The appetite of New Zealanders to take on consumer debt is waning with weak consumer confidence appearing to be the key factor behind this, credit bureau Centrix says.

In Centrix's March credit indicator Managing Director Keith McLaughlin says the signs point to an overall decline in demand and lending conversions. Consumer confidence, as measured by the ANZ-Roy Morgan Consumer Confidence Survey, sunk to its lowest level since the survey began in 2004 for the second consecutive month in March.

"Faced with uncertainty around Omicron, a retreating housing market, increasing mortgage rates, and rising inflation, Kiwis are starting to tighten the purse strings for discretionary spending," McLaughlin says.

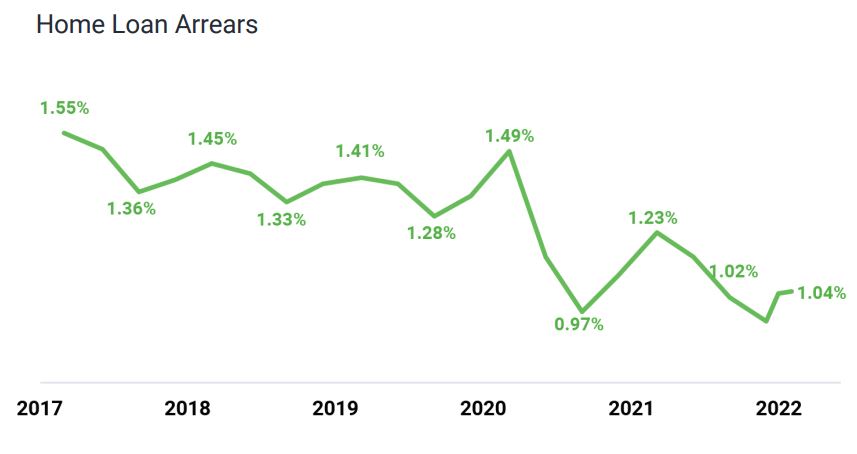

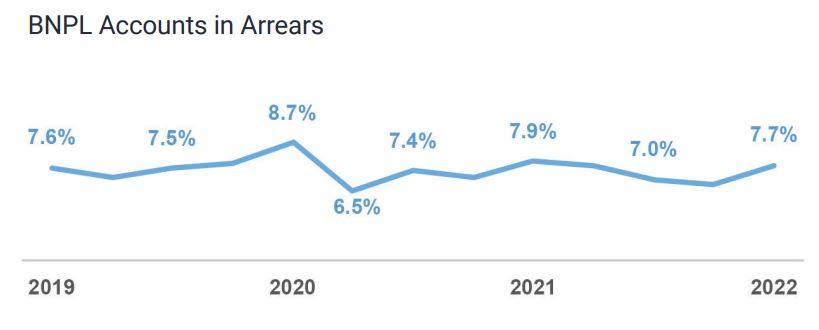

"The hardships facing Kiwi consumers are beginning to become apparent as well, with arrears on personal loans increasing to 7.8% in February – the highest level recorded since March 2020. Despite this, home loan arrears have been steadily improving, offering a glimpse into where Kiwi financial priorities are."

McLaughlin also says company closures were down 35% in the March quarter as business owners continue to adapt their business models to operating with Covid-19, with business credit scores increasing three points to 764 in March.

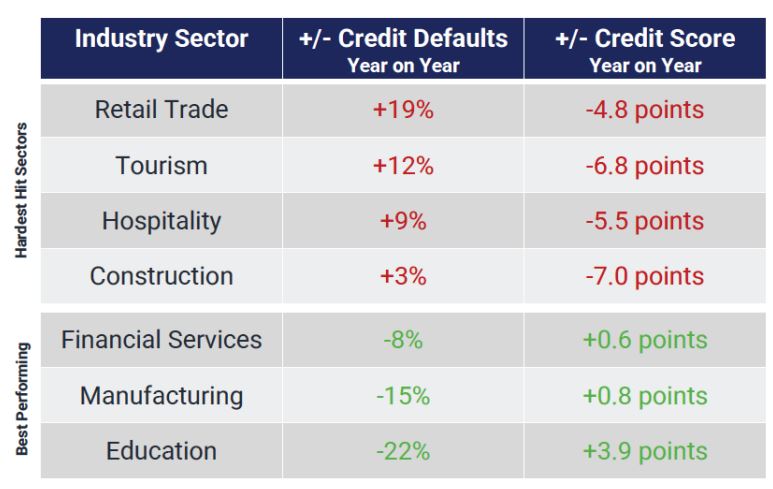

"However, the specific flow on effect of consumer credit trends is seen in the retail business sector, where defaults were up 19% in March, as business owners struggled to balance an impacted cashflow with the looming threat of Omicron potentially forcing employees into self-isolation," McLaughlin says.

"These issues, coupled with rising inflation, will be putting additional pressure on Kiwi business owners across the board. March represents the rising peak of Omicron, with these impacts expected to ripple into April."

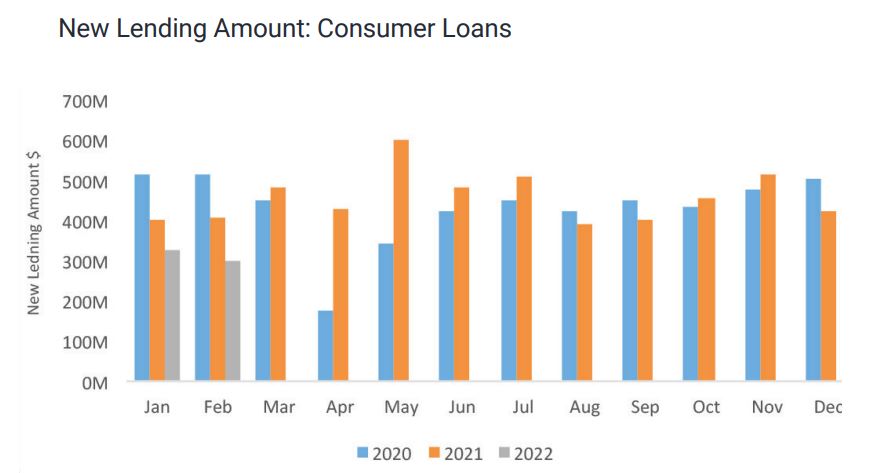

Following changes to the Credit Contracts and Consumer Finance Act in December, Centrix says lenders appear to have rejected 5% of new loan applicants who would have qualified for lending in November. New lending across consumer loans was down 26% year-on-year in March as conversion rates and decreased approval numbers continue to impact lending across the board, Centrix says.

"Demand for consumer credit remains down year-on-year, down 9% in March 2022."

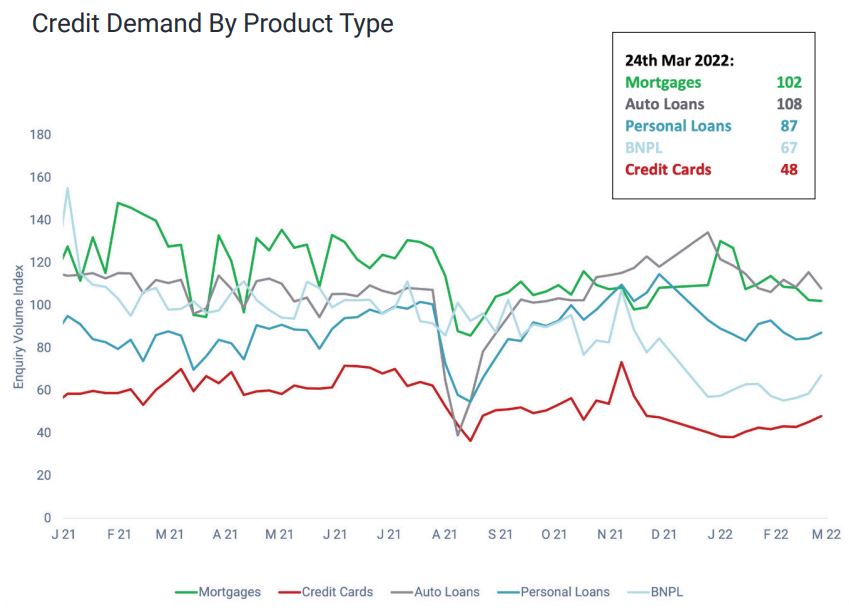

Centrix says the buy now pay later (BNPL) sector and bank lending have been the hardest hit, whilst vehicle lending remains strong reporting similar levels of demand year-on-year. However, mortgage applications were down 19% year-on-year. Despite this the proportion of home loans with missed payments was unchanged at 1.04 % in February, and down from 1.22% in February 2021.

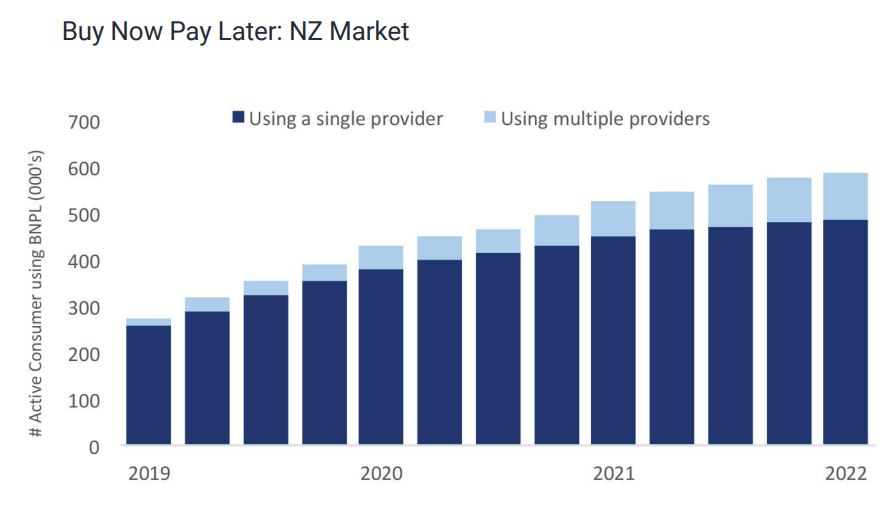

Some 587,000 New Zealanders are active BNPL users with half all active consumer credit borrowers under 30 using BNPL. Centrix says 7.7% of BNPL customer accounts are currently past due.

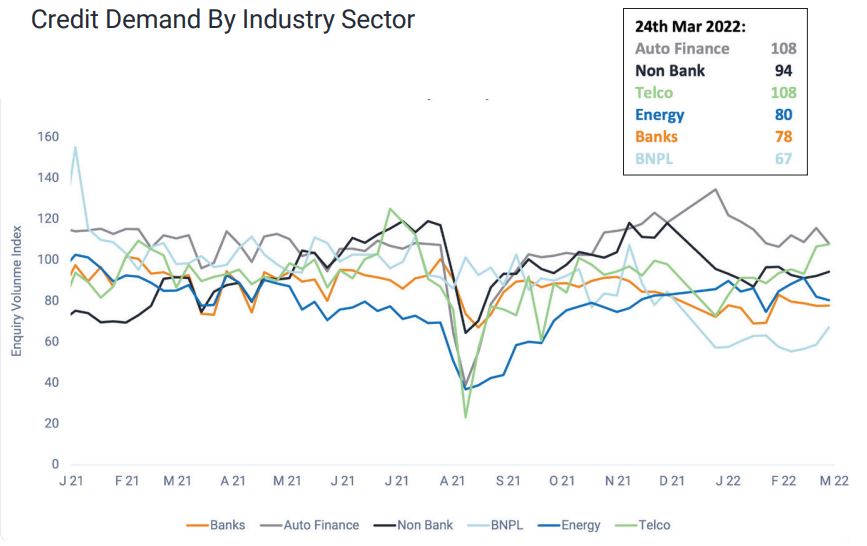

"Looking at year-on-year trends, business credit demand was down 5% in March 2022, with impacts in retail trade and hospitality driving these changes. Despite this, the average business credit score in February was up three points to 767 month-on-month. Retailers are one of the hardest hit sectors at present, with credit defaults up 19% on the same period last year due to falling consumer confidence," Centrix says.

"Furthermore, hospitality and tourism continue to suffer from ongoing restrictions and consumer uncertainty impacting bookings and spending, with credit defaults of 9% and 12% respectively recorded in March. Supply chain issues continue to impact the construction sector, with rising prices and skilled labour shortages also impacting the sector."

The charts below come from Centrix.

20 Comments

So many people are up to their eyeballs in consumer and property debt. Its going to be interesting to see how things unfold in the coming months with interest rates rising on that debt.

I feel sorry for hospo. They've been absolutely pummelled. People stop buying lattes before they stop paying their mortgages.

Yes, fight tooth and nail to get through the pandemic only to find that when they come out the other side all battered and bruised Joe Public's discretionary spending has fallen off a cliff due to rising inflation and interest rates.

Recession and correction are necessary. The strong and stable survive, those close to the wire fail, allowing space for innovation and opportunities for new entry over the next 1-3 years.

I believe our covid response has tried to save everyone, to the detrement of the whole long term.

This would hold some water if we hadn't artificially pumped and use our political and taxation system to essentially totally de-risk property investment at enormous social cost. It had nothing to do with 'strong and stable', it had everything to do with voters repeatedly voting explicitly for change and reform and governments betraying their democractic mandate.

Yet when it comes to recent FHBs, the Finance Minister has the stones to suggest that the value going down is a 'risk of owning property that people need to be aware of'. Funny, where was this thirst for reform when they were elected? I seem to recall quite a different song sheet not too long ago. But then again good luck telling who is singing what tune over the sound of the printers.

Since the 80s, the largest innovation we've seen from boom bust cycles is financial reinvention.

Was it really necessary to drop interest rates so low? If they could go back in time and change things would they have done it differently.

A bit of a hit on property prices and other investments right at the start and through the pandemic would have been quite acceptable and understandable. Yet property owners along with billionaires all got considerably richer during the pandemic. Now we face people, mostly less wealthy people, becoming impoverished as the interest rates rise.

Overall it seems a very unacceptable outcome. What on Earth were they thinking?

Not just the low interest rates but people also used the mortgage holiday to build up a cash buffer. This negated uncertainty and left more money in people's pockets, provided they owned a home.

I think you're quite right that people would have accepted a property market hit as the pandemic could be blamed for it. The stock market took a hit and kept on functioning. It's not like there was going to be a liquidity problem in the property market.

It is looking like the US is going to try to pop the bubbles in their various markets. Yet it is unlikely to succeed without blowing up their entire economy. The primary US export seems to be the USD and the demand is still considerable. If they stop printing more money the cash flows in the bond market would blow up somewhere else in the world. Due to this I cannot see the RBNZ or our banks going against the interest rates in the global market. Higher interest rates will be a short term event unless something goes very wrong.

It's been a long time since whole industries got turned off, the central bankers tried to pre-empt that by making money super cheap.

Less wealthy people would've been buggered back then if there were mass business closures, even more so if money was more expensive then.

A lot of it's a case of trying to envisage every possibility and please everyone when ultimately that's not possible.

If there are 10's of thousands of people who have no assets and no savings,. Then suddenly no jobs and no income. Then they can not pay the rent. Who really suffers then? The people who cant pay or the people who receive the rents?

The answer to that is why we did what we did. Asset owners have more political power than the poor.

Rising interest rates in the past have equaled the playing field between wealthy/poor and reduced the inequality gap.....here's hoping we see the same this cycle if we really have turned a corner from 1980-2020 where we have 40 years of falling rates and rising inequality.

Perhaps now we are setting up for a 1946-1980's cycle of rising rates? Similar to what the greatest generation experienced post-WWII. We do have war time like debts...although the only difference is household debt levels are very high.

Unless the poor become a voting majority that likely won't change.

That's unacceptable DGM thinking sorry Zachary Smith.....go and wash your mouth out! Unless you want property prices to go up, you're turning into a doom goblin....regardless of the financial and social consequences...

Everyone has been tempted by the super low rate environment to take on bucket loads of more debt, rather than paying off what they had as fast as possible. Debt is not your friend, and leverage works in both directions. Default will be come a commonly used word again.

The Fed is clearly signaling they are preparing to hammer inflation under control via interest rate rises. This will have a massive effect on the spectulative gambling in their asset markets. The tsunami of that change will effect NZ exactly the same way.

Popcorn

Yeah nah mate....best time to load up with debt and get the biggest mortgage possible as inflation is your friend and will help you pay off your excess debt! Its like free money they tell me.

Loading up is fine but at the right entry price. Entry at the peak bubble means you have to survive the inflation rate squeeze.

RBNZ DTI figures for 4th quarter 2021.

Total lending to FHB in Auckland with DTI > 7 was 297 million. Spread over 331 borrowers. Average of 897 k each. If D is 897 and the multiple is 7 That makes the combined income 128 k.

Q4 2022 354 million lent to 291 Auckland Owner Occupier non FHB borrowers with DTI > 9. That's 1.2 million loan average with incomes to support of 135K.

How many in these 2 groups took the 1 year fixed rate option to get the lowest possible payments?

Q4 2022 we are entering recession.

The DTIs for investors are much more scary.

Orr begged for DTi for ages. Now hes got it he is afraid to use it.

Good idea before the horse has bolted....but when the entire housing market moves outside what would be rational DTI's for given levels of income....the tool becomes like a sledge hammer.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.