Retirement Commissioner Jane Wrightson is encouraging financial service providers and others to use a new guide recommending language they can use to removes jargon from words and phrases used for money matters.

Wrightson says Te Ara Ahunga Ora Retirement Commission has worked with the financial sector, including regulators, and tested with ASB customers and high school students, while developing De-jargoning Money over 18 months. It's designed for use by organisations and institutions working in the finance and insurance sectors to use when explaining personal finance on their websites, in documents, on the front line, and in the media.

“It’s critical we focus on standardising industry language, removing jargon, banishing outdated terms, and trying to avoid the many acronyms. We know that many terms are not readily understood by New Zealanders and this is a chance to reshape and demystify our customer and consumer-facing language," says Wrightson.

“While this is not a legally binding document, the more organisations that adopt it, the better off consumers will be.”

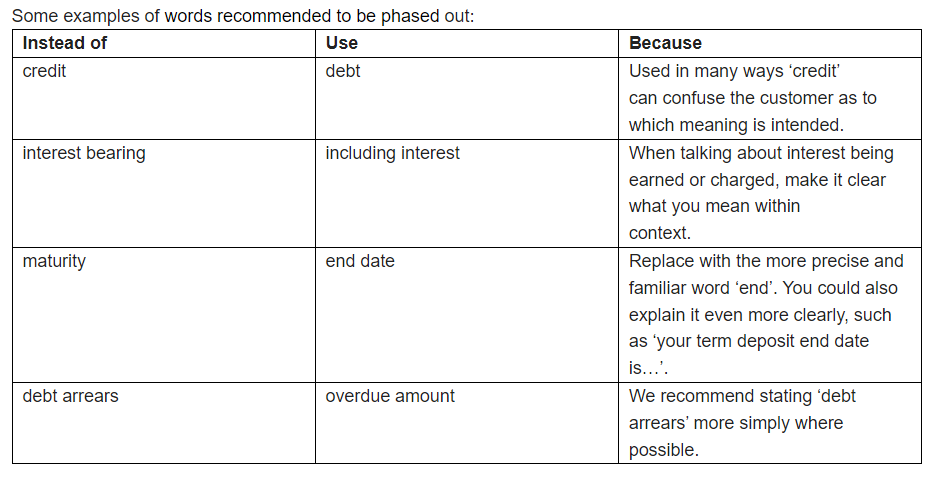

Some examples suggested are using "debt" instead of "credit", "including interest" instead of "interest bearing", "end date" instead of "maturity", and "overdue amount" instead of "debt arrears." (See table below).

The guide offers suggestions for words to be phased out and a plain language term used instead, or Wrightson says where they can't be changed, encourage financial service providers to provide good context for customers. It covers everything from general terms for everyday banking and spending, lending and loans, insurance and estate planning, investment and KiwiSaver to ethical and sustainable investing.

Wrightson suggests using more consistent language and less jargon, could lead to improved financial wellbeing outcomes.

Wrightson says the guide be reviewed every two years with feedback sought from the financial services industry, and updates made reflecting changes in products, language, and regulations.

(The Retirement Commission has also issued a feedback and testing report).

8 Comments

OMG - Why should everything be dumbed down, these terminologies are well established and I believe generally understood by the majority. Perhaps they should better use their time and resources educating people as to what the words already in common usage mean. This country is going to the dogs on so many, many levels now.

*Shrug* If it helps people better understand finance then what's the issue?

While those terms are frequently used in finance, are they actually correct in the context of the borrower? Or even correct terms in general?

If I'm in debt, I'm not in credit am I? And what does "maturity" have to do with the end date of my loan? Maturity is at best "bond speak", but how many 30 year mortgages are backed by a 30 year bond?

We are all retarded because the system is so dumbed down already as a PAYG employee you can claim almost nothing against tax.

Actually a good one would be "Saving" instead of "buy cigarettes"

It is interesting that end date is considered more precise than maturity. I would imagine that an automatically rolled over fixed deposit with an end date could cause some confusion!

Just wait for the "Millennial Edition" to come out ;)

This is just market speak. Leave the Words and Phrases as they are. Both mean exactly the same

What a great idea to call the credit card a debt card, as this is what it is. It might help to deter users from swiping it willy-nilly.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.