Is the fact that homeownership has become an unrealistic dream for millions of young adults around the world a reason why the cryptocurrency bubble grew so big?

According to UBS chief economist Paul Donovan, it may well be.

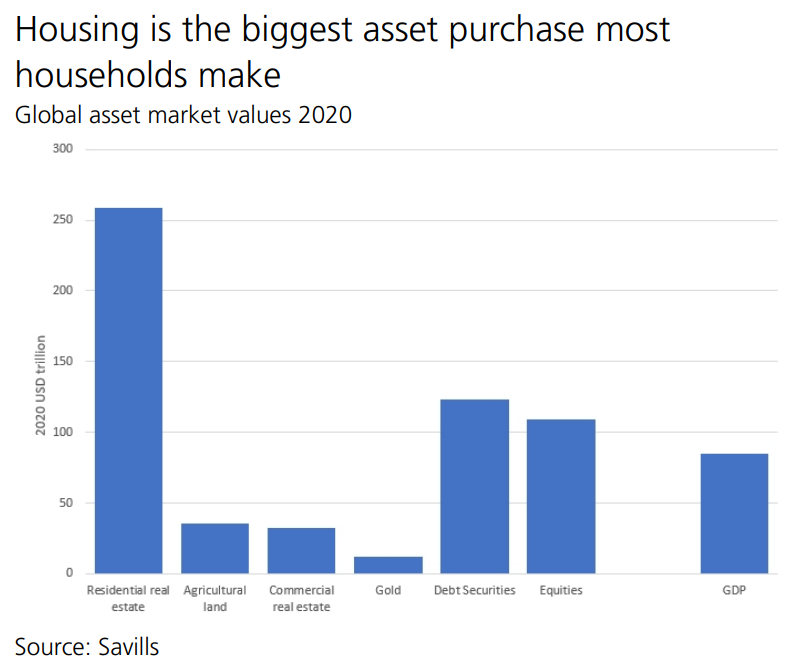

In a research report Donovan notes that in developed economies, housing is typically the most important asset an individual will own. So if homeownership is a realistic goal, young people will save for a deposit and other homeownership costs.

Alternatively if housing is so expensive young people give up hope of homeownership, there's less incentive to save for a deposit. Instead, argues Donovan, younger adults have an incentive to spend more or speculate.

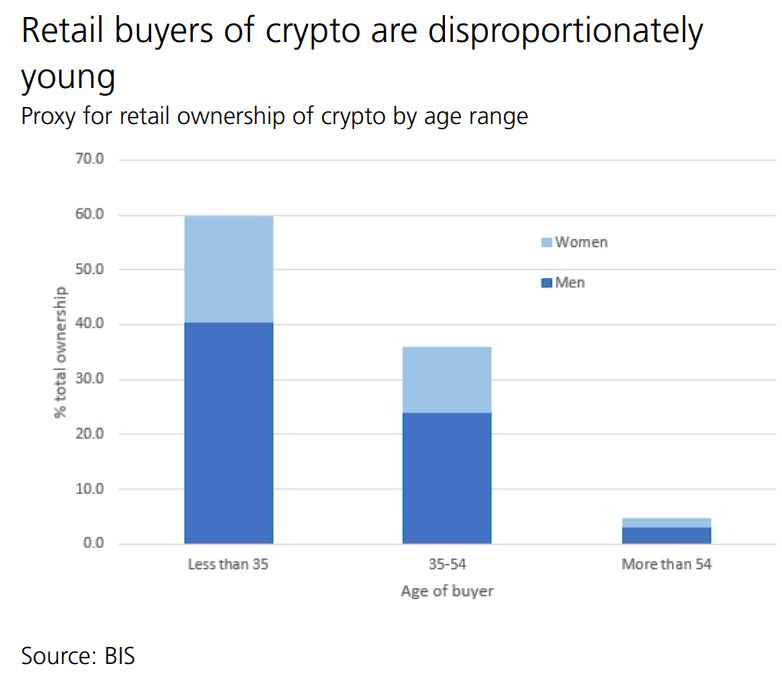

Pointing to research from the Bank for International Settlements, the central banks' bank, Donovan says crypto and meme stocks, equities whose value is driven by social media promotion rather than anything economic, are disproportionately owned by young people.

"Fewer and fewer young people can afford homeownership. Data suggests that speculation is more likely in countries with rising homeownership costs. The stereotype of many crypto-owners as young men still living in their parents' basements may be well-founded," Donovan says.

"If homeownership remains unattainable, gambling on crypto, meme stocks, and other speculations may remain attractive to younger generations. If homeownership becomes affordable for young people, this speculation may quickly fade."

Donovan argues that the importance of housing as an asset creates a very specific type of savings behavior with wannabe homeowners needing to save a deposit. Additionally they need to save money to cover things like legal fees and taxes associated with the purchase. On top of these are the start-up costs associated with owning a home such as property taxes, furniture, and maintenance.

"If someone is saving to buy a house, the savings approach is likely to be low risk. Buying a house entails a specific cost. There is a clear, nominal currency target that has to be hit. As house prices rise, the amount of money that must be saved will normally increase in proportion," says Donovan.

"Wannabe homeowners are not going to gamble the money needed for their deposits. Losing money through speculative investments means that the dream of homeownership fades further into the distance, and conceivably disappears. This is especially important for first-time buyers. This groups will tend to save toward a house in a conservative way. Gambling with the deposit for a home risks more than a monetary loss. If you lose the deposit, you lose the social status associated with homeownership, and potentially the independence that property ownership can bring. No one wants to be living in their parents’ basement in their forties, because of reckless investment decisions in their twenties."

But what happens if buying a house seems permanently out of reach? If homeownership becomes unaffordable for the young, their motives for saving change. And critically, Donovan argues, the risk appetite around savings is also likely to change.

Donovan notes that in the United States a majority of people aged between 18 and 29 live with their parents, the first time since the Great Depression.

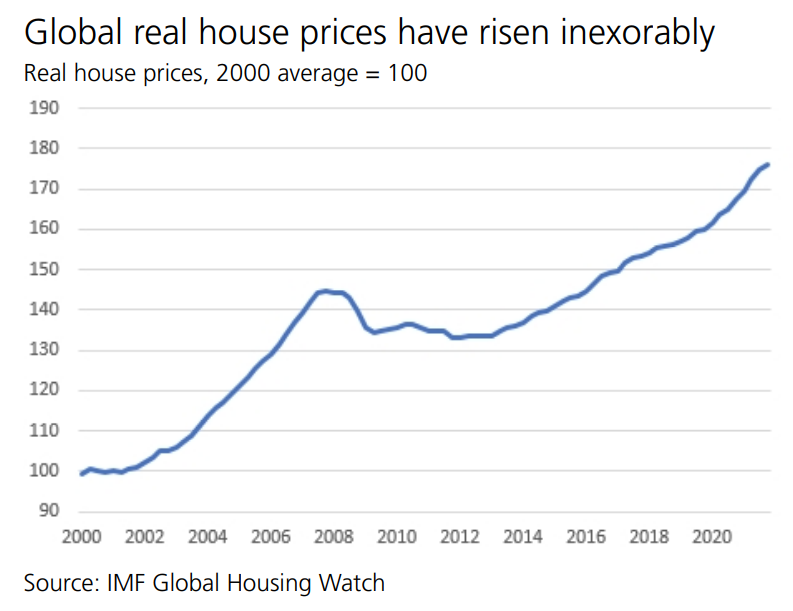

"The story is repeated across the OECD. In most OECD countries a majority of people aged 20-29 live with their parents, and the share still in the parental home has increased over the past fifteen years in twenty of those countries. The increasing share of younger people excluded from the housing market coincides with an increase in house prices around the world," says Donovan.

If young adults aren't saving for a home deposit, they can speculate with their money or spend more on the consumption of goods and services. If they take the speculation path Donovan says this must have an element of fun.

"To compete with consumption, and in particular the consumption of leisure 'experiences' like holidays, there needs to be some entertainment in the act of speculating. Crypto and meme stocks help provide that with online discussion groups which create a sense of community. Crypto in particular has been compared to a religious zeal in the approach of retail investors. Crypto and meme investing is not a passive experience."

"Second the speculation must offer the potential for extraordinary rewards. This is an aspect of most forms of gambling, but in this case housing may make this more important. The stereotypical 'crypto bro' is a young man in his twenties, still living at home in his parent’s basement with no conventional prospect of homeownership," says Donovan.

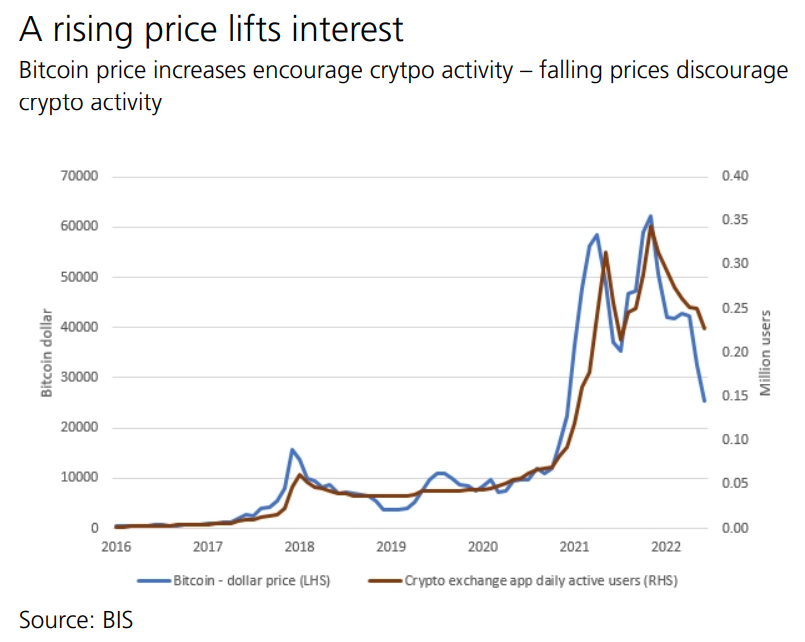

"This sort of person will be attracted to speculation if it holds out the possibility of being able to purchase his own home in the event of the speculation paying off. A belief in being able to get out before the bubble bursts means that as long as prices are rising, more and more people will be attracted to the speculation, as the BIS research has shown in crypto. This is sometimes referred to as the 'greater fool theory' [with] the idea being that the speculator will be able to sell to someone who is a greater fool than they are," says Donovan.

"If the speculation does not pay off, then provided the speculator has not leveraged in order to participate the cost is not so significant. A wannabe homeowner who speculates with their deposit loses not just the money, but the prospect of owning a home if the speculation fails."

"The speculator who does not have a meaningful prospect of buying a home has a smaller loss - they just lose the money they put into the speculation. While loss aversion means that the speculator is not going to be completely indifferent, they are also not going to be so negatively affected. The loss can be characterized as the price paid for the entertainment of the gamble," says Donovan.

He goes on to say that older generations often regard Generation Z, born between 1997 and 2012, and younger Millennials activity in meme stocks and crypto with bewilderment.

"But the disbelief that people would willingly buy crypto or meme stocks comes from a different set of values, values shaped by a realistic aspiration of homeownership. Speculation looks more rational to a generation that will inherit rather than buy property. As long as homeownership is unrealistic, Gen Z and young millennials are likely to keep speculating, although of course the vehicles in which they speculate may change in the future," says Donovan.

"Of more interest, perhaps, is what might happen if housing becomes more affordable in the future. Declining populations and changing patterns of real estate use, e.g. offices converted into apartments, may alter both supply and demand for housing. If that rekindles the homeownership dream for younger generations, the speculation and conspicuous consumption of recent years suddenly acquires a higher cost. Improved housing affordability may end up bursting Gen Z's speculative bubbles."

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

121 Comments

I think it’s a valid conclusion to come to. I also think younger people can see that physical cash use is near non existent nowadays and feel that some kind of digital currency is the future. I also think the likes of Sharesies have made alternative investments easier than previous generations and along with the smaller investment amounts people find it appealing

Lots of young-uns have never seen a crash and don't really believe it can happen (they're learning fast though).

There's also an element of reckless gambling whether it be on cryptocurrencies, NFT's or stocks. Check out wallstreetbets.

Same applies to residential property investment over the past 15 years. It's just that it has a higher barrier to entry.

But crypto has a drop of 50% pretty much every year.

No one who has been in cryptonfor more than a few months should be surprised.

If a sensible and traditional savings path won't ever get you into home ownership then of course speculation becomes more prevalent. It probably makes sense.

Interesting article. Crypto options also have that slight anti-establishment aura as well.

"anti-disestablishment"

I think you mean "anti-establishment." But somewhat true. BTC started as an alternative to fiat with a different monetary policy.

Thank you J.C. - edited

Well betting on the All Blacks has not worked that well recently.

People have 3 options when they have money; consume, save, or invest. When real rates are negative, people have 2 options, consume or invest.

When young people are priced out of housing, they look to put their money into other assets to try and keep ahead. Young people (and everyone else) are forced to speculate and become traders. Crypto and stocks (Sharesies etc) are accessible and people can get started with small amounts. Crypto and stocks become the savings accounts. Young people have nothing (and everything) to lose by gambling what little money they have.

What you are seeing is the monetisation of assets because the fiat monetary system is BROKEN. Housing, crypto, stocks, have all become the savings vehicles of people who simply want to store the value of their hard earned money.

When the money is broken, everything becomes money. Fix the money, fix the world :)

They can "print' as much FIAT money as they like .....but there will only be 21,000,000 Bitcoin !

Money is based on NOTHING ...was backed by gold to 1971 ....not now ....while they can inflate the debt away....till they can't.

That's when this "system" crashes and the debt can no longer be paid ...."domino effect", as once one party can't pay, neither can the other.

So everyone's broke and then they'll will introduce the CBDC (Central Bank Digital Currency) controlled by each country's government, to the point of where THEY will direct where YOUR money goes ....an example.... you have a mortgage and are behind on your payments, while you have a drinking problem and are spending way more than normal on alcohol monthly, so THEY decide you have had a enough booze for the month and next month put a "limit" on how much you can spend ....but not manually, as your money in the bank will be programmed not to accept a transaction (already codes for each and every product) for purchase of alcohol.

Also Labour party nirvana !! as they could stop YOUR money from being spent, if you happen to disagree with one of their policies (truckers in Canada anybody ???) .....there are just so many examples.....

MORE control of the population.... for whose "benefit" ??? ....ASK YOURSELF THIS QUESTION

Yep and CBDC will also be programmed to be non compatible with every other Crypto out there so at that point the value of Bitcoin will go to zero.

Carlos. No.

Missing the point Carlos67 ......have you ever thought you could pay someone else in BTC or a similar cryptocurrency ie Monero .....bypassing CBDC's totally.

Tell us you know nothing about crypto, without saying it.

Tell us you have read a heap of crypto sales pitches without saying it.

21 million Bitcoins x 100 million (Satoshis). Do we then start dividing Satoshis into 100 million pieces? Or is there a limit to how many times Bitcoin can be divided down?

Even then, there is a limit of 2.1 quadrillion Satoshis if I'm not mistaken? How does that compare to Money?

Further divisibility can be added pretty easily if needed, it could be done by a soft fork.

Ok, there are 21m Bitcoins (by modifying the protocol more could be created - it's just software after all).

However, the minimal transaction unit with Bitcoin gets smaller and smaller. Irrespective of how many fiat dollars you print, your minimal transaction unit is 1 cent. With Bitcoin one guy famously paid 10,000 btc for a pizza in 2008, last year it was 0.0001 btc and maybe in the future it will be 0.0000001btc. By printing fiat, infinity is created before the decimal point, with Bitcoin it's created after the decimal point.

Difference in outcome? Anyone paid in Bitcoin will get fewer and fewer Bitcoins every year, anyone paid in fiat will get more and more. But in terms of purchasing power, things remain unchanged. The only ones who really win in crypto are the early adopters who stashed away thousands of Bitcoins before 2010.

Besides: there are now more cryptocurrencies than fiat ones, most of them in nearly endless supply. There's plenty of "printing" going on in the crypto space.

As a technology and and investment is probably appeals to the more digitally aware, aka the younger generations.

Also of note Crypto started as anti monetary statement after the financial manipulations that created the GFC. Many younger people probably look at the "status quo" of the Central Bank world and question the true nature of their role in the world. All before questions of the stupidity of non asset back FIAT speculation that is seen everywhere, and locally in housing in NZ.

Not just the young. I'm 60 and renting again, and have certainly made minor speculations on crypto out of desperation.

Sorry there ain't no get rich quick scheme any more. Except perhaps ram raiding.

I think it is more than just homeownership. It is the entire whole of life costs that are the issue (nod to PDK as it is the resource crunch starting to hit)

Run the maths and you realise the work hard and save route will not see you retiring early, or even at all. In fact you probably won't be able to afford kids, utilities, food, clothes.... within 20 years.

The only way to not be a wage slave until death is to take some risks (Read gambles) and hope they pay off. In the old days you bought a lotto ticket, but $1m is chump change these days.

You also have the problem whereby everyone else is doing the same, so you have to take on even riskier strategies than your peers if you want to get ahead (read survive)

"................ if you want to get ahead (read survive)"

is there a right for everyone to have the access to a get rich quick scheme?

Time was when there was gold in them there hills. Or marry for money. Or art. Roll the dice....

Well back in the day you had more options. See what happens these days if you just go our digging for gold, drilling for oil, run a few cows on some public land, or claiming some random island.

This is true but it is also an incredibly negative social arrangement, with huge negative consequences for families in future.

Houses need to fall 60% from Peak Prices in Real terms to render it reasonable for people to buy again.

Did the boomers have the same excuse in 1986-87 when mortgage interest rates went to 20% and they all piled into the share market? It ended the same way. With about the same level of dodge as anything SBF could have dreamed up.

Interesting, I never associated the high interest rates with the share boom but I guess they would have been related.

Even if you had a first home then investment properties would have been unattractive as prices weren't sure to rise and interest was high.

I guess every generation has it's deer antlers, or llamas, or pine trees, or whatever.

Remember when it was Ostriches?

What's that old saying, in a goldmine, sell shovels?

If everyone's talking about making money off the hot new thing, usually they're the customer for some grade A snake oil.

How many of them piled into South Canterbury Finance?

Interest rates may have been high for a short period, but the average house was only around 50k.

No, the sharemarket was deregulated at that time and all the boomers were into get rich quick as well. With great productive companies such as Equitycorp and Brierley investments what could go wrong.

Yes however the average house cost 3x one persons average salary, therefore 20% interest was still manageable as over time the expectation was that the interest rates would lower again and wages would rise across the lifespan of an individual, therefore it was seen as viable to have children and a house.

Today we are looking at 8x DTI or more and this is 8x dual income of a couple, and while interest rates may lower, we have far less resources to use compared to 35years ago

In New Zealand crypto is not a every day thing for youth, most are struggling to survive going to university just sets them up with huge student loans and many are just unable to stay in further education. When anyone over 40 was younger if we had a good job we could get a mortgage with higher rates than today but how can the youth today have any hope when 700k might get them a small 2 bedroom place in Auckland that if they have managed to save for a deposit. The crime we see today will get worse unless things change.

In New Zealand crypto is not a every day thing for youth.....

Yes and no. But generally I agree. But for diffferent reasons: NZ lacks a well-functioning crypto trading infrastructure. Sure, you can oboard fiat via Easycrypto and then set up accounts on FTX and Binance. However, even getting to those two required a level of commitment from the newcomer.

Why isn’t there a platform then? Probably not worth it due to limited demand, then circle back to initial comment for why theres not much demand.

Why isn’t there a platform then? Probably not worth it due to limited demand, then circle back to initial comment for why theres not much demand.

NZ does not have sophisticated trading platforms with large mkt depth and volume so nudged towards using unregulated exchanges like Binance and FTX. Personally, I don't see that as an issue as long as people accept individual responsibility.

Why does a digital currency need a geographically centric trading apparatus?

Sound plausible but my reasoning is more cynical. As the get rich quick Ponzi scheme called the housing market became inaccessible some of the younger generation moved onto the next well marketed option called crypto. Crypto just played out much faster.

I think it's the same motivation to get ahead. Working does not do it, so any of these "investments" that look to getting people ahead become very attractive for those who are not smart enough to do real investing. (That house that you spent your life paying off you bought for >7-10 times income might revert to it's historical average by the time your done)

its possibly one part of the equation --- another is the get rich quick mentality --- the short out to life -- invent and app and retire --- the you can have it all mentality -- but certainly part of it is the inaccessibility of a deposit openeing young peoples eyes to a much wider array of alternative investments.

Given that much is written about how having all our eggs in the one Housing Basket -- has caused much of the house price challenges --- perhaps the diversity should be welcomed and applauded ?

Anecdotally I know of a couple of people in our company who are buying into tech stocks (Nvidia) and crypto, their main goal to accumulate a house deposit.

Bitcoin is an excellent way to save

/s

Bitcoin is an excellent way to save

Agreed. Or I would say BTC is a good way to save. Rule of thumb: 4-5 years seems to be minimum time needed to make it worth your while. Otherwise you're just gambing.

Either way you are gambling. Its like investing all your money in a single tech stock and hoping that technology pays off.

Investing in a diversified portfolio of stocks that have a current intrinsic value would be much less of a gamble.

Either way you are gambling. Its like investing all your money in a single tech stock and hoping that technology pays off.

Nobody said that you should be "all in" on a single asset class. But if you're going to be "all in", the bets on BTC and crypto are as assymetrical as you will ever see.

Nope the people that made it big got in early and got out a year ago when it peaked.

People who got in early have already seen one or two of these somewhat predictable boom/bust cycles. If they didn't sell in early 2018 or 2013/14 then I doubt they sold 2021. Speaking from experience.

Nope the people that made it big got in early and got out a year ago when it peaked.

65% of circulating supply of BTC has not moved in the past 12 months. 23% has not moved in the past 5 years.

It seems you do not understand how BTC markets work. Most people who "got in early" represent a tiny proportion of owners and there are strong indicators that they have either left the markets or are holding for dear life.

They might represent a tiny portion of individual owners but they represent the lions share of the ownership of crypto.

If you charted the ownership structure using a simple heirarchical order from most to least held, you'll find it looks remarkably like a triangle.

So just for claritys sake, how do you know that 23% that hasn't moved in 5 years is still in circulation, and not lost/stranded/abandoned?

So just for claritys sake, how do you know that 23% that hasn't moved in 5 years is still in circulation, and not lost/stranded/abandoned?

Good question. I don't know what proportion are lost.

Bitcoin is an excellent way to save

Can you please explain why? IMO owning a house and having a mortgage is a better way to save because you have to pay your P&I every month until you own a $million house, mortgage free.

Housing is subject to market fluctuations as much as the next asset. Im picking owning housing will be shunned by future generations, effectively cutting your wealth from under you, if thats how you see housing - wealth.

I dont have a horse in either race, but I think crypto is the classic sticking it to the man, with out the sex drugs and rock n roll. Although it appears to have longer legs than Hendrix.

I think land is an excellent way to save too. The major disadvantage that Bitcoin has is that it doesn’t earn a yield. And banks won’t lend as much to buy it. A minor mitigating factor is that it doesn’t incur rates or maintenance costs, and can never incur a forced annual property tax. If you can stomach the volatility, the return on investment is excellent in the long run.

Regarding your P&I point - Nothing to stop you paying off your Bitcoin in the same way you would a house.

This still doesn't explain why or how Bitcoin is an excellent way to save...

It is a good question.

This is my answer.

It was not designed to save, or to invest. It was designed to provide a way to exchange a fungible asset in a fully decentralized way.

The reliability of the system does not have equals (not in the crypto space and not in the fiat).

Nobody can take them from you unless they have your private key.

Houses can burn, bank accounts can be blocked, every registered asset can be confiscated. Btc, as long as you keep it in your private wallet, is safe.

Is more fungible than gold or cash, in a sense, because you don't have to declare at the airport or hide it somewhere.

On the flip side of that. If you lose your private wallet, who do you call? If you die tomorrow, can your family access it?

It's not that hard to write down 12 words and not lose them.

It's not that hard to write down 12 words and not lose them.

Is that your 12 words ?

It is an excellent way to save due to its characteristics of durability, portability, divisibility, fungibility, scarcity and likely long term return on investment.

House prices are a factor, if they could afford a house then they may have bought one and not had any money to gamble. Although I didn't even think about buying a house until age 30 so for many it wouldn't be a factor.

I would say the biggest factor is not having learnt the valuable life lessons yet. Every generation needs to go through (or at least witness) something as stupid as Crypto or an inflated share market or tulips etc.

Agree. The 88 share market crash put and entire generation off gambling on the stock market.

Hopefully the impending realestate crash will cure this generation from gambling in realestate.

What's happened to Barfoot & Thompsons results from last week?

I think things maybe so bad they dont want to continue with that sponsored article?

I think you are right on the Money from what I seen last week.

Must have cost them bit for last weeks result to be put out there.

If you read the article last week David/Greg? Said that was it for their reporting till volumes pick up early next year, no point reporting on the tiny holiday season volumes. Same as other years.

Loosen the tinfoil hats.

Yes, of course. Young people need hope in this hopeless country. Hope gets you out of bed in the morning. Crypto can represent that which the old timers took away ... hope.

"hope is a good, may be the best of things, and no good thing ever dies" - Andy Dufresne

Hell No! They have been taught gambling at school! Game Theory has been a staple diet in mainstream education for the past 20 years.

Most everything was taught by the theory of probability which replaced actual reason and logic, and factoids.

This has led to this culture of thinking that crypto is an 'investment' when in fact its gambling! Crypto has no real value. Its a belief system for suckers who want to trade tangible assets mainly borrowed cash to the covert into 'tokens' in a world that has little regulation and you can lose your 'token' in a flash. Aside from actual bitcoin, cryptos hold no value other than beliefs, suckers! Go Hard!

Please explain the difference between the tokens you describe above and the digits in your bank account or the bit of plastic in your wallet with "20" printed on it.

I'll grab the popcorn with extra butter.

Mr Brock Landers ....I think before making any comments about Cryptocurrencies, can you at least do some minimal research.

I wish I had your faith with FIAT currencies, that are so easily "manipulated" and inflated away to nothing.....

Bought some BTC around March 2020 @ $3,000 .......didn't sell....still worth $16,789 as at today.

What would your $3,000 sitting in cash since March 2020 be worth now ? .....rest my case.

What if you bought some BTC around March 2021?

I bought some BTC in March 2021. I also bought some in 2013 and 2017 and so on. I sold it all at much higher prices, but have been buying a bit lately, as low as $15.8k

I doubt you would be telling us if you purchased BTC at 65k. You have to change BTC into currency to spend it in most countries, once the governments around the world start own digital currencies they will run BTC into the ground as you will be able to use this when buying a coffee. BCT will become a relic but not very rare as 21 million out there.

Your comment makes zero sense. You didn't do the minimal research of even reading what I wrote and what it was a reply to.

The point I was making is that fiat is also just worthless tokens.

Worthless tokens backed by the military, police and productivity of the issuing country? Tokens that every single person in the country needs a supply of, to pay their taxes with? Tokens that everyone freely accepts in exchange for goods and services?

All Bitcoin is backed by is its own popularity. In the technology world, that doesn't count for much for long.

Backed by fiat. It's in the name.

Worthless in other words.

FIAT, Fabbrica Italiana di Automobili a Torino, it's all in the name!

Wrong Brock, take a look around you, everything is backing Fiat, houses, cars, business you name it. Everything has a value in fiat, try and buy something without it in the real world.

Yes Mr Brock Landers, with all due respect, your opinion is valid, as both FIAT money and BTC are "worthless" .....however the central banks can dictate the "value" and it's purchasing power, you are holding in you hand with that FIAT dollar, with the rising of interest rates .....INFLATION is the classic tool these central banks have, as it increases costs to nearly all members of the public, meaning they save less, if at all .....except the very rich or major asset holders. While they can "extract" as much cash out of the economy as possible. This is why I am a great believer in central banks and governments to keep their sticky beaks out of the markets .....and let the market find it's true "price point".

So at least with BTC it can go BOTH ways and you can long term "swing trade" - can't do that with FIAT money, as it's value is always going down..... except for "deflation" and that's another story in itself..... and doesn't happen very often.

On that basis I'm holding cash and property for the moment, as I can see some opportunities on the horizon - while my crypto holdings are minimal (<6%) as I have only invested what I can afford to lose.

I guess I'm a gambler then - and an old dude to boot. When I was making almost zero on TDs, I figured I might as well get into crypto and meme stocks (DEX and DRSd respectively). I prefer eth over btc and even at today's price, am up. I got lucky and cashed out BBBY at it's high and did incredibly well.

Goodonya and congrats EdwardD !! .....my biggest mistake was not selling enough crypto around November last year...but overall I still have most of the capital in tact.

Thx. I'm finding it difficult to resist buying buying eth at this price.

Just a correlation honestly, FOMO and ultra low interest rates are more to blame.

Did bailing out the idiot bankers of 2008 (UBS for example) mean we needed a decade of ultra low interest rates from our central banks?

Global debt to GDP is approx 4x. Assume that the long-term average interest rate is 3%. At what rate does GDP have to grow at to maintain an even keel?

In the short to medium term inflating asset prices faster than growth can mimic stability.

Until inflation becomes very bad.

Its the opposite for me. Thanks to crypto I have two very houses and no debt (and a very nice nest egg on top).

But I agree generally on this, its not like the old days when a $50k deposit was enough for a 3 bedroom rental in a blue chip suburb.

On the other hand, I'm happily dollar cost averaging a bit into crypto each day. A small bit mind you. Personally I see that as less risky than plonking down say a $400k deposit along with $800k or so debt for an asset that will be cash flow negative with some unfortunately tax limitations.

I don't know its its "not a passive investment". It absolutely can be if you want

And let's not forget about the young first home buyers who bought 0-2 years ago. They will be feeling more pain than the ones that one some money into dogecoin as a lark

As above to EdwardD ……goodonya and congrats lonewolfnz ! with your crypto investments.

I’m watching XRP very carefully at the moment.....

From WaPo in 2014. Bitcoin's financial network is doomed. Its USD price at the time was $325.

"https://www.washingtonpost.com/news/monkey-cage/wp/2014/12/16/bitcoins-… n

The Washington Post is a running joke though...

It does a very good job making active DC connections allowing Amazon to be free from undue regulatory hurdles.

IMO, owning a house and gambling on crypto have nothing to do with each other whatsoever. The first provides with one of the most basic necessities in life of having a roof over your head and growing a family in the house, the second is a "pure get rich quick scheme", that's why it's taken up mostly by younger people who haven't yet faced the collapse of previous "marvellous new ideas" which 95% of investors, sorry gamblers, don't understand at all.

BITC is not a "pure get rich quick scheme". Never has been. That is why the weak hands are usually washed out.

Doesn't the founder own over a million of them, like 15x more than the next largest holder?

They got very rich, very quick.

But that billionaire who has captured 5% of the wealth of Bitcoin owners would never ever actually sell their bitcoin. They are purely operating for the good of mankind.

Just like Elon, who said he would never sell his Tesla stock.

Pump and dump.

Yep it all just becomes a "Game" for the people at this level. hell what's 3.8 Billion dollars of Tesla stock sales anyway ? Yep they all say they are keeping it, that keeps the price high then they dump it. Its only takes a couple of the top Bitcoin holders to head for the exit and it all over.

What about owning more than one house?

Thats not gambling, its a sure thing, even if you leveraged the mother in laws place to achieve such greatness.

Better BBQ stories.

A sure thing? Tell that to the people invested up the gills who are now facing negative equity AND negative cash flow going into a recession. And the tax man wants his share too.

My Sarcasm was obviously well hidden.

I have a fund in the Bahamas they can safely invest in.

I dont think un-affordable housing is driving crypto...I think its more a case of Im young, lazy and into the get rich quick game by joining the pyramid scheme that is not a pyramid scheme (Gambling )....the problem for crypto currently is most folks actually prefer a cash settlement even if it is via the current banking system...Not sure folk would be too happy being paid in fractions of various crypto at the end of the week....its useless unless it can be converted to dollars via more participants.... Possibly the higher a particular crypto goes the less attractive it is to those on lower incomes/newbies or greedy speculators thus as a new crypto enters the market the pyramid players know its best to be in early (top the pyramid) .. Can crypto knock out cash if theres multiple cryptos ? Good luck to the crypto Egyptians because as sure as the sun comes up sooner or later another pyramid will rise.....Why would someone want to spend tens of thousands of dollars to buy 1 unit when they can just wait for the next crypto to show itself and buy thousands of units for a pittance in the dollar and possibly reap exorbitant returns for a nominal outlay? I find it absurd that regulators have allowed the circus to continue and even entertained crypto as a legitimate activity.

You're so out of touch with what crypto even is and how it works.

Sad

Theres a reason IRD classes Bitcoin as 'property'. At its core it allows us to purchase slices of a limited pie (similar to land on earth) except in this case its the property rights to units of a digital network which happen to also be very easily tradable (liquid property).

So now boomers also conveniently get the blame for the younger generations gambling habits as well… what’s next In the boomer dominoes blame game?

Home ownership can (and has often) take up to a decade or more and need lots of sacrifice to achieve (as many boomers experienced and can attest to).

Many younger ones fail to accept that and bemoan how it’s never been harder.

Newsflash: Achieving first home ownership was never easy for us either and yes took a mountain of sacrifices to get there.

Gambling is a free choice… no one forces you to gamble but you.

Patience is the virtue, 1st home ownership is a marathon not a sprint.

If it took you up to 10 years to buy a house when they were 3 x the median salary then you're doing something wrong. Look, we all make frivolous mistakes when we're young I get it.

I could not agree more. My wife and I bought our first home for $69500 in 1984 after saving for 18 months for a deposit. Paid it off in 1987 and upgraded. Now in our third home bought for $490000 and now worth $3m. It was never hard.

Define "Never Hard". I presume you didn't just sit on your ass every day and actually went to work to pay of that mortgage ? That's what you did back in the day, you got up and went to work and didn't complain about it. Never heard a peep from my Father over his entire lifetime, he traveled to work on a Honda 125 over the harbour bridge whatever the weather to be stuck in a dark engineering factory in noise and grime, he just did it. Just doing a 40 hour week now these days is defined as "Too Hard" by the next generation

There's next generation working as diesel mechanics, in engineering workshops, my 25 year old brother works in a foundry.

But you're right, your father's generation was the silent generation that just got on with it. The Boomers on the other hand, well where do we begin?

If it was never hard why'd ownership rates never bust through about 70%.

Because the boomers made pigs of themselves buying real estate and made it harder for those who are at the bottom of the heap.

That's been the highest historical ownership rate going back decades. So either it's always been clearly hard for some people, or around 1/3 of people never aspire to own a home.

Because in mobile societies that % is about as good as it gets, as at certain times of your life it can be better to rent than own, and that as a % of the total population the older you get, the more likely you are to own.

Because if it was never hard, why would you rush to own a home if there was no FOMO or fear of not being able to do it whenever?

Boomers that really think it is the same today as it was back when they did it are in denial and out of touch.

A relative by marriage sold his house a few years ago to speculate in crypto. Let's just say he can't afford a house now.

Yes and No.

In jurisdictions where housing is much more affordable to own or rent, any occupier has more discretionary income to invest in other asset classes. Depending on your age etc., some of which would have been in crypto regardless.

But Yes, when you live in a country that is deliberately taking the ability to own out of the reach of many, and it is difficult to have any discretionary income to save at all, then if they do have some, in desperation, they look to invest in riskier (although they don't recognize that it is risky), but potentially more rewarding asset classes.

It would also be argued that it was the waste of having savings sit in term deposits due to their lower returns that were also a factor.

100%. Savings and TD are a loss service with inflation + asset rising %s per year.

Houses rose 10-20% a year while savings paid 0.20%, now rates are higher, savings are still far below inflation.

The banks have a part to play in this. They are a biz to make money but are scalping the ability of many to grow wealth in this country

I am 24 and have ditched saving a house for crypto, and yes before some of you assume it's gone badly, it hasn't

I am still up 170% on my average buy in starting early 2020.

Why in god's name would a young person save for a house when savings + TD rates are far below inflation and the average rate a house climbs in a year?

"Saving for a deposit" is the stupidest thing if you are unable to save faster than the required amount of a deposit is climbing which is a large majority of young kiwis unless they are

a. partnered and both working towards a house,

b. on decent incomes, 160k+ before tax combined and

c. are not paying much in rent at the moment or staying with parents.

Even then you are signing yourself up to either a 20x, 10x or 5x leveraged purchase and gambling that house prices will only ever rise in the long term which at the rates it has since boomers bought young, is impossible.

I have had to do the math with some friends that are saving 1k a month for a house deposit. While houses climb 10% a year, that 150k deposit you need is climbing 15k a year, and you're saving 12k, go figure, you've lost already from the start.

That's to buy a 750k property which in most towns and cities is a low low end property.

Yes, housing is becoming a joke for young people and is not worth the effort. Some I know are just giving up and spending their money on nice cars and holidays, some still save and are in denial and some invest in the hope of gaining returns that will give them more asset portfolio or enough to get a house at somepoint.

100% in NZ, young kiwis are driven towards volatile assets that they trust and can understand over property. They 100% would go for property if it wasn't a pipe dream :)

Far worse: the prospect of never owning a safe place to stay means an existential necessity remains unmet. As a result, anxiety disorders, drug abuse and suicides are skyrocketing among younger generations around the world. Needless to say that birth rates are collapsing too when living under the permanent threat of homelessness.

Criminally low interest rates, massive debt burdens and (asset price) inflation driven by boomer greed have left subsequent generations with a bleak future. We'll find ourselves in a series of financial catastrophes and wars in years to come as billions of people are priced out of bare necessities of life.

At least the boomers will still be around to reap the rewards of their greed as their wealth gained on the backs of future generations evaporates in hyperinflation. Good luck in old age.

if it's been so easy to make money speculating and getting rich on property, why haven't you done it yourself? Hyperinflation? Why will there be hyperinflation, there hasn't been any since the Great Depression except in 3rd world countries.

I'm always amazed at people who criticise landlords as being 'rich' or 'greedy' - if it's so easy to make money on property and as a landlord, do it yourself and see how easy it is.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.