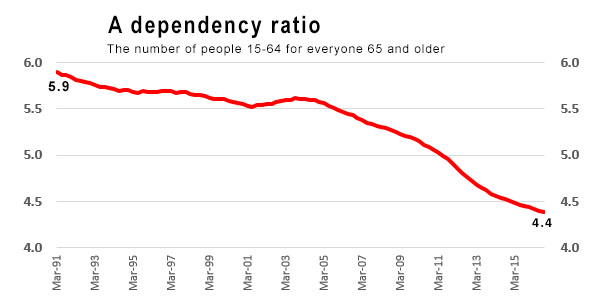

This is a chart that worries many.

It shows how many people 15 to 64 years of age there are compared with those 65 and older.

It is trending in such a way that it is hard not to conclude that 'soon' there may be too few workers paying tax to afford public retirement superannuation.

It calls into question the viability of the universality of NZ Superannuation.

How long could this trend continue?

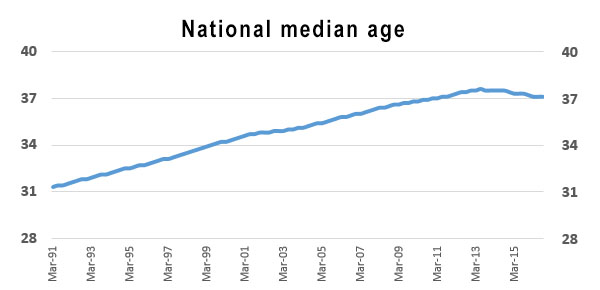

But other data from Statistics NZ's population database produces this:

The median age of our population peaked in 2013 at 37.6 years, and has been falling since.

That hardly seems consistent with what the data in the first chart shows.

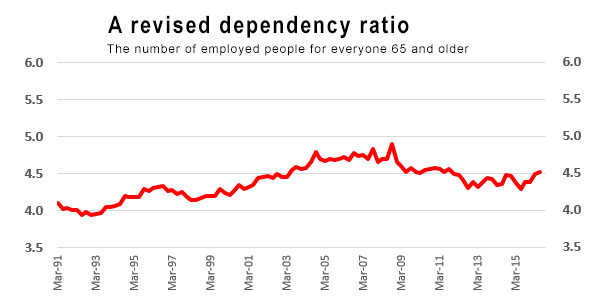

Part of the issue with the data in the first chart is that it assumes everyone 65 and over is not working. Everyone 65 and over is receiving the universal NZ Super, but increasing numbers of them are working (many by choice; me for example).

If that data is adjusted to show how many people are working for each person over 65 (and getting NZ Super), then there is no deterioration.

In fact, this ratio has been largely stable for the past 15 years.

Of course, this is not to say that the numbers of people 65 and over won't live a lot longer, nor to deny that the retirement surge of boomers is actually just beginning and has some time to go.

But a key way to manage that is to try to keep the median age of the population from growing, something we have been fairly successful at recently.

And one way to do that is via immigration of under 35 year old workers.

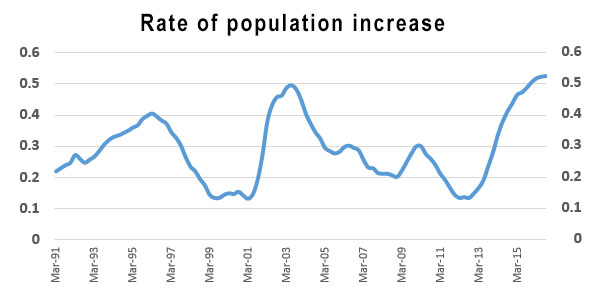

Migration opportunities come in cycles, cycles that ebb. Even the current high levels haven't pushed our rate of population growth to unusual levels. It may be relatively high now, but it is not by much margin.

Curbing migration aggressively will likely have the unfortunate effect of making NZ Super unaffordable at current levels much sooner.

(All data in this article is from the "Population Estimates" tab (DPE) in their Infoshare resource.)

38 Comments

So let us just start with the recent recommendations to make a 25 year qualifying period.

Doesn't go far enough. Something like pro rata of 35 - 40 years in the NZ work force.

What if you haven't worked? eg, if you spent time bringing up a family, or if you were unable to work.

Any penalty for such people would clearly be unfair and counterproductive. But for example people like me who spent 10 years of my working life overseas should arguably not get the full amount.

Another easy to implement approach would be for anyone aged 65 or older who chooses to apply for the super and has an IRD statement of earnings to be greater than (say) $50,000 to then be subject to a tax surcharge for each such year. Easily done with a one line change to the IR3. Hard to avoid. No need for complicated asset testing. And fair on those working who don't need the Super and fairer on those unable to work at that age.

Or simply make the pension a tax credit.

We had this back in the '80s. It was called the Superannuation Surcharge, and it wasn't very equitable then either.

Much like other income based tax approaches it was (and would still be) easy to avoid if your income is other than salary/wage based. So while Bob the 70 year old school principal on $100k would be paying his surcharge, Mary who earns $100k a year through passive means (dividends, rents etc) pays nothing.

"Equitable" to be sure is in the eye of the beholder.

Those who are able to remain in paid employment (and choose to do so) at age 65 are not retired. No means test or asset testing is required - the IRD already has the earnings data in its system for these non-retired folk.

Passive earnings is another matter. Maybe someone who is retired and has saved for their retirement shouldn't be penalized for that and maybe that's equitable in my view.

If you don't want to penalise somebody who has saved for their retirement and now wants to sit about on their backside doing nothing, why do you want to penalise somebody who is willing to continue working, helping to pay the taxes that fund NZS and other public benefits?

David this is based on busines as usual. What about all the jobs we simply won't need people to do? This has been covered at length, be it driveless cars, IBM's Dr Watson, factory robotics, retail, farming and so on.

At present we are filling jobs using discounted cheap labour (and many of these jobs are self generated..only neccesary due to extra mouths), the techno experts believe these labour units will soon be displaced also.

On this basis, our iimgration policy is in conflict...both arguments cannot be correct. I believe immigartion is more about bringing in comsumers to line the pockets of a few, not for reasons of superannuation.

Rastus,

Compelling logic. In my view, and only somewhat related, the world's biggest security and environmental issue is all the countries with growing populations beyond what their country can possibly provide for in any time of crisis. Examples include

Syria: 2016 population 18.5 million; 1960 population 4.5 million; median age 24 years.

Yemen , 27.4 million; 5.4 million; 19 years.

Egypt, 93.3 million; 27 million 24 years.

Nigeria, 187 million 45 million 18 years,

Pakistan, 202 million 44.5 million 23 years

Mexico, 123 million 28 million 28 years

There are of course countless other examples. I understand the countries concerned are not really comparable to NZ in any way, but any suggestion that their low median ages and still high population growth is a good thing for them is clearly not correct. It is not a coincidence that 4 of the countries noted are in significant states of conflict. I'm not sure how it can end well, while the developed world does not have the capacity to materially help them when the SHTF, which it is starting to do in a big way. It is no surprise that from the US to Europe they are starting to shut their doors to the hordes trying to escape from these places. We of course do not have our doors open to them at all, and I don't think anyone is advocating that we should.

I also understand there is a different debate on whether we do allow/encourage people in to do useful things. I am happy that we do up to a point, and probably slightly less than we have been, to both let our infrastructure catch up a little and then keep pace, but also to put just a bit of tension into the labour force to help lower paid folks get their wages up.

Okay , so here is the suggested tweeks :-

1) Retirement age goes up to 67

2) the NZ Immigration Service changes the settings , so like Australia , if you are over 40 you dont stand a chance of migrating there ( here )

3) Invest more in the NZ Super ( Cullen Fund ) so that it is able to generate the returns to keep current levels of payment

4) Encourage workers to work past 65 (or 67) , so their tax payments roughly equal the benefit they receive ( almost a zero sum game)

5) The NZ Super Fund itself , should be tax exempt to stop this silly merry-go-round of tax in and payments out

The 64 Billion Dollar question is .... what will work ?

Does Australia not allow parents to migrate to join their children?

State superannuation is a pyramid scheme with a rapidly approaching expiry date.

With all due respect, the solution to the problem is "bring in more contributors"? Well, isn't that just the solution to every failing pyramid scheme.

But what does it matter to me, anyway? Anyone under 45 who still expects a state pension should be sectioned and heavily medicated.

exactly as as those get old enough to qualify you need even more to pay for them, the whole immigration to pay for super is a ponzi scheme doomed to failure

I have to agree anyone younger than 45 would have to be retarded to think they will receive a pension. Most will be expected to use their kiwisaver (which will be inadequate for most) or survive on a below poverty pension, but with the added costs of being older.

Those under 45 are paying into the failing pyramid scheme, having to save their own retirement fund, will most likely work for most of their retirement and are being shat on by a bunch of worthless politicians.

I have to ask where my tax money is going and why the superannuation fund will be depleted by the time I'm retirement age. All I'm receiving for my retirement is a tiny tax credit in my kiwisaver account, along with the $1k kickstarter. That is not going to provide an amount suitable to last for my entire retirement.

How do you envisage this transition from universal entitlement to NZS to no entitlement to NZS, actually happening?

Do you think any Government is going to get elected on the basis of, or survive the implementation of, a policy to stop paying NZS to old people?

For the very reasons you have stated the transition will likely be sudden and may be a humanitarian disaster. Those that are in need will receive some amount of money, however I doubt that housing, medicine, heating and food will all be affordable. People may need to cross 2 or 3 of those items off their list.

Would the Government be elected? No. More likely imposed by the IMF similar to the ECB and IMF process in Greece.

You know we could address the problems now rather than pretend that this disaster isn't going to hit in the next 25-30 years when we hit peak retirement population. However that would be a responsible action to take.

Can we please get some sense of perspective here?

The costs of NZS are projected to peak at less than 8% of GDP. That is considerably less than some European countries are already paying for their pension systems. It is not a disaster and it most certainly does not indicate the remotest likelihood of the IMF being called in to take over.

Diane Maxwell ignores all of this because she has a barrow to push.

Please remember that while the baby boomer bulge is decreasing the dependency ratio now, it also means that in past times our dependency ratio has been abnormally high, so a more normal figure lies somewhere in the middle. As the baby boomers die off it should trend back to a more steady state level and the only factor effecting it will be the increasing life expectancy and birth rates. We have a good life expectancy now; will it increase much more with the various rising poor health indicators?

I believe that raising the eligibility age to 67 is not the big save all that we think that it will be. Approximately 4% of our population is aged between 65 to 69 so there must be roughly 73,000 65 and 66 year olds.

http://www.health.govt.nz/nz-health-statistics/health-statistics-and-da… (note the shocking difference between the races)

A single person gets $385 p/w and a married person $296/p/w, average say $340/w = $17680/year. So the Total cost for 73,000 people is $1.27 Billion. However you have to realise that the government taxes this so, say, 20% will come straight back = net $1.02 B. Now we have to make a bunch of other allowances, how many other people are already on a benefit, 7% say, maybe more? They are also saying that if they make these changes that they will have to make an exception for labouring workers whose s bodies are not up to it. How many would qualify? 10-20-30%? Similarly Maori who have a shorter life expectancy ( see the reference) How many more ? How do you police that one; everybody with a minute fraction of Maori blood? I am sure that while many of us don't bother with the Maori role, a large percentage of the population will be able to dig up a Maori ancestor somewhere. And I am sure that they will under these circumstances.

So what will the real saving be? I would be surprised if it saves $500 -$600 million.

Then we have to consider the fairness of making exceptions for different races and worker skills. Do we really think that it is going to work and people will mildly accept that.

Next we have to put this cost into the context of the tax evasion that is occurring under our present tax laws. The governments own estimates of tax evasion are between $3 to $11 billion. At this point the whole proposition looks stupid and can be easily countered by the response that the Government needs to get off it's backside and do something about collecting the taxes that it should. Further if they changed the tax laws to eliminate the many loopholes, they would have more money than they would know what to do with and they would be able lower the tax rates to everybody while continuing to pay super to over 65 year olds.

Mis-information and Mis-direction?

The following article tells a somewhat different story - and highlights what is missing from the above article

10 Jan 2017

Age Distribution of recipients of Welfare

http://www.stuff.co.nz/business/better-business/88241409/chart-of-the-d…

The working age population is supporting far more in the under 65 age group than 65+

Data provided by the Ministry of Social Development

Actually, I don't think you are right here. We don't have data back as far as 1991, but here are the totals for the number of people on all Welfare benefits: (all as at September)

1991 - [don't have] vs NZS = 392,800

1996 - [about 400,000] vs NZS = 430,800

2001 = 352,492 vs NZS = 461,600

2006 = 282,147 vs NZS = 514,500

2011 = 328,496 vs NZS = 584,900

2016 = 282,875 vs NZS = 701,100

We do have the Welfare data quarterly since December 1998, so I should be able to chart that in a similar way to the charts in the article. But it is pretty clear from the numbers above that it will show that the Welfare benefit load on the taxpayer is not rising because of increasing numbers accessing them. We are back to pre-GFC levels, even though our population is much larger.

That's the problem with Stuff's Chart of the Day - it gives no perspective, even though it is from the same data source, MSD.

The numbers of people on NZ Super are much larger and growing. The number of people on Welfare are much smaller and declining.

Apologies

Had to look at that MSD graph 3 times to see I had misread it

Had been reading the right-hand bar as 65+

On re-examining it now, more carefully, I see it's not

Interesting. The other thing that I take from it is that while the middle two age brackets cover 15 years, the last 55 to 64 covers only 10 years and the numbers on a benefit only drops from 83,000 to 63,000. This is not proportionate and indicates that as people age, more of them need a benefit. It is logical to suggest that, regardless of superannuation, this trend will significantly accelerate as people age over 65 years. So how much would the government really save by excluding 65 and 66 year olds?

The "Immigration for Superannuation" scheme/concept seems quite flawed and one dimensional.

This seems to be more of a political justification for maintaining high levels of immigration than a sustainable economic one.

Many recent immigrants have reasonably low levels of authentic business-building industry-building skills, many at the retail & primary sectors, many are transient and move back & forward to their home countries after gaining PR.

NZ may end up having to support many recent immigrants in various ways as well as supporting more deserving superannuitants.

A significant number of people are going to live long enough to live 30 years in retirement, after 45 years in the workforce. Would they have paid enough tax to cover it ? I would say for a significant number, (50%?), the answer is no .

The only way to pay in the future is to pay into a investment fund now. That the current govt has failed to do so , only makes it more expensive from here on in.

God save NZ

You haven't shown us the number of dependent's 0-15. That changes too over time and will change the figures. Indeed with a stable total population, the very dependent young would be small and ease the dependency load considerably.

The population growth might have produced some extra tax payers but it hasn't raised the countries productivity per person. we now have more people who have to be supported by what the country produces.

The larger population needs more than $100 billion dollars spent on urgent infrastructure to support this population growth. That's more than $100,000 per tax payer.

Had we kept our population stable the infrastructure was already built and paid for by the oldies and the younger less numerous generation would have coped just fine. Not now though, because on top of looking after the oldies we have to build the infrastructure to support all these immigrants and get Auckland out of gridlock.

I think when the penny finally dropped for John Key and he finally realized his legacy for NZ is that he has lowered our standard of living, damaged our lifestyle and introduced permanent poverty to a generation of NZers he finally realized his folly and thought, I'm out of here, some one else can try and clean this mess up.

I think that we should look at the past and see how they did it in those days. NZ super has been around for a long long time. The post war baby boomers were, as children, supported by a very depleted work force. A work force depleted by war and also married women were only just starting to work. So how was it done in those days because not only was there super there was a family benefit for each child and university education was free. We must be very very dim not to consider these factors. Or perhaps it just politics.

Right. Governments are wasting funds in many inessentials these days, just to keep up with the Joneses. Just like families who fritter away resources, the governments also do and get caught short for essential things. And then the debate starts as to what is essential and what is not..and the current fashion is to think Super is not essential. It is the inefficiency of the government that will be perpetuated, not the welfare of citizens.

And there are umpteen number of economists/analyst who can work the figures to suit their conclusion.

It is all a sham/scam. An healthy skepticism of government is what is required among the voting public.

I agree Smokey. It seems to me that somebody has an opinion and then finds an economist who will provide them with the mathematic formula to prove what is wanted is true. The more complicated the model the more it manages to confuse. Gove was certainly right when he said the people are sick of 'experts'. It is all just an elaborate scam

Statistics. A lot of people died before reaching the retirement age of 60. Even those that collected the government pension didn't collect it for that long before dying.

People are living a lot longer so more people collect NZS and for a longer period of time. When the first pension was first introduced in England it was an equivalent to having a retirement age set at 115 these days. Let's change the retirement age to 115 to return to the good old days.

I never received a free tertiary education but you should not less people went to university and other tertiary education. Now more do (even though it doesn't help most people) so the total cost is a lot higher for the Government and only around 25% is paid by students/student loans. We could decrease education costs by removing student loans completely.

Dictator - Unfortunately I have to call you out on the retirement age of 115 claim. In the UK the beginning of the modern state pension was the Old Age Pensions Act 1908.(1) While average life expectancy was 47 on 31 December 1908 a total of 596,038 pensions had been granted.(2)

I very much doubt there are anywhere near this number of 115 year olds living today. I understand that a bit of hyperbole is allowed but it should at least be a little believable.

(1) Pensions in the United Kingdom

(2) Old-Age Pensions Act 1908

yes, and there was hospitals even in small towns but then the rich paid their share in taxes,death duties,stamp duty.

There are rules regarding supporting balance -of-family migrants who are too old to work

I agree. Immigration to New Zealand is helping to lower the median age.

NZ has a low birth rate below replacement level due to Pakeha birth rates still declining in New Zealand which is now lower than the birth rates of Maori,Pasifika & Asian.

Immigration is replacing the people leaving New Zealand for overseas.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.