Seen this Economist chart recently?

It has been reproduced everywhere, after RadioNZ first highlighted it.

Scary stuff.

How do Kiwis afford to buy houses like this? Last year we bought 90,462 of them from other owners and an unknown number of new-builds (probably about 27,000). All up that is 117,500 transactions.

These 2016 numbers are +2,000 more than for 2015.

So, we are doing more transactions even though there are sharply higher prices year-on-year.

But houses are rarely paid for in cash. They are almost always bought with mortgages. In fact, between 2015 and 2016 RBNZ data shows there were +40,500 additional mortgages over the year, a +2.7% rise. (Just in case you thought it was all those naughty cashed-up foreigners who are driving our markets with their cash-only deals. Apparently those are just random anecdotes and not market-moving trends.)

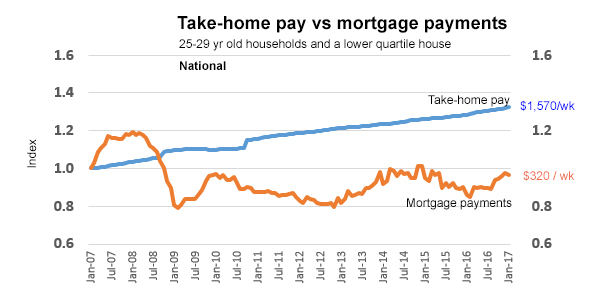

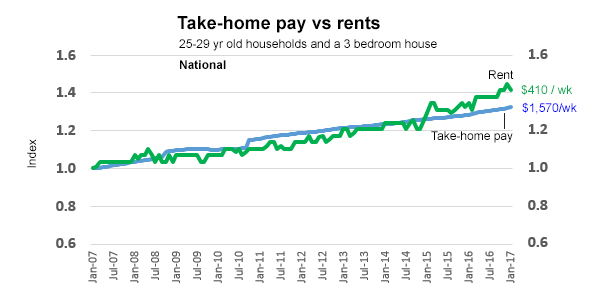

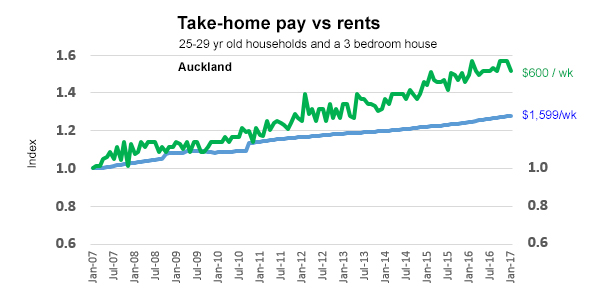

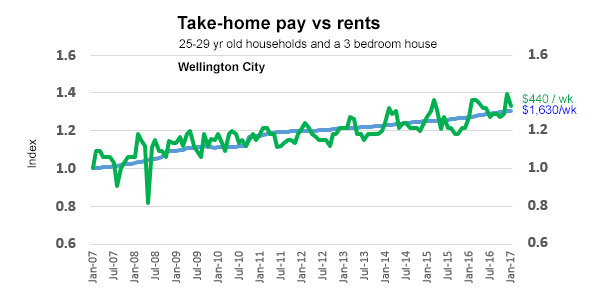

When you benchmark the actual experience against mortgage payments and rents, the story is nowhere near as scary.

We did that a few days ago and it is worth repeating here. We don't have data all the way back to 1980 to match the Economist chart; our review started in 2007, and looked at changes over the past decade.

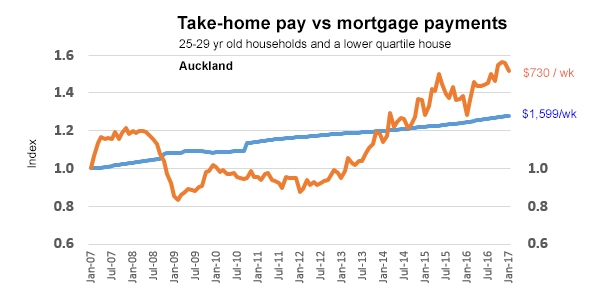

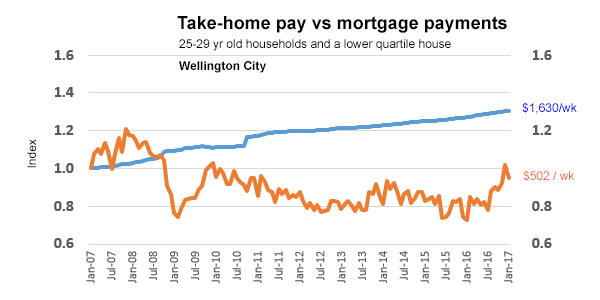

Here are the national perspectives again, updated with some main centre detail.

The lines in these charts are indexed to a common point of January 1, 2007 which shows the relative change since then. The values at the starting point are not the same; it is only the index point. That explains why the values displayed will always have the mortgage payment or the rent less than the household take-home pay, even if one has changed faster than the other. The lines reveal the rate of change.

The lines in these charts show the relative changes over the decade from January 2007, and not the absolute values. The ending values are noted to the right of each line.

The bottom line? New Zealand has a recent affordability issue, but it is relatively minor when related to take-home pay.

Lower house prices would help affordability everywhere, but household budgets need to deal with rent or the mortgage payments, rather than the face value of house prices.

The real issues are in Auckland, and that is distorting national averages. In most other urban areas, home loans are affordable for those households on median incomes.

We will add Christchurch charts later.

62 Comments

This graph is visual real talk.

Thank god the bubble is bursting.

The bubble will only burst if labour government comes to power. We all can also expect interest rate rise too.

Yes, the crops will all spoil in the fields and the skies will darken.... And any troubles that occur will have nothing to do with the way National set the country up for the last decade...

And what happens to first home buyers who have saved hard for a house and now find their mortgage is more than the value of the house.

Blood on the streets no matter who wins.

They keep paying the mortgage and can't move house. Blood on the streets is when the mortgage can't be paid due to mass job losses or interest rate hikes

This was exactly the fallout in the US in the subprime crash. People either refused to leave their houses or just abandoned them.

In the long term those with underwater mortgages that could make the payments often stayed in place, stuck in their house. Some are just reaching the point where the mortgage isn't underwater with the combination of price rises returning (years later) and the principle payments. Of course their net worth probably went negative during the crisis.

Payback ....

We all remember the sub-prime crash ...

Those affected are the ones who voted for Trump and turfed the elites out

Good piece, I love seeing the logic / work / data etc behind the words, thanks

Those Auckland rents and mortgage payments are high. I feel sorry for people paying the average rate or above.

So a Auckland lower quartile house comes with $700K mortgage and a Wellington one comes with a $500K mortgage. What about the average house?

The point of this is to show that there are affordable homes at entry level. Social change such as less people getting married at all or early in their life, or the fact that above entry level housing the housing is unaffordable aren't factored in.

Use of median income figures, for the age range, means that this applies to the highest earning top 50% households and may only marginally apply to the poorest 50%.

But houses are rarely paid for in cash. They are almost always bought with mortgages

Exactly.

What banks do is to simply reclassify their accounts payable items arising from the act of lending as ‘customer deposits’, and the general public, when receiving payment in the form of a transfer of bank deposits, believes that a form of money had been paid into the bank.

No balance is drawn down to make a payment to the borrower.

The bank does not actually make any money available to the borrower: No transfer of funds from anywhere to the customer or indeed the customer’s account takes place. There is no equal reduction in the balance of another account to defray the borrower. Instead, the bank simply re-classified its liabilities, changing the ‘accounts payable’ obligation arising from the bank loan contract to another liability category called ‘customer deposits’.

While the borrower is given the impression that the bank had transferred money from its capital, reserves or other accounts to the borrower’s account (as indeed major theories of banking, the financial intermediation and fractional reserve theories, erroneously claim), in reality this is not the case. Neither the bank nor the customer deposited any money, nor were any funds from anywhere outside the bank utilised to make the deposit in the borrower’s account. Indeed, there was no depositing of any funds.

The bank’s liability is simply re-named a ‘bank deposit’.

Banks create money when they grant a loan: they invent a fictitious customer deposit, which the central bank and all users of our monetary system, consider to be ‘money’, indistinguishable from ‘real’ deposits not newly invented by the banks. Thus banks do not just grant credit, they create credit, and simultaneously they create money.

Instead of discharging their liability to pay out loans, the banks merely reclassify their liabilities originating from loan contracts from what should be an ‘accounts payable’ item to ‘customer deposit’ .... Read more

Leverage from fictitious capital. So far no political party is pushing to change from private money creation to public money creation, nor to decouple it from debt creation. Too bad it's not an issue that many people understand, and there's little pressure to change.

This is so counterintuitive even economists argue over it.

However, sadly it's true and the root of the debt fuelled ponzi bubble in residential housing that benefits a handful of the bankers and elites.

Don't expect the system to change anytime soon but do expect it to blow up eventually. Nothing learnt from 2008/9.

But why are we comparing inter-related variables as they are exogenous?

So as long as interest rates forever go down (including eventually going negative), there is no issue with house prices continuously going up more than wages. Well I can sleep soundly now.

I didn't notice any mention of deposit size in the article however, which people do have to pay in cash for...

I reached a real milestone yesterday, my morgtage is now under $200K on a $1.5M house. Still higher than my original mortgage of $170K in 1996, but that was for a house worth $188K then. That same property now has 4 houses on it incl the one we brought selling for $650K each in 2015. Times are sure different.

Does this take into account duration of mortgage and total interest paid?

It states mortgage payments so I would assume it's an amortised mortgage. Working backwards from an affordability report it seems to use a standard 30 year mortgage for calculations.

e: so interest paid and so on are not factored in as it's the same cash flow out no matter the proportion of interest and principle.

Thanks. I was hoping duration of mortgage was standardized as this would massively skew things given longer terms are becoming more necessary.

I looked closely at the first home buyer numbers and a criticism that could be leveled at the method is the use of a 20% deposit. While this is financially prudent a lot of people only muster up 10% or less for their first home and the higher interest rates are not factored in with respect to affordability.

If the age of eligibility goes up to 67, then may as well make the assumption of 32 year mortgages since people will be working longer. I'm sure the banks will be modelling such a scenario already.

Interesting how some people think. For me the interest paid was the SAME as any rent paid so you always come out on top buying a house. Either you give the money to the bank or you give it to the landlord who then gives it to the bank, you work it out.

My parents told me exactly what you said when I was little. They have now lived (rented) the same place for...50 years ! and they have nothing to show for it. Had they bought 50 years ago, they would now be millionaires

Good graphs, the Auckland gap between wages and rents is on a really bad trajectory. I assume the average take home pay is for a couple? So if there were 117,000 homes brought, and 40,000 mortgages issued do we have any clues as to who purchased the other 60%?

Yeah, this (housing costs vs. wages) is something that doesn't make sense from a policy perspective, to me. You move to a city like London, NY, Sydney or San Francisco because of the job opportunities and their commensurate salaries. Auckland does not offer these, in comparison, it only offers the expensive housing.

Sure, it makes sense if you're from a Third World country - a move to Auckland is still a massive step up in lifestyle...but if it's just the easiest to get into when you're coming from a Third World country, that's a completely different proposition to being a genuine world class city.

NZ born and bred, well-educated Kiwis looking for a viable lifestyle...for what reasons should they stay in Auckland? Wages are not "world class" nor are opportunities, compared to the other cities above - yet increasingly more cities are offering a more viable mix of lifestyle and career opportunity for educated professionals.

This seems like NZ Inc. shooting itself in the foot, all for the short-term financial gains of a generation whose primary genius was being born at the right time to access affordable real estate.

As opposed to, say, Germany, who has placed great emphasis on housing outcomes for its population (and is worth holding up because it's a mix of renting and ownership). They haven't been the 100% have cake and eat it too investor-focused model NZ has chosen.

Edit: I should add, much like Vancouver, it also makes sense if your primary motivation is moving money out of mainland China and putting it somewhere safe from the Party.

Sadly, it's NZ Inc's leaders shooting Auckland in the foot. The rest of the country is not so affected. Auckland has been ruined by National. 9 years ago was simply not this bad.

Maybe we should aim a bit higher. It is a basket case of a city.

double post.

No. There were 117,000 homes bought & sold, of which about 27,000 were new to the market. Almost all sellers would also be buyers (less those who finally pay it off, die, or leave the country). So those 27,000 new houses attracted 40,000 new mortgages. Many people have more than one because they split the fixed and variable arranagemnets between two or more contracts/banks.

There is no missing 60%.

"Almost all sellers would also be buyers (less those who finally pay it off, die, or leave the country)"...."Many people have more than one [mortgage] because they split the fixed and variable arrangements between two or more contracts/banks"

I'm happy to be corrected as I am a relative layman compared to others on this site but don't we need to know how many people leave the country for example, or more importantly, how many people have split mortgages? Without those figures surely it becomes unscientific?

Camel's Back,

Looking at these figures,my assumption is that much of the apparent gap would be explained by the transfer of existing mortgages from one property to another? Am I wrong?

What about those greedy XYrs who bought their houses before Mid 2014 and have enjoyed no decrease in affordability since then? Have they no conscience? Nearly as bad as the damn boomers.

I think there are many folk who would prefer to see a downturn in the economy in general , as this will act as a reset button for all asset prices .

Right now if you are a renting family , you are unlikely to be able to save a deposit for a home , and wages are not showing signs of massive increases to offset the house price increases

I hope not and a downturn in the economy would benefit no one, least of all those at the lower end of the spectrum and FHB's - as these are usually the first employment casualties and where wage freezes hurt most.

I think that in addition to the LVR, the perception of interest rate rises (as the reality is many people are on higher fixes anyway) possible inflation with the weaker dollar, a general election in the offing that is now more uncertain than previously - there is a basic affordability challenge for the majority of people, especially in Auckland.

Rents have not kept pace with prices as people simply can't afford any more - there are only so many cuts you can make in food , fuel, clothes and living expenses to add to rent payments and I think that ceiling has now been reached -

it wont effect the top end properties - it never does - but for the lower 50% of rentals / properties we are pretty much at maximum payments -

Looking at the charts, Auckland is overvalued by about 50% by house price and 20% by rent

it depends what's driving the prices...

See the example of Vancouver: https://www.theguardian.com/cities/2016/jul/07/vancouver-chinese-city-r…

Also shows that those who say there is no housing shortage in Auckland because rents aren't rising are using alternative facts. Rent inflation is clearly outstripping wage inflation.

Well, yeah, recent record immigration will be pushing rents up, as foreign purchasing has inflated house prices before it.

Stop blaming immigrants. The increase in immigration 2013/14 caused no discernible increase to the rate of rent divergence.

The graph shows the Auckland rent divergence started occurring in 2009/10 when we had low immigration.

2010 marked the formation of the Super City and commencement of a planning regime that has slowed home construction to a crawl. The resulting housing shortage caused rents to rise. End of story.

Another person saying it's all only about supply, and not increasing demand? Demand for rentals will encompass both immigration and international students - and isn't all about only the recent acceleration in migration.

Christchurch charts will be interesting, would they be moving in the more affordable direction?

YES, of course

I would think they will show a post-earthquake increase in rents then a return to normality in the last year

"The real issues are in Auckland, and that is distorting national averages. In most other urban areas, home loans are affordable for those households on median incomes"

@ David C - Appreciate you have your more detailed affordability series by-city that you link to that bear out this point, but any chance of just including a 'National-excluding-Auckland' graph in articles such as these? It'd make the significant distorting effect of our largest city more immediately apparent to the reader.

As that 'National' figure would include smaller urban and non-urban areas beyond those addressed in your affordability series (or listed on your 'Median Multiples' analysis - http://www.interest.co.nz/property/house-price-income-multiples), you could potentially provide aggregate views of the 'national' affordability picture from a range of angles

- National (entire NZ)

- National ex Auckland

- National - Main urban centres ex Auckland (the urban centres per your Median Multiples page)

- National - Rural and small urban only (from memory this still comprises a material ~1.5m population)

Can only assume the atke home pay of 1599 / w is for a couple or the household as a whole? I dont know many 25 - 29 year olds on $115,000 a year !

There are a few in IT, but Auckland is not particularly viable for them either, anymore.

And they have the professional portability to be able to move around the world to places that provide a more balanced lifestyle, whenever they wish.

Thank you DC. Having somebody cut through with basic information is so useful. Such a contrast to the froth contributed by us interest.co common taters. I like the opinions - reading them combined with your factuals works.

Great work David, thanks for adding Auckland (as I begged you to). Christchurch will be interesting too although it will show it being affordable.

May I make 1 suggestion: put the mortgage payments and rent ON THE SAME GRAPH for each location (with take home pay as well of course). It will be interesting to visually compare both costs (mortgage & rent) over time, together with income.

So the graphs explain why FHB nationwide account for just 12 percent of the mortgage market , the average age for a FHB is over 40, and home ownership rates in Auckland are south of 55 percent, and interest only loans are necessary to get on the slope. Take a big pencil , starting from the top left corner and extend it all the way thru to the lower right corner , and put interest rates. Move that line up 100- 200 basis points and see what affordability looks like. 7.7 times joint income for Mr and Mrs Median ( or combinations of ) to gain a mortgage for the lowest quartile home . Moral of the story do not shack up with Mr less than median , otherwise that mortgage is 10x joint income.

Unfortunately the exceedingly expensive Auckland region house prices, and rents, is having a devastating effect on the social, financial and psychological welfare of a large number of especially younger families, who are unable to make ends meet, and getting nowhere, and feeling hopeless. It is not from lack of trying and they are working. Only option is move in with parents or friends - or move to middle of nowhere where prices much cheaper, but away from family and current social groups, eg west coast south island, Southland. But that is sort of how NZ got colonised, people moving from Europe to the remote isolated land of NZ at the end of the world - turned out good for most. Worth considering for those struggling in Auckland region. I know a few who have done it - moved out of Auckland and very glad they did.

Being newly crowned the 3rd most livable city in the world, Auckland is my pride & joy and will be my home forever, but I won't discount the possibility of buying a holiday home or two outside of Auckland. I have to admit Westport / Greymouth / Awatuna / Hokitika / Franz Josef / Cromwell / Clyde / Alexandra are all amazing places to holiday and to have some peace & quiet if I need a break away from Auckland...

Is it the time of year for that buzzfeed list of "liveable" cities again already?

The next generations of Kiwis can rest easy knowing that housing in NZ is all about you, and not the wider populace.

I'm struggling to see how the median net income for that age bracket 25-29 is $1599/week - I assume that is based on a couple's earnings?

'households' take home pay, so yes it will be a double income.

yep, two incomes and no children allowed until the 30 year mortgage is paid off

...and an unknown number of new-builds (probably about 27,000).

Way too low a number, due to the incompetent twits at Auckland Council dragging down the rest of the country. Auckland Super City forgets that people need to build houses and they have caused Auckland's rate of construction to fall to the lowest possible levels.

There is no level of immigration or interest rate setting that can mitigate the shear incompetence of Len Brown/Phil Goff Auckland. Auckland has a rate of construction that sits at about 1/3 to 1/2 as fast as Brisbane or Tauranga.

The real issues are in Auckland, and that is distorting national averages.

How do you come to the conclusion that it is not as scary as we think?

These graphs, as you state, are just relative to January 2007. Were houses affordable or unaffordable at that date?

If we assume they were affordable (so just theoretically), then the above is just an exercise in noting what interest rates have done in the last 10 years.

As interest rates go up, do you expect to see a reversal in house prices to keep mortgage payments static?

If not, what other drivers are there that you have not considered?

Indeed. Choosing to index from January 2007 just before the peak of the last housing boom is shonky.

It was bad then and its even worse now.

Ok but deposits must be paid in cash, which you mentioned in the title, but I didn't see deposit mentioned anywhere else.

First home buyer saving for deposit in 2007 needed the following for a median house 20% deposit. (I don't have the lower quartile data, but am assuming it follows the same trend as median prices)

Auckland: 20% of 460K = 92K

Wellington: 20% of 370K = 74K

Now the need

Auckland 20% of 805K = 161K

Wellington 20% of 520K = 104K

So deposits have increased a massive 75% for Auckland and a still troubling 40% for Wellington. Is this not part of the affordability picture for first home buyers in particular.

This is a big problem, if house prices go up 20% in a year then that can live those saving for a deposit, making no progress towards the deposit they need i.e they may save 20K in a year, but the required deposit they will need will increase by the same amount. It's hard to reconcile this type of house price increase, with what you are claiming here.

In 2007 you only needed a 5% deposit.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.