Although the number of New Zealanders behind on debt repayments is increasing, it's still behind historic levels, data from credit bureau Centrix shows.

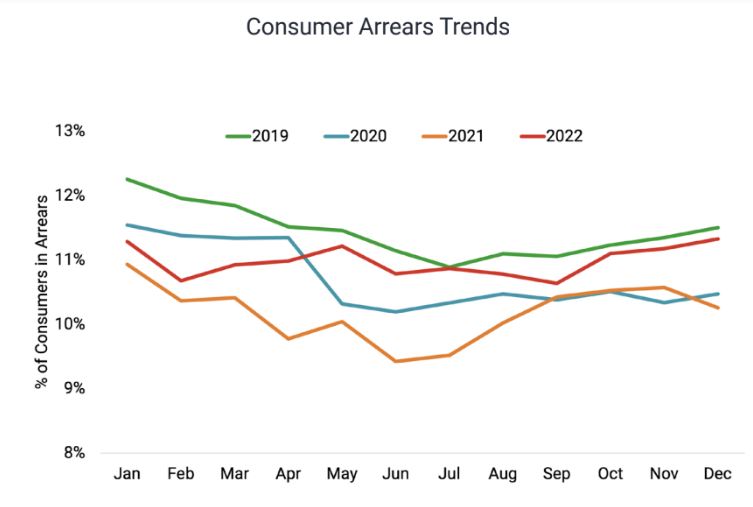

According to Centrix's latest monthly Credit Indicator report, the number of people behind on debt repayments increased to 11.3% of the active credit population, or 410,000 people, in December. That's up from 400,000 in October and is a 10% increase year-on-year as cost of living pressures bite. At 11.3%, it's the highest portion of borrowers since 11.4% in February 2020 just before the Covid-19 pandemic kicked-off and large quantities of public money started sloshing around the economy.

"Although the rise in arrears is concerning, overall arrears rates are still low compared to historic levels," Centrix says.

In terms of regions, it says Gisborne has the highest overall arrears rate at 14.7%, and Northland has the highest proportion of mortgage borrowers past due at 2.4%.

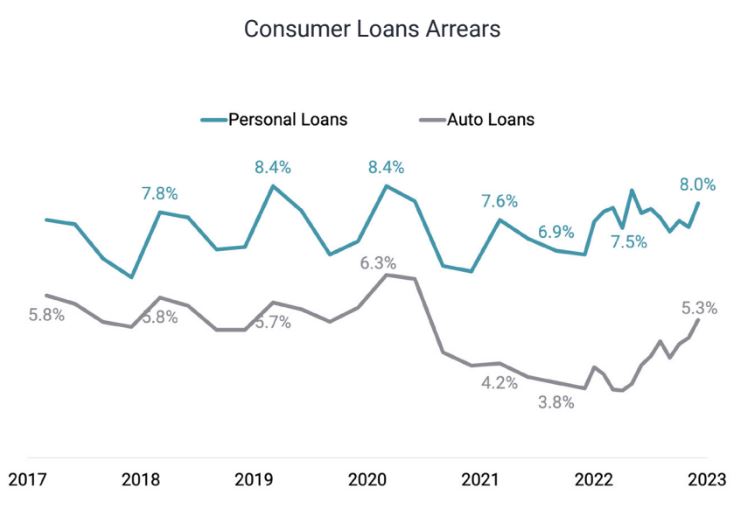

Centrix highlights a rise in car loan arrears as evidence of increasing financial pressure, noting these are usually one of the last credit repayments people let slip.

"As a key indicator of financial pressure, the rise in vehicles arrears is concerning - up 5.3% in December, the highest recorded since June 2020 (6.2%)," Centrix says.

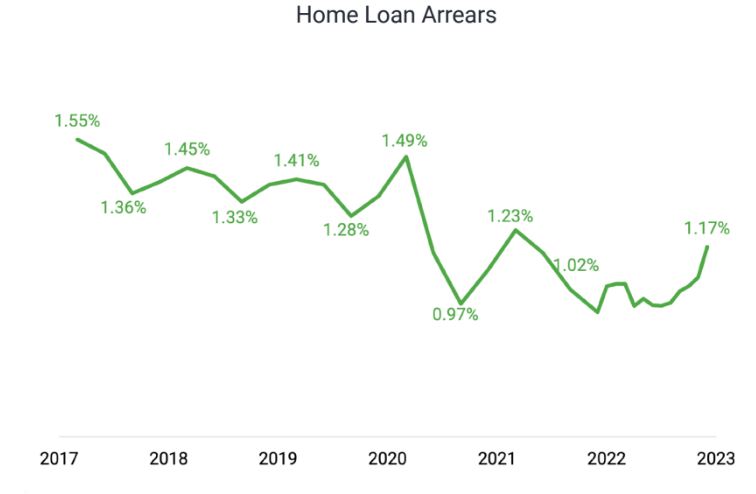

"The number of home loans with missed repayments has also crept up to 1.17% in December, the largest proportion since April 2021 (1.23%). There are currently 17,200 mortgage accounts

past due."

20 Comments

On the business side, my debtor days are pushing out noticeably now. I'd say I've gone from 80% of invoices being paid on time, 15% being paid slow (within 2 weeks past due date) and the last 5% taking much chasing to around 60% being paid on time, 30% being slow and 10% being very behind or potentially unrecoverable.

Was talking to another business owner the other day (who runs a decent-sized firm that sends out a lot of invoices) and he was complaining of the same.

I haven't picked up any change yet, but as a word of advice, if you havent already formed a relationship with a decent collector, get onto that. As much as you want to maintain good relationships with clients, you can't afford turning into a bank for them.

Good advice, thanks.

My lawyer has generally done a good job at recovering slow receivables in the past, and if I look back over the past five or so years in business there's only been a handful of unrecoverable invoices.

But yes I can't afford I become a bank for my clients, and being firm on getting paid on time is going to be a big focus for me this year.

17k houses going for mortgagee sale soon.

Going cheap or free?

Is that an opinion or do you have any evidence for your claim?

Reality starting to hit. Big tax time for businesses on the back of holiday pay at Xmas. Aka a double cash hit. Inflation still far from being suppressed, and that only means one thing on 23rd Feb. Another decent rate increase.

Do the math...before your bank does.

Reality starting to hit. Big tax time for businesses on the back of holiday pay at Xmas. Aka a double cash hit.

This is unlikely to be much of a factor in anything.

Not at all, look at the graphs, I suppose you understand them? Arrears are lower in December 2022, than any time before Covid

So.. The post Xmas peak in all these measures (Except BNPL) are lower than they were in 2019? Sounds like a bit of a nothingburger then.

Nice to see someone able to read graphs properly, and come to their own conclusion, rather than msm hype.

Yeah, i must be behind on my doom and gloom pills. Maybe i'll have a Pils to compensate.

I find this information only partly useful. Number of days, weeks or months behind would improve in getting a better picture of the arrears situation.

Tick...tock...

...Plop - goes the housing market

The graphs clearly show there isn't a problem (maybe yet). The consumer arrears are lower throughout 2022 compared to pre Covid 2019.

Home loan arrears at 1.17% are lower now, than any time before Covid, range 1.28%-1.55%.

Same for auto loans, lower arrears in Dec 2022, than any time before Covid!

yvil maybe add the number of people switching to interest only for a real gauge of what's going on

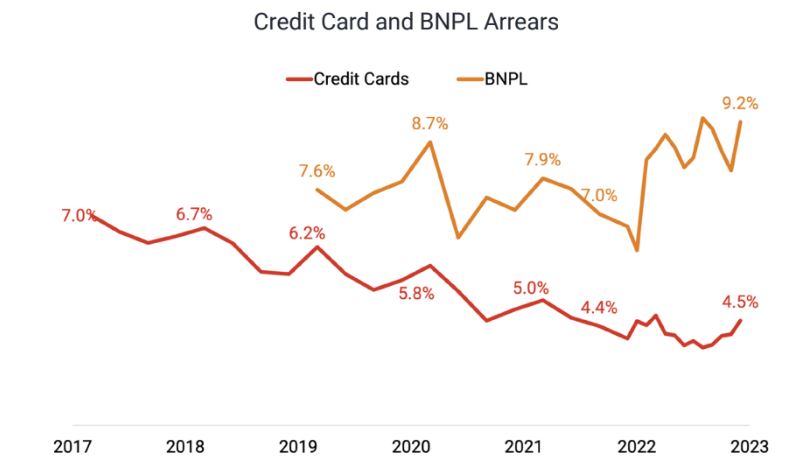

BNPL is the dumbest of all debt and where the trouble is now starting to show.

The Centrix data will be extremely interesting in the coming months.

Worth remembering that the pre-covid repayments were at significantly lower rates and on significantly lower sums (remember the mantra from Orr and co, ‘spend spend spend everyone - save the economy from recession’!)

This means the potential for these trends to accelerate rapidly is alarmingly real.

It would be nice to create a similar timeframe trend of IRD tax write offs for each year and a trend showing the tax delinquencies for each year. That would provide a more comprehensive debt picture of New Zealand.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.