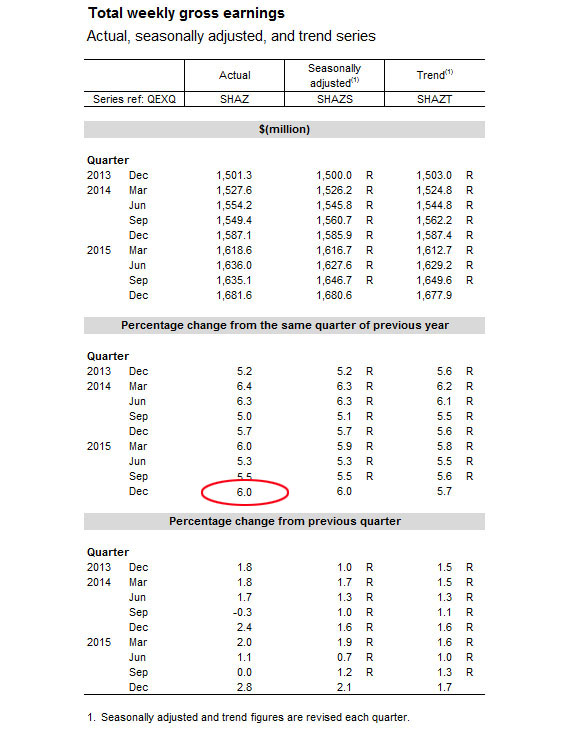

Just as important, and to my mind mis-reported, is the related payroll data. The standard narrative is that we have low unemployment but with low wage growth. Wage growth is lowish but far higher than headline inflation: real wages are rising. And actually, I think by focusing on the seasonally adjusted measures Stats NZ uses, we are overlooking the much higher 'actual' pay rises that are really occurring. Seasonal adjustment is useful, but only when the past patterns reflect the current trends.

Anyway, my point is that 'actual' wages rose +6.0% year on year, as revealed in Table 5 in Stats NZ data release. By anyone's measure, these are healthy rises.

4. Rooftop solar wars.

Rooftop solar adoption has so far depended on subsidies and tax incentives to justify its adoption. In countries that have offered incentives that upend normal market forces, adoption has been high. Although when those incentives are removed, adoption collapses.

One especially problematic area is regulation requiring transmission utilities to buy back electricity fed back into the grid from household rooftop systems. In New Zealand it is a mere token, and that is holding back adoption.

Remarkably, in California that buy-rate is regulated to be the same as the retail sell-rate and that gives a huge incentive for roof-top adoption. The California regulator is certainly not in the pockets of the utility industry when it forces them to do that. But there is real push-back, and some of it is existential for the utilities. Elon Musk's Tesla batteries will allow millions of homes to potentially go off-grid. And Musk's solar business (Solar City) is pushing hard for the retention of the buy-back premium price. But any utility required to pay retail at the same time their clients stop buying any product is hardly a sustainable situation. This from Bloomberg:

California regulators are set to decide how much rooftop solar customers can get for selling their excess clean energy in a pivotal vote for the largest U.S. solar market.

The California Public Utilities Commission will consider a proposal Thursday that would continue a policy called net metering, which requires utilities to pay rooftop solar customers the full retail rate for electricity they put onto the grid. The solar industry has been largely supportive of the proposed measure while the state’s investor-owned utilities have called it unfair and say it means people who don’t have solar systems are subsidising those who do.

5. A game-changer.

This item is not really the usual fare for a Top 10, but is interesting all the same. A Chinese research institute has developed a low cost and relatively low tech way of desalinising sea water. It uses the waste heat from a diesel electricity generator and some novel use of a low pressure tank. Seems to have wide drinking-water potential. More from the SMH:

But the Guangzhou team used a different approach. They reduced the seawater to tiny droplets at the top of a chamber filled with heat-exchanging rods. The rods were warmed by water from the diesel generator’s cooling system. Upon touching the rods, the droplets evaporated, and the resulting vapour was blown into a condenser, where it became fresh water.

One of the boons of the system is that it only requires relatively low heat, which can be produced easily by the generator, the team said. It is also compact, making it suitable for transport to local islands.

Moreover, lab tests have shown that the fresh water which is produced fully meets national safety standards and is immediately drinkable, the team added.

6. Falling interest rates exacerbates inequality.

According to Antonio Foglia, a London-based Italian and Swiss economist, the problem with the current notions of inequality (Piketty's especially) is that the crisis is seen in terms of 'assets' whose values have been suddenly spruiked higher by low interest rates. He is particularly scathing of analysis the ends up showing that the Italian's are much more wealthy and (oddly) equal than the Germans. This can be completely explained by higher housing ownership rates in Italy than Germany, and the fact that the sudden fall in interest rates has benefited the home-owning Italians much more than the renting Germans. Such data actually tells us nothing realistic about Germans and Italians. His article is entitled "The invention of inequality".

It is driving perverse discussions about equality and even more perverse potential remedies, he says. And the urban myths created and fuelled are generating politicians keen to capitalise.

His argument is in an article on Project Syndicate:

A 2013 study of household finances in the eurozone, conducted by the European Central Bank, showed that in 2010 – the last year in Piketty’s research – the average Italian household was 41% richer than the average German household. Moreover, whereas the difference between mean and median household wealth is 59% in Italy, it is a whopping 282% in Germany.

This difference can be explained largely by the fact that 59% of households in Italy own homes, compared to only 26% in Germany. A larger share of Italians has thus benefited more from a larger drop in interest rates.

This example highlights how household investment decisions shape wealth outcomes. Complicating wealth measurements further is the fact that, as Martin Feldstein recently pointed out, for the vast majority of households, a large proportion of wealth is in the form of unaccounted future social benefits.

Then there are the numerous factors affecting incomes, such as demand for particular skills. For those whose skills are not in demand, the availability of skills upgrading or training opportunities will have a significant impact on income prospects.

7. Fear and awe - 'violence', then progress.

This is how the heavy-hitters at Davos 2016 are looking at the impact tech change will have on societies: it will hurt, but you will like it in the end. Larry Hatheway thinks regulators and financial markets don't pay sufficient attention to human ingenuity.

Technological innovation has long triggered diametrically opposed reactions: awe of new possibilities for some; for others, fear of disruptive change. But most of us don’t even realize what is happening. We take change for granted.

Human ingenuity is far too little recognized or appreciated, particularly in financial markets. Investors obsess about more pedestrian concerns: fears about a hard landing in China, the repercussions of falling oil prices, and the risk that some shock could tip a fragile world economy into renewed recession or deflation.

Obviously, worries about global demand conditions are not unfounded – surely the last thing the world economy needs now is renewed stress. Yet, for all our angst about excessive debt and policy inadequacy, nothing is as important as human ingenuity for delivering improved living standards and investment opportunities. Indeed, the advent of new technologies holds out the promise of a Fourth Industrial Revolution.

...

Ingenuity it is. But, to paraphrase Joseph Schumpeter, it is also destructive. In today’s parlance, we speak of “disruptive technologies.” But no-one should be gulled by jargon: New ways of producing things often kill off old industries and jobs before the full benefits of the successor mode of production are realized. A certain degree of violence inevitably accompanies human progress.

8. Incentives matter

Back in eighteenth century Britain, Scotland was a backwater, England the master. Same with their universities. But then something quite remarkable happened: Scottish universities became world-class rivalling (even besting by some accounts) the best the English had to offer.

What happened was pure economics - the Scots had their students pay their professors directly, essentially by-passing the central university authorities. Quite quickly, standards shot up.

Might be worth looking at again. Certainly NZ university vice-chancellors would hate it, but they are still presiding over a tertiary system that lags way down the achievement and quality stakes on a world-wide benchmark basis.

There are of course reasons why it could be very problematic to unbundle tuition and let students pay their professors directly. Disturbing evidence has recently pointed to the patent unfairness and sexism of student evaluations of their professors. Many an academic has bemoaned the growing “customer” mentality of their students, and with good reason: It can lead to grade inflation and a subsequent lowering of standards.

But as Smith would surely have appreciated, the right incentives could bring 18-year-olds to seek out the highest-quality teachers rather than the most forgiving graders. That’s how it worked in Scotland in the 18th century, where there was a simple way of dealing with the problem that the best professors were not always the easiest fellows: rigorous, frequent, and comprehensive oral and essay examinations, which were administered in lieu of evaluations in individual courses. Students were allowed to select which university services and which university teachers they would pay for, but in the end if they could not pass a university-wide exam, their choice to take the 18th-century equivalent of Rocks for Jocks would have been swiftly punished.

Smith himself was by all accounts the professor whom many students dread to meet on the first day of class: Disheveled and uncharismatic, he wore his frequent absent-mindedness heavily, and the discrepancies in his students’ surviving notes may point to poor delivery. Nevertheless, when he quit his academic post halfway through the year to take up a prestigious tutoring position to the Duke of Buccleuch, his students declined his offer to refund their fees. They had, they said, already learned enough to justify paying for the whole course.

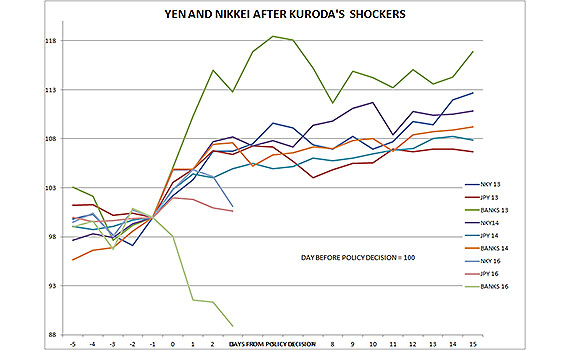

9. Do low or negative interest rates eventually kill banks?

Some people are clearly worried about that possibility. Since the Bank of Japan's adoption of negative rates, markets have reacted with horror over the prospects for Japanese commercial banks. This is in sharp contrast to how they reacted previously over Japanese QE decisions. This is what one observer said:

Kuroda and the rest of the NIRPsters ought to fire their screenwriters, because markets are not playing out according to the script. Although the Nikkei and USD/JPY are still higher than they were before last Friday's BOJ announcement, the same cannot be said for Japanese banks, which have tumbled further since Macro Man highlighted them on Monday. It's quite a contrast, really: banks were the star performer after QQE 1, generated middle-of-the-pack gains after QQE2, and are a steaming pile of dog dirt this time around. Although perhaps not conclusive, it is nevertheless persuasive evidence of how the market views the impact of negative rates.

10. Today's quote.

"Establishing a 0.03% Wall Street speculation fee, similar to what we had from 1914-1966, would dampen the dangerous level of speculation and gambling on Wall Street, encourage the financial sector to invest in the productive economy and reduce the deficit by more than US$350 billion over 10 years." - Bernie Sanders.

And for those of you who only come here on Fridays to find the latest Clarke & Dawe, they have not yet started up again in 2016. They obviously get paid too much by the ABC to need to get back to work. But they are thinking, and tinkering, here.

18 Comments

#1 David this chap has nailed it. As a Quality specialist I have long advocated, to many others frustration, that everyone's first reaction is always an emotional one, and not every one can get past their emotional response to apply reason and logic to analyse the situation or their reaction. A very good example here was when Air NZ almost went down the gurgler, the share price fell well below even what just the Christchurch engineering base was worth on it's own. I was doing a financial paper at Massey at the time, and had a fairly robust discussion with my lecturer about the taught perspective that the market is "efficient" being the collective opinion of all the inputs, whereas I maintained that while there is an element of rationality, overall the market is largely an emotional response to what is happening in the world.

#9 during QQE the banks were essentially handed cheap or free money to fix up their won failures, so this would obviously look good on their books. Low or negative rates however creates the risk for banks that their returns are rapidly diminishing and negative rates could cause a run on them. I hope they are sweating because their sense of power and invulnerability has been unchecked for too long.

"overall the market is largely an emotional response to what is happening in the world." yes....the human factor.

"I hope they are sweating" You are kidding right? They own the Republicans hook line and sinker, probably Hilary and as self-confessed masters of the financial universe consider themselves infallible anyway. I think Kunslter has summed up quite well how they will finally come to understand they are wrong.

yeah, yeah OK rose tinted glasses. Can't help being hopeful though.

Re#2 As I have noted before, in terms of financial stability, claimed unfunded collective asset values are fiction. After a reported bank insolvency event the market will only need to know the market clearing value of the ~1,500,000 mortgaged properties currently registered in debt to the tune of ~$214 billion. View RBNZ data

My unencumbered residential property does not collateralise unrelated third party mortgage debt.

Re 2: The structural problem in NZ is that most of the savings are held by those at the wrong end of the life spectrum (read retirees/nearing retirement) and the debt is held by those deemed to have the highest MPC. If retirees are complaining about low TD rates then start spending because the younger generations are broke.

And counting the housing stock as "assets" is a joke. How about we put it all on the market at once and see what it's worth.

...which is what will happen as BB retire and cash up.

Rastus, I don't follow your logic , and I think you are clouded by either wishful thinking or sheer delusion

1) I don't think that BB's own all the rental stock , many landlords in Auckland are young(ish) Asians

2) If retirees do owns the rentals, then then need the weekly rent because the NZ Super is a joke

3) You assume we will all sell simultaneously , I intend to stay in my home until age 90 if possible , so my home is not coming on the market anytime soon .

Mike , the value of a property , like any asset is purely based on its current and future earnings , to suggest an asset class that generates income , has no value and is as you suggest a "joke" , is simply wrong .

As long as we have 1,000 to 1,200 new migrants crowding through the arrivals gate at Auckland every week , we will have demand for housing to rent

And you accuse rastus of bring delusional - kettle pot black

Well thank -you MM. I have never been able to comprehend how a house is an "asset" . Ongoing liability seems more apt.

Very few are able to logically separate "property" and "house". Almost all use the terms as interchangeable. The "property" is the asset. Any improvements or "house" is a liability as it depreciates. On top of that "ownership" only holds to the extent that the state has no better use for the parcel of land than to allow you to believe you own it. This is found out when the "owners" cannot prevent the property from being taken by the government or mineral rights being allocated to others. I suspect a few Cantabrians will have an enlightened perspective on this.

Has anyone seen this story in The Telegraph ?

The Institute of International Finance is the world’s biggest association of commercial banks has warned the Chinese about CAPITAL FLIGHT .

CAPITAL FLOWS went into NEGATIVE in 2014 , and now seem to be exploding beyond control of the Chinese Authorities.

The Renmimbi could depreciate by a huge % damaging consumer spending on things like expensive imported NZ milk powder .

If anyone wants the link to the TELEGRAPH article on 5 Feb please let me know

#1. It appears what you describe is scientific method. Using imagination, develop a theory, then set about justifying it by observation and collection of supporting data in an environment which has been engineered to lead to the desired outcome. Like raising teenagers the results are not guaranteed and you may find out more of what not to do. Human innovation has used this since before the dreamtime to advance over other species as it dramatically reduces improvement time over straight trial and error reiterations.

I note that Medical Assurance (finance co essentially) will no longer lend or take deposits, ?? a victim of low rates/low margins./low profits.??

They are subbing their biz out to Westpac (too big to fail??)

#7 Will robots take over our jobs - not so sure about that - we will just get different jobs.

#1. All investment is unearned income and speculative, so motivated by feelings. The primary one being that of greed. But people that covet material things, including money, also have a tremendous fear of loss. The comment stream here is often full of people looking for validation to assuage their fears or confirm their greed.

Wealthy Immigrant category. Come to NZ. Shuffle your money in ( to satisfy Immigration), get Residency, then shuffle it out.

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=115…

Or was this straight money laundering?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.