Lockdowns always cause a few interesting happenings under the hood of the economy. Our current stint over the past seven weeks has been no different.

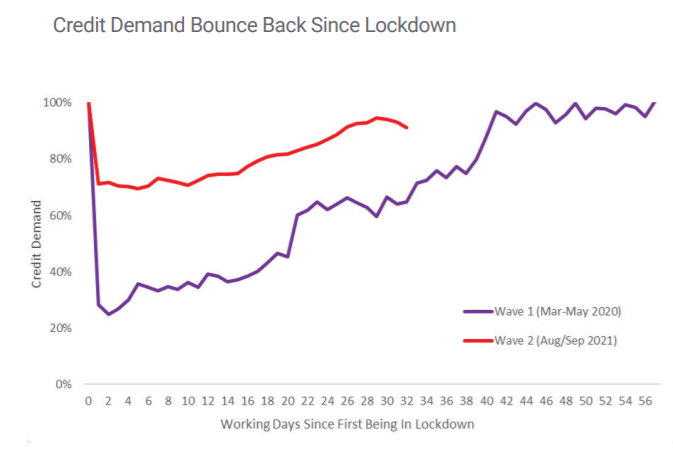

On one side we have the swings and roundabouts of credit/debt demand. This dropped 30% overnight in August when Auckland was plunged into level 4. However, it has recovered strongly across all sectors, even in level 3, with a 16% increase in demand.

In other parts of the country, at lower alert levels, it has fully recovered, according to credit bureau Centrix.

On the other side are the grim realities of a tough climate for business. Many were putting off rolling the dice on new ventures: company registrations were down 11%. Company closures remained high as some threw in the towel on their current circumstances. Others were struggling to make ends meet, with company credit defaults rising by 13%.

“Unsurprisingly, we see higher rates of credit defaults in rental and property services, accommodation, food services and transport, as closed borders and restricted movement impact business cashflow,” said Keith McLaughlin, managing director of Centrix.

Ripple effects in the economy in response to the most recent lockdown are lest drastic than our first, in March 2020. At that time we experienced a 70% drop in credit demand.

Businesses are also adapting to the Covid roller coaster and have now had more time to plan for these disruptions. Many provide a wider range of online offerings during higher alert levels, compared to last year.

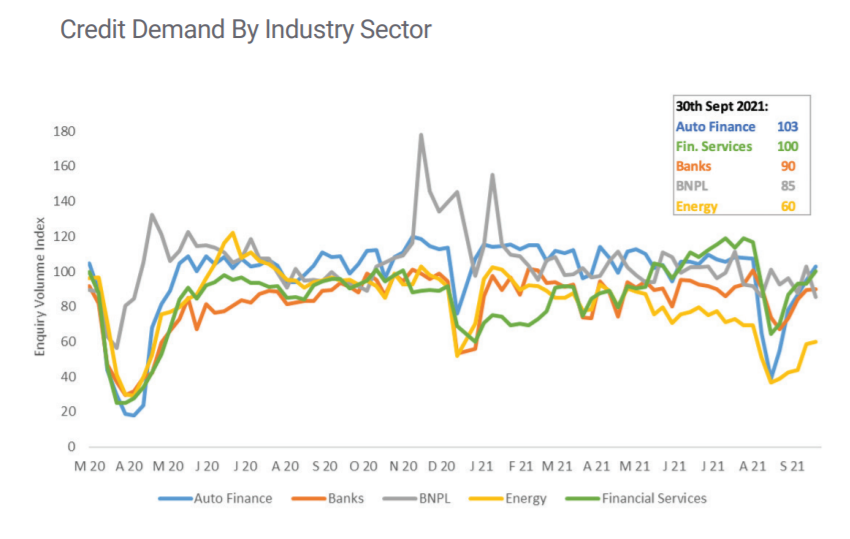

The buy now pay later (BNPL) sector, which offers an alternative to credit cards, thrived during level 4 lockdown. Demand increased during August as consumers sought to reward themselves during challenging times and worry about the bill later.

In line with increased vehicle sales, demand for auto finance is also looking healthy again after taking a dive during alert level 4. This bounce-back shows that consumers are adjusting to the ‘new normal’ and less inclined to put off large discretionary purchsaes, even at relatively high alert levels.

August was a tough, if not impossible, month to buy a new property. This was reflected in the value of new home loans which fell by a third. Again, September saw a recovery through industry workarounds of limited open homes and the resumption of property sales.

Despite the pitfalls, McLaughlin said there was reason for optimism. “Credit is a leading indicator of consumer confidence and the strong rebound in the credit market demonstrates that consumers remain confident. This should help power our economic recovery when restrictions eventually lift.”

4 Comments

It will be expected that a number of businesses will fold now as there is still no certainty for many particularly hospitality and the wishy washy pathway out provides no clear dates for a business to budget on for them or their creditors. This government does not understand business, that was proven with the foolish interference in contract law regarding business turnover and rent . They are completely amateurish when economic acumen is required.

The government just gave up elimination. I don't think any sit-in hospitality business once it is in lock-down should be expecting normal turnover till about this time next year.

Once you have slipped into level 3 it will be indefinite. The wave might end by late summer but the fear and restrictions won't. Maybe after the winter wave we'll be over the shock. If you can't adapt to takeaways, I just don't know.

Credit demand by itself is not a good gauge to compare economic impacts between the first and current lockdown.

Could the number of business closures be announced at the 1pm COVID briefings for balance?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.