By Gareth Kiernan

The Reserve Bank’s recent announcement of new loan-to-value restrictions that it plans to implement from the start of October caught us a little by surprise – not the idea itself, because that was pretty well telegraphed, but the magnitude of the latest changes.

We’ve spent some time analysing the mortgage lending data and believe that these changes could have the biggest effect on housing market activity of any of the Bank’s moves since 2013.

This article presents our analysis of the potential effects of the upcoming LVR changes in October, as well as providing our estimates of the effects of the previous two sets of LVR restrictions in 2013 and 2015.

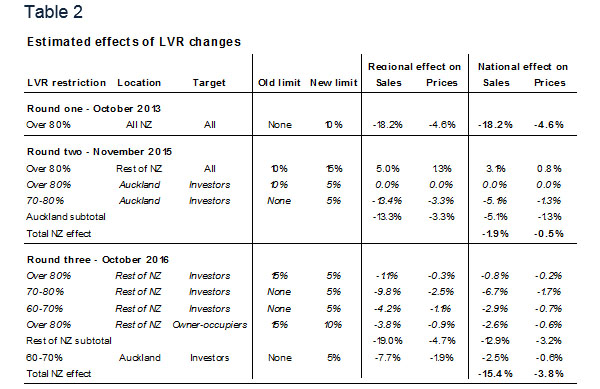

Our full estimates of the effects of the three sets of LVR changes on house sales and house prices are contained in Table 2 at the end of this article.

Round three: damn those investors

Dissatisfied with its failure thus far to slow the Auckland housing market and quell apparently speculative behaviour by investors, the Reserve Bank has announced it intends to implement further LVR restrictions in October this year. The Bank also appears, for now, to have given up on the idea of targeting Auckland specifically, and intends to return to a single nationwide policy.

The key points of the proposed changes in two months’ time are:

· an increase in deposit requirements for investors buying property in Auckland, with the maximum LVR reduced from 70% to 60%, and no more than 5% of lending to investors failing to meet this criterion

· a reduction in the proportion of lending that can be made to owner-occupiers outside Auckland with an LVR of over 80%, with the ceiling being brought down from 15% to 10% of lending

· the standardisation of lending rules for investors in Auckland and around the rest of the country – previously investors outside Auckland had been subject to the less stringent lending requirements faced by owner-occupiers.

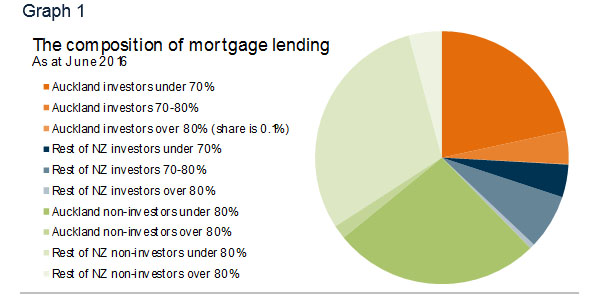

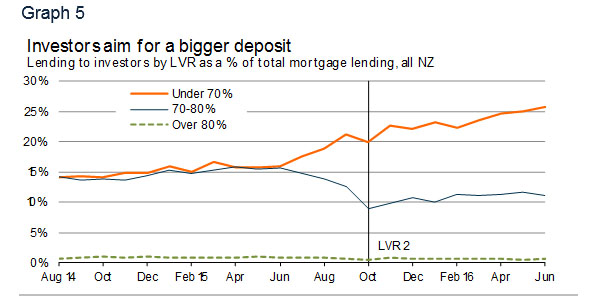

The biggest effects of the proposed changes will be on investor demand outside Auckland. Over the last eight months, an average of 37% of lending to investors outside Auckland has been with an LVR of over 70%. Furthermore, the Reserve Bank’s estimates suggest that 35% of lending to investors nationally has an LVR of between 60% and 70%. In other words, as much as 72% of investor borrowing outside Auckland could be affected by the proposal to eliminate lending to investors with an LVR of more than 60%.

However, the Auckland experience shows that a relatively large proportion of investor lending is able to be exempted from the restrictions. Since the LVR restrictions for investors were introduced last November, an average of 13% of lending to investors in Auckland has had an LVR of over 70%. This relatively high figure is due to the “combined collateral” exemption, whereby an investor might have a high-LVR loan tied to their investment property (which makes sense for tax purposes), offset by a high degree of equity in other property (eg their family home or, because the policy was regionally targeted, in investment properties in other parts of the country).

The effects of the upcoming changes in October

As the LVR restrictions become tighter, there is less ability for investors to use combined collateral to get around the LVR requirements. From later this year, investors getting a new mortgage will need to have 40% equity in investment properties across the country (rather than, previously, 30% in Auckland and 20% across the rest of the country), which will enable less “shuffling” of equity between properties. And the 60% LVR ceiling will mean that, all other things being equal, fewer investment properties can have a “deposit” financed using equity from the family home than under the current regulations.

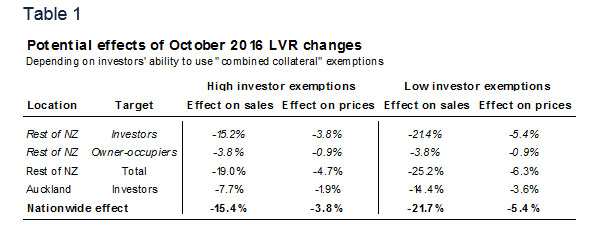

Table 1 shows our estimates of the potential effects of the upcoming LVR changes on housing market activity. The tighter LVR restrictions for investors could result in a fall in house sales volumes in Auckland of between 7.7% and 14% in sales in Auckland, and a drop in sales outside Auckland of 15-21%. The reduction in high-LVR lending for owner-occupiers outside Auckland would also contribute a 3.8% reduction in sales.

Overall, these results add up to a fall of between 15% and 22% in sales activity nationally.

How did we get calculate our estimates?

Our estimates based on high investor exemptions assume that exemptions for investors with an LVR of over 60% continue at the same level as exemptions for Auckland investors with an LVR of over 70% since the most recent changes in November 2015.

The other end of our estimated range assumes that, going forward the proportion of high-LVR lending to investors both within and outside Auckland comes in below the Reserve Bank’s ceiling by a similar amount as current lending to owner-occupiers. For example, an average of 8.0% of lending to owner-occupiers in Auckland over the last eight months has been to people with an LVR of over 80%, which is two percentage points below the 10% ceiling. So we have assumed that investors with an LVR of between 60% and 70% will make up just 3.0% of lending to investors in Auckland (ie two percentage points below the 5.0% ceiling).

Similarly, around the rest of the country, an average of 13.5% of lending to owner-occupiers over the last eight months has been to people with an LVR of over 80%, which is 1.5 percentage points below the current 15% ceiling. So we have assumed that investors with an LVR of over 60% will make up just 3.5% of lending to investors outside Auckland (ie 1.5 percentage points below the 5.0% ceiling). The slight difference of an assumed 3.0% of lending in Auckland and 3.5% of lending around the rest of the country does not make much difference to the final outcomes, and reflects that collateral exemptions may be slightly more easy to achieve for investment property outside Auckland, which will generally be cheaper than purchasing property in Auckland.

Which of these outcomes is more likely?

In our view, the effects of the upcoming changes are likely to be closer to the first (less significant) set of estimates. Although investors will have less scope to use the combined collateral exemption, we expect that most investors will still have considerable scope to rearrange their financial affairs to get around the new restrictions.

Nevertheless, it is clear that the effects of October’s proposed changes on the housing market will be significant, with the decline in sales and slowdown in price growth likely to be of a similar magnitude to the results of the initial LVR restrictions implemented in late 2013.

Background: effects of the previous LVR moves

The remainder of this article provides background on the estimated effects of the first two sets of LVR restrictions implemented in October 2013 and November 2015. Understanding the magnitude of the effects of these policy changes helps provide a better frame of reference for understanding how housing market activity is likely to evolve later this year when the latest set of restrictions is introduced.

Round one: experimenting with the unknown

Back in 2013, Reserve Bank Assistant Governor John McDermott presented some back-of-the-envelope estimates about what effect the upcoming LVR restrictions could have on the housing market. His guess was that about 20% of mortgage lending was to borrowers with a deposit of less than 20%, and that share would drop to 10% when the new restrictions came into force[1]. On that basis, he estimated that about 10% of house sales would be affected (or, at the most extreme outcome, prevented from taking place), with a flow-on effect of knocking 2.5 percentage points off house price inflation.

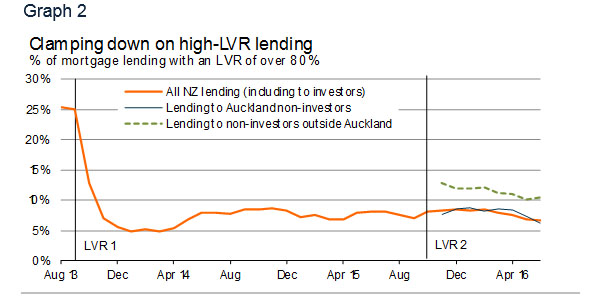

As it turned out, the effect of the first set of LVR restrictions on the housing market was bigger than those estimates. Data subsequently released by the Reserve Bank showed that high-LVR mortgages made up 25% of new lending in August and September 2013 before the new restrictions came into place (see Graph 2). And the retail banks took a very cautious approach to making sure they came in under the Reserve Bank’s ceiling – high-LVR’s share of total lending got as low as 4.8% in January 2014. Our estimates now suggest that house sales volumes were knocked down by over 18% over the following 9-12 months – a figure that lines up with the 15% drop in seasonally adjusted sales volumes between the September 2013 and June 2014 quarters.

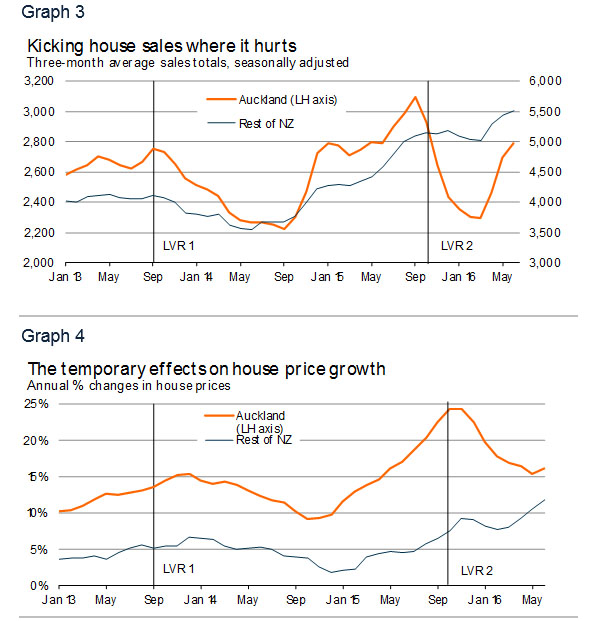

Auckland was hit harder by the changes, an expected result given that housing in the city is more expensive than the rest of the country. However, the difference in the drop in sales in Auckland and around the rest of the country was surprisingly small (see Graph 3), and the same was true of the slowdown in house price inflation (see Graph 4).

Round two: focusing in on Auckland

By late 2014, the housing market was regaining momentum, confirming our view that the effects of the LVR restrictions in slowing the market would be only temporary. The most galling aspect for politicians and officials was that it was the highly priced Auckland market that was leading the resurgence. By May 2015, house price inflation in Auckland was running at 16%pa (faster than it had been in 2013).

This outcome prompted a more focused attack on Auckland. From November 2015, virtually all investors buying property in Auckland would need to stump up with a 30% deposit.[2] The 10% ceiling for owner-occupiers would remain in place in Auckland but, in recognition that other regional housing markets did not pose the same financial stability risks as the Auckland market, outside Auckland, the ceiling was lifted to 15% (across all borrowers).

Our modelling suggests that sales volumes outside Auckland should have increased by 5.0% as the LVR restrictions were eased, with the tighter investor restrictions within Auckland leading to a 13% drop in sales volumes in the region. Seasonally adjusted sales data actually shows a 26% decline in activity in Auckland between the September 2015 and March 2016 quarters. The larger magnitude of this shift probably reflects the change in capital gains rules that came into place in October last year, which resulted in investors bringing property purchases forward ahead of the change in rules, thereby putting additional upward pressure on sales volumes in the September 2015 quarter.

Around the rest of the country, there was a modest 1.5% decline in house sales volumes over the same six-month period. The divergent trend lines up with what we would expect given the difference in policy directions between Auckland and the rest of New Zealand.

This divergence was also evident in house price growth. Between November 2015 and May 2016, house price inflation in Auckland slowed by nine percentage points, from 24% to 15%pa. Around the rest of the country, house price inflation accelerated (after a brief wobble between November 2015 and February 2016), lifting from 9.2% to 11%pa.

In conclusion

The effects of the upcoming LVR changes look likely to be of a similar magnitude to the first round of restrictions introduced in 2013, hitting sales volumes nationally by 15-22% and slowing house price inflation by around 4-5 percentage points.

Nevertheless, we believe that the effects of the upcoming LVR changes will again be temporary. In Auckland, in particular, the demand and supply equation remains profoundly out of balance, and further significant and sustained increases in residential building activity are necessary before house price inflation can be brought under control.

The housing market outside Auckland does not have the same undersupply issues and so is less resilient to changes in policy settings or other external shocks, but underlying fundamental drivers such as population growth and mortgage rates remain very favourable for strong housing market activity once the effects of the upcoming LVR changes have worked their way through the system.

[1] The restrictions required that no more than 10% of banks’ mortgage lending be to borrowers with an LVR of over 80%. However, there were some exemptions from this calculation that meant total high-LVR lending could end up being 10% or higher. Exempted lending categories include lending made under Housing NZ’s Welcome Home Loans scheme, refinancing of an existing high-LVR loan, bridging finance, or the “porting” of a high-LVR loan between properties. Since the LVR restrictions were first introduced in October 2013, some other loan types have subsequently been added to the exempted lending category.

[2] The Reserve Bank allowed for 5% of lending to investors in Auckland to have an LVR of over 70%, rather than no lending at all, to allow some margin for bank error.

Gareth Kiernan is Chief Forecaster at Infometrics.

38 Comments

I am unsure when Mr John Key, PM of NZ, the brilliant, genius, Forex trading head of global trading at the now defunct Lehman Bros & who was a member of the New York branch of The US Federal Reserve will FINALLY ADMIT TO ALL NZ'ers That the Auckland Housing Market Is A PONZI SCHEME. Supported by his government through lax immigration policies and lax foreign investor policies requiring no NZ tax number & no NZ bank account until recently & a scheme supported by the banks to increase profits over prudent lending practices. For a long time supported through utter inaction until recent years by the RBNZ. When does it ever become palatable in NZ to just Call it like it is a PONZI HOUSING MARKET complete with all the downside which will come and when it does watch Mr Key run for cover.

I'd have to say, having read the definition of "ponzi" that the Auckland (and now NZ) housing market could quite reasonably be described as one.

From the very Wikipedia article describing Ponzi schemes comes this quote, nestled under the "Similar Schemes" section:

An economic bubble: A bubble is similar to a Ponzi scheme in that one participant gets paid by contributions from a subsequent participant (until inevitable collapse). A bubble involves ever-rising prices in an open market (for example stock, housing, or tulip bulbs) where prices rise because buyers bid more and buyers bid more because prices are rising. Bubbles are often said to be based on the "greater fool" theory. As with the Ponzi scheme, the price exceeds the intrinsic value of the item, but unlike the Ponzi scheme, there is no single person misrepresenting the intrinsic value.

Tell me truly now: Does that not describe the lamentable state of affairs in our fair city in the most succinct and indisputable manner?

I don't think so because properties get rent yields similar to bank deposits plus capital gain. Properties can also be lived in. Many people are buying properties so that their children will have a place to live as well. A global market for choice property ensures that an Auckland property will be fairly safe.

JK still has 15 months to squeeze kiwi out of housing market and to help his overseas masters.

Height of arrogance and corrupt power.

All systems are go. Begin countdown: 10, 9, 8,...

To the moon...

No Mate , we are going to implement the Canadian 15% tax on foreign speculators , and the whole bubble will burst .......... and not a moment too soon .

Will it have any effect?

Comparing Auckland to a normal city with a normal 70 Up : 30 Out growth pattern. There has been a 50% short supply of land supply to Auckland City, since we were operating to the precepts of the non-ratified unitary plan. Post the adoption of the IHP recommendations there will now be a 30% short supply of land to Auckland City. Either way it is a severe supply constraint.

Short supplying land in the extreme like we have done and to the high extent that we will now do, this is going to make land prices go up. This will continue until people no longer want to live in Auckland. Perhaps the best solution is we allow freer flow of money so that more construction takes place outside of Auckland and people can make the choice not to live in Auckland.

Or our stupid council could open up some land.

here is a radical idea, cut demand.

cut back on migration to 15k per year, no matter how they come in student or not

stop non citizens buying

supply would no longer be a problem.

but we can not do that as this is the only growth policy this government has

Auckland City Council didn't ask for uncontrolled population growth. ACC are tasked with providing infrastructure for this population growth.

Do the rate payers want to pay higher rates to front the money needed? NO!

Do the tax payers of NZ want to pay more tax to pay for the infrastructure needed? NO!

Do the immigrants bring roads, bridges sewage systems and medical facilities with them? NO!

and there's the problem, Don/t blame the council, they represent their voters who don't want to pay higher rates or pay road tolls.

Blame the government who are allowing 70,000 people to arrive in NZ in the last year alone.

Heres an example to think about;

The new pipeline to collect sewerage from West Auckland is costing 1 billion dollars.

If Auckland had 1 million rate payers that would require $1,000 from each rate payer.

Auckland now has a huge deficit of infrastructure needed to maintain Auckland's standard of living.

The more population growth we have, the less wealth and lower living standards for everyone.

Will it have any effect?

Just for a moment ignore the shortage of land and slow building.

The mix of demand from overseas buyers ( including students looking for an easy resident visa) local investors and occupier buyers is critical short term.

If it results in prices falling so that investors quit buying and occupiers obtain a home that will be worthwhile.

However short term any buyer into a falling market had better have a significant deposit and the stomach for losing equity.

Why become the biggest fool when a little patience will be rewarded.

ANSWER : It will not have the desired effect , it will simply exclude more Kiwi buyers from the market , and open the gates for offshore buyers with cash to burn .

Its time to restrict offshore and non-resident buyers to new builds only and slap a duty on them , like Australia and Canada has done

Has the Reserve Bank considered whether these new LVR rulings (whilst putting a number of Kiwi's hopes out to pasture) will just serve to create more available listings for the much talked about foreign investors as well as all those domestic speculative investors who've already earned a shed load of equity? Low equity lending was only a small part of the housing problem. Also, it seems pretty counterintuitive to take measures that will purportedly limit risky lending the same month as they raise lending limits in the first home scheme. Crazy town.

What Foreign Buyers. Government is not able to see foreign buyer in NZ. Though is different if you go to any auction specially in Auckland.

May be government is not able to see as they do not see them as forigner but as rich friends who are helping them to run ecenony and it does not matter even if you sell NZ in the process to them - use it as casino

A question regarding housing supply and Gareth's statement:

"In Auckland, in particular, the demand and supply equation remains profoundly out of balance, and further significant and sustained increases in residential building activity are necessary before house price inflation can be brought under control."

I wonder if 'price stickiness' in the overall supply chain will mean that supply might have to overshoot markedly (and worse also happen ... read on,) before any discernible reduction in relative pricing of homes and increased affordability? Meaning there might be risk of what Ireland suffered post GFC? See the part about oversupply here:

http://www.economicshelp.org/blog/7334/economics/irish-property-market-…

If there is a similar risk for the Auckland and NZ, are there additional ways to reduce house price inflation and improve affordability?

Keen for any wise thoughts, thanks.

I find these restrictions a little scary. Someone living and working in Auckland with a 100K deposit can buy a 500K house in Auckland or a 250K investment property in say Hamilton or Tauranga. Both of those upper borrowing limits fall well short of even the lower quartile prices in the aforementioned areas. Has the RBNZ effectively prohibited Kiwi FHBs who live in Auckland from buying property?

In Auckland you can use the housing NZ "welcome home loan" scheme to buy a house worth $600k ($650k new) with a 10% deposit. The house has to be your main residence.

Actually, up to 10% of flows can be between 80.01 and 95 LVR, so there's still hope. If one wanted to pay over the odds for an over valued asset class.

No that would be the work of the National party when they sold your future to the Chinese.

Yes FP now FHB's are truly locked out of doing anything, as they now can't buy anything, investors and existing home owners are the winners and FHB's are totally stuffed by the 40% LVR's, my first home was an investment property an now the rest is history as they say...

yep a worry for FHB's but house owners outside Auckland too. To my mind house prices increases are predicated on three sources. 1) Chinese money coming in to Auckland. 2) Baby boomers consolidating their Auckland portfolios and/or moving to the provinces. 3) traditional credit driven growth.

It looks like financial source 3 has just been all but removed from the list. What happens to median and lower quartile properties in the provinces that are not investment targets for money sources 1 and 2.

That foreign money is now in more places than Auckland, has spread to Auckland and Tauranga and probably much further. It WILL destroy us unless something is done to stop it. I can still here Key's words from 2010 about us not becoming tenants in our own land, and all that has happened since then is that we have continued, unabated, towards that exact end.

Yes, I have been told recently I should 'invest somewhere else in NZ' why is it so hard for people to understand exactly what you've said above??? Furthermore, on top of needing 40% for an investment property, I wouldn't be able to use my Kiwisaver for said investment. Kiwisaver is NOT my main source of deposit but I would need it. Actually what am I saying, I don't need it at all. I'm screwed either way.

Let's say I've owned my own home in auckland for last 5 years, entering with 20% deposit 100k for a 500k house in 2011. My house got revalued at 800k a year ago and I was surprised to see i could borrow more (a lot more) if they yielded well to get over servicability hurdles.

So in 2015, my equity is 100k plus 300k = 400k and my loan is still 400k as interests so cheap why pay it back.

2015 LVR is 50%. Sweet. I'll buy a couple of good yielded properties in Hamilton for 350k each. 750k more property.

I only need 20% for these in early 2015. I have 400k equity so can buy up to 2mill property, another 1.2 mill. Maybe I'll buy a 3rd in ham? Nah just 2 for now and see how it goes.

A year later today, my auckland house is up another 15% to 920k... another 120k equity

My 750k ham property is up 30% to 975k.. 225k extra equity.

I now have 745k equity (sweet almost a millionaire, who said life was hard?). My property is now worth in total 920k + 975k =1895k. Almost 2 mill. Cripes. Was just doing what my smart accountant told me to do?

My LVR is now 60%. Nice. Rbnz even recon that's safe.

Actually, my valuations are 3 months old. I'll get them updated tomorrow and see how we sit. 6% over last 3 months? Extra 115k equity. At 40% that buys me something at 275k. Hmm. Better look beyond Hamilton. I hear Palmys about to follow Hamiltons boom as we all look for lower priced but growing cities, wonder if I can pick up one there...

Why aren't you satisfied just to have a house to live in?

Most are.

And get a real job.

I'm making the point that even a new investor in 2011 would not be too far away from buying again due to the extent of price rises and how dramatically they can improve your lvr in a very short time.

90% of investors who were around (the vast majority) in 2011 would of been starting from more than 100k equity, the big boys at 35% limited anyway

You are of the type society can do without. You are happy to exploit our young, forcing them out of the property market, engorging yourslef whilst our once family friendly suburbs become filled with overcrowded unkept properties. Take a look around mate....look at the stressese, misery, dispair and depression you are inficting on the next generation. You won't escape it either - you are also creating an asylum for your children to grow up in..

If everyone keeps borrowing up to their limit and there is no limit to the money the bank can lend, then what we are witnessing is not economic growth, but an expansion of credit. As the prices keep rocketing up will the bank ever say to you, no we think that house is too expensive we won't lend you the money for that? The answer is no, because the more prices rise the more your equity grows and the more they can lend you for the next property. Sounds a bit like a ponzi to me. It is the banks assessment of risk that should restrict the market. But is there any risk?

Have I missed something? The changes take effect 1 September 2016. What is all this talk of October now?

Now assume the above investor was less aggressive (the above pushed the limit pretry hard).

They just bought 1 in Hamilton instead. 350k now 455k, made 105k in a year. Gee that went well.

Own home in auckland still 920k. But only borrowed 400k plus 350k = 750k.

And own 920 + 455 = 1375k

My LVR is 55%.

Even safer. Palmy next they recon ?

RBNZ and central govt are deliberately playing dumb by ignoring obvious but by no means 'radical' alternative solutions to the housing issue (solutions that have been suggested on this website over and over and over again). If they want to slow down the market without wrecking it and killing home ownership dreams for New Zealanders like my kids, I reckon just four or five measures would help:

- moratorium on ALL international and non-resident buyers until further notice.

- full secondary rate taxation on ALL investment property sales less than three years after purchase, as well as a properly enforced capital gains tax for sales outside of this threshold.

- total loan to actual (non-investment) salary or wages, income lending restrictions for all property investors capped at 7x annual income or therabouts.

- restore 90% lending to New Zealand resident owner-occupiers and include apartments in this threshold.

- dangle a carrot in front of councils offering CAPEX funding on key initiatives in exchange for reducing property consent costs and doubling speed of approval processes.

I suspect implementing even the first of those measures would have the same effect on the economy as detonating a thermonuclear bomb in every suburb of Auckland.

Haha probably. Therein lies the problem, as measures like these could be considered commonsense and pro domestic business investment.

Stamp duty 15% on investors and foreign buyers. Take them out of the existing homes market and encourage new supply by exempting stamp duty on new builds.

Stamp duty 15% on investors and foreign buyers would :

Reduce demand ( investors 46%, students & temp visa 32% of resident buyers)

Increase supply (stamp duty exempt)

Raise funds ( for those where 15% isn't an issue)

Lowers prices (economics 101, drastically reduce demand and encourage supply so prices will likely drop)

What a fantastic tool.

Labour, Greens , NZ First ...... this is an election winning move ....

"the effects of the LVR restrictions in slowing the market would be only temporary".

If that is the end result then there is no point in implementing them in the first place.. Investors would see them as a merely as a "bump in the road" and carry on.

If the powers that be really want to control house prices then ban all purchases of investment homes such as in Norway and Sweden.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.