By Martien Lubberink*

Seven and a half years after the collapse of Lehman Brothers one would think that the regulatory response to the Global Financial Crisis would start abating.

Many countries in the world implemented Basel III, an important overhaul of rules on bank solvency and bank liquidity.

To deal with large banks that are about to fail, there is the TLAC proposal of the Financial Stability Board. This proposal, which will enter into force in full by 2022, requires global systemically important banks to hold so much loss absorbing capital that taxpayers will no longer have to foot the bill of a failing bank.

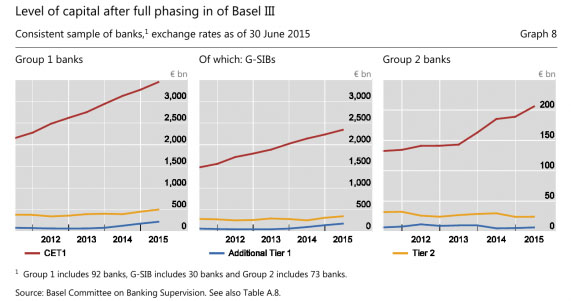

Banks have largely responded by complying to the new regulatory paradigm. For example, Basel III monitoring exercises have shown that since end-June 2011, banks have increased their Common Equity Tier 1 capital by about 60%, see the graphs below:

So far so good.

Basel IV

The Basel Committee, however, has shown no signs of relenting. Over the last months, this global bank regulator has churned out document after document in support of higher bank capital requirements. Some have dubbed these reforms "Basel IV", but William Coen, Secretary General of the Basel Committee, recently denied the existence of Basel IV.

Before I measure New Zealand against the non-existing Basel IV yardstick, three Basel Committee proposals in particular caught my attention.

The first is a consultation on a revised Standardised Measurement Approach for operational risk. Published on 3 March, this new approach removes the Advanced Measurement Approach (AMA) from the operational risk framework. The result is a less complex operational risk standard, one that helps curbing excessive variability in risk-weighted assets (these form the denominator of the risk-based bank solvency measure) and insufficient levels of capital for some banks.

Stefan Ingves, chairman of the Basel committee admitted this proposal would affect bank capital: “... it is inevitable that minimum capital requirements will increase for some banks."

Secondly, in a move to further reduce the variation in risk-weighted assets, on March 24 the Basel Committee published a proposal that will bar banks from using internal models for the calculation of the amount of capital they need to hold against loans. The proposal will affect lending to other banks and corporates in particular. It is a fine example of lessons learnt from the crisis: Once a supporter of the use of internal models, the Basel Committee now has somewhat reversed that position. There is just too much evidence of banks using internal models to imprudently cut capital.

The third proposal is about the Leverage Ratio. Here too, the Basel Committee signals its determination to increase capital, that is, for the largest banks. According to the proposal, the world’s biggest financial institutions shall meet a higher Leverage Ratio threshold than 3%.

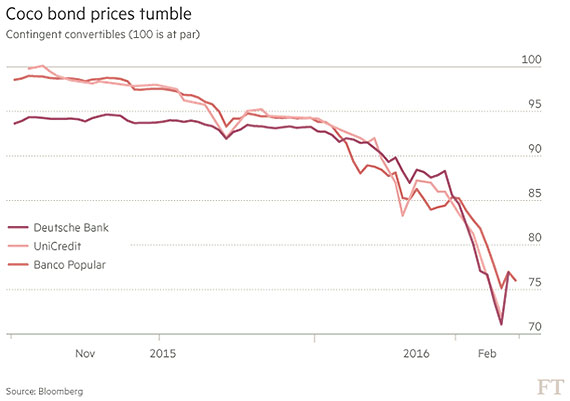

In addition, the Basel Committee contemplates introducing a cap on the amount of CoCos that banks can use to satisfy the Leverage Ratio. Such a cap make sense: CoCos are hybrid securities - they are neither debt, nor equity - that count towards the Leverage Ratio.

And yes, CoCos pay handsome coupons, but they are very risky as well, extremely risky. So risky that they affect the financial stability of bond markets. Only weeks ago, CoCos came under attack when Deutsche Bank contemplated not paying interest to its CoCo bonds. Just the thought of a bank not paying interests on its bond shocked the CoCo bond market: prices quickly tumbled, and for weeks in a row no banks dared to issue CoCos.

The idea to limit CoCos and let equity be the predominant element of the numerator of the Leverage Ratio therefore makes sense.

New Zealand

New Zealand is not a member of the Basel Committee. So, there is no formal requirement to implement any Basel proposals. However, entirely ignoring the proposals may be at our peril, especially if one considers the relentless increase in residential property values.

In an alarming op-ed, Interest.co.nz's David Hargreaves last week called upon our Reserve Bank to elevate capital requirements - to create a much bigger safety net for the banks and our economy if a big market correction came.

So, how are our banks doing now?

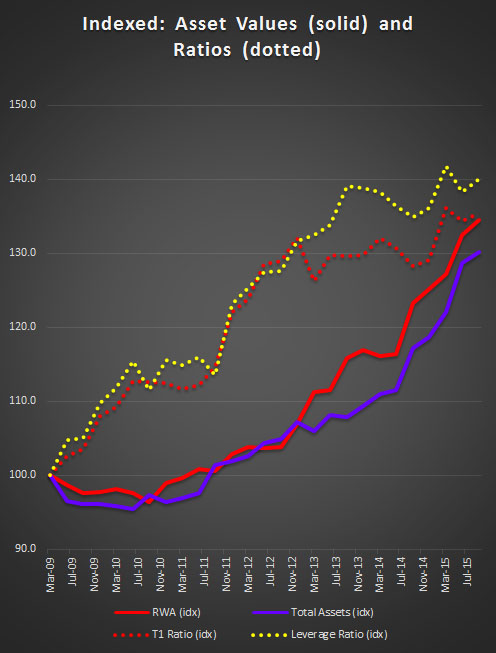

To answer this question, I toyed a bit with bank data from the Reserve Bank website, and from the accounts of our banks. I added all assets and capital of our banks together to create an overall bank balance sheet for New Zealand. The size of the balance sheet, measured in Total Assets is roughly $437bn, up from $339bn in 2009. To show trends, I decided to index the data, with March 2009 as the starting point of the index, when the worst of the crisis started abating.

The graph below summarises the data. It shows the development of Total Assets (blue solid line) and Risk Weighted Assets (red solid line).

Both assets types have increased, but it is not that one is clearly outpacing the other: the relation between RWA and TA is remarkably constant: 58.4% with a standard deviation of 2% and no discernible trend. The solid lines show that banks, in the absence of a leverage ratio requirement, do not overinvest in assets with a low risk weight. In addition, the data appears to debunk the Basel Committee claim that there is serious variation in Risk Weighted Assets. In New Zealand, there is little variation over time.*

What about New Zealand solvency ratios?

The dotted lines in the graph above show that both the Tier 1 ratio (red dots) and the leverage ratio (yellow dots) have increased, with growth picking up again since mid-2014. The Tier 1 ratio now stands at a comfortable 12%. Even more interestingly, the Leverage Ratio that I calculated (Tier 1 over Total Assets x 100%) stands at 7%, more than twice as much as the Basel committee requires.

This is encouraging. To me it indicates that the RBNZ acknowledges the risks of the housing market and motivates our banks to build that bigger safety net that David Hargreaves wants.

The only weakness that I found is the amount of Tier 1 CoCos issued by New Zealand banks, which drives a 133 basis points wedge between the Tier 1 and Common Equity Tier 1 ratios. Perhaps the Reserve Bank could think about introducing the cap that the Basel Committee proposes.

*There is some variation between banks, with some banks holding more risky assets than others. However, my analysis looks at aggregate data, in line with the way the Basel Monitoring exercises treat country data.

*Martien Lubberink is an Associate Professor in the School of Accounting and Commercial Law at Victoria University. He has worked for the central bank of the Netherlands where he contributed to the development of new regulatory capital standards and regulatory capital disclosure standards for banks worldwide and for banks in Europe (Basel III and CRD IV respectively).

4 Comments

A move away from the internal risk models is the best idea. The banks demonstrated they were incompetent at creating those models and had no idea what position their banks were in which led to the US collapse and the problems in London. There are a number of global banks that will suddenly find themselves in a non-compliant position if some or all of the regulations are put in place.

The risk weightings are also significant, I think they are too lax on residential housing. It's good to see that our banks seem well positioned relative to Basel III but that doesn't eliminate risks to the financial system. It's also not a protection from a major event.

I think there should also be some additional capital required where a certain asset class exceeds X% of the banks total exposure (i.e. the risk weighting % for housing is X% up until 30% of the banks total exposure, and X+Y% for all exposure above 30% of the banks total exposure).

This is needed to factor in the correlation risks for a bank's exposure (if they are well diversified, they should be rewarded with lower capital requirements as their risks are more spread, and vice versa).

NZ's banks have a globally unusual high proportion of exposure to residential property - thus the risks (and capital required) should reflect this.

It would be far more comforting if the headline were able to not say "RBNZ is motivating our banks to 'build a bigger safety net'" but were able to say that the RBNZ was "requiring the banks to build a bigger safety net"

The RBNZ has many powers of prudent regulation they choose not to use.

Good suggestion, however, I cannot see what exactly the RBNZ tells banks to do. I assume there is some moral suasion at work here.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.